Is a Fixed Annuity the Right Home for Your Cash?

Fixed annuity rates look attractive right now, but the real cost of a MYGA shows up if you cash out before 59½. Here’s how they actually work.

In This Article

If your CD is maturing and the renewal rate disappoints, a fixed annuity is likely on your shortlist of safe places to move the money. This guide speaks to three readers: the saver weighing a fixed annuity against a CD or Treasury before committing a lump sum, the pre-retiree wanting a guaranteed rate without market risk, and anyone uneasy about handing a large balance to an insurer. Each gets a straight answer — current rates and what moves them, the real cost of early access, and what protects your principal if the insurer fails.

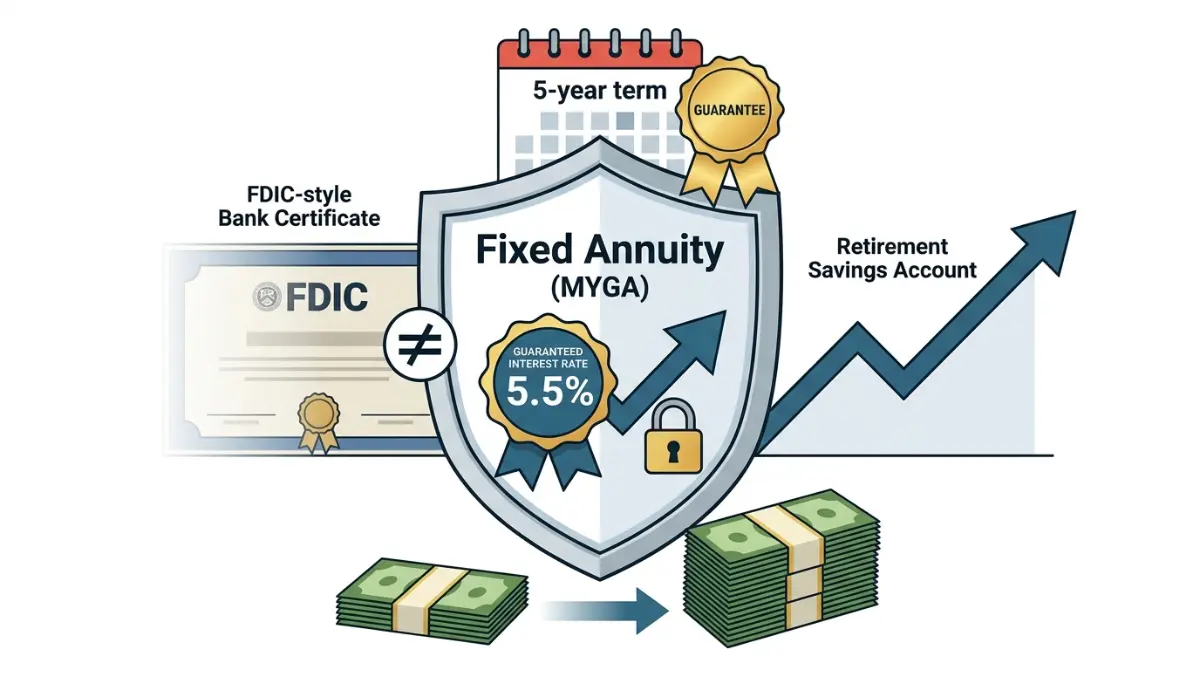

A fixed annuity, sold today mainly as a multi-year guaranteed annuity (MYGA), locks one interest rate for a fixed term. It works like a CD from an insurer, except your interest grows tax-deferred until you withdraw. Our overview of how annuities work across every type maps where MYGAs fit.

ℹ️ Financial Disclaimer: This is general educational information about annuities, taxes, and related products — not personalized investment, tax, insurance, or legal advice. Rates, surrender terms, and tax treatment vary by carrier, state, age, and deposit and change often. Before you buy, exchange, or withdraw, consult a fiduciary financial advisor and a CPA.

