The NPV Breakdown of Lump Sum vs Structured Settlement

Lump sum vs structured settlement: the 2026 NPV math reveals what break-even return rate you need before a factoring offer makes financial sense.

In This Article

Is the lump sum offer actually worth taking?

The factoring company’s offer arrived with a deadline.

A number that sounds significant — and a countdown clock designed to force a decision before you have done the math.

Why most comparisons give you the wrong number

The most expensive mistake structured settlement recipients make is comparing the lump sum dollar amount directly to the total remaining payment stream.

That comparison ignores the time value of money entirely.

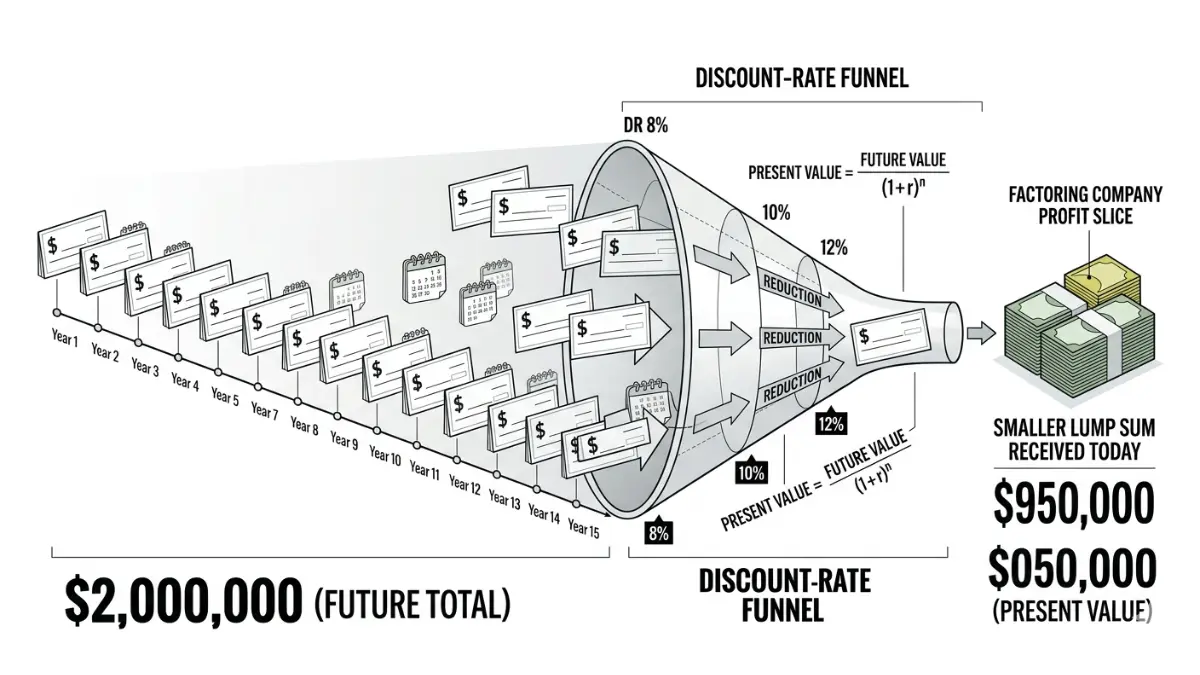

The correct benchmark is the lump sum versus the present value of your future payments — discounted to reflect what those dollars are actually worth in today’s terms.

A stream of $150,000 paid over twenty years is worth considerably less than $150,000 right now.

What this article will calculate for you

This analysis delivers the NPV break-even framework used in capital markets advisory, anchored to 2026 Federal Reserve benchmark rate data.

By the end, you will know the specific annual investment return you must beat to justify accepting the lump sum payment over keeping your structured payments.

Use the investment return modeling tool to pressure-test your specific offer numbers alongside this analysis.

