Home Loan Closing Costs: What You’ll Actually Pay in 2026

Home loan closing costs in 2026 run 2%–6% of your loan. On a $350K home, that’s up to $21,000. See every fee breakdown and how to legally pay less.

In This Article

Home loan closing costs in 2026 range from 2% to 6% of your loan amount. On a $350,000 home, that means $7,000–$21,000 on top of your down payment. The national average sits at approximately $6,900 (excluding prepaid items), according to industry data — and costs rose roughly 3.8% from 2025 due to inflation on labor-intensive services. Most buyers can realistically save $2,000–$5,000 by shopping strategically. Here’s exactly what you’ll pay — and how to pay less.

What Are Home Loan Closing Costs? Every Fee, Explained

Closing costs are the fees and expenses required to finalize your mortgage and legally transfer home ownership. You pay most of them on closing day, in addition to your down payment.

They fall into four categories: lender fees, third-party service fees, prepaid items, and government charges.

Complete Closing Cost Fee Table — 2026

| Fee | Typical Cost | Negotiable? | Who Pays |

|---|---|---|---|

| Loan Origination Fee | 0.5%–1% of loan | ✅ Yes | Buyer |

| Appraisal Fee | $300–$600 | ❌ No | Buyer |

| Lender’s Title Insurance | $500–$1,500 | ✅ Yes | Buyer |

| Owner’s Title Insurance | $500–$1,500 | ✅ Optional | Buyer |

| Title Search Fee | $75–$200 | ❌ No | Buyer |

| Escrow / Settlement Fee | 1%–2% of sale price | ✅ Yes | Buyer/Seller |

| Credit Report Fee | $10–$100 | ❌ No | Buyer |

| Recording Fee | $50–$250 | ❌ No | Buyer/Both |

| Transfer Tax | Varies by state | ❌ No | Varies |

| Prepaid Interest | Varies | ❌ No | Buyer |

| Homeowners Insurance (1st year) | $1,200–$3,000 | ❌ No | Buyer |

| Property Tax (prepaid 2–8 months) | Varies | ❌ No | Buyer |

| Attorney Fee | $400–$1,500 | ✅ Yes | Buyer |

| PMI (if <20% down) | $30–$70 per $100K | ❌ No | Buyer |

| Discount Points | 1% of loan per point | ✅ Optional | Buyer |

| HOA Transfer Fee | $200–$500 | ❌ No | Varies |

| Survey Fee | $400–$700 | ❌ No | Buyer |

| Pest Inspection | $75–$150 | ❌ No | Varies |

💡 Key Takeaway: Before agreeing to any fee, ask your lender: “Is this negotiable?” That single question saves most buyers $500–$2,000 at the table.

Use our Closing Cost Calculator to instantly estimate your total fees based on your loan amount and state.

