Who Really Controls a Minor’s Structured Settlement

Minor’s structured settlement funds are court-locked — parents can’t touch them. The exact rule that controls access and what the 18th birthday unlocks.

In This Article

What is a structured settlement for a minor?

A structured settlement for a minor is a court-approved financial arrangement in which a child receiving injury compensation collects payment in scheduled periodic installments rather than a single lump sum.

Every US state requires judicial oversight for these arrangements — because minors cannot legally enter binding financial agreements on their own behalf.

The court’s role is substantive, not ceremonial.

Judges evaluate whether the proposed payment schedule genuinely serves the child’s long-term financial interest before issuing an approval order.

Most families navigating this process carry four unanswered questions: Who approves the structure? Who controls the money during childhood? Is it taxable? And what happens the day the child turns 18?

Understanding how structured settlements work as a financial baseline matters — but the rules governing minors add court protections and federal tax treatment that change every answer.

Why minor settlements are treated differently under US law

A minor’s inability to contract means any settlement finalized without court approval is legally voidable.

That exposure applies to the defendant, the insurer, and the family — which is why no competent personal injury attorney finalizes a minor’s settlement without a signed judicial order.

The four questions this article answers

Court approval mechanics, parental access restrictions, IRC Section 104 tax treatment, and the three financial decisions at 18 — this article answers each with the regulatory and financial specifics that most general-audience coverage omits entirely.

ℹ️ Disclaimer: The structured settlement and personal injury settlement information in this article is intended for educational purposes only. Tax treatment under IRC Section 104, transfer restrictions under state Structured Settlement Protection Acts, and court approval requirements vary by jurisdiction and individual case facts as of 2026. Consult a licensed structured settlement consultant, a qualified personal injury attorney, and a CPA familiar with personal injury tax rules before making any decision to structure, access, modify, or transfer a minor’s settlement proceeds.

Court approval for a minor’s structured settlement: how it works

In all 50 states, obtaining structured settlement court approval for a minor requires a formal judicial petition — filed by the minor’s parent, legal guardian, or personal injury attorney — before any settlement becomes legally binding.

The court does not simply review the settlement dollar amount.

The petition process: what parents must file and when

Petitioners must submit the proposed compensation amount, the full annuity payment schedule, the present value of the total payment stream, and a financial needs analysis demonstrating how the structure serves the minor’s projected needs.

A college savings calculator can help families build that needs analysis — particularly when part of the payment structure is designed to fund education expenses at a future date.

From filing to court order, the approval timeline typically runs four to eight weeks, depending on jurisdiction, caseload, and whether the court requests supplemental information.

What the court evaluates before approving the settlement

Judges assess four factors: the adequacy of total compensation relative to the injury, the payment schedule’s alignment with the minor’s anticipated needs, the financial strength of the annuity issuer, and whether the minor has independent legal representation through a guardian ad litem.

📊 Data Point: Guardian ad litem fees in minor structured settlement cases — paid by the settling defendant or insurer — typically range from $750 to $3,500 in 2026, depending on case complexity and jurisdiction. Source: State civil court fee schedules and settlement practice standards, 2026.

For more on what courts examine and what happens when a proposed structure is rejected, the CFPB’s overview of structured settlement consumer protections provides a useful regulatory baseline.

For additional detail on how courts handle structured settlement approvals — including petition requirements by settlement size — see the linked resource.

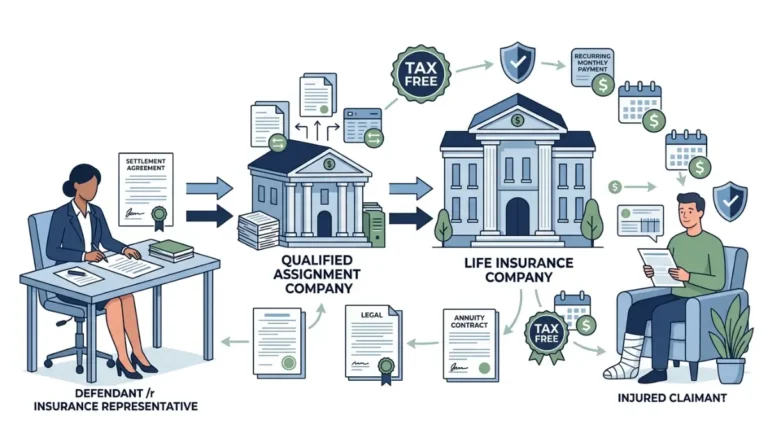

Qualified assignment: how liability transfers from the defendant

A qualified assignment transfers the periodic payment obligation from the defendant to a third-party assignment company, which then funds an annuity through a licensed life insurance carrier.

