Sell Structured Settlement Credit Score Guide

Sell structured settlement credit score concerns stem from confusion about FICO reporting, hard inquiries, and mortgage income verification rules.

In This Article

Does selling a structured settlement hurt your credit score?

Selling a structured settlement does not directly hurt your credit score.

The transaction creates no new debt, generates no hard inquiry, and falls entirely outside the categories that consumer credit bureaus are authorized to track.

That may seem counterintuitive for a transaction involving tens of thousands of dollars.

But a credit report tracks one specific category of behavior — how you borrow money and whether you repay it on time.

A structured settlement sale does not involve borrowing.

It transfers payment rights from the original recipient to a factoring company.

No lender extends credit to you. No account opens. No balance appears against your name.

That structural fact is why Equifax, TransUnion, and Experian have no record of the transaction — and it is the starting point for every other answer in this article.

Understanding how structured settlements are legally defined and what changes hands when you sell provides the legal grounding this answer requires.

What actually determines whether a transaction affects your credit

Whether a financial event touches your credit file depends entirely on whether it involves a creditor reporting data to a bureau — not on the dollar amount.

Structured settlement transfers never involve a creditor relationship.

Why so many people get conflicting answers on this question

Factoring companies conduct due diligence before purchasing a payment stream, which some sellers confuse with a credit check.

That review examines the settlement documents and the annuity issuer’s financial stability — not the seller’s credit history.

Why a structured settlement sale doesn’t trigger a credit hit

Your credit report is not a general financial ledger — it is a specific record governed by the Fair Credit Reporting Act.

Only financial institutions with formal furnisher agreements can submit data to the bureaus.

What actually gets reported to Equifax, TransUnion, and Experian

Credit bureaus receive data from lenders, card issuers, and collection agencies — not from companies that purchase future payment streams.

A factoring company that buys structured settlement payments is not a creditor and holds no furnisher agreement with any bureau.

📊 Data Point: The CFPB’s 2026 consumer credit reporting guide identifies five categories of reportable information: credit accounts, payment history, public records, inquiries, and collections. Structured settlement transfers appear in none of these five categories. — Source: Consumer Financial Protection Bureau, 2026.

Why this transaction falls outside the credit reporting framework

The CFPB’s consumer credit reporting guide outlines which financial events qualify as reportable under federal consumer protection law.

A payment rights transfer creates no credit account, triggers no collection action, and generates no public record filing — leaving the bureaus with no mechanism to document it.

Establishing a baseline score before any major financial event is straightforward with the free credit score estimator, giving you a reference point for the months surrounding the sale.

The five FICO factors — and why this sale touches none of them

Every FICO score in 2026 is calculated from exactly five weighted factors.

A structured settlement sale does not interact with any of them — and the table below demonstrates that precisely.

How FICO 9 and FICO 10 score your credit in 2026

📊 Data Point: According to FICO’s 2026 scoring methodology, your score is determined by five factors with the following weights — Source: official FICO score factor breakdown, myfico.com, 2026.

| FICO Scoring Factor | 2026 Weight | Impact of a Structured Settlement Sale |

|---|---|---|

| Payment History | 35% | Zero — no payment record is created or altered |

| Amounts Owed | 30% | Zero — no debt or account balance is generated |

| Length of Credit History | 15% | Zero — no account is opened or closed |

| New Credit | 10% | Zero — no hard inquiry is filed with any bureau |

| Credit Mix | 10% | Zero — no credit product is added to the file |

Source: myfico.com, 2026

Payment history and amounts owed together represent 65% of your total FICO score.

A structured settlement transfer does not create a payment record, does not add to your debt load, and does not generate an inquiry — making the transaction structurally invisible to the FICO algorithm.

What would actually move your score — and why this sale doesn’t

Every event that affects a FICO score shares one feature: a creditor reported data to a credit bureau.

A factoring company never becomes your creditor, never reports to a bureau, and never triggers any of the five weighted factors.