How a fixed annuity (MYGA) actually works

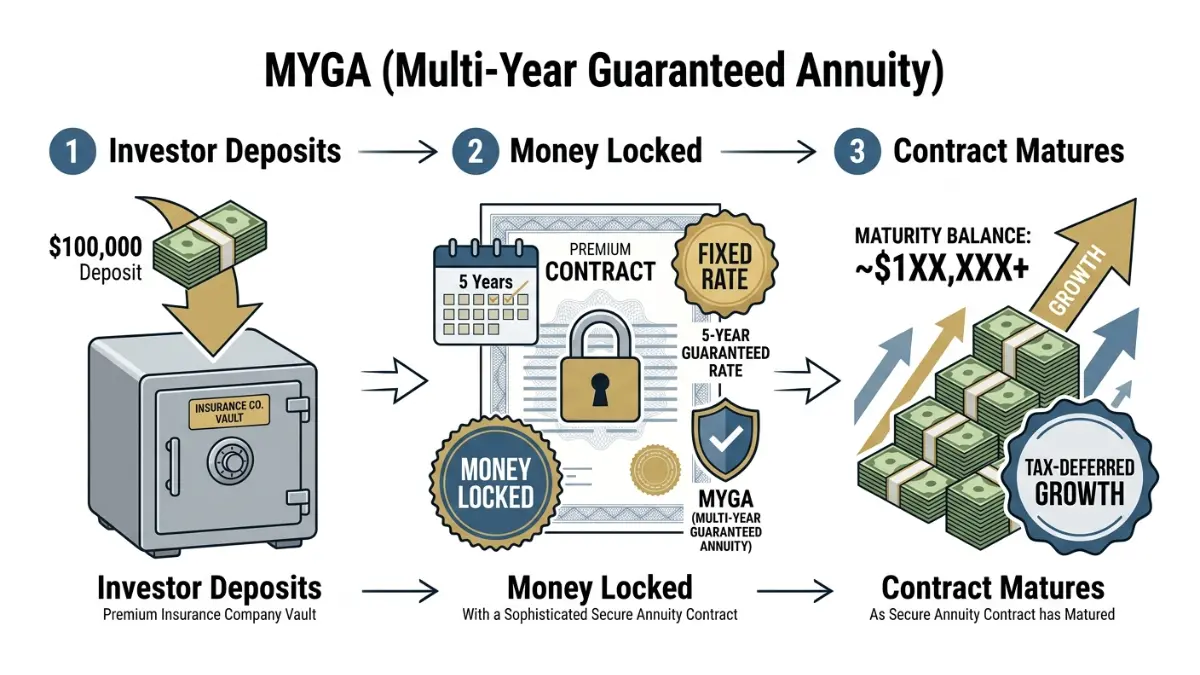

A fixed annuity works in three steps: you give an insurer a lump sum, the insurer guarantees a fixed rate for a set term — usually three to ten years — and your balance grows tax-deferred until you take it out. That guaranteed-rate version is a multi-year guaranteed annuity, the type most buyers mean by “fixed annuity.”

The guarantee and the term

The rate is contractual, not a teaser — whatever the insurer quotes holds for the full term regardless of markets. Term length is the trade-off: longer terms usually pay more but lock your money up longer.

Accumulation versus payout

During the accumulation phase, your money compounds at the guaranteed rate. At term’s end you withdraw, renew, exchange, or convert to income (the payout phase). Most buyers never annuitize; they treat the contract as tax-deferred savings.

🔍 How It Works: Tax deferral means your interest isn’t taxed in the year you earn it — it compounds inside the contract, and you owe ordinary income tax only on withdrawal, unlike a CD’s yearly-taxed interest.

Variable and indexed annuities tie returns to markets; a MYGA does not. Our breakdown of the main types of annuities compares them.

Fixed annuity rates right now — and what moves them

As of June 2026, top-rated insurers offer fixed annuity rates of roughly 5.00% to 5.75%, with five-year terms generally paying the most; some lower-rated carriers advertise up to about 6.30%. Rates change daily, so treat any figure as a starting point to confirm with a live quote.

Why rates sit where they do

Annuity rates track the broader rate environment. The Federal Reserve held its federal funds rate at a target range of 3.50% to 3.75% at its late-April 2026 meeting, with the next decision due in mid-June, per the Federal Reserve’s April 2026 rate decision. When the Fed holds rates higher, insurers can fund richer guarantees; when it cuts, new annuity rates drift down.

