What a Variable Annuity Really Costs You

A variable annuity blends market growth with insurance — but its ~1.25% M&E fee, surrender charges, and 10% early-withdrawal penalty hide the real cost.

In This Article

A variable annuity promises two things at once — market growth and a future income stream — which is exactly why it is one of the hardest retirement products to evaluate honestly. The fees are real, the tax rules are strict, and the sales pitch rarely leads with either.

Where you are right now shapes what you need from this page. If an advisor or insurance agent has just put a contract in front of you, skip ahead to what it actually costs and the questions to ask before you sign. If you are comparing it against a fixed annuity or a regular investment account, the comparison section is built for you. If you already own one and someone is urging you to swap it for a newer contract, the section on costly mistakes covers that exact situation.

Every figure here is tied to the SEC, IRS, or FINRA, and we show the dollar math instead of asserting it. This is general education to help you ask sharper questions — not a recommendation to buy or avoid. For the wider picture, start with how annuities work in general.

ℹ️ Financial Disclaimer: This article is educational and not personalized investment, tax, insurance, or financial advice. Variable annuities are securities sold only by prospectus and carry market risk, including the possible loss of principal. Figures are drawn from the SEC, IRS, and FINRA as of the last-reviewed date and can change; contract terms vary. Before buying, exchanging, or withdrawing from any annuity, consult a fiduciary financial advisor and a CPA or tax professional about your specific situation.

What a variable annuity actually is

A variable annuity is a contract with an insurance company in which your money is invested in market-based subaccounts, so the contract value rises and falls with those investments while growing tax-deferred until you withdraw it. That one feature — market exposure inside an insurance wrapper — is what separates it from a fixed annuity, which credits a set rate.

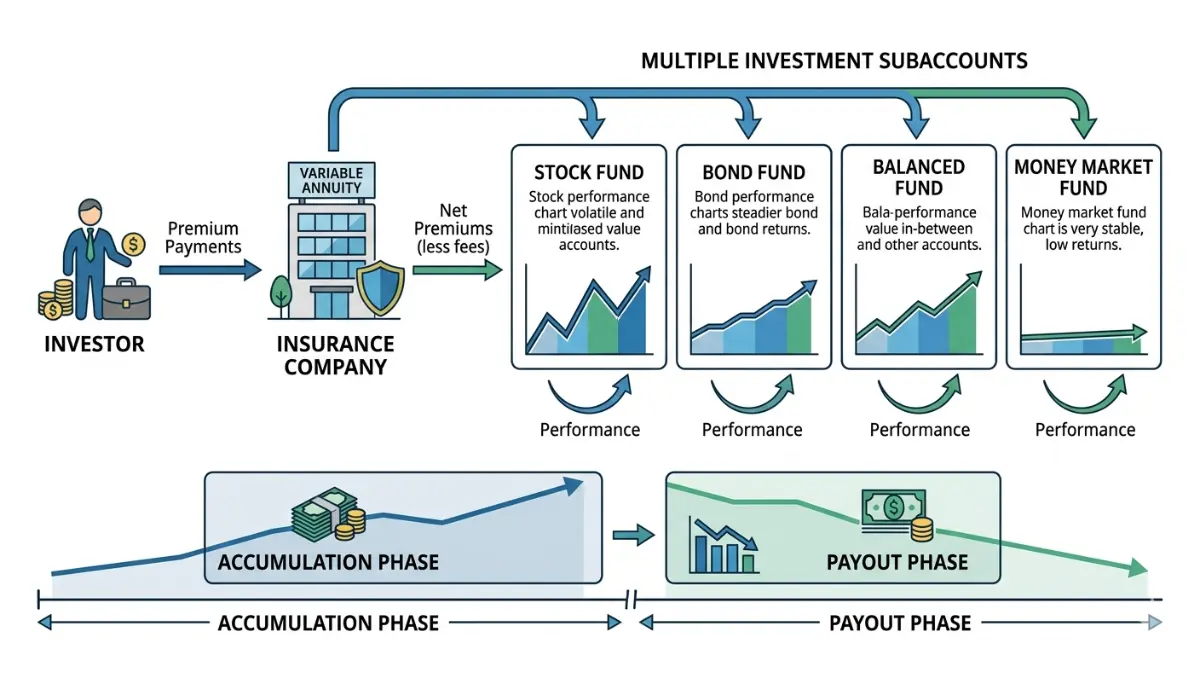

Subaccounts: where your money actually goes

A subaccount works much like a mutual fund held inside the annuity. You pick a mix of stock, bond, and money-market options, and your contract value tracks their performance. Because that performance can be negative, you can lose money, including your original principal, as the SEC’s investor bulletin on variable annuities makes clear.