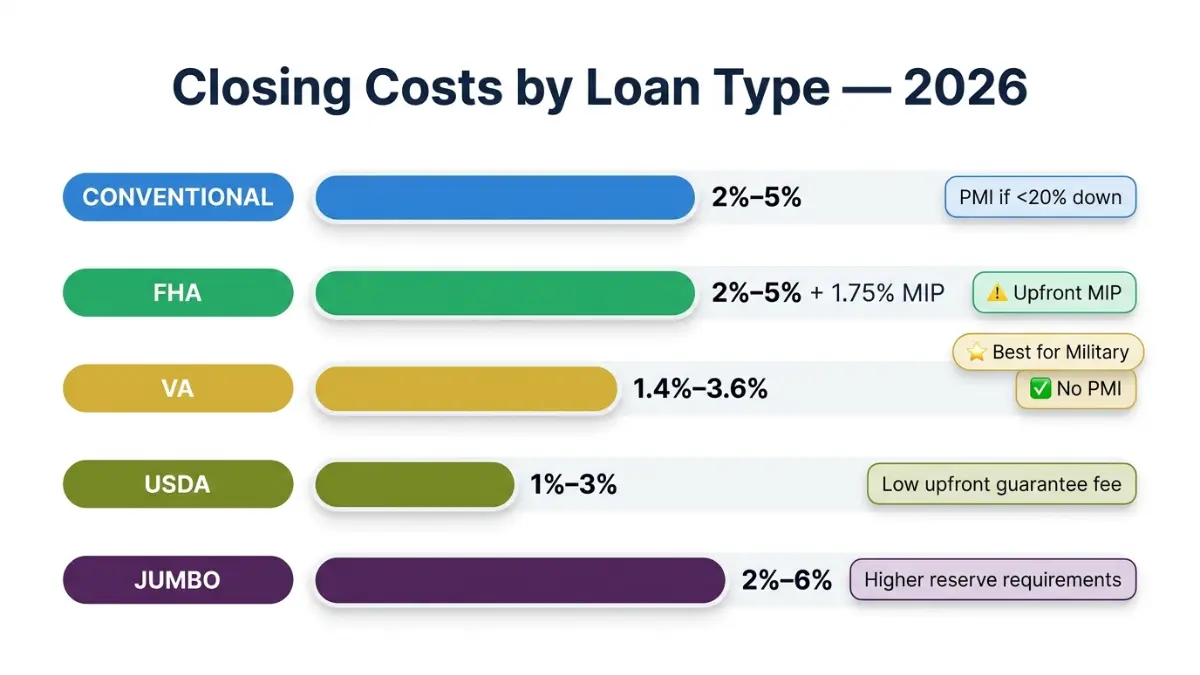

Average Home Loan Closing Costs in 2026 — By Loan Type and State

How Much Are Closing Costs by Loan Type?

Your loan type significantly determines which fees you pay — and how much.

| Loan Type | Typical Range | Key Unique Fee |

|---|---|---|

| Conventional | 2%–5% | PMI if <20% down |

| FHA | 2%–5% + 1.75% upfront MIP | Upfront Mortgage Insurance Premium |

| VA | 1.4%–3.6% funding fee | No PMI, but mandatory funding fee |

| USDA | 1%–3% + 1% guarantee fee | Upfront guarantee fee |

| Jumbo | 2%–6% | Higher origination and title fees |

- FHA loans are buyer-friendly on credit requirements, but the 1.75% upfront MIP on a $300,000 loan adds $5,250 to your closing costs. See a full FHA Loan vs Conventional Loan comparison to decide which fits your situation.

- VA loans eliminate PMI entirely — a massive long-term saving. Read our VA Loan vs FHA Loan breakdown if you’re a military borrower.

Average Closing Costs by State — Highest to Lowest (2026)

| State | Average Closing Costs |

|---|---|

| Washington, D.C. | ~$17,545 |

| New York | ~$13,000+ |

| Delaware | ~$12,000+ |

| Maryland | ~$11,000+ |

| California | ~$8,000–$10,000 |

| Texas | ~$6,500–$8,000 |

| Florida | ~$6,000–$7,500 |

| Missouri | ~$1,740 |

| Iowa | ~$1,640 |

| South Dakota | ~$1,551 |

Why such massive gaps? State transfer taxes, mandatory attorney requirements, and local property values are the three biggest drivers. Buyers in D.C. and New York face compounding layers of city, county, and state transfer taxes that simply don’t exist in Midwest states.

2026 Market Shift: Inventory is up approximately 15% nationally, shifting negotiating power toward buyers. This is the best year since 2019 to push for seller concessions on closing costs.

The NAR settlement, which took effect in mid-2024, changed how buyer agent commissions are negotiated. Buyer agent fees are now separate from the MLS listing — meaning your total cash-to-close calculation must account for agent compensation that previously was folded into the seller’s side. Factor this into your budget using our Home Affordability Calculator.