What the rate means in dollars

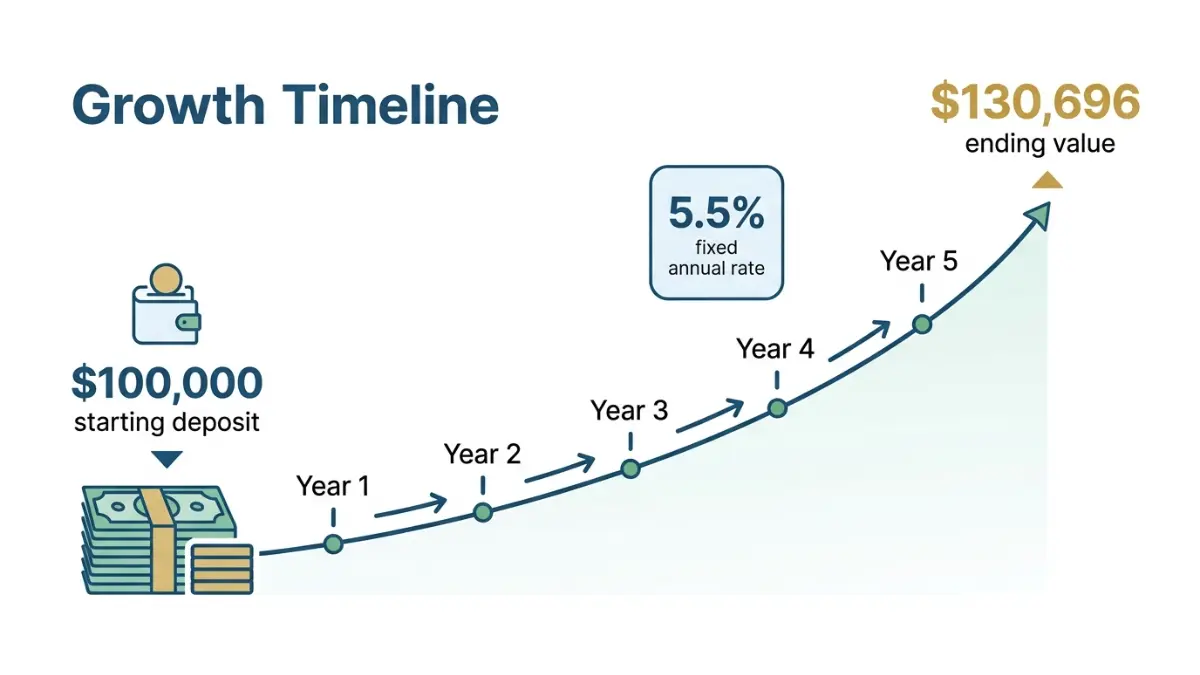

Put $100,000 into a five-year MYGA at an illustrative 5.50% — inside today’s A-rated range — and compound it annually.

📊 Data Point: $100,000 compounding at 5.50% for five years grows to $130,696 — a $30,696 gain. — Source: FinanceAuthorityHub editorial calculation; rate illustrative, within the 5.00%–5.75% A-rated range (June 2026).

🔍 How It Works: Compounding adds each year’s interest to your balance, so the next year’s interest is figured on a larger number — that is why the five-year total outruns multiplying one year’s interest by five.

Run your own figures with our compound interest calculator, then compare against current high-yield savings and CD rates.

How to buy a fixed annuity in five steps

Buying a fixed annuity takes five steps:

- Set the goal and term. Match the term to when you’ll need the cash, not just the highest rate.

- Compare carriers by financial strength. Check the A.M. Best rating — a measure of claims-paying ability — not just the headline rate, since a MYGA is only as safe as its insurer.

- Check your state guaranty limit. Most states protect up to $250,000 in present value per owner, per insurer; if your deposit is larger, split it across carriers.

- Confirm the terms in writing. Get the rate, the surrender schedule, and any penalty-free withdrawal allowance on paper before signing.

- Fund the contract. Move money directly — from a bank account, a maturing CD, or another annuity through a tax-free exchange.

Once you grasp how annuities work mechanically, the rest is mostly paperwork. The SEC’s investor guide to annuities is a useful neutral checklist while you compare offers.