This structure removes the defendant from ongoing payment responsibility — and is governed by IRC Section 130, which must be satisfied for the tax-free status of payments to remain intact.

💡 Expert Note (CFA): In my work with families negotiating minor settlement structures, the most common petition mistake I see is a payment schedule that front-loads large disbursements before age 18 — often because a parent wants earlier access to funds. Courts are skeptical of these designs. A structure that appears to benefit the parents more than the child will draw direct questions from the judge, and I have seen courts reject petitions on exactly that basis.

The court’s approval order begins the financial protection of the minor’s funds — but it does not answer the question families ask most urgently afterward.

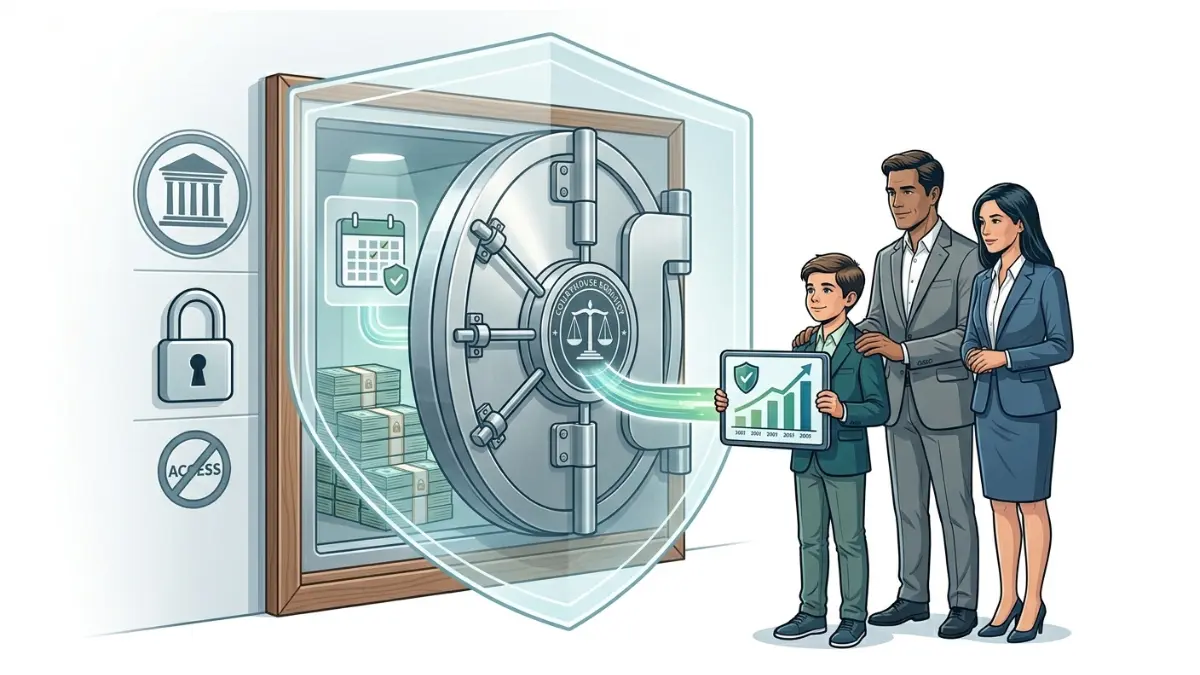

Who controls a minor’s structured settlement funds?

The most financially costly misunderstanding families carry into a minor settlement is the assumption that court approval also grants parental access to settlement funds.

It does not.

Parents vs. guardians: access rights and legal limits

A minor’s structured settlement annuity is issued with the minor as the designated beneficiary, governed by a court protection order that bars parents and guardians from redirecting payments without separate judicial authorization.

Parents who attempt to collect, redirect, or encumber annuity payments without court approval violate the terms of the settlement order — regardless of how the funds will be used.

⚠️ Warning: A parent who redirects periodic annuity payments — even for the minor’s documented medical expenses — without a separate court petition is acting in violation of the settlement order. Courts treat this as a serious breach. Document every financial need and file formally before touching a single payment.