For a complete understanding of how each FICO factor works and what score tiers mean for borrowing power, the complete credit score guide and 2026 credit score tier breakdown cover both scoring mechanics and real-world lending implications.

💡 Expert Note (CFA): In 28 years reviewing client financial files following large liquidity events, I have not seen a single FICO report with an entry attributable to a structured settlement sale. The confusion arises because people conflate a large financial event with a credit event — those are distinct categories with entirely different reporting mechanisms.

The court approval process and what it means for your finances

Every structured settlement sale in the United States requires a judge’s approval before any funds are disbursed.

This mandatory legal step is a consumer protection — and it has no connection to your credit profile.

What the Structured Settlement Protection Act requires

The Structured Settlement Protection Act is a state-level statute enacted across all 50 states and the District of Columbia.

Before a sale proceeds, the factoring company must file a petition with the appropriate state court demonstrating that the transfer serves the seller’s best financial interest.

📊 Data Point: FINRA’s regulatory overview of structured settlements classifies structured settlement annuity payments as a regulated financial product. All transfers of payment rights require judicial authorization under applicable state law. — Source: FINRA, 2026.

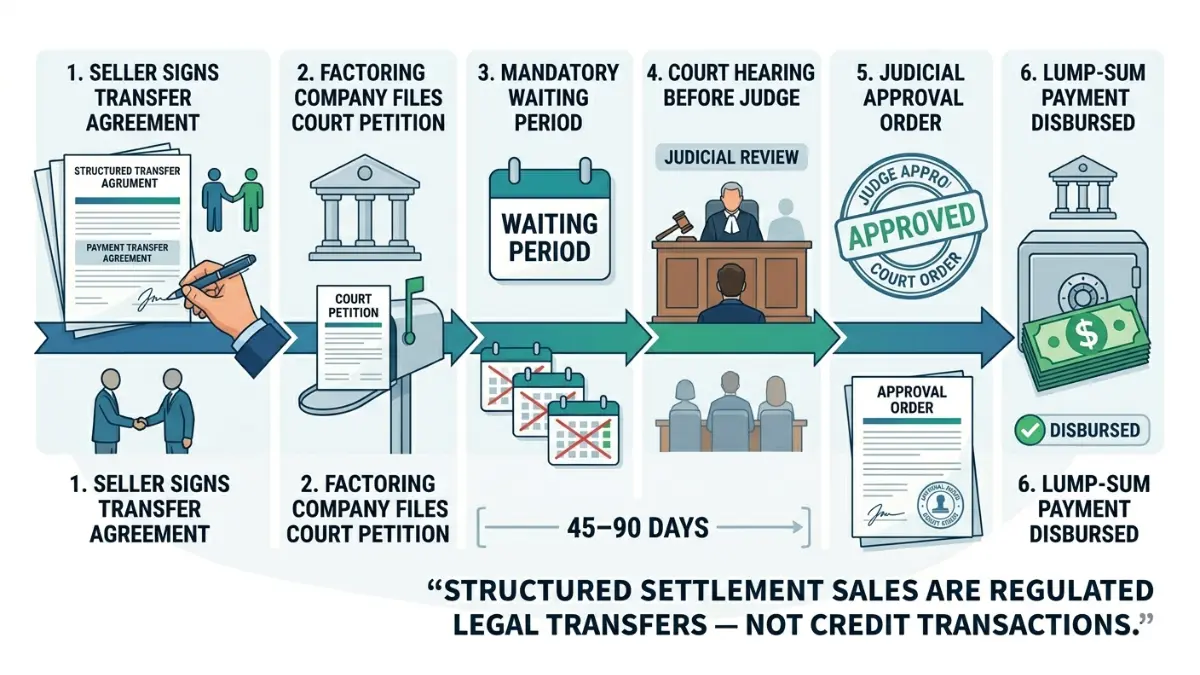

The court approval timeline: what happens and how long it takes

Most structured settlement sales take between 45 and 90 days from signed agreement to funded lump sum.

