VA Loan vs FHA Loan: Which Is Better for Military Borrowers in 2026?

VA loan vs FHA loan: for most veterans VA wins with $0 down and no MIP. But 6 scenarios exist where FHA is smarter. See the 2026 decision matrix.

In This Article

For most military borrowers, the VA loan vs FHA loan comparison ends quickly: VA wins. You get $0 down, no monthly mortgage insurance, and lower long-term costs. But there are 6 specific situations where FHA is the smarter choice — even for eligible veterans. Here’s exactly how to decide in 2026.

Quick Comparison: VA Loan vs FHA Loan (2026)

| Feature | VA Loan | FHA Loan |

|---|---|---|

| Down Payment | $0 required | 3.5% minimum |

| Monthly Mortgage Insurance | None | 0.55%–0.75%/year (never cancels on 30-yr) |

| Upfront Fee | 2.15% funding fee | 1.75% MIP |

| Minimum Credit Score | ~620 (lender overlay) | 580 (or 500 with 10% down) |

| 2026 Loan Limit | No cap (full entitlement) | $541,287–$1,249,125 |

| Who Qualifies | Veterans, active duty, surviving spouses | Any eligible U.S. borrower |

| Delinquency Rate (Q4 2025) | Declining | 11.52% — highest since 2021 |

| Seller Concessions Allowed | Up to 4% of purchase price | Up to 6% |

What this means for you: If you have VA eligibility and full entitlement, you are holding the most powerful home loan benefit available to any borrower in the United States. Use it. Before you run the numbers, try our Home Affordability Calculator to see exactly what home price fits your income.

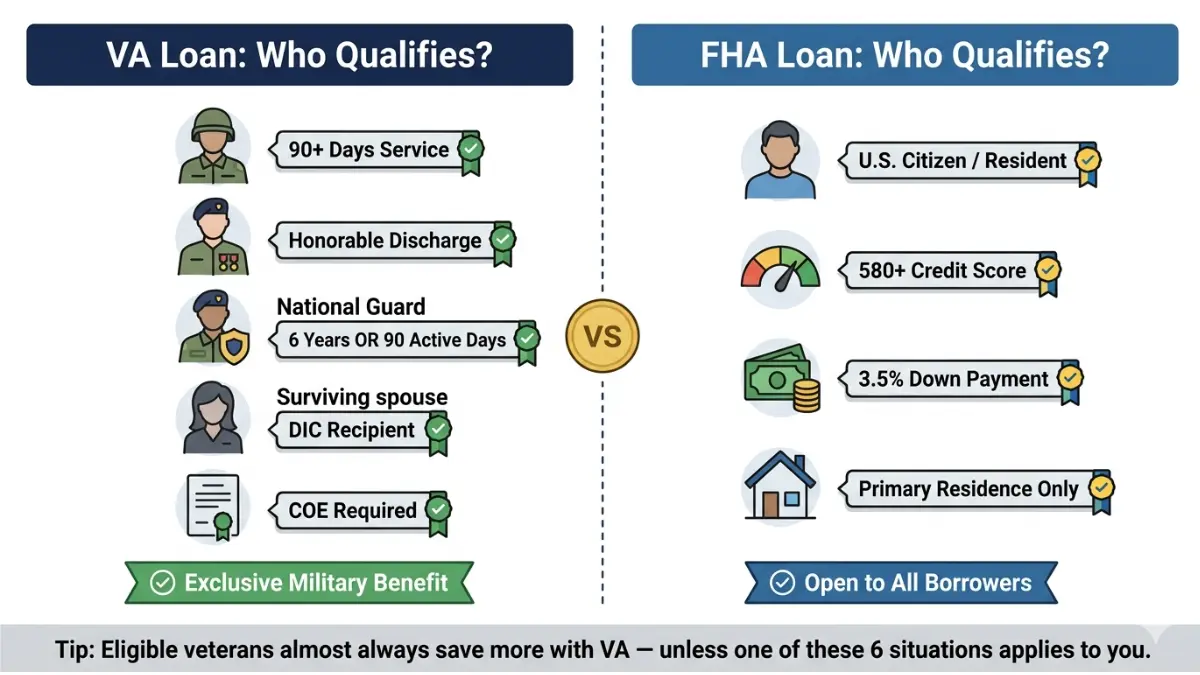

Who Qualifies — VA Loan vs FHA Loan Eligibility

VA Loan Eligibility (2026 Updated Rules)