To understand the underlying annuity mechanics and payment structures that govern how periodic payments are held and distributed, the linked resource covers the financial product in detail.

Blocked accounts and custodial annuities: how funds are protected

When a minor’s settlement is paid as a lump sum rather than a structured annuity, courts typically require the funds to be deposited into a blocked account — a court-restricted bank or investment account from which withdrawals require judicial approval.

A savings calculator is useful here: families can model how a blocked account balance grows at a conservative interest rate between settlement date and the minor’s 18th birthday, helping frame the long-term value of leaving funds untouched.

Structured settlement annuities and blocked accounts are not interchangeable instruments — annuities carry scheduled payment obligations from a life insurer, while blocked accounts hold liquid assets subject to market and interest rate risk.

Hardship provisions: when courts may authorize limited access

Some jurisdictions allow parents to petition for limited fund access to cover extraordinary medical expenses, necessary educational costs, or documented living expenses that the minor’s regular income cannot cover.

The petition standard is high, the documentation burden falls entirely on the petitioning parent, and courts grant access narrowly — not as a general household supplement.

💡 Expert Note (CFA): In my experience, the families who navigate hardship petitions most successfully are the ones who document the specific need with medical records or school invoices before filing — not after. A petition that says “we need money for the child’s care” without line-item documentation is almost certain to fail. Specificity is everything in these proceedings.

The access restrictions that apply during the minority period expire automatically when the minor turns 18 — but what happens at that transition is not what most families expect.

What happens at 18: accessing your structured settlement as an adult

When a minor with a structured settlement reaches the age of majority — 18 in most US states — legal control of the annuity transfers automatically to the young adult without any court petition required.

The payment schedule continues exactly as the court originally approved.

The automatic transfer of legal control at the age of majority

At 18, the young adult becomes the sole legal authority over the structured settlement payment stream.

They can instruct the annuity issuer to update contact and banking information, name or update beneficiaries, and initiate the legal processes required to modify or sell the payment rights — subject to state SSPA restrictions covered in Section 6.

Your three financial options at 18: keep, modify, or sell

The three paths available at 18 carry very different financial outcomes, and the decision is among the most consequential a young adult will make.

The first option — keeping the payment schedule as approved — is typically the most financially efficient choice because the annuity was structured to deliver maximum value over time at a guaranteed rate.

The second option — petitioning to modify the payment schedule — requires a court filing and approval, is infrequently granted, and is appropriate primarily when the original schedule no longer fits documented financial circumstances.

The third option — petitioning to sell some or all payment rights — is discussed in depth in Section 6, but the short version is this: most factoring company offers deliver 40–60 cents on the dollar of the full payment stream’s present value.

Evaluating the full financial picture of these three options starts with running the numbers. An investment calculator can model what a lump sum offer from a factoring company could realistically grow to over 20 years — the comparison against simply keeping the annuity is often decisive. For a fuller analysis of the structured payment vs. lump sum trade-off, the linked article covers the decision framework in detail.

Building a financial plan around periodic settlement income

Periodic annuity income is not like a paycheck — it does not automatically grow, and it is not compounding unless the recipient actively invests it alongside other income.

A compound interest calculator illustrates the difference between receiving $1,500 per month and spending it versus investing a portion of it over a 20-year period — a comparison that consistently changes how young adults approach their first year of direct payment access. A budget calculator built around the specific payment amount and frequency is a practical first step for any 18-year-old receiving their first independent annuity payment.

✅ Pro Tip: Before the 18th birthday, request a full annuity policy summary from the issuing insurance company. Confirm the payment schedule, total remaining benefit, beneficiary designations, and the insurer’s AM Best financial strength rating — all in writing. This takes 15 minutes and eliminates the most common administrative surprises at the transition point.

📊 Data Point: The CFPB provides financial planning resources for young adults navigating their first independent financial decisions, including how to approach periodic income streams. Source: Consumer Financial Protection Bureau, 2026.

The payment schedule is clear and the financial options are defined — but one critical question remains before any decision is made at 18: are those payments taxable?

Are structured settlement payments tax-free after 18?

Yes — and the reason matters more than the answer itself.

IRC Section 104(a)(2) excludes from gross income all damages received “on account of personal physical injuries or sickness,” regardless of the recipient’s age, the number of payments, or the total amount received.