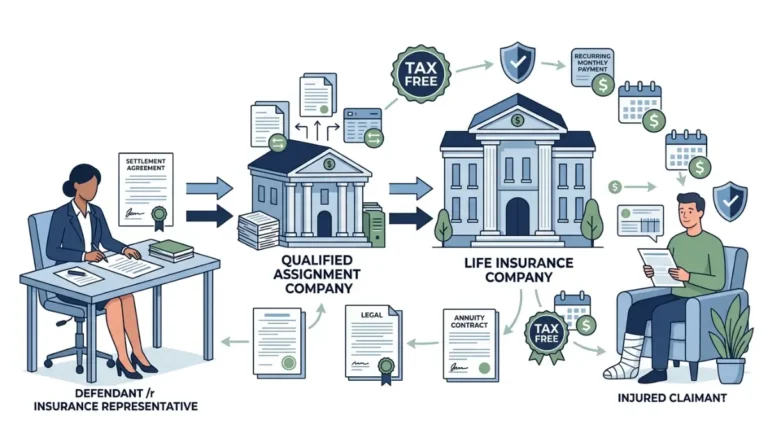

How structured settlements and lump sum buyouts actually work

A structured settlement is a legally binding arrangement in which a claimant receives tax-free periodic payments rather than a single lump sum — typically established after a personal injury, wrongful death, or workers’ compensation claim.

Those payments are backed by a fixed annuity purchased from a life insurance carrier at settlement origination.

The annuity structure behind every periodic payment

Every structured settlement payment is guaranteed by an annuity contract locked in at origination — the amount, schedule, and duration are fixed and cannot be modified after the agreement is executed.

The payments are legally protected and, in most cases, cannot be garnished by creditors or seized in a bankruptcy proceeding.

Use the payment stream growth comparison tool to model how a guaranteed payment schedule compounds differently from a self-directed invested lump sum over a 10- or 20-year horizon.

How factoring companies earn their margin

When a factoring company makes a lump sum buyout offer, they are discounting your future payments at a rate — typically between 9% and 18% in 2026 — that builds their profit margin directly into the offer.

Their fee is not a service charge layered on top of fair value.

📊 Data Point: Structured settlement factoring companies applied discount rates of 9% to 18% on most consumer transfer transactions documented in FINRA’s structured settlement investor protection guidance as of Q1 2026. — Source: FINRA Investor Alerts, Q1 2026. Verify current ranges at finra.org.

It is the discount rate applied to the present value of your payments — and understanding that distinction is the only way to evaluate whether the offer is fair.

How to calculate whether the lump sum beats your payments

To determine whether a lump sum offer is mathematically worth accepting, calculate the net present value of your remaining payment stream using these three steps:

Step 1: Calculate the present value of your remaining payments

Net present value (NPV) is the sum of each future payment divided by (1 + discount rate) raised to the number of years until that payment arrives — applied to every payment, then added together.

Use the Federal Reserve’s 2026 10-year Treasury yield as your discount rate anchor — not the rate the factoring company states in the offer.

📊 Data Point: The Federal Reserve H.15 release reported the 10-year Treasury constant maturity yield at approximately 4.48% in May 2026, establishing the appropriate risk-free rate benchmark for structured settlement NPV calculations. — Source: Federal Reserve H.15 Selected Interest Rates, May 2026.

Use the break-even return rate calculator to apply your specific payment schedule to this formula.