VA loan eligibility is tied to military service. You qualify if you meet one of the following:

- Active duty: 90+ continuous days of service

- Veterans: Honorable or general discharge (character of service matters)

- National Guard / Reserves: 90 days on active non-training duty OR 6 creditable years — plus a 2026 update: members with 30+ consecutive days under Title 32, Sections 316, 502, 503, 504, or 505 now qualify

- Surviving spouses: Unremarried spouses of veterans who died in service or from a service-connected disability, including those receiving Dependency and Indemnity Compensation (DIC)

You’ll need a Certificate of Eligibility (COE) — get it through your lender, VA.gov, or by mail.

FHA Loan Eligibility (No Service Required)

FHA loans are open to any U.S. citizen or lawful permanent resident who meets financial benchmarks:

- Credit score 580+ → 3.5% minimum down payment

- Credit score 500–579 → 10% minimum down payment

- Primary residence only — no investment properties

- No military service requirement whatsoever

When Would a Veteran Choose FHA Over VA?

This is the question every competitor ignores. Here are the 6 real scenarios where FHA makes more sense — even for eligible veterans:

- VA entitlement already tied up on another property (not yet restored)

- Need a non-occupant co-borrower — FHA allows this; VA purchase loans do not

- Credit score below 580–620 — most VA lenders impose overlays FHA won’t

- Property fails VA Minimum Property Requirements (MPRs) but passes FHA standards

- Need a rehab/fixer-upper loan — FHA has the 203(k) program; VA has no equivalent

- Faster closing urgency — no COE process, broader lender pool

Understanding your debt-to-income ratio is critical for either loan. Check our Debt-to-Income Ratio Calculator before applying, and read our guide on Debt-to-Income Ratio for Home Loans for lender benchmarks.

The Real Cost Battle — VA Funding Fee vs FHA MIP (2026 Numbers)

This is where VA loans absolutely dominate — and where most articles fail to show you the full picture.

VA Funding Fee 2026 — Complete Rate Chart

| Loan Use | Down Payment | Funding Fee |

|---|---|---|

| First use | 0% | 2.15% |

| First use | 5%–9.99% | 1.50% |

| First use | 10%+ | 1.25% |

| Subsequent use | 0% | 3.30% |

| Subsequent use | 5%+ | 1.50% |

| IRRRL (streamline refi) | N/A | 0.50% |

| Cash-out refinance (first use) | N/A | 2.15% |

Who pays $0 in funding fees? Per VA.gov funding fee guidelines, the following are fully exempt:

- Veterans receiving VA compensation for any service-connected disability

- Veterans with a disability rating of 10% or higher

- Active-duty Purple Heart recipients (documented before closing)

- Surviving spouses receiving DIC payments

- Veterans with a pre-discharge pending disability claim

🔥 2026 Exclusive Update: Starting in 2026, the VA funding fee became tax-deductible for eligible borrowers who itemize deductions — a benefit zero competitors have covered yet. This further tilts the math in VA’s favor for disabled veterans and high-income military borrowers.

FHA Mortgage Insurance Premium (MIP) 2026

FHA borrowers pay two layers of mortgage insurance:

- Upfront MIP: 1.75% of the loan amount (paid at closing or rolled in)

- Annual MIP: 0.55%–0.75% of the loan balance, paid monthly

The brutal reality: FHA MIP on a 30-year loan with less than 10% down never cancels. You pay it for the entire loan term unless you refinance out.