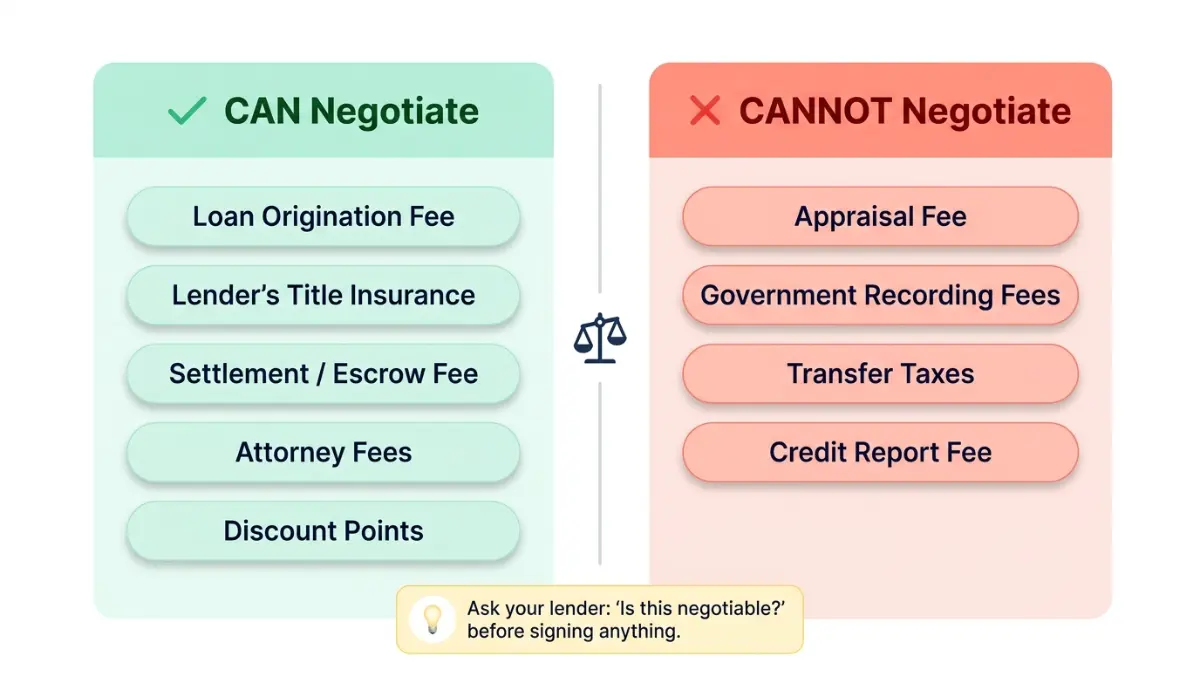

The Fee Negotiability Scorecard — What You Can Actually Fight

This is what competitors won’t tell you. Not all closing costs are created equal. Some are legally fixed. Others are pure lender profit — and fully negotiable with the right approach.

Fees You CAN Negotiate

- Loan origination fee — This is the lender’s processing charge, typically 0.5%–1% of the loan. On a $400,000 loan, that’s $2,000–$4,000. Get Loan Estimates from at least three lenders and use them as leverage. Lenders routinely reduce origination fees when they know you’re shopping.

- Lender’s title insurance — Prices vary by $500–$1,000 for identical coverage. In most states, you can shop for your own title company. The CFPB’s guide to shopping for title insurance explains exactly what you’re buying.

- Escrow/settlement fee — The escrow company or closing attorney charges this. Get quotes from multiple settlement agents in your area.

- Discount points — You choose whether to buy down your rate. If you plan to sell or refinance within 5–7 years, skipping points is almost always the right move.

- Attorney fees — In states where attorneys are required, fees range from flat-rate to hourly. Ask upfront and negotiate a flat fee.

Fees You CANNOT Negotiate

- Appraisal fee — Set by Appraisal Management Companies (AMCs), not the lender. You cannot shop for this.

- Government recording fees — Fixed by your county.

- Transfer taxes — Set by state and local law.

- Credit report fee — Fixed by the credit bureaus.

The Lender Credit Strategy — Underused and Powerful

Ask your lender for lender credits — the lender covers part of your closing costs in exchange for a slightly higher interest rate.

Example: $3,000 in lender credits on a $350,000 loan requires roughly a 0.25% rate increase, adding approximately $52/month. The break-even point is about 58 months. If you plan to move or refinance before that — lender credits are a clear win.

💡 Key Takeaway: Get a Loan Estimate from at least three lenders and compare Section A (Origination Charges) line by line. One lender study found an average $2,600 difference in origination fees on identical loans.

Run your numbers with our Mortgage Calculator and APR Calculator to see how lender credits affect your true long-term cost.