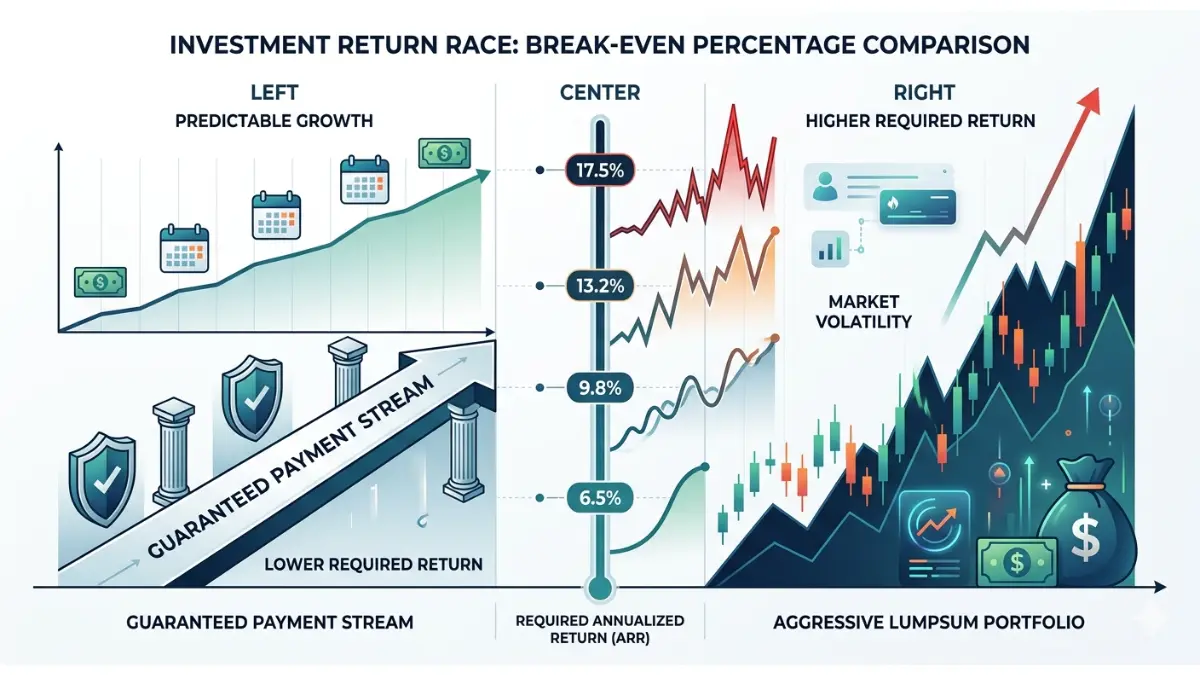

Step 2: Find your break-even investment return rate

The break-even return rate is the annual investment return you must earn on the invested lump sum to match the value of keeping your structured payments over the same period.

| Lump Sum Offer (as % of Payment NPV) | Break-Even Annual Return Required |

|---|---|

| 50% of NPV | ~17.5% per year |

| 60% of NPV | ~13.2% per year |

| 70% of NPV | ~9.8% per year |

| 80% of NPV | ~6.5% per year |

Based on a 15-year payment horizon at the 2026 4.48% Treasury rate benchmark. CFA analysis — Finance Authority Hub, May 2026.

💡 Expert Note (CFA): This table surprises almost every client I walk through it. An offer at 60% of NPV sounds like “most of your money back” — it actually requires 13.2% annual returns just to break even. That exceeds realistic long-run equity return expectations for most individual investors, before fees and taxes are deducted.

Use the ROI analysis calculator and the compound interest growth tool to model how your specific lump sum would realistically grow under your planned strategy.

Step 3: Compare your break-even rate to 2026 portfolio benchmarks

The broad U.S. equity market has delivered approximately 10.3% annually over a 30-year period before inflation — well below the break-even threshold at most factoring company offer levels.

S&P 500 benchmark returns are a historical average, not a guarantee — and individual investor results after fees, taxes, and behavioral slippage consistently fall below it.

When taking the lump sum makes sense — and when it doesn’t

Whether a lump sum or structured payments produces the better lifetime financial outcome depends on three converging factors: the discount rate in the offer, your actual investment discipline, and your current financial stability.

Three profiles where the lump sum is mathematically and behaviorally sound

Consider the lump sum buyout seriously only when all three of these conditions apply:

- The offer is at 80% or more of your payment NPV — at that level, the break-even annual return drops to roughly 6.5%, a threshold a disciplined, diversified portfolio can realistically target over a long horizon.

- You have a specific, funded investment plan already established before signing — not a general intention to invest, but an account opened with a written allocation strategy in place the day you sign.

- Your financial stability does not depend on this payment stream — emergency reserves cover at least six months of expenses, and core living costs are fully supported by other income sources.

💡 Expert Note (CFA): In 28 years of capital markets advisory work, the clients who most regretted taking a lump sum almost always shared one trait: they planned to invest the proceeds but spent the money within eighteen months. The guaranteed payment stream has behavioral value that no NPV formula captures — and that safety net is worth pricing into the decision before you commit.

Use the inflation-adjusted return calculator to see what your payment stream is worth in real 2026 purchasing power over its remaining term before comparing it to any buyout.

Three situations where keeping structured payments protects you

The structured payment stream is the stronger financial outcome when any of these conditions apply:

- The offer is below 70% of NPV — requiring 9.8% or more in annual returns just to break even, which exceeds realistic long-run equity expectations for most individual investors in 2026.

- You have no specific, documented investment plan — behavioral research consistently shows that recipients without a written strategy in place spend rather than invest a lump sum.

- You are in active financial distress — using a settlement buyout to cover immediate expenses permanently surrenders long-term guaranteed income for a one-time cash event with no recovery mechanism.

⚠️ Warning: FINRA’s 2026 investor protection guidance identified structured settlement buyouts used to cover short-term expenses as among the most financially damaging misuses of settlement assets documented in the consumer market. Once a court approves the transfer, the decision is permanent and cannot be reversed.