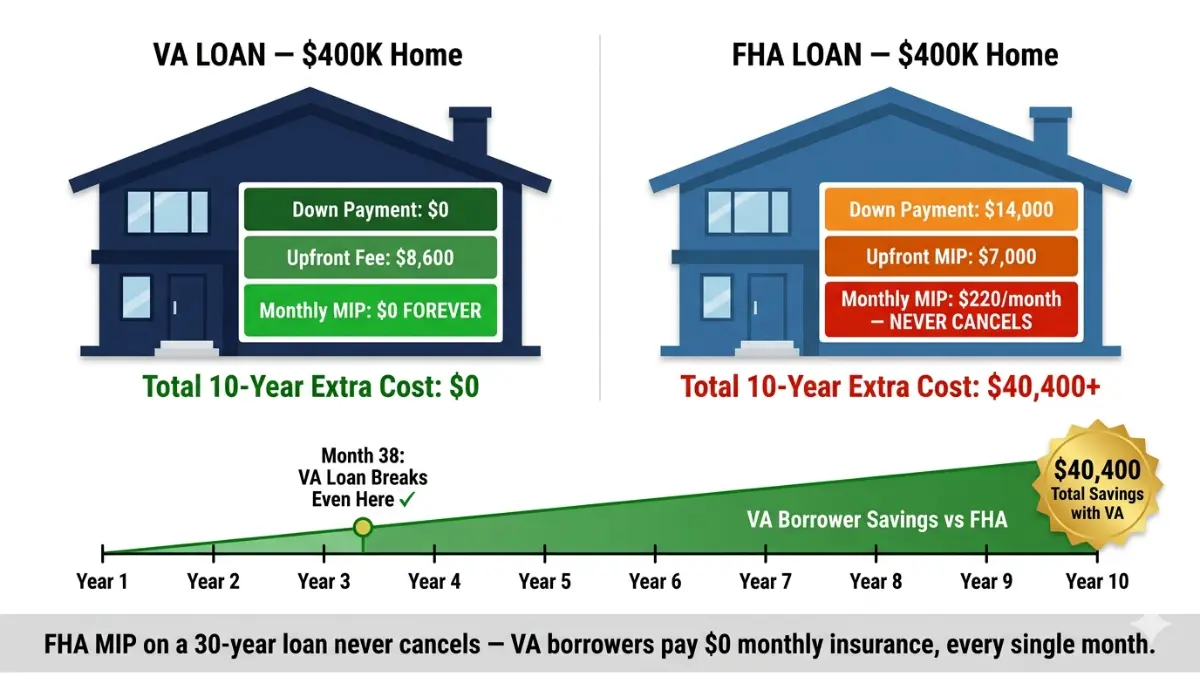

Real Dollar Comparison — $400,000 Home in 2026

| Cost Item | VA Loan (First Use) | FHA Loan |

|---|---|---|

| Down Payment | $0 | $14,000 (3.5%) |

| Upfront Fee | $8,600 (2.15%) | $7,000 (1.75%) |

| Monthly Insurance | $0 | ~$220/month |

| Cumulative MIP — Year 3 | $0 | $7,920 |

| Cumulative MIP — Year 5 | $0 | $13,200 |

| Cumulative MIP — Year 10 | $0 | $26,400 |

| Total Extra Cost (10 yrs) | $0 | ~$40,400 |

Break-even insight: Even accounting for the higher VA upfront funding fee, VA loan borrowers typically come out ahead by month 36–42. After that, every month is pure savings.

Use our Mortgage Calculator to run your exact scenario with today’s rates.

Interest Rates, Loan Limits & Property Rules

2026 Interest Rate Reality

Here’s what competitors won’t tell you: VA loan rates look higher on paper — but they’re cheaper in real terms.

- VA loan average (Dec 2025): 6.46% (30-year)

- FHA loan average (Dec 2025): 6.37% (30-year)

- Conventional average: 6.34%

The VA rate is 0.09% higher than FHA on paper. But add FHA’s $220/month MIP on a $400K loan and the effective cost swings dramatically in VA’s favor. VA loan rates ran 0.244% lower than FHA on average in 2024, and even when they’re slightly higher in nominal terms, the absence of monthly mortgage insurance makes VA the cheaper net payment in almost every scenario.