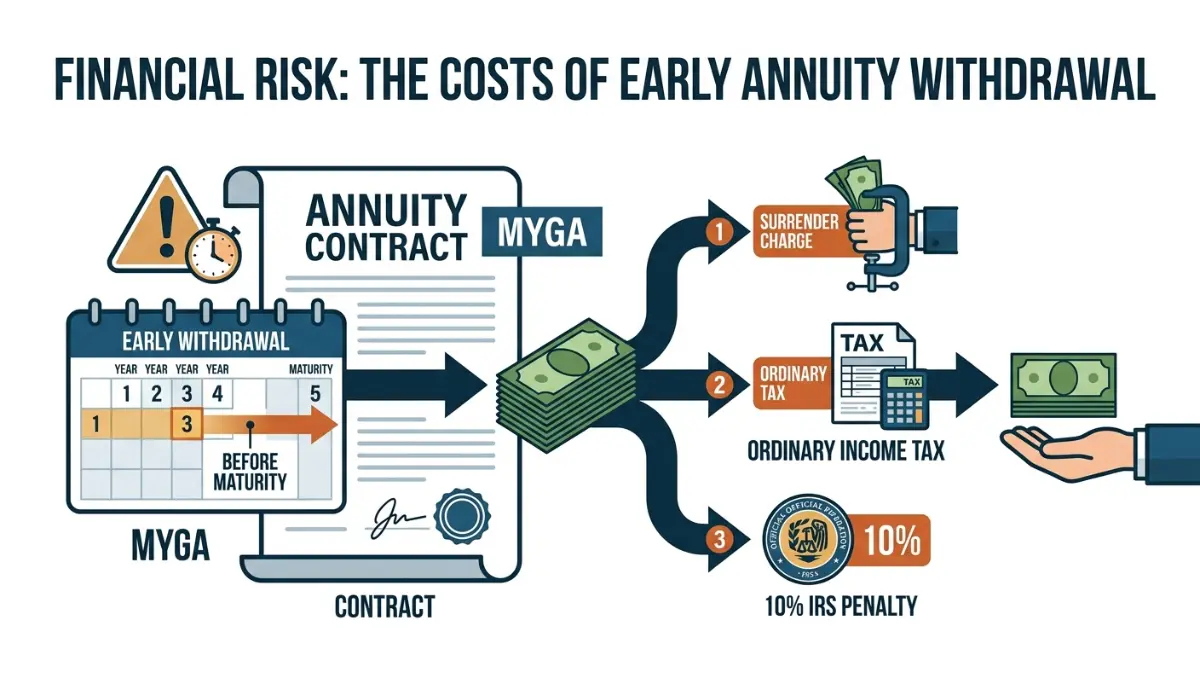

Surrender charges, taxes, and the real cost of early access

Your money is committed for the term, and getting it out early triggers two separate costs buyers often confuse.

Surrender charges and the surrender period

The first cost comes from the insurer. Surrender charges typically start around 5% to 10% of contract value and decline each year to zero by the surrender period’s end, which often matches the term.

Your penalty-free withdrawal allowance

Most contracts let you withdraw a slice each year — commonly around 10% of the value — without a surrender charge, though that cushion does not exempt you from taxes or IRS penalties.

The 10% IRS penalty and how gains are taxed

The second cost comes from the IRS. Withdraw before age 59½ and the earnings portion generally faces a 10% early withdrawal penalty on top of ordinary income tax, per the IRS rules on pension and annuity income. Exceptions include death, disability, or substantially equal periodic payments.

🔍 How It Works: With a non-qualified annuity, the IRS uses “last in, first out” accounting — withdrawals count as earnings first, principal second, so early withdrawals are taxed as ordinary income before you reach your already-taxed deposit.

⚠️ Costly Mistake: Treating a MYGA like a savings account. Pull money during the surrender period and before 59½, and you can stack a surrender charge, a 10% IRS penalty, and ordinary income tax on one withdrawal.

Before locking in a multi-year term, make sure accessible cash covers near-term needs — our savings calculator helps size that cushion.

✅ Action Step: Before any early withdrawal, ask a CPA: “Given my age and whether this annuity is qualified or non-qualified, exactly what tax and penalty would a withdrawal trigger for me?”

