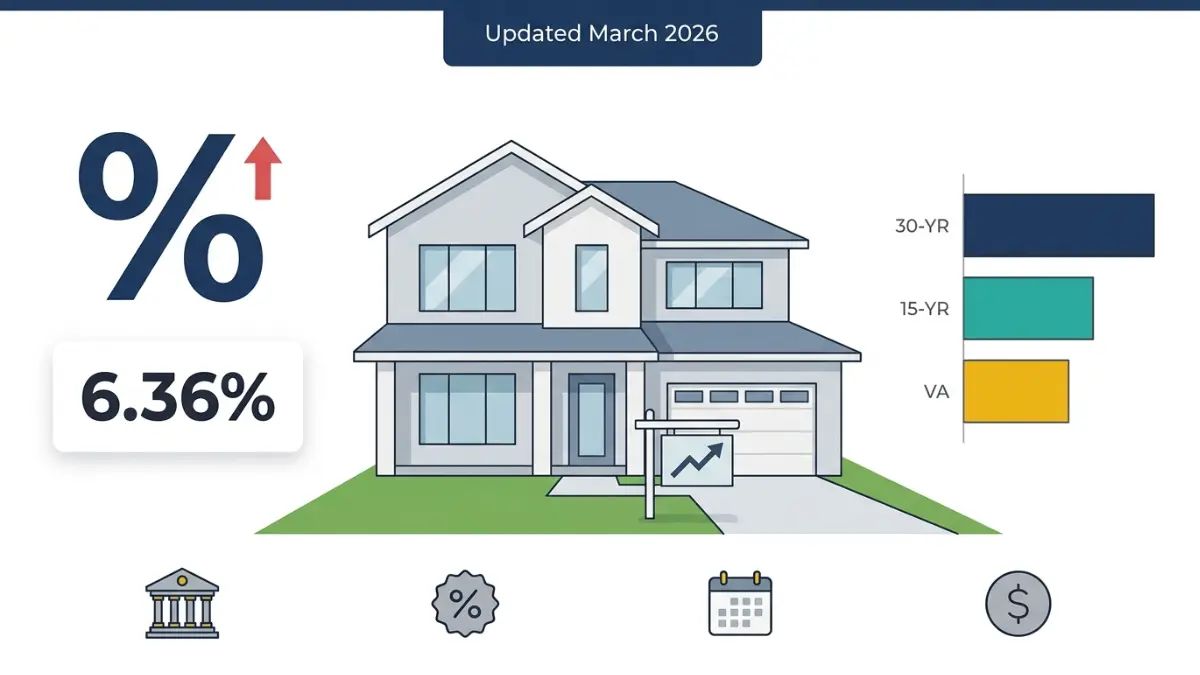

Current Home Loan Interest Rates in the USA — Updated March 2026

Home loan rates just hit a 2026 high of 6.36%. See today’s rates for 30-yr fixed, FHA, VA, USDA & jumbo loans — plus 5 proven ways to lock a lower rate now.

In This Article

Rates just hit a 2026 high. Here’s every loan type, what’s driving the surge, and your 3-step action plan right now.