2026 Loan Limits: Where VA Destroys FHA

VA Loan Limits:

- Veterans with full entitlement face no VA-imposed loan limit — they can borrow as much as a lender will approve with no down payment required.

- For partial entitlement: the 2026 FHFA baseline conforming limit is $832,750 (up from $806,500 in 2025), with high-cost area ceilings of $1,249,125

FHA Loan Limits:

- For 2026, FHA loan limits for single-family homes range from $541,287 in designated low-cost areas to $1,249,125 in high-cost areas.

- In mid-tier markets, FHA’s lower baseline cap can force veterans into larger down payments or block the purchase entirely

Partial Entitlement Explained (the gap competitors miss): If you have an existing VA loan on another property, your entitlement is partially used. You can still get a VA loan, but the $0-down benefit applies only up to your remaining entitlement. Above that, you’ll need a 25% down payment on the difference. This is the #1 scenario where FHA becomes a viable alternative.

Property Requirements: VA vs FHA

Both loans require the property to be a primary residence. The differences:

- VA Minimum Property Requirements (MPRs): Safe, sanitary, structurally sound — enforced strictly. Older homes with peeling paint, exposed electrical, or roof issues can fail VA appraisal.

- FHA standards: Similar requirements — structural integrity, functioning electrical, heating, plumbing — but slightly more flexible on cosmetic issues.

Real scenario: A 1960s-era foreclosure with a cracked foundation may sail through FHA underwriting but get rejected at VA appraisal. In that specific case, FHA wins — but you’ll pay for it in MIP for the life of the loan. See our Mortgage Refinance Calculator to model refinancing out of FHA MIP once you build equity.

For a full breakdown of types of home loans beyond VA and FHA, including USDA and conventional options, we cover every program in detail.

Refinancing — VA IRRRL vs FHA Streamline

Both programs offer fast, low-documentation refinancing options for existing borrowers.

VA IRRRL (Interest Rate Reduction Refinance Loan)

- Only available if you already have a VA loan

- Funding fee: flat 0.50% (waived for exempt disabled veterans)

- No appraisal required in most cases

- No income verification in many scenarios

- Must lower your interest rate OR move from adjustable to fixed rate

- Per VA.gov, this is officially called a “VA to VA” loan — you cannot use it to refinance an FHA loan into VA (that requires a full VA cash-out refinance)

FHA Streamline Refinance

- Only available with an existing FHA loan

- No appraisal required

- Must demonstrate a “net tangible benefit” (lower rate or lower payment)

- Upfront MIP still applies at reduced rate: 0.01%

- Annual MIP continues — this is the critical weakness

The strategic play: If you’re currently in an FHA loan and you have VA eligibility, refinancing into a VA loan via a VA cash-out refinance eliminates your monthly MIP permanently. The funding fee applies, but you recover it within 3–4 years through MIP savings. Use our Refinance Calculator to calculate your break-even timeline. Also read our Refi Rates Guide for 2026 rate forecasts.