🔍 How It Works: A variable annuity has two layers. The insurance layer provides features like a death benefit and optional income guarantees; the investment layer is your subaccounts, which behave like funds. You pay for the insurance layer through fees — and those fees are why the product costs more than investing directly.

Accumulation vs. payout phase

During the accumulation phase, your purchase payments grow in the subaccounts. In the payout phase, you can convert the balance into periodic income — a process called annuitization — that can last a set number of years or for the rest of your life. This is the feature marketed as protection against outliving your savings, and it is best understood alongside an annuity’s accumulation and payout phases generally.

The free-look window

After you sign, most contracts give you a short free-look (cancellation) period — often at least 10 days — to back out and get a refund, though the refund may be adjusted up or down for investment performance, per the SEC. A variable annuity is one of the main types of annuities, and it is the only one that puts your principal directly at market risk.

What a variable annuity really costs

A variable annuity carries several stacked fees that compound against your return every year:

- Mortality and expense (M&E) risk charge — typically about 1.25% of account value per year, though some contracts run to 1.65% or higher (SEC).

- Administrative fees — recordkeeping costs, sometimes a flat annual contract charge (commonly around $30–$45 in filed prospectuses).

- Underlying fund expenses — the cost of each subaccount you choose, which varies by fund.

- Surrender charges — a fee for withdrawing early, covered just below.

- Optional rider charges — extra cost for features such as a guaranteed lifetime withdrawal benefit or a stepped-up death benefit (FINRA).

📊 Data Point: The M&E risk charge on a variable annuity typically runs about 1.25% of account value per year — Source: SEC Investor.gov, 2026.

Surrender charges and the surrender period

A surrender charge applies if you withdraw more than a set amount during the early years — the surrender period — which commonly lasts six to eight years and sometimes ten, per the SEC. A typical schedule starts at 7% and steps down each year:

| Contract year | Typical surrender charge | Key detail |

|---|---|---|

| Year 1 | 7% | Highest charge, right after purchase |

| Year 2 | 6% | Most contracts let you take ~10% of value each year charge-free |

| Year 3 | 5% | The 10% free amount comes out before any charge applies |

| Year 4 | 4% | |

| Years 5–6 | 3% → 2% | |

| Years 7–8 | 1% → 0% | Surrender period ends |

Source: the SEC’s investor guide to variable annuities (illustrative schedule; your contract’s prospectus governs the actual numbers).