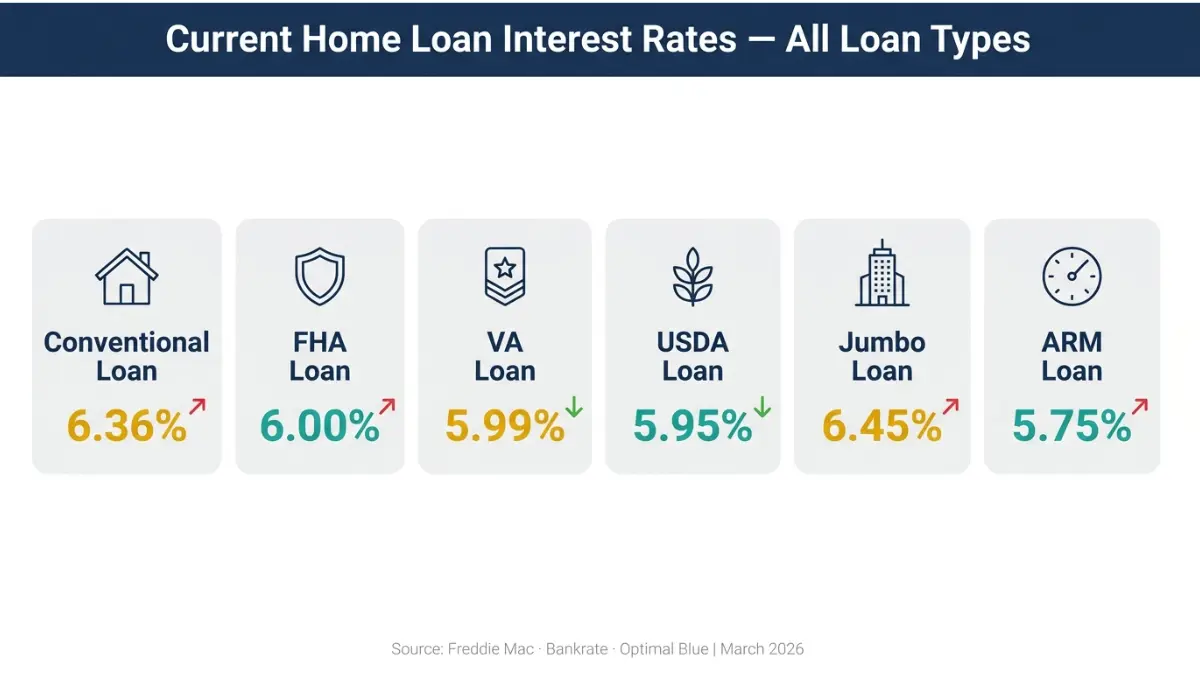

As of March 26, 2026, the average current home loan interest rate for a 30-year fixed mortgage is 6.36%–6.45%, and 5.54%–5.71% for a 15-year fixed loan. VA and USDA loans offer lower rates — currently near 5.99%–6.32%. Rates have risen sharply in March 2026, driven by rising oil prices and geopolitical uncertainty. Here is everything you need to make a smart borrowing decision today.

Today’s Current Home Loan Interest Rates — March 26, 2026

Updated daily. Data sourced from Freddie Mac PMMS, Optimal Blue, and Bankrate (March 24–25, 2026).

Current home loan interest rates across all major loan types are listed below. This is the only table you need — unlike competitors who scatter this data across five separate pages.

| Loan Type | Term | Interest Rate | APR | Week-over-Week |

|---|---|---|---|---|

| Conventional Fixed | 30-Year | ~6.36% | ~6.45% | ▲ +0.11% |

| Conventional Fixed | 15-Year | ~5.71% | ~5.89% | ▲ +0.06% |

| FHA Loan | 30-Year | ~6.00% | ~6.74% | Stable |

| VA Loan | 30-Year | ~5.99%–6.32% | ~6.35% | ▼ −0.07% |

| USDA Loan | 30-Year | ~5.99% | ~6.10% | ▼ −0.05% |

| Jumbo Loan | 30-Year | ~6.42% | ~6.51% | ▲ +0.11% |

| 5/1 ARM | Adjustable | ~5.64% | ~5.72% | Stable |

| 30-Year Refi | 30-Year | ~6.56%–6.64% | ~6.70% | ▲ +0.08% |

Data: Freddie Mac PMMS (Mar 19, 2026), Optimal Blue (Mar 24, 2026), Bankrate (Mar 25, 2026).

Interest Rate vs. APR — What’s the Difference?

This confuses millions of buyers every year. Here’s the simple version:

- Interest rate = the base percentage you pay to borrow money

- APR (Annual Percentage Rate) = interest rate + lender fees + points + closing costs

Always compare APRs, not just interest rates, when shopping multiple lenders. You can use our APR Calculator to see the true cost of any loan offer side by side. For a deeper breakdown, read our guide on APR vs. Interest Rate.

Why VA and USDA Rates Run Lower

VA and USDA loans are government-backed, meaning lenders face less default risk. That reduced risk translates directly into lower rates — often 20–40 basis points below conventional loans. Eligible veterans and rural buyers who bypass these programs leave real money on the table every month.