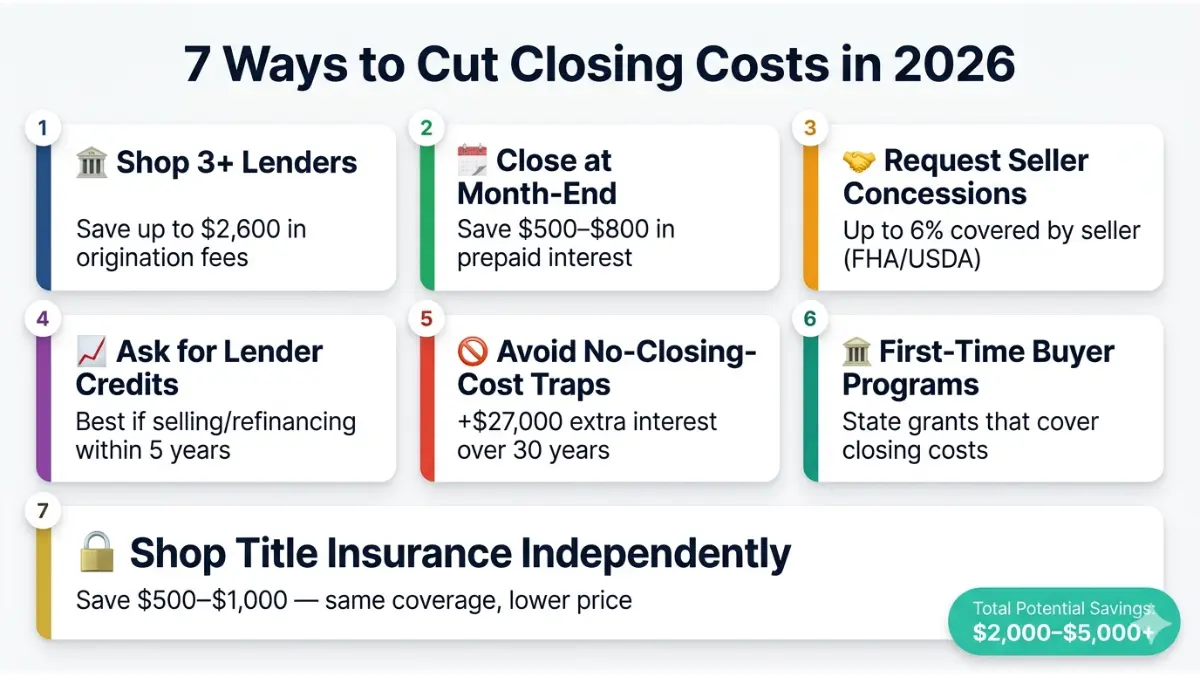

7 Proven Ways to Lower Your Home Loan Closing Costs in 2026

These aren’t generic tips. These are strategies with real dollar amounts.

1. Shop a minimum of three lenders — non-negotiable. A Freddie Mac study found borrowers who obtained five rate quotes saved an average of $3,000 over the loan’s life. Fees vary just as much as rates. Compare Section A of the Loan Estimate — not just the headline rate.

2. Close at month-end. Prepaid interest covers the days between your closing date and your first payment. Closing on the 28th–31st instead of the 1st can save $500–$800. On a $400,000 loan at 7%, you’re paying approximately $75/day in prepaid interest.

3. Request seller concessions — 2026 is the moment. With inventory up roughly 15%, sellers are negotiating again.

| Loan Type | Maximum Seller Concession |

|---|---|

| Conventional (≥10% down) | Up to 6% of purchase price |

| Conventional (<10% down) | Up to 3% |

| FHA | Up to 6% |

| VA | Up to 4% |

| USDA | Up to 6% |

Negotiation approach: Offer list price but request 3% in seller concessions. On a $400,000 home, that’s $12,000 toward your closing costs.

4. Ask about a no-closing-cost mortgage — but do the math first. The lender rolls closing costs into your rate. On a 30-year $350,000 mortgage, a 0.375% rate increase adds approximately $27,000 in extra interest over the life of the loan. This only makes financial sense if you won’t keep the loan beyond 5–6 years. Use our Refinance Calculator to run your break-even analysis.

5. Check first-time buyer assistance programs. Many states offer closing cost grants or zero-interest deferred loans. These programs are separate from down payment assistance. Our full Down Payment Help Guide covers state-by-state options including programs that cover closing costs directly. HUD maintains a searchable database of housing counselors who can identify programs you qualify for at no cost.

6. Shop title insurance independently. In most states, you have the legal right to choose your own title company. The same $400,000 policy from one company might cost $800 at another. This is the single most overlooked negotiable fee in the entire closing cost stack.

7. Understand your DTI ratio before applying. A high debt-to-income ratio can push you toward higher-cost loan products. Check your current ratio with our Debt-to-Income Ratio Calculator — and read our full guide on Debt-to-Income Ratio for Home Loans before you apply.