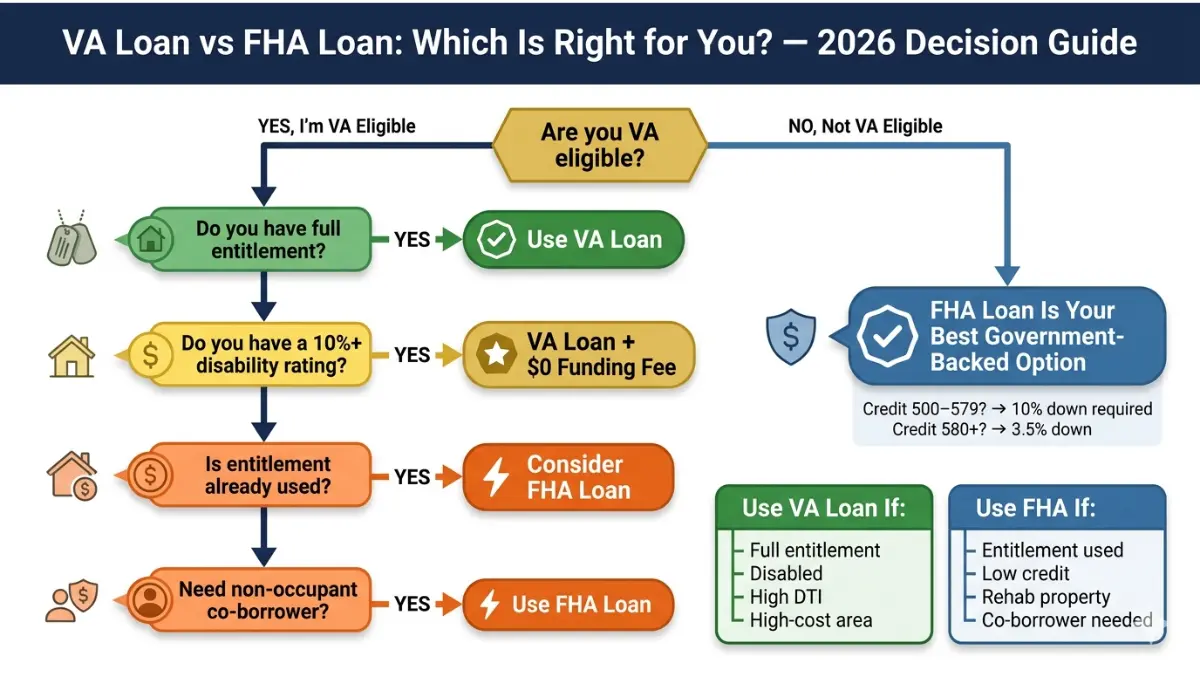

Scenario-Based Decision Framework — Which Loan Is Right for You?

Stop guessing. Use this framework to make the right call in under 2 minutes.

The 2026 VA Loan vs FHA Loan Decision Matrix

| Your Situation | Best Choice | Reason |

|---|---|---|

| Eligible veteran, full entitlement, first purchase | VA Loan | $0 down, no MIP — unbeatable total cost |

| Disabled veteran (10%+ service-connected rating) | VA Loan | Funding fee fully waived — best terms available anywhere |

| Credit score below 580 | FHA Loan | VA lender overlays start at 580–620; FHA accepts 500+ with 10% down |

| Need non-occupant co-borrower | FHA Loan | VA purchase loans don’t allow this structure |

| Entitlement tied up, not yet restored | FHA Loan | Avoids complex partial entitlement math and forced down payment |

| Buying a 203(k) rehab property | FHA Loan | VA has no rehab loan equivalent |

| DTI ratio above 41% | VA Loan | VA uses residual income model — more flexible than FHA’s hard DTI caps |

| Surviving spouse receiving DIC | VA Loan | Eligible + funding fee exempt — exceptional terms |

| Home price over $541k in low-cost county | VA Loan | FHA hits hard county cap; VA full entitlement stays unlimited |

| Currently in FHA, have VA eligibility | Refinance to VA | Eliminate lifetime MIP with one-time refinance |

Real Borrower Scenario: Sergeant Maya’s Story

Maya is an active-duty Army sergeant buying a $380,000 home in Texas in 2026. She has full VA entitlement, a 680 credit score, and zero disability rating. Here’s her actual comparison:

VA Loan:

- Down payment: $0

- Funding fee (2.15%): $8,170 (rolled into loan)

- Monthly mortgage insurance: $0

- Estimated monthly payment (6.46%, 30-yr): ~$2,387

FHA Loan:

- Down payment: $13,300 (3.5%)

- Upfront MIP (1.75%): $6,403 (rolled in)

- Monthly MIP (~0.55%): ~$174/month

- Estimated monthly payment (6.37%, 30-yr): ~$2,536

Maya saves $149/month with VA — that’s $1,788/year and $53,640 over 30 years, not counting MIP that FHA charges forever. Her VA loan breaks even vs FHA’s lower upfront cost in month 38.

What this means for you: Even if you don’t have a disability rating, the VA loan nearly always wins. If you do have a 10%+ rating, the funding fee is waived — and you may be looking at the best mortgage terms available to any homebuyer in America.