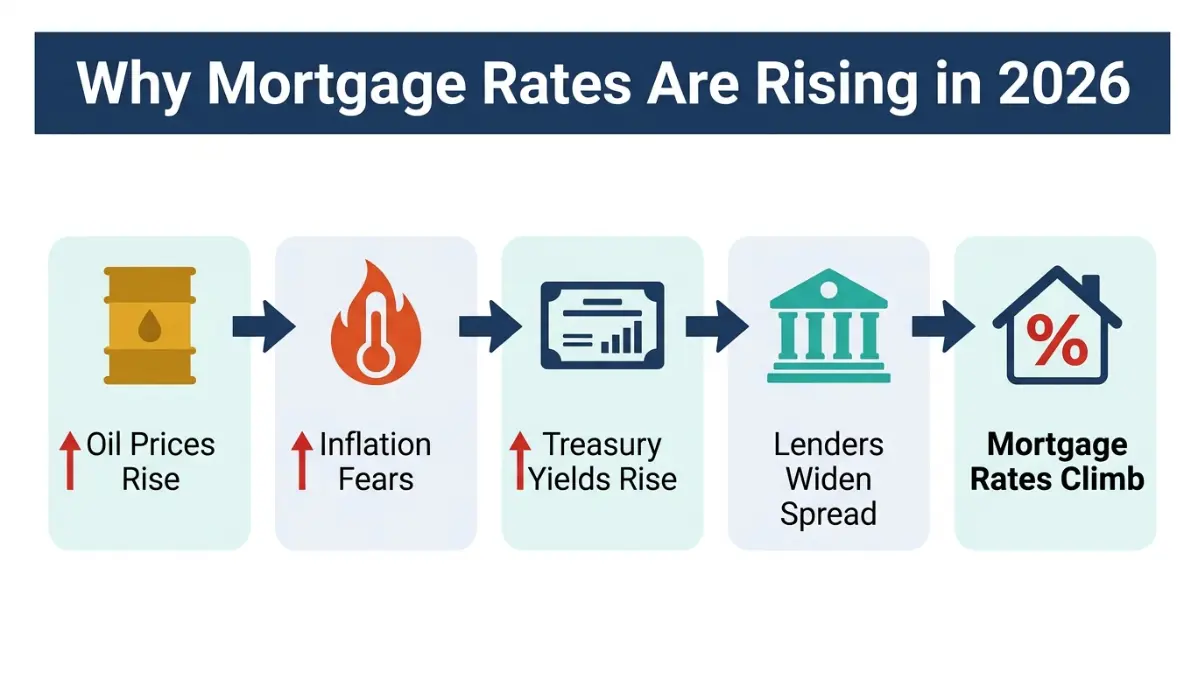

Why Are Home Loan Interest Rates Rising in 2026?

Current home loan interest rates don’t move in a vacuum. Three interconnected forces are pushing mortgage rates higher in March 2026 — and most competitors explain only one of them.

The Full Causal Chain (What Competitors Miss)

Here is the real mechanism driving today’s elevated rates:

- Geopolitical conflict → Oil prices surging past $100/barrel

- Rising oil → Renewed inflation fears in the U.S. economy

- Inflation fears → Investors demand higher yields on 10-year Treasury bonds

- Higher T-10 yields → Lenders widen the spread, pushing mortgage rates up

- Result: 30-year fixed rates near 6.36%–6.45%, a 2026 high

As Bankrate chief economist Selma Hepp noted, this is not a short-term disruption — supply chain pressure and transportation cost increases compound the problem for new construction.

The Fed’s Role — And Its Limits

The Federal Reserve held its benchmark rate at 3.50%–3.75% at the March 17–18, 2026 FOMC meeting. Many buyers assume the Fed directly controls mortgage rates. It doesn’t.

- The Fed controls the federal funds rate (overnight bank lending)

- Mortgage rates track the 10-year Treasury yield, not the Fed rate

- The typical spread between T-10 yield and 30-year mortgage rate is ~2%

What this means for you: Even if the Fed cuts rates in April or June, mortgage rates may not fall proportionally — especially if oil-driven inflation persists.

The Next FOMC Meeting: April 28–29, 2026

The FOMC meets again on April 28–29. No rate cut is currently expected, but if inflation data surprises to the downside, mortgage rates could ease. Watch the 10-year Treasury yield — not just Fed headlines.