The timeline depends on state court scheduling, mandatory waiting periods, and annuity provider documentation requirements.

The process follows this sequence:

- Seller reviews and signs the transfer agreement with the factoring company

- Factoring company files a petition with the appropriate state court

- Mandatory waiting period begins — typically 10 to 30 days depending on state law

- Court holds a hearing; a judge evaluates whether the sale serves the seller’s best interest

- Judge issues a written approval order and the qualified assignment executes

- Lump-sum payment is disbursed within 3 to 5 business days of court approval

The article on what to expect at a structured settlement court approval hearing covers each step from petition filing through final disbursement.

Can you sell just part of your structured settlement?

Partial sales — transferring only a portion of future payments while retaining the rest — are permitted in most states.

The IRS guidance on structured settlement proceeds and a full breakdown of which structured settlement payments are taxable address the tax implications of both full and partial transfers in detail.

When to sell — timing the transaction around your credit goals

Selling a structured settlement is credit-neutral — but selling at the wrong moment in your financial timeline can complicate a simultaneous credit-dependent goal.

The most common collision point is a mortgage application.

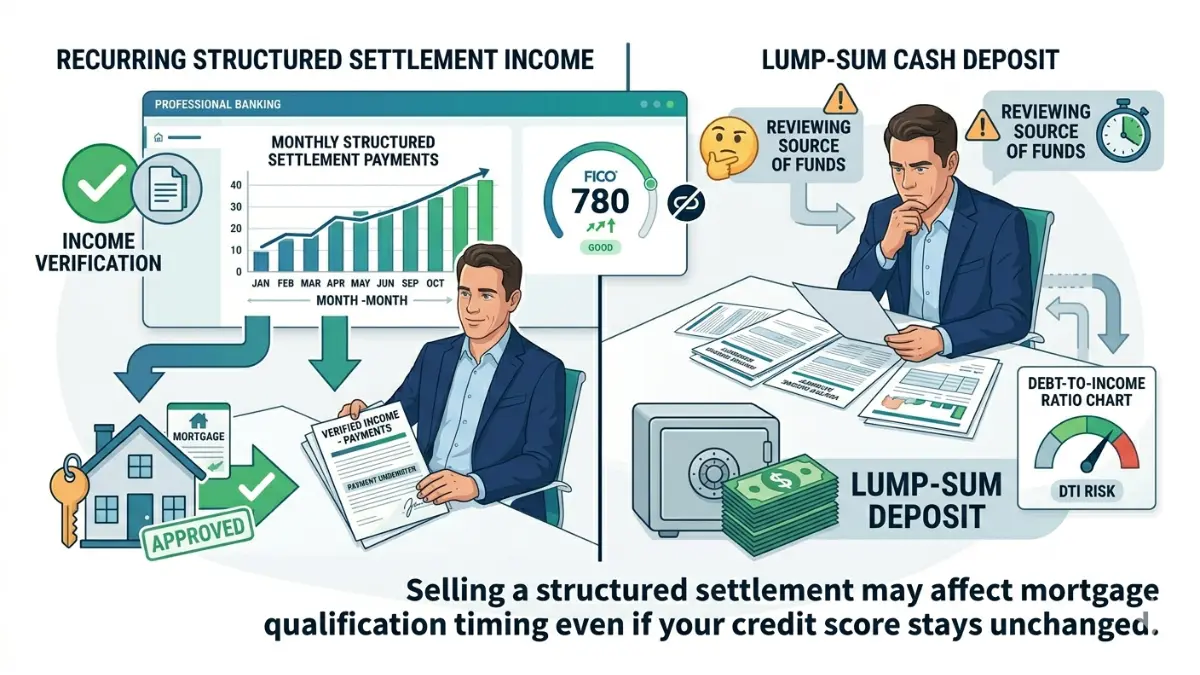

How mortgage underwriters view lump-sum income vs. structured payments

Mortgage lenders do not just evaluate credit scores — they evaluate repayment capacity.