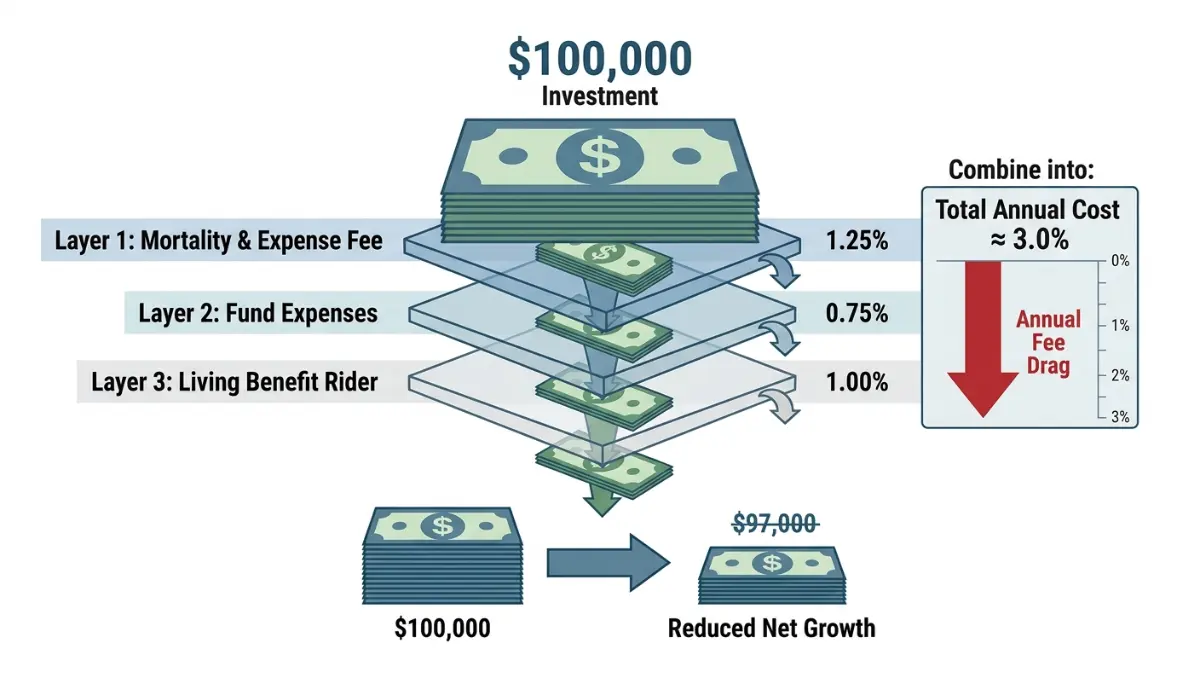

What it adds up to: a worked example

Here is the part the sales illustration rarely totals for you. On a $100,000 contract with a living-benefit rider, a realistic all-in annual cost stacks up like this:

- M&E at ~1.25% → about $1,250

- Underlying fund expenses (assume ~0.75%) → about $750

- Living-benefit rider (assume ~1.00%) → about $1,000

- Total ≈ about $3,000 a year, or roughly 3.0% — before any market loss.

The M&E rate comes from the SEC; the fund-expense and rider figures are assumptions for this example, so your real number depends on your own contract’s fee table. Now the exit cost: surrender that same $100,000 in year one, and the ~10% free amount ($10,000) comes out clean, but a 7% charge on the remaining $90,000 is $6,300 — and if you are under 59½, the taxable portion also faces a 10% IRS penalty, covered next.

✅ Action Step: Request the contract’s prospectus fee table and add every line — M&E, admin, fund expenses, and each rider — to get your true annual cost. Then model how fees compound against your balance over your real time horizon, and run a net-of-fees projection to see what the drag costs you over decades.

How variable annuities are taxed

Variable annuity earnings grow tax-deferred until you take the money out — and then the treatment surprises many buyers. Tax-deferred is not tax-free.

Tax-deferred now, taxed as ordinary income later

While your money stays in the contract, earnings are not taxed. When you withdraw them, the taxable portion is taxed as ordinary income — at your regular income tax rate, not the lower long-term capital gains rate — according to IRS Publication 575, which specifically covers commercial variable annuity contracts.

The 10% penalty before age 59½

Withdraw earnings before age 59½ and you generally owe an extra 10% penalty — a 10% federal additional tax on the taxable amount, on top of ordinary income tax — unless an exception applies, per the IRS rules on the additional tax on early distributions.

🔍 How It Works: For a non-qualified annuity (one bought with after-tax dollars), the IRS treats earnings as coming out first. So an early withdrawal is largely taxable, and on a contract that has grown, much of what you pull out can be hit by both ordinary income tax and the 10% additional tax at the same time.

Withdrawals and inherited annuities

A beneficiary who inherits an annuity generally owes ordinary income tax on the earnings, and unlike inherited stock, the contract does not receive a step-up in cost basis (IRS Publication 575). Because the tax outcome depends on your age, your cost basis, and whether the annuity is qualified or non-qualified, this is a place for specifics rather than rules of thumb.

✅ Action Step: Before taking any withdrawal, ask a CPA or tax professional: “Given my age, my cost basis, and whether this annuity is qualified or non-qualified, how much of this withdrawal is taxable, and will the 10% additional tax apply to me?”