Mortgage Application Data: A Warning Signal

MBA data shows total mortgage applications dropped 10.5% for the week ending March 20, 2026 — following a 10.9% drop the prior week. Refinancing activity collapsed 14.6%. This signals that elevated current home loan interest rates are already cooling demand significantly.

Which Home Loan Type Has the Best Rate for You?

Not all home loan interest rates are equal — and the right loan type can save you tens of thousands of dollars over the life of your mortgage. Use this section as your personal decision framework.

Loan Type Decision Table: Match Your Situation to the Best Rate

| Your Situation | Best Loan | Min. Credit Score | Min. Down Payment | Today’s Rate |

|---|---|---|---|---|

| Strong credit, stable income | Conventional 30-yr | 620 | 3%–20% | ~6.36% |

| First-time buyer, limited savings | FHA Loan | 580 | 3.5% | ~6.00% |

| Active military / veteran | VA Loan | No minimum | 0% | ~5.99% |

| Rural or suburban buyer | USDA Loan | ~640 | 0% | ~5.99% |

| Short-term homeowner (< 7 yrs) | 5/1 ARM | 620 | 5% | ~5.64% |

| High-value property ($806,500+) | Jumbo Loan | 700+ | 10%–20% | ~6.42% |

Before choosing, use our Home Affordability Calculator to know exactly how much home you can afford at today’s rates.

FHA vs. Conventional: Which Is Actually Cheaper?

FHA loans show a lower current interest rate (~6.00% vs. ~6.36%), but the true cost is higher for many borrowers due to Mortgage Insurance Premiums (MIP):

- Upfront MIP: 1.75% of the loan amount (added to your loan balance)

- Annual MIP: 0.15%–0.75% of the loan amount, paid monthly — for life if your down payment is under 10%

Bottom line: If your credit score is 680+, a conventional loan often costs less over time despite the higher rate. Our detailed comparison at FHA Loan vs. Conventional Loan walks through the true cost math with real numbers.

VA Loans: The Advantage Most Veterans Miss

The national average 30-year VA loan interest rate is approximately 6.32%, with a 30-year VA refinance rate around 6.45% — consistently 20–40 basis points below conventional. Zero down payment required. No private mortgage insurance. See our full VA Loan vs. FHA Loan comparison to see which option saves veterans more.

Is a 15-Year Mortgage Worth It in 2026?

At ~5.71%, the 15-year rate is significantly lower than the 30-year rate. But the monthly payment is much higher. Our 15-Year vs. 30-Year Mortgage guide breaks down the total interest savings vs. monthly payment trade-off with real scenario math.