Consult the SEC’s investor education resources for individual investors before constructing any plan to deploy a lump sum into market-linked investments.

Use the retirement income modeling calculator and the equity return analysis tool to model whether your specific investment plan can realistically outperform your payment stream across your horizon.

What actually happens when you sell structured settlement payments

Selling structured settlement payments is not a private contract between two parties.

It is a regulated judicial process — one with legal protections that most factoring company representatives will not volunteer during the sales presentation.

The court approval requirement factoring companies rarely volunteer

Every state in the United States has enacted a Structured Settlement Protection Act requiring a judge to review and approve any payment transfer before it becomes legally valid.

The factoring company files the petition — but the judicial review exists to protect you, not the buyer.

📊 Data Point: All 50 states have enacted Structured Settlement Protection Acts as of 2026, requiring court approval before any structured settlement transfer is legally binding. A judge can reject any transfer not found to be in the seller’s best interest. — Source: FINRA Investor Protection Alerts — Structured Settlement Transfers, Q1 2026.

A judge has full authority to reject the transaction if it does not serve the seller’s financial best interest — and exercises that authority regularly.

Most recipients do not learn this protection exists until after they have already signed the initial agreement with the factoring company.

Your right to cancel and the timeline you need to know

Most states require a minimum review period — typically three to five business days — between signing the initial agreement and its submission to the court.

That window is your right to cancel, and it is the most immediate legal protection available against high-pressure sales tactics.

The full buyout process runs 45 to 90 days from the initial offer to funding disbursement, depending on the state court’s calendar and filing requirements.

Review the CFPB’s consumer guidance on structured settlement transactions before signing any initial agreement, and consult FINRA’s investor protection alerts on structured settlement sales to understand the specific red-flag behaviors regulators have documented in this market.

💡 Expert Note (CFA): The court approval requirement is the most powerful protection a structured settlement recipient holds — and the most consistently omitted detail in a factoring company’s sales presentation. A judge can reject an unfair deal. That protection exists before you sign, not after. Use it.

The real cost of taking the lump sum: taxes, fees, and discount math

Original structured settlement payments for physical injury or illness are fully excluded from gross income under IRC Section 104(a)(2) — one of the most valuable tax protections in the U.S. tax code.

The lump sum buyout proceeds are also tax-free at receipt.

The growth on those proceeds is not.

Why original payments are tax-free but your investment gains are not

Every dollar your deployed lump sum earns in a brokerage account, index fund, or dividend-paying asset is subject to capital gains tax in the year those gains are realized.

The tax-free status of the original payment stream does not transfer to the investment returns generated after deployment.

📊 Data Point: In 2026, long-term capital gains rates are 0% for taxable income up to approximately $49,000 (single filers), 15% up to $553,850, and 20% above that threshold. Investment gains from deployed lump sum proceeds are taxable at these rates in the year of realization. — Source: IRS Publication 4345 — Settlements: Taxability, 2026.

A reader projecting $60,000 in ten-year investment gains must reduce that figure by 15% to 20% before making any comparison with what the tax-free structured payment stream would have delivered over the same period.

Calculating your true net lump sum after fees, discount, and taxes

The real financial comparison is not gross lump sum versus total payment stream.

It is net lump sum after the discount rate cost, minus projected capital gains taxes on investment returns, versus the NPV of the tax-free payment stream over the same horizon.

Use the capital gains tax estimation tool to calculate your specific tax exposure on investment gains and the income and total tax liability calculator to model your full-year tax picture in the year you receive and begin deploying the lump sum.

⚠️ Warning: Readers who exclude capital gains taxes from lump sum projections overestimate the net financial benefit by 15% to 20% — a margin large enough to flip a break-even scenario into a net loss compared to keeping the structured payments. Consult a licensed tax professional before finalizing any net-value assumptions.

Three questions to answer before you sign anything

The NPV math, the decision framework, the legal process, and the tax picture are all complete.

Three questions remain — and a confident answer to each is the minimum standard before any structured settlement buyout is the right financial choice.

Your next step: model the math or find a fiduciary

Question one: Does the factoring company’s implied discount rate produce a break-even annual return that a realistic, diversified portfolio can achieve — or does it require above-market performance with no guarantee of delivery?

Question two: Do you have a specific, funded investment plan in place for the lump sum proceeds before signing — documented in writing, with an account already established and an allocation strategy committed to?