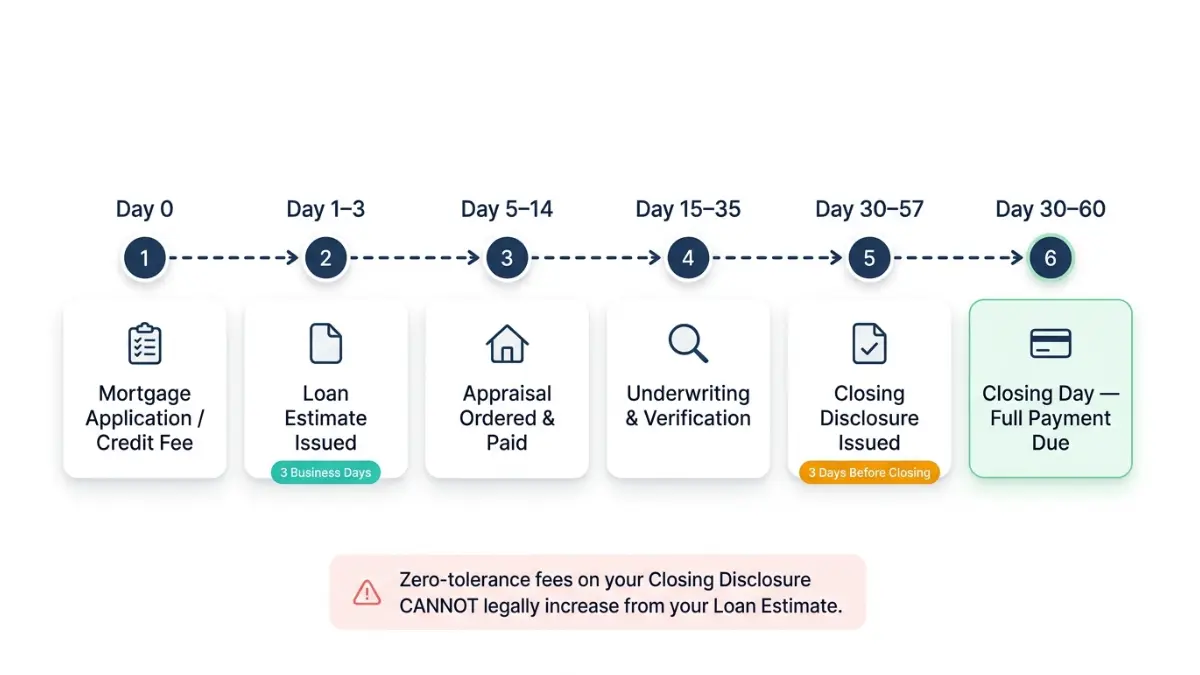

The Closing Cost Timeline — From Application to Closing Day

Most buyers are surprised by closing costs because they don’t know when to expect each charge. Here’s the complete timeline.

| Stage | Timing | What Happens |

|---|---|---|

| Mortgage Application | Day 0 | Credit report fee may be charged upfront |

| Loan Estimate Issued | Within 3 business days | All estimated closing costs disclosed in writing |

| Appraisal Ordered | Days 5–14 | Appraisal fee paid (often before closing) |

| Underwriting Approval | Days 15–35 | Lender verifies income, assets, property |

| Closing Disclosure Issued | At least 3 business days before closing | Final costs confirmed — compare to Loan Estimate |

| Closing Day | Days 30–60 | Remaining fees paid via cashier’s check or wire |

What to Check on Your Closing Disclosure

The Closing Disclosure is a 5-page document that lists your final costs. Compare it carefully to your original Loan Estimate.

Fee tolerance rules protect you:

- Zero tolerance (cannot increase): Origination fees, credit report fee, transfer taxes

- 10% tolerance (can increase up to 10%): Recording fees, required third-party services

- Unlimited tolerance (can change freely): Prepaid interest, homeowners insurance premiums

💡 Key Takeaway: If any zero-tolerance fee increased on your Closing Disclosure compared to your Loan Estimate, your lender must legally absorb that cost — not you. Raise this immediately and in writing.

Your credit score directly affects what fees you qualify for. Borrowers with scores below 680 often face higher origination fees and lender surcharges. Check our Credit Score to Buy a House guide, and use our Credit Score Calculator to track your current standing.