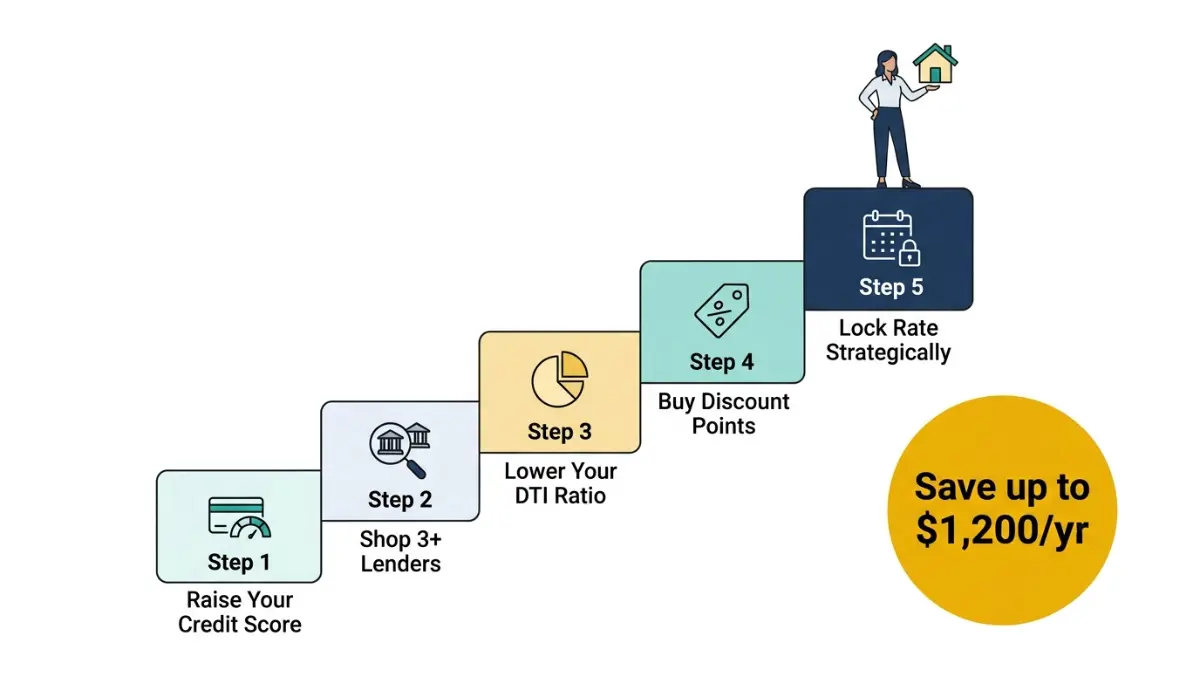

How to Get the Lowest Home Loan Interest Rate in 2026

Most buyers accept the first rate they’re quoted. That’s a costly mistake. Here are the five levers you directly control — with the dollar impact of each.

The 5 Rate Levers You Control Right Now

1. Raise Your Credit Score

Your credit score is the single biggest rate lever you hold. Here’s the real dollar impact on a $300,000, 30-year loan:

| Credit Score Range | Typical Rate | Monthly Payment | Extra Cost vs. 760+ |

|---|---|---|---|

| 760+ | ~6.10% | ~$1,819 | Baseline |

| 700–759 | ~6.35%–6.60% | ~$1,870–$1,921 | +$50–$100/mo |

| 650–699 | ~6.85%–7.25% | ~$1,970–$2,046 | +$150–$230/mo |

| 580–649 | ~7.60%–8.00%+ | ~$2,126–$2,202 | +$300–$380/mo |

Check where you stand using our Credit Score Calculator. If your score needs work, our Credit Score Complete Guide shows you the fastest path to 760+.

2. Shop Multiple Lenders — The Most Overlooked Strategy

Freddie Mac research shows that homebuyers who apply with multiple lenders might save as much as $600 to $1,200 per year. On a 30-year loan, that compounds to $18,000–$36,000 in total savings. Apply with at least 3 lenders within a 14–45 day window — credit bureaus count multiple mortgage inquiries as a single hard pull during this period.

3. Lower Your Debt-to-Income (DTI) Ratio

Lenders want your total monthly debt (including the new mortgage) below 43% of gross income. A lower DTI = lower perceived risk = better rate offers. Use our Debt-to-Income Ratio Calculator to find your current ratio, and read Debt-to-Income Ratio for Home Loans for strategies to improve it before applying.

4. Consider Discount Points

One discount point = 1% of your loan amount paid upfront, typically reducing your rate by 0.25%. On a $300,000 loan, one point costs $3,000 and saves ~$44/month. Break-even: approximately 68 months (~5.7 years). Only worth it if you plan to stay in the home that long. Use the Mortgage Calculator to model your exact break-even point.

5. Time Your Rate Lock Strategically

With the next FOMC meeting on April 28–29 approaching and geopolitical uncertainty elevated, the risk of rates rising further in the short term is real. If you’re within 30–45 days of closing, locking your rate now protects against upside rate risk. If you believe the Fed will cut in April, floating could save you 0.10%–0.25% — but it’s a gamble in the current environment.

The Consumer Financial Protection Bureau Recommends

The CFPB advises borrowers to compare Loan Estimates from multiple lenders using the same loan parameters — same loan amount, same loan term, same down payment — so you’re comparing apples to apples. This is the most actionable step most buyers skip entirely.