Variable annuity vs. the alternatives

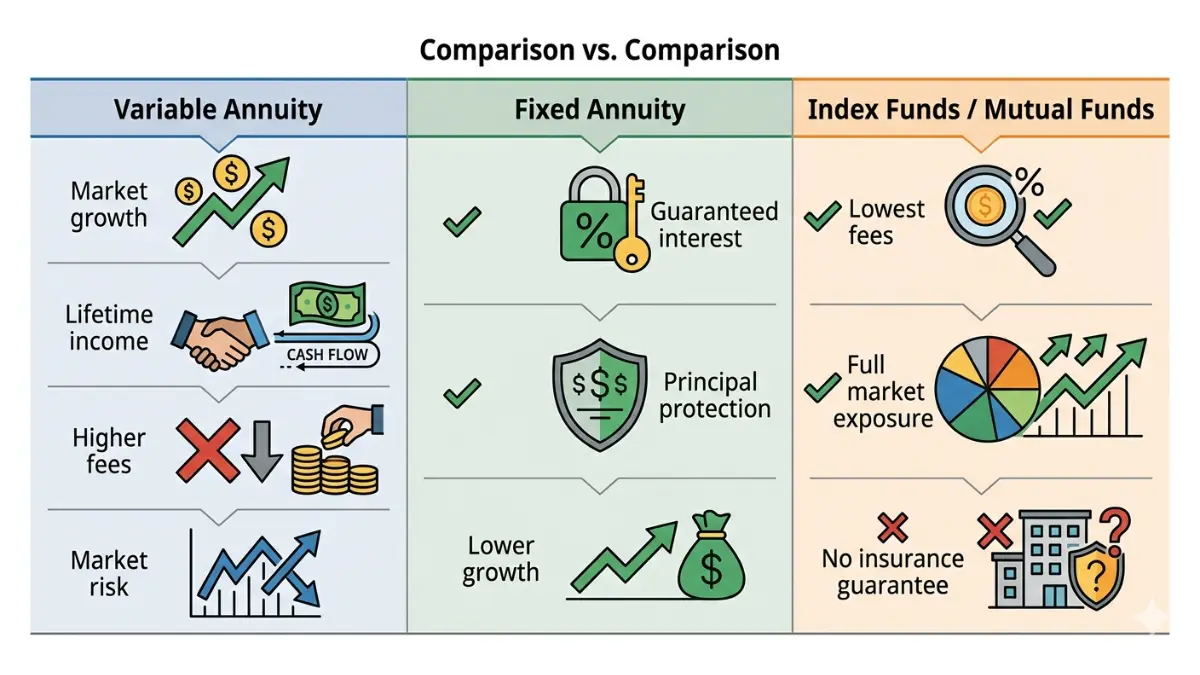

The honest trade-off in one line: a variable annuity gives you market growth potential with market risk, while a fixed annuity gives you a guaranteed rate with a lower ceiling.

Variable vs. fixed annuity

Your variable annuity’s value rises and falls with its subaccounts, so it can earn more than a fixed annuity — or lose value when markets fall, per the SEC and FINRA. A fixed annuity credits a set rate and protects principal, trading upside for predictability.

| Option | Growth | Principal risk | Typical cost | Best for |

|---|---|---|---|---|

| Variable annuity | Market-linked, uncapped | Yes — can lose value | Highest (stacked fees + riders) | Long horizon; wants market upside plus optional lifetime income |

| Fixed annuity | Set credited rate | No (insurer-guaranteed) | Low | Wants predictable, principal-protected growth |

| Index or mutual funds | Market-linked | Yes | Low (fund expenses only) | Wants market exposure at lower cost with full liquidity |

Source: SEC Investor.gov and FINRA (general product features).

Variable annuity vs. investing directly

Holding low-cost index or mutual funds in a brokerage account or IRA gives you similar market exposure at a fraction of the cost — but without the insurance features, so no lifetime-income rider and no death-benefit guarantee. The annuity’s extra fees buy those guarantees; whether they are worth it depends on how much you value them.

Where a variable annuity can fit

It tends to make the most sense for someone with a long time horizon who has already used their lower-cost tax-advantaged accounts, wants market exposure plus an optional income guarantee, and is comfortable paying for it.

💡 Expert Note: FINRA guidance stresses comparing a new annuity’s fees, investment restrictions, and any new surrender period against your current option before exchanging — the features can look similar while the costs differ sharply.

✅ Action Step: Ask a fee-only fiduciary advisor: “Given my retirement timeline, my existing accounts, and my risk tolerance, does a variable annuity beat a fixed annuity or low-cost funds for me — and specifically why?”

Is a variable annuity right for you?

Whether a variable annuity fits comes down to your time horizon, your other accounts, your need for liquidity, and how much you value an income guarantee.

Who a variable annuity may suit

It can suit someone with a long time before they need the money, who has already maxed out a 401(k) or IRA first, wants market exposure with an optional guaranteed-income rider, and can leave the money untouched through the surrender period.