IRC Section 104: the personal injury tax exclusion explained

The tax-free status of a structured settlement is tied to the origin of the claim — the fact that the compensation arose from a personal physical injury — not to the recipient’s status as a minor.

This means a 22-year-old who has been receiving structured settlement payments for a decade is in exactly the same tax position as the 8-year-old who first received them: the payments are excluded from gross income under federal law.

📊 Data Point: The IRS confirms under Topic 431 — Compensatory Damages that compensatory damages received for personal physical injury or sickness are excluded from gross income under IRC Section 104. Source: Internal Revenue Service, 2026.

For additional context on how structured settlement payments are taxed across different claim types — including workers’ compensation and emotional distress cases where the tax treatment differs — the linked article covers the distinctions in detail.

Does the exclusion survive the 18th birthday?

It does — with no action required by the recipient.

The 18th birthday does not create a taxable event, does not trigger any IRS reporting requirement on the structured settlement payments themselves, and does not require the young adult to file any new documentation with the annuity issuer or the IRS.

💡 Expert Note (CFA): The misunderstanding I encounter most frequently in this area — among both clients and, frankly, some general financial writers — is the assumption that the IRC 104 exclusion is tied to minor status. It is not. The exclusion is tied to the physical injury origin of the claim. A 35-year-old still receiving payments from a childhood injury settlement does not owe income tax on those payments. That distinction is critical, and getting it wrong costs clients in unnecessary withholding and overstated gross income.

What happens if payments are modified or sold: the tax risk

Here is where the tax picture changes.

If a structured settlement recipient sells some or all of their payment rights to a factoring company, the lump sum received in exchange may not qualify for the same IRC Section 104 exclusion — creating a potential taxable event that the factoring company’s advertising materials rarely disclose.

The IRS has made clear that the factoring transaction itself is a separate financial event from the original settlement, and its tax treatment depends on the specific facts of the transfer.

Any recipient considering a sale should consult a CPA familiar with IRC Section 104 and factoring transactions before proceeding. Using an income tax calculator to estimate the potential tax exposure on a lump sum factoring payment — compared to the ongoing tax-free status of keeping the annuity — is a useful starting exercise.

Can a minor’s structured settlement be sold or changed?

The short answer is no during the minority period — and yes after 18, but only through a court-approved transfer process that most factoring company ads do not accurately describe.

SSPA requirements: state court approval before any sale

Every US state has enacted a Structured Settlement Protection Act (SSPA) that requires a court order before any transfer of structured settlement payment rights can take effect — regardless of whether the recipient is a minor or an adult.

For a structured settlement that originated as a minor’s settlement, courts apply heightened scrutiny: judges must affirmatively find that the proposed transfer is in the seller’s best financial interest, considering their age, financial circumstances, and the specific terms of the offer.

The court process for a sale typically runs 30 to 90 days, requires independent legal counsel for the seller, and involves a hearing at which the judge can — and frequently does — reject proposed transfers that are not financially justified.

For a detailed breakdown of the full sale process, costs, and state-specific court requirements, selling structured settlement payments covers the mechanics step by step.

The IRC 5891 excise tax and what it costs factoring companies (and you)

IRC Section 5891 imposes a 40% excise tax on any factoring company that purchases structured settlement payment rights without a qualifying court order.

This federal penalty is why factoring companies always seek court approval — not because they’re protecting the seller’s interest, but because bypassing the process costs them 40 cents on every dollar of payment rights they acquire.

📊 Data Point: The IRS confirms the 40% excise tax on structured settlement factoring transactions under IRC Section 5891 — applicable to transfers that do not meet qualified order requirements. Source: Internal Revenue Service, 2026.

⚠️ Warning: Any factoring company that contacts you directly, creates urgency around your decision, or discourages you from seeking independent legal counsel is exhibiting behavior the courts treat as a red flag. A legitimate factoring transaction requires a 30–90 day court process. Any offer framed as faster than that is not following the law.

Present value math: why most factoring offers are 40–60 cents on the dollar

A factoring company calculates the present value of your remaining payment stream using a discount rate — typically 9% to 18% in the current rate environment — and offers you a lump sum significantly below that present value.