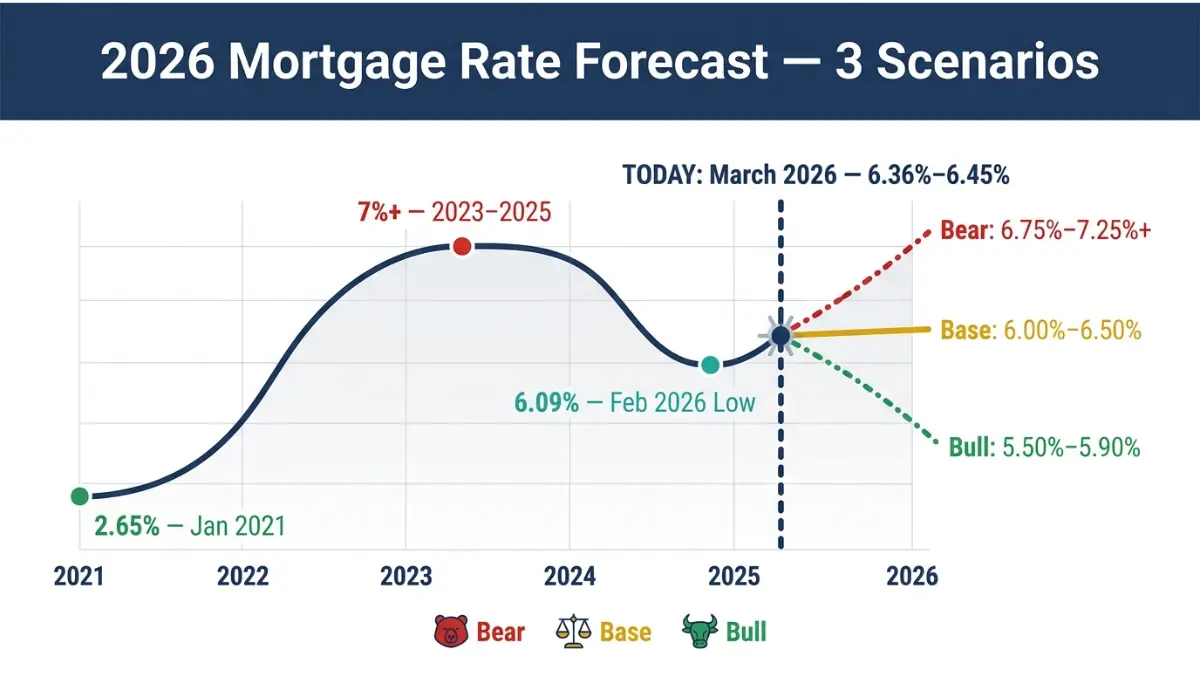

2026 Mortgage Rate Forecast — Will Rates Go Down?

Current home loan interest rates are near a 2026 high, but where are they headed? Here’s what the data and expert forecasts say — in three realistic scenarios.

The Rate Timeline: Where We’ve Been

- January 2021: 30-year fixed hit a historic low of 2.65% (Fed rate at zero, pandemic stimulus)

- 2023–early 2025: Rates climbed above 7% — the highest in two decades

- Late 2025: Fed cut rates three times (Sept., Oct., Dec.) — each cut 0.25%

- Early 2026: Rates dipped to a 2026 low of ~6.09% in February

- March 2026: Rates climbed back to 6.36%–6.45% — near 2026 highs

According to Bankrate senior industry analyst Ted Rossman, the average 30-year fixed mortgage rate could fall below 6% for the first time since summer 2022, potentially reaching as low as 5.5%, given anticipated Fed rate cuts and recession concerns — though stubbornly high inflation and other pressures could keep rates bouncing around 6% throughout much of 2026.

2026 Rate Forecast: Three Scenarios

| Scenario | Key Triggers | 30-Year Rate Outlook | Your Best Move |

|---|---|---|---|

| 🐂 Bull (rates fall) | Fed cuts April or June; oil stabilizes below $85 | 5.50%–5.90% by Q3 | Float your rate; don’t lock yet |

| ⚖️ Base (rates hover) | Fed holds; inflation steady near 3% | 6.00%–6.50% all year | Lock within 30–45 days of closing |

| 🐻 Bear (rates rise) | Conflict widens; oil stays >$100; inflation spikes | 6.75%–7.25%+ | Lock immediately |

The base case is most likely. Most housing economists expect rates to stay in the 6.00%–6.50% band for the remainder of 2026. The spring homebuying season is already showing improvement in purchase applications — making now a more competitive window than many buyers realize.