Who should probably look elsewhere

If you might need the cash during the surrender period, you are under 59½ and likely to withdraw, you want the lowest possible fees, or you do not value the insurance features, the costs are hard to justify. Variable annuities suit long-term goals, not short-term needs, and substantial taxes and surrender charges can apply to early withdrawals, per the SEC.

Questions to ask before you buy (or exchange)

Before signing, confirm each of these — they mirror the disclosures FINRA’s investor guidance on annuities expects a representative to make:

- What is the total annual cost — M&E, admin, fund expenses, and every rider — expressed as a single percentage?

- How long is the surrender period, and what is the charge in each year?

- Will a withdrawal before age 59½ trigger the 10% additional tax for me?

- Exactly which guarantees am I paying for with each rider?

- If this is an exchange, does it restart the surrender clock or cost me benefits I already have?

⚠️ Costly Mistake: A variable annuity is not FDIC-insured. Your payments depend on the issuing insurer’s ability to pay, with a state guaranty association as a limited backstop whose coverage caps vary by state — so the insurer’s financial strength matters before you commit.

✅ Action Step: Map your full retirement picture first — see where an annuity fits your retirement plan — before committing a large sum to any single contract.

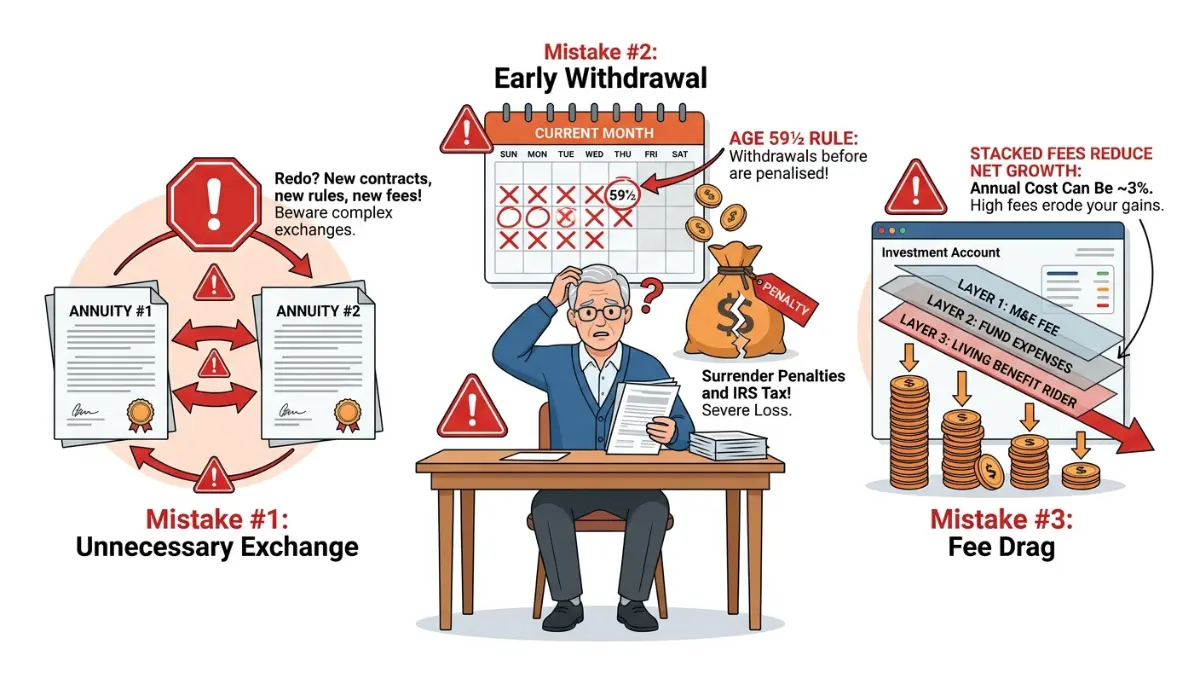

The mistakes that cost variable-annuity buyers the most

Most trouble with a variable annuity starts not with the product but with the details — and the same few mistakes appear again and again.

The unnecessary exchange

Swapping an existing annuity for a newer one can restart the surrender clock and add new charges, and regulators keep finding it done when it should not be. In 2026, FINRA enforcement actions documented customers pushed into more expensive contracts and rider features they did not need, incurring avoidable cost and surrender fees. FINRA’s guidance on annuity exchanges walks through what to compare before agreeing.