Question three: Are you financially stable enough that you do not need the behavioral certainty of a guaranteed income stream — and is the theoretical upside of a self-directed portfolio worth permanently surrendering that guarantee?

If you cannot answer all three with full confidence, use the household budget analysis tool to assess your financial position before you commit to anything.

A licensed CFA, CFP, or SEC-registered RIA is the appropriate professional to stress-test your answers — and to model the complete break-even analysis against your specific payment schedule, investment horizon, and tax situation — before this decision becomes permanent.

Frequently asked questions about lump sum vs. structured settlement

1. Is it better to take a lump sum or structured settlement?

Neither is universally better. A lump sum is the stronger outcome when the offer reaches 80% or more of your payment NPV and you have a documented investment plan in place before signing. Structured payments win when the implied discount rate exceeds 12% or your financial stability depends on guaranteed income. Consult a licensed financial professional before deciding.

2. What discount rate do structured settlement factoring companies use?

Factoring companies in 2026 typically apply discount rates between 9% and 18%, depending on your payment stream’s length and their cost of capital. This rate determines your lump sum offer directly — a higher discount rate produces a lower buyout number. Always calculate the implied discount rate in your specific comparison before accepting any structured settlement buyout offer.

3. Are structured settlement payments tax-free?

Yes. Original structured settlement payments for physical injury or illness are excluded from gross income under IRC Section 104(a)(2), making them fully tax-free at receipt. However, investment gains earned after you deploy a lump sum buyout are taxable at standard capital gains rates. Consult a licensed tax professional for guidance on your specific settlement type and 2026 filing status.

4. Can you invest a structured settlement lump sum?

Yes. Once you receive a lump sum buyout, there are no legal restrictions on investing those tax-free proceeds. Common strategies include index funds, diversified brokerage accounts, and IRA contributions. Your annual return must exceed the factoring company’s implied discount rate to justify the invest lump sum vs structured settlement tradeoff. Consult a licensed financial professional before deploying the proceeds.

5. What return rate do you need to beat your structured settlement?

The required return depends on the discount rate embedded in the offer. A lump sum at 70% of your payment NPV requires approximately 9.8% annual returns to break even — above realistic long-run expectations for most investors. At 60% of NPV, the break-even rises to roughly 13.2% annually. Model your specific offer numbers before committing to any buyout.

6. What happens when you sell your structured settlement?

When you sell, the factoring company files a court petition under your state’s Structured Settlement Protection Act. A judge reviews whether the transaction is in your best interest and can reject the transfer. The full process runs 45 to 90 days from the initial agreement to funding disbursement, depending on the state court calendar and mandatory review period.

7. Is selling a structured settlement worth it?

Selling is worth it only when the offer approaches a fair present value and you have a specific, documented investment plan for the lump sum proceeds. Many recipients accept below-NPV offers without calculating the required break-even return first. A licensed financial professional can model your specific lump sum versus structured settlement numbers before the decision becomes irreversible.

8. How much of a structured settlement can you sell?

You can sell all or a portion of your remaining payment rights. Partial sales — transferring a defined number of future payments while retaining the remainder — are permitted in most states and reduce the total buyout cost relative to a full transfer. Consult a licensed financial professional to determine which structure preserves the most long-term financial value in your situation.

9. Do you pay taxes on a structured settlement lump sum?

The buyout proceeds themselves are tax-free at receipt for physical injury settlements under IRC Section 104. Investment gains earned from deploying those proceeds are taxable at capital gains rates — 0%, 15%, or 20% in 2026 depending on your taxable income. Consult a licensed tax professional for a determination specific to your settlement classification and investment approach.

10. What are the risks of investing a lump sum from a settlement?

Primary risks include market volatility, behavioral risk — spending rather than investing — and sequence-of-returns risk in the early years of deployment. Unlike structured payments, a self-directed portfolio carries no income guarantee. If annual returns fall short of the break-even rate, the lump sum buyout will have cost more than it returned. Consult a licensed financial professional before proceeding.

11. How long does a structured settlement buyout take?

A structured settlement buyout typically takes 45 to 90 days from the initial offer to funding. This includes a mandatory review period of three to five business days in most states, court filing, a judicial hearing 30 to 60 days after filing, and post-approval disbursement. Confirm your state’s specific timeline requirements with independent legal counsel before signing any initial agreement.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.