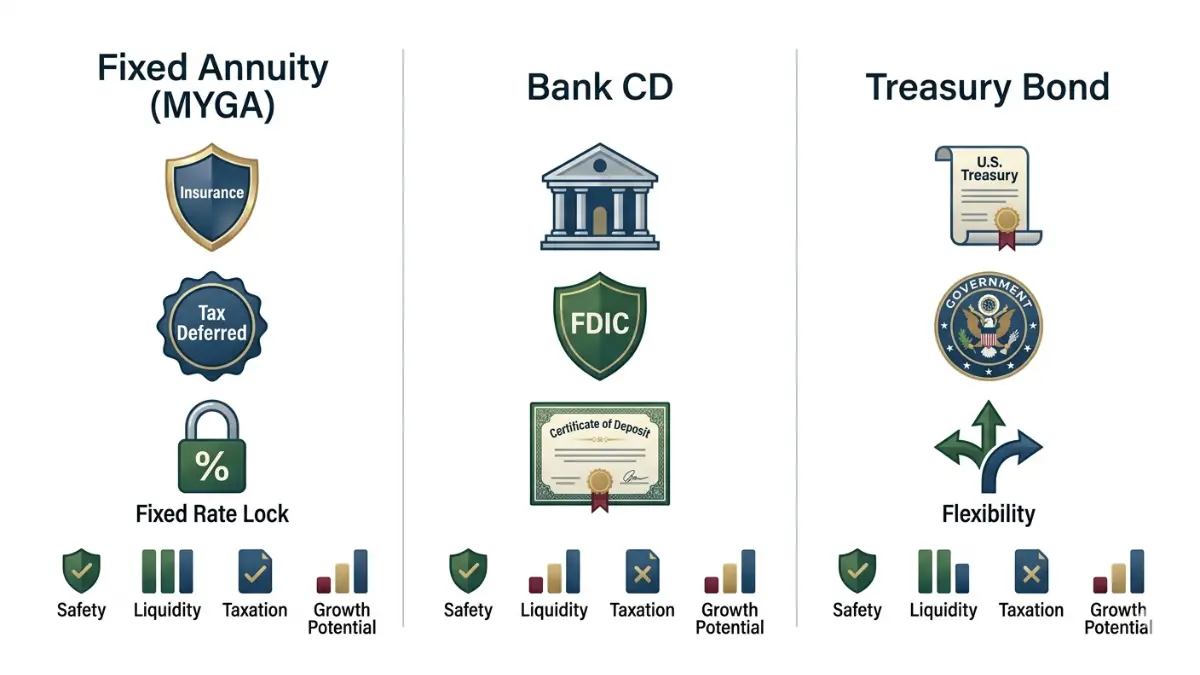

Fixed annuity vs. CD vs. bond — which fits you

A CD is a bank deposit insured by the FDIC, a Treasury is a government IOU, and a fixed annuity is an insurance contract that adds tax deferral but commits your money longer.

| Option | Backing | Tax Treatment | Liquidity | Best For |

|---|---|---|---|---|

| Fixed annuity (MYGA) | Insurer + state guaranty backstop (~$250k present value, per owner per insurer); not FDIC-insured | Tax-deferred; ordinary income on withdrawal | Surrender charge + 10% IRS penalty before 59½ | Tax-deferred growth on cash you won’t need for 3–10 years |

| Bank CD | FDIC, $250k per depositor per bank | Taxed yearly | Early-withdrawal interest penalty | Insured savings on shorter terms |

| Treasury bill / note | Full faith of the U.S. government | Taxed yearly; state-tax exempt | Sell on the secondary market anytime | Maximum safety with flexibility |

Sources: NOLHGA / NAIC Model Act #520 (guaranty limit); FDIC (deposit insurance); IRS Publication 575 (annuity tax); carrier rate aggregators, June 2026.

How the safety net differs

A fixed annuity is not FDIC-insured — it is backed by the insurer’s financial strength and, as a backstop, your state guaranty association. FINRA notes that an annuity’s guarantee lasts only as long as the issuing insurer stays solvent, per FINRA’s investor guidance on annuities.

A simple way to decide

If you want tax-deferred growth and won’t touch the cash for years, a MYGA fits; if you need liquidity or federal insurance, a CD or a Treasury bill may serve better. Compare a MYGA against what a CD would earn over the same term; for income instead of a lump sum, our primer on how bonds work covers that path.

✅ Action Step: Ask a fiduciary financial advisor: “Given my time horizon, tax bracket, and need for liquidity, which of these fits my plan — and how much should sit with any one issuer?”

Five mistakes that cost fixed-annuity buyers money

The lessons above turn into five avoidable errors, each quietly expensive at the moment of decision.

- Chasing the top rate from a weak carrier. A higher rate from a lower-rated insurer carries more risk that the guarantee falls back on the guaranty association; weigh the A.M. Best rating alongside the rate.

- Ignoring the guaranty limit. Coverage is roughly $250,000 per owner, per insurer, in most states; more than that with one carrier sits outside the backstop.