Structured settlement payments function as verifiable recurring income on a mortgage application, carrying similar documentation weight to a pension or annuity.

Converting that recurring income stream into a single lump-sum deposit removes it as a verified income source the moment the court order executes.

⚠️ Warning: If you plan to apply for a mortgage within 12 months of selling, discuss the timing with your lender before signing a transfer agreement. Eliminating a recurring income source may alter your debt-to-income profile and affect loan qualification — even though the sale itself never touches your credit score.

The debt-to-income ratio calculator lets you model how removing a structured payment stream affects your DTI before making a timing decision.

The mortgage payment estimator shows the monthly payment your current income profile supports — and how that changes if a recurring income source is removed from your application.

Should you sell before or after applying for a mortgage?

The right timing depends on your total income picture, the lump sum’s size relative to existing income, and your specific lender’s documentation standards for non-salary income sources.

The minimum credit score requirements for buying a house in 2026 covers current FHA, conventional, and VA loan thresholds — useful context for evaluating your overall mortgage readiness alongside any structured settlement decision.

Three post-sale behaviors that can indirectly damage your credit

The structured settlement sale itself will not move your FICO score by a single point.

What happens to the lump sum in the 12 to 24 months after it arrives is an entirely different matter.

The revolving debt trap: paying down balances and re-accumulating

Using settlement proceeds to pay down credit card balances immediately improves your amounts-owed factor — which accounts for 30% of your FICO score.

Re-accumulating those same balances over the following year creates a visible worsening trend that FICO’s algorithm registers as financial instability.

💡 Expert Note (CFA): In my practice, the most consistent credit damage I see following lump-sum events is not from the sale — it’s from this pattern: use proceeds to zero out revolving balances, feel the financial relief, resume previous spending habits, and rebuild the same debt load within 18 months. The amounts-owed factor reflects every step of that deterioration. Before paying off any revolving account with settlement proceeds, build a written post-payoff spending plan first.

The credit card payoff calculator helps you model whether directing proceeds toward revolving debt produces better long-term outcomes than alternative uses before you commit.

Why a sudden cash influx can trigger unexpected credit changes

A lump-sum deposit does not affect your credit file directly.

But financial confidence following a windfall often leads to new credit applications — and each application generates a hard inquiry that reduces your FICO score by an average of 5 to 10 points.

📊 Data Point: FICO’s 2026 scoring model treats each hard inquiry as a 5- to 10-point score reduction, with impact diminishing after 12 months and disappearing fully after 24 months. — Source: myfico.com, 2026.

How to deploy the lump sum without touching your utilization ratio

Keep all revolving balances below 30% of your total available credit at each statement date — the threshold above which FICO begins applying utilization penalties.

For scores in the 800-plus range, the target is below 10%.

The budget planning tool lets you allocate proceeds across debt payoff, emergency reserves, and savings goals before the money arrives — reducing the likelihood of unplanned spending that erodes financial discipline over time.

The bottom line on structured settlements and your credit score

The answer to the question driving this search is definitive: selling a structured settlement is a credit-neutral event.

The sale creates no debt, triggers no inquiry, and produces no bureau notification — by design.

Key takeaways before you sign anything

Three structural facts explain everything covered in this article:

- A structured settlement transfer is an asset sale, not a debt instrument — credit bureaus track debt behavior only, and this transaction creates none

- Factoring companies review settlement documents and annuity issuer strength — not your credit file — so no inquiry of any kind is ever filed

- The only real credit risks are behavioral — how you manage the lump sum in the months following disbursement determines whether your score is affected

Your next step: three actions before moving forward

Before signing any transfer agreement, take these steps in this order:

- Pull your free credit report at annualcreditreport.com to confirm your current file and establish a pre-transaction baseline

- If a mortgage or major credit application is within 12 months, discuss timing with your lender before executing the transfer

- Consult a licensed financial advisor and a structured settlement attorney before signing — the court approval process protects you, but professional review of your specific situation adds an additional layer

For a complete financial analysis of whether selling makes more sense than retaining the payment stream, the structured settlement vs. lump sum comparison covers long-term income stability, investment trade-offs, and tax implications side by side.