Check how much home you can afford with our Down Payment Calculator and Closing Cost Calculator before you apply. For a complete picture of credit score requirements to buy a house in 2026, our dedicated guide covers every loan type in detail.

For the FHA loan vs conventional loan comparison — useful if you’re not VA-eligible — we break down every cost difference in a separate analysis.

FAQs — VA Loan vs FHA Loan

1. Is a VA loan always better than an FHA loan for veterans?

For most eligible veterans, yes. VA loans offer $0 down, no monthly mortgage insurance, and lower long-term costs. FHA only makes more sense in 6 specific situations covered in Section 1 above.

2. Can I use an FHA loan if I qualify for a VA loan?

Yes — you can choose FHA even with VA eligibility. Veterans sometimes prefer FHA when their VA entitlement is tied up, when the property needs a 203(k) rehab loan, or when they need a non-occupant co-borrower.

3. What is the VA funding fee in 2026?

For a first-time VA purchase with 0% down, the fee is 2.15%. Subsequent use rises to 3.30%. Putting 5%+ down reduces it to 1.50%. Many veterans pay $0 due to disability exemptions — see VA.gov’s funding fee page for full details.

4. Do disabled veterans pay the VA funding fee?

Veterans with a service-connected disability rating of 10% or higher typically do not pay the funding fee, which can save thousands. Purple Heart recipients on active duty and qualifying surviving spouses are also exempt.

5. What credit score do I need for a VA loan vs FHA loan?

VA loans don’t have an official minimum, but most lenders impose a 580–620 overlay. FHA requires 580 for 3.5% down, or 500 for 10% down. Check our Credit Score Calculator and our Credit Score Guide to understand where you stand.

6. What are the FHA loan limits in 2026?

FHA loan limits for single-family homes range from $541,287 in low-cost areas to $1,249,125 in high-cost areas. VA has no limit for borrowers with full entitlement.

7. Does a VA loan require mortgage insurance?

No. VA loans have no private mortgage insurance (PMI) and no monthly MIP — ever. This single fact saves most veterans $150–$300 per month compared to FHA.

8. Can a surviving spouse get a VA loan?

Yes. Unremarried surviving spouses of veterans who died in service or from service-connected disabilities are eligible. Those receiving DIC are also exempt from the funding fee, per HUD.gov’s government mortgage program guidelines. Confirm eligibility status during pre-approval.

9. What is the VA IRRRL vs FHA streamline refinance?

Both are fast, low-doc refinance programs for existing borrowers only. The VA IRRRL charges just a 0.50% funding fee and has no appraisal requirement in most cases. The FHA streamline continues charging MIP. If you have a VA loan, IRRRL is almost always the better path.

10. How do VA and FHA loan closing costs compare?

VA closing costs typically run 1%–6% of the loan amount. FHA closing costs run 2%–6%. The key VA advantage: sellers can pay up to 4% of the home’s purchase price in concessions — enough to cover the funding fee entirely in a buyer-friendly market.

11. Can I switch from an FHA loan to a VA loan?

Yes — through a VA cash-out refinance. You don’t need to pull cash out, but you do need to meet VA eligibility and appraisal requirements. The benefit: you permanently eliminate monthly FHA MIP. Use our Mortgage Refinance Calculator to see if your break-even timeline makes it worthwhile.

Key Takeaways

- VA loan wins for most veterans — $0 down, no MIP, lower long-term cost

- Disabled veterans (10%+ rating): $0 down + $0 funding fee = best mortgage in America

- FHA has 6 valid use cases for veterans — don’t dismiss it automatically

- The MIP trap is real: FHA borrowers on 30-year loans pay mortgage insurance forever

- 2026 update: VA funding fee is now tax-deductible for eligible itemizers

- VA delinquency rate is falling while FHA delinquency hit 11.52% in Q4 2025

⚠️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, mortgage, or legal advice. Loan terms, interest rates, program rules, and limits are subject to change. All figures cited reflect publicly available data as of early 2026. Consult a licensed mortgage professional or VA-approved lender for guidance specific to your financial situation, service history, and eligibility status.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.