- Locking up money you’ll need. A MYGA is not an emergency fund; the surrender charge and 10% IRS penalty before 59½ make early access expensive.

- Assuming the rate renews. At term’s end, the renewal rate can differ sharply from your original — shop or exchange rather than auto-renew.

- Underestimating inflation. A fixed rate is fixed; if prices rise faster, purchasing power erodes. Our inflation calculator shows the effect on a set payment.

💡 Expert Note: FINRA points out that fixed annuity payments usually carry no cost-of-living adjustment, so a long lock-in trades certainty today for less buying power later — a reason to match the term to your horizon rather than reaching for the longest one.

Fixed annuity FAQs

1. What is a fixed annuity in simple terms?

A fixed annuity is a contract with an insurance company paying a guaranteed interest rate for a set term, usually three to ten years. Most are sold as multi-year guaranteed annuities (MYGAs). It works like a CD from an insurer, except your interest grows tax-deferred until you withdraw.

2. Is a MYGA the same as a fixed annuity?

A MYGA is a type of fixed annuity — the most common one sold today. “Fixed annuity” is the broad category for any annuity paying a guaranteed rate; a multi-year guaranteed annuity locks that rate for a specific term, typically three to ten years.

3. What are current fixed annuity rates?

As of June 2026, top A-rated insurers offer fixed annuity rates of roughly 5.00% to 5.75%, with five-year terms generally paying the most; some lower-rated carriers advertise up to about 6.30%. Rates change daily and vary by carrier, state, age, and deposit, so confirm with a live quote.

4. Are fixed annuities FDIC insured?

No. Fixed annuities are not FDIC-insured because they are insurance products, not bank deposits. They are backed by the insurer’s financial strength and, as a backstop, your state guaranty association — which covers roughly $250,000 in present value per owner, per insurer, in most states.

5. What happens if the insurance company fails?

If the insurer becomes insolvent, your state guaranty association steps in, typically covering up to $250,000 in present value per owner, per insurer, in most states. Amounts above that may be recovered as a claim in the liquidation. Splitting large deposits across carriers keeps each contract within coverage.

6. Can I lose money in a fixed annuity?

The guaranteed rate means you won’t lose principal to market swings if you hold to term and stay within coverage limits. You can still lose money by withdrawing early — surrender charges plus a 10% IRS penalty before age 59½ — or to inflation, since a fixed rate does not rise when prices do.

7. How are fixed annuities taxed?

Your interest grows tax-deferred, and you owe ordinary income tax — not lower capital-gains rates — when you withdraw, per IRS Publication 575. For a non-qualified annuity, the IRS treats earnings as withdrawn first. Annuities held inside an IRA or 401(k) follow that account’s rules. Consult a CPA.

8. What’s the penalty for withdrawing early?

Withdraw before age 59½ and the earnings portion generally faces a 10% IRS early-withdrawal penalty on top of ordinary income tax. Separately, the insurer may charge a surrender fee — often 5% to 10% early in the term, declining to zero. Exceptions to the IRS penalty exist, so ask a CPA.

9. Can I get my money out before the term ends?

Usually yes, but with costs. Most contracts allow a penalty-free withdrawal each year — commonly around 10% of the value — while larger early withdrawals trigger surrender charges. If you are under 59½, the 10% IRS penalty also applies to the earnings. Read your surrender schedule.

10. Fixed annuity vs CD — which is better?

Neither is universally better. A CD is FDIC-insured up to $250,000 per depositor and stays liquid sooner; a fixed annuity adds tax deferral and often a higher rate but locks money longer and penalizes early access. Match the choice to your timeline and need for liquidity.

11. What happens when my MYGA term ends?

At maturity you get a short window to choose: withdraw the cash, renew at the insurer’s new rate, move it to another annuity through a tax-free 1035 exchange, or convert it into income. Renewal rates can differ sharply. A 1035 exchange defers taxes but may still incur surrender charges.

The bottom line on fixed annuities

A fixed annuity is a straightforward trade: a guaranteed, tax-deferred rate in exchange for locking your money up for a set term. It fits the saver who wants more than a CD pays, won’t need the cash for years, and values a predictable result over market upside — and fits less well if you might need liquidity soon or want federal insurance.

If a MYGA is on your list, vet the carrier’s strength, confirm your state guaranty limit, and run the numbers against your plan — our retirement calculator shows where a guaranteed slice fits. Then take the contract to a fiduciary advisor and a CPA before you sign.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.