Ignoring the surrender clock and the 59½ rule

Withdrawing early can mean paying a surrender charge and the 10% additional tax at the same time, as the earlier example showed. Knowing exactly when your surrender period ends — and whether you will be past 59½ — prevents an expensive surprise.

Underestimating the all-in fee drag

A single rate sounds small; stacked fees of roughly 3% a year are not, and they compound against you whether the market is up or down. That drag is the most underestimated cost in the entire product.

⚠️ Costly Mistake: Judging a variable annuity by its monthly income illustration instead of its total fees and surrender terms is how buyers end up locked into a contract that quietly underperforms a far cheaper alternative.

Variable annuity FAQ

1. What is a variable annuity in simple terms?

A variable annuity is a contract with an insurance company where your money is invested in market-based subaccounts. The value grows tax-deferred but can rise or fall with those investments, and you can later turn it into retirement income. It can lose principal, unlike a fixed annuity.

2. How is a variable annuity different from a fixed annuity?

A variable annuity’s value moves with its subaccounts, so it can earn more but can also lose value. A fixed annuity credits a guaranteed set rate and protects your principal. The variable version offers higher growth potential and higher fees; the fixed version offers predictability.

3. What are the fees on a variable annuity?

Expect several stacked fees: a mortality and expense charge of about 1.25% a year (SEC), administrative fees, underlying fund expenses, surrender charges for early withdrawals, and optional rider charges. Together these can approach roughly 3% annually. Read the prospectus fee table and confirm your total before buying.

4. Can you lose money in a variable annuity?

Yes. Your money sits in market-based subaccounts, and if they perform poorly your contract value falls, including possible loss of principal, according to the SEC. The insurance features and optional riders may offer some guarantees, but the underlying investment itself carries real market risk.

5. How are variable annuities taxed?

Earnings grow tax-deferred and are taxed as ordinary income when withdrawn, not at lower capital gains rates, per IRS Publication 575. Withdrawals before age 59½ generally face an extra 10% federal additional tax on the taxable amount. Consult a CPA about how a withdrawal would be taxed in your situation.

6. What is a surrender charge on a variable annuity?

A surrender charge is a fee for withdrawing more than the allowed free amount during the early years. A typical schedule starts around 7% and declines to 0% over six to eight years, the surrender period, per the SEC. Most contracts let you take about 10% of value each year charge-free.

7. What is the 10% penalty on a variable annuity?

It is a 10% federal additional tax on the taxable portion of withdrawals taken before age 59½, charged on top of ordinary income tax, per the IRS, unless an exception applies. It is meant to discourage early use of retirement money. A CPA can confirm whether any exception fits your case.

8. Are variable annuities a good investment?

It depends on your time horizon and what you value. They can suit a long-horizon investor who has maxed lower-cost retirement accounts and wants an optional income guarantee, but the fees and market risk make them hard to justify for short-term needs or fee-sensitive savers. Ask a fiduciary advisor before deciding.

9. What is a living benefit rider?

A living benefit rider, such as a guaranteed lifetime withdrawal benefit, is an optional add-on that promises a certain income or withdrawal amount regardless of market performance, for an extra annual fee (FINRA). It can reduce the risk of outliving your money, but it raises your total cost, so confirm exactly what it guarantees.

10. Is a variable annuity FDIC-insured?

No. Variable annuities are not FDIC-insured. Payments depend on the issuing insurer’s claims-paying ability, with a state guaranty association as a limited backstop whose coverage caps vary by state. The insurer’s financial strength matters, so check its ratings before committing a large sum.

11. How do I get my money out of a variable annuity?

You can withdraw, but timing matters. During the surrender period, withdrawals above the free amount (often ~10% a year) face a surrender charge, and earnings taken before age 59½ face a 10% additional tax plus ordinary income tax, per the SEC and IRS. Most contracts also allow a short free-look cancellation after purchase.

The bottom line on variable annuities

A variable annuity can deliver real market growth and an optional income stream you cannot outlive — but you pay for both in layered fees of roughly 3% a year and tax rules that treat every gain as ordinary income. Whether that trade is worth it depends on your time horizon, your other accounts, and the specific contract in front of you.

The most useful move is to turn the sales illustration into real numbers: total the fees, map the surrender period, and check how a withdrawal would be taxed for you. Then compare every annuity type side by side and bring specific questions to a fiduciary advisor and a CPA before committing a dollar.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.