For a full overview of the mortgage process before your closing date, our How Does a Home Loan Work guide walks through every stage in plain language.

Expert Panel Insights, FAQs & Disclaimer

What Financial Experts at FinanceAuthorityHub Say

Laura M. Bennett, CFP — “In the current 2026 buyer-favorable market, the biggest mistake I see is borrowers accepting the first Loan Estimate they receive. Most lenders have a 20–30% flexibility window on origination fees they will never volunteer. Getting three Loan Estimates takes two hours — and routinely saves clients $2,000 or more.”

Daniel Moreau, CPA/CFP — “Rolling closing costs into the loan only makes sense if you’re exiting the property within five years. Long-term holders almost always come out ahead paying upfront. Every dollar rolled in accrues 30 years of compound interest.”

Michael R. Thompson, CFA — “Owner’s title insurance is optional in most states, yet most buyers automatically pay it. Evaluate your specific risk profile — if the title search is clean and the seller has clear ownership history, this is a cost worth scrutinizing.”

Frequently Asked Questions — Home Loan Closing Costs 2026

1. What are typical home loan closing costs in 2026?

Closing costs typically range from 2% to 6% of the loan amount. On a $300,000 home, expect $6,000–$18,000. The national average for a purchase loan is approximately $6,900 excluding prepaid items, with costs rising roughly 3.8% from 2025.

2. Are closing costs paid upfront or rolled into the mortgage?

Most are paid on closing day via cashier’s check or wire. Some lenders allow rolling costs into the loan, but this increases your loan balance and adds interest cost over the life of the mortgage.

3. Can the seller pay my closing costs?

Yes — this is called a seller concession. Limits are 3%–9% for conventional loans, 6% for FHA and USDA, and 4% for VA loans. In the current 2026 buyer’s market, requesting seller concessions is highly viable.

4. What closing costs are tax-deductible?

Discount points are generally deductible in the year paid (for purchase loans). Origination fees structured as points may also qualify. Transfer taxes and title insurance are not deductible. Always consult a tax professional — the IRS Publication 530 covers homeownership tax deductions in detail.

5. What is a no-closing-cost mortgage — is it worth it?

A no-closing-cost mortgage rolls fees into the loan or trades them for a higher interest rate. It can make sense if you plan to move or refinance within 5–6 years. Long-term, it typically costs $20,000–$30,000 more on a 30-year mortgage.

6. How are closing costs different for FHA vs VA loans?

FHA loans require a 1.75% upfront mortgage insurance premium, adding thousands at closing. VA loans eliminate PMI entirely but require a funding fee of 1.4%–3.6%. VA loans usually have lower total closing costs for eligible borrowers.

7. Can I negotiate origination fees with my lender?

Absolutely — and you should. Origination fees are the lender’s profit margin and are among the most negotiable items. Getting competing Loan Estimates and presenting them to your preferred lender is the most effective leverage you have.

8. When exactly do I pay closing costs?

You pay the majority on closing day. The exception is the appraisal fee, which is often paid when the appraisal is ordered (days 5–14 of the process), and the credit report fee, which may be collected at application.

9. What happens if closing costs are higher than the Loan Estimate?

Zero-tolerance fees (origination, credit check, transfer taxes) legally cannot increase. If they did, your lender must absorb the difference. Escalate in writing immediately if you spot discrepancies on your Closing Disclosure.

10. How much should I budget for closing costs on a $400,000 home?

Budget $8,000–$24,000 (2%–6%). A realistic midpoint is $12,000–$14,000, depending on your state and loan type. Always use our Closing Cost Calculator to model your specific scenario.

11. Do closing costs differ for refinancing vs. buying?

Yes — refinance closing costs average $2,400 nationally, significantly less than purchase closing costs. However, you must factor in the break-even timeline. Our Mortgage Refinance Calculator calculates your exact break-even point.

Disclaimer

This article is for educational and informational purposes only and does not constitute financial, mortgage, or legal advice. Home loan closing costs vary by lender, state, loan type, and individual financial profile. All figures cited reflect 2026 market data and may change. Always consult a licensed mortgage professional or HUD-approved housing counselor before making any borrowing or real estate decisions. FinanceAuthorityHub.com is not responsible for actions taken based on the information provided in this article.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.