✅ Pro Tip: Pull your credit reports from all three bureaus within 30 days of a completed structured settlement transfer. A sale leaves zero new entries on any report — confirming in writing what this article explains.

Frequently asked questions about selling a structured settlement and your credit score

1. Does selling a structured settlement affect your credit score?

Selling a structured settlement does not affect your credit score. The transaction transfers payment rights — no debt is created, no credit account opens, and no hard inquiry is filed. None of the five FICO scoring factors are triggered, so no entry of any kind appears on your Equifax, TransUnion, or Experian report.

2. Will a structured settlement sale show up on my credit report?

A structured settlement sale does not appear on your credit report. Credit bureaus document activity reported by creditors holding furnisher agreements with the bureaus. Factoring companies are not creditors and have no furnisher relationship with Equifax, TransUnion, or Experian — leaving those bureaus with no mechanism to record the transaction.

3. Does a factoring company run a credit check when buying my structured settlement?

Factoring companies do not run credit checks on structured settlement sellers. Their due diligence focuses on the settlement documents, the payment schedule’s legal validity, and the financial strength of the annuity issuer — not your personal creditworthiness. No hard inquiry or soft inquiry is submitted to any consumer credit bureau during this process.

4. What are the downsides of selling a structured settlement?

The primary downsides of selling a structured settlement are financial, not credit-related. Factoring companies apply a discount rate — typically 9% to 18% in 2026 — meaning you receive substantially less than the total face value of your remaining payments. Permanent surrender of guaranteed future income is the most significant long-term risk to consider.

5. How much do you lose when you sell a structured settlement?

The loss depends on the discount rate applied to your payment stream. At an 18% discount rate, a $100,000 remaining payment stream may yield a lump sum in the range of $74,000 to $82,000, depending on payment timing and duration. Requesting offers from multiple factoring companies is the most reliable way to improve your net result.

6. How long does it take to sell a structured settlement?

Most structured settlement sales take between 45 and 90 days from signed transfer agreement to funded lump sum. The timeline reflects state court scheduling, a mandatory waiting period of 10 to 30 days depending on state law, payment stream complexity, and documentation requirements from the annuity provider.

7. Is the money from selling a structured settlement taxable?

Tax treatment of a structured settlement lump sum depends on the original settlement type. Proceeds from personal physical injury or sickness settlements are generally tax-exempt. Proceeds from punitive damages, employment disputes, or non-physical injury cases may be fully or partially taxable under IRS guidelines applicable to the 2026 tax year.

8. Can I sell only part of my structured settlement?

Partial structured settlement sales are permitted in most states. You can transfer a defined portion of your future payments — such as the next five years — while retaining the remainder of your payment stream. The same court approval process that governs full transfers applies equally to partial structured settlement sales under state law.

9. Does selling a structured settlement affect a mortgage application?

Selling a structured settlement does not hurt your credit score, but it may affect your mortgage borrower profile. Structured payments function as verified recurring income on a loan application. Converting that payment stream into a one-time lump sum removes it as a documented income source — a distinction lenders assess during underwriting, not credit scoring.

10. What is the Structured Settlement Protection Act?

The Structured Settlement Protection Act is a state consumer protection law requiring judicial approval for all structured settlement payment transfers. All 50 states and the District of Columbia have enacted versions of this statute. A judge must confirm that the transfer is in the seller’s best financial interest before any structured settlement sale may proceed.

11. Should I sell my structured settlement before or after applying for a mortgage?

The right timing depends on your income sources, lump-sum size relative to your income profile, and your lender’s standards for documenting non-salary income. Structured payments may strengthen a mortgage application as recurring verified income. Selling before applying removes that income from your borrower file — a variable worth discussing with your lender and a licensed financial advisor before proceeding.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.