Should You Buy Now or Wait?

Waiting for lower current home loan interest rates carries its own cost: home prices may rise, competition intensifies in spring, and rental costs continue accumulating. Use our Rent vs. Buy Calculator to calculate the real break-even point for your specific situation. Also explore our full Buy First Home 2026 Guide for a step-by-step first-purchase roadmap.

For homeowners considering refinancing, our Mortgage Refinance Calculator shows exactly how much you’d save at today’s refi rates versus your current rate.

Frequently Asked Questions — Current Home Loan Interest Rates (2026)

1. What is the current home loan interest rate in the USA?

As of March 26, 2026, the average 30-year fixed mortgage rate is 6.36%–6.45% and the 15-year fixed rate is 5.54%–5.71%. VA and USDA loan rates are near 5.99%. Data sourced from Freddie Mac and Bankrate.

2. What is a good mortgage rate in 2026?

Any rate below 6.25% on a 30-year fixed is considered solid. Below 6.00% is excellent. Below 5.75% is outstanding. Your rate depends on your credit score, loan type, down payment, and lender.

3. Will home loan interest rates go down in 2026?

Possibly. The Fed held rates steady at 3.50%–3.75% in March. If the April 28–29 FOMC meeting brings a cut and oil prices stabilize, rates could ease toward 5.50%–5.90% by mid-2026. No cut is guaranteed.

4. What credit score do I need for the best mortgage rate?

A 760+ credit score gets you the best available rates. Below 700, expect to pay 0.25%–1.25% more. Below 620, you’ll likely need an FHA loan. Read our guide on Credit Score to Buy a House for a full breakdown.

5. Are FHA loan interest rates lower than conventional?

FHA rates (~6.00%) are currently lower than conventional (~6.36%), but mandatory mortgage insurance premiums (MIP) add significant cost — especially if you put down less than 10%. The true monthly cost is often higher with FHA for borrowers with strong credit.

6. What is the difference between interest rate and APR on a home loan?

Interest rate is the base borrowing cost. APR includes the interest rate plus lender fees, points, and other charges. Always compare APRs across lenders — not just the headline rate. Learn more in our APR Complete Guide.

7. What is a jumbo loan, and what is its rate in 2026?

A jumbo loan exceeds the $806,500 conforming loan limit set by the FHFA for 2026. Current jumbo rates average ~6.42% for a 30-year term. Jumbo loans require a 700+ credit score and typically 10%–20% down.

8. Is now a good time to buy a house in 2026?

For financially ready buyers, yes. Rates are near 2026 highs but still well below the 7%+ peaks of 2023–2025. Spring 2026 purchase applications are rising, signaling improved market conditions. The longer you wait, the more rent you pay. Use our Home Affordability Calculator to check your readiness.

9. How many lenders should I apply to for the best mortgage rate?

Apply to at least 3 lenders within a 14–45 day window. Multiple mortgage inquiries during this window count as a single hard pull on your credit. This shopping strategy can save you $600–$1,200 per year according to Freddie Mac research.

10. What is a VA loan rate today?

VA loan rates average 5.99%–6.32% as of March 25, 2026 — typically 20–40 basis points below conventional rates. Plus, VA loans require zero down payment and no private mortgage insurance. Check the complete breakdown in our VA Loan vs. FHA Loan comparison.

11. How does my down payment affect my mortgage rate?

A larger down payment reduces lender risk and typically earns you a lower rate. Putting down 20% or more also eliminates Private Mortgage Insurance (PMI), which adds 0.5%–1.5% of the loan amount annually to your cost. Use our Down Payment Calculator to model the impact on your monthly payment.

📋 Disclaimer: This article is for educational and informational purposes only. It does not constitute financial, mortgage, or investment advice. Mortgage rates change daily and vary based on credit profile, lender, loan type, loan amount, and location. Always consult a licensed mortgage professional or financial advisor before making borrowing decisions. Rate data sourced from Freddie Mac PMMS, Optimal Blue, Bankrate, and Zillow as of March 2026. financeauthorityhub.com is not responsible for rate changes occurring after publication.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.