To illustrate with a representative 2026 scenario: a $1,500-per-month payment stream continuing for 20 years has a future value of $360,000 and a present value of approximately $165,000–$185,000 at a 9–12% discount rate. A factoring company offering $120,000 for that stream is offering roughly 65–73 cents on the present value dollar — and considerably less against the full future value.

Running the math yourself before any meeting with a factoring representative is not optional. An inflation calculator helps frame the real purchasing power of future payments relative to today’s lump sum offer, and the structured settlement discount rate article explains exactly how factoring companies calculate the discount they apply to your stream.

💡 Expert Note (CFA): In 28 years of financial analysis, I have not encountered a factoring offer that represents better financial value than simply keeping the annuity — for a healthy recipient with no acute financial emergency. The cases where selling makes financial sense are narrow and specific: a documented irreversible financial crisis, no other liquid assets, and a factoring offer that has been reviewed by an independent financial advisor before signing. The default position should always be to keep the payments.

The right financial decisions start with understanding what you actually own

A minor’s structured settlement is one of the most legally and financially protected instruments in personal finance — protected precisely because the stakes of getting it wrong are permanent.

The court approval process, the parental access restrictions, the IRC Section 104 tax-free status, and the SSPA sale protections all exist to preserve one thing: the financial outcome for a child who cannot yet protect it themselves.

Three decisions define whether the protection holds. First: whether the initial structure was designed for the child’s real long-term needs, not for administrative convenience. Second: whether the access rules during the minority period are respected, not circumvented. Third: whether the 18-year-old makes a fully informed decision about keeping, modifying, or selling — with real present value math, not a factoring company’s sales materials.

For families within one to two years of a minor’s 18th birthday, now is the right time to begin that financial planning conversation. A retirement calculator can help frame how the structured settlement fits into the young adult’s longer-term financial picture — particularly if they plan to let the payments run alongside investment contributions for the next two to three decades.

Work with a licensed structured settlement consultant, a qualified personal injury attorney, and a CPA before making any decision to structure, access, or transfer these funds. The financial protection the court built takes years to construct and minutes to undo.

Frequently asked questions about structured settlements for minors

1. What happens to a structured settlement when a minor turns 18?

At 18, legal control of a structured settlement for a minor transfers automatically to the young adult — no court petition is required for this transition alone. Payments continue on the original court-approved schedule. The recipient then has legal authority to keep, petition to modify, or — subject to state SSPA court approval — petition to sell the payment rights.

2. Do parents have access to a minor’s structured settlement?

Generally no. A structured settlement for a minor is protected by a court order that bars parents and guardians from redirecting payments without filing a separate petition demonstrating specific, documented financial necessity. Courts apply a high evidentiary standard for access approvals and do not grant them as a routine matter for household expenses.

3. Do structured settlements for minors require court approval?

Yes — in all 50 states, a structured settlement for a minor requires a judicial approval order before it becomes legally binding. Courts evaluate the compensation adequacy, the payment schedule, the annuity issuer’s financial strength, and whether the minor has independent representation. Approval cannot be waived by the parties.

4. Is a structured settlement for a minor tax-free?

Yes. Under IRC Section 104(a)(2), payments received as compensation for personal physical injury are excluded from gross income regardless of the recipient’s age. A structured settlement for a minor carries tax-free status determined by the physical injury origin of the claim — not by the recipient’s minor status. That status continues through every scheduled payment.

5. Who controls a minor’s structured settlement?

The annuity issuer holds and manages the payment obligation. The minor is the designated beneficiary, governed by a court protection order during the minority period. Parents and guardians have no unilateral authority over payments. At 18, the young adult assumes full legal control of the structured settlement and all associated payment rights.

6. What is a guardian ad litem in a structured settlement?

A guardian ad litem is a court-appointed independent representative who reviews the proposed structured settlement terms and submits a formal recommendation to the judge on whether the arrangement serves the minor’s best financial interest. The GAL is not selected by the family. Guardian ad litem fees in minor settlement cases typically range from $750 to $3,500 in 2026, paid by the settling defendant.

7. Can a minor’s structured settlement be sold?

A structured settlement for a minor cannot be transferred during the minority period under any circumstances. After the recipient turns 18, a sale of payment rights requires a court order under the applicable state Structured Settlement Protection Act, finding the transfer is in the seller’s best interest. The IRS also imposes a 40% excise tax under IRC Section 5891 on transfers without a qualifying court order.

8. What is a blocked account in a minor’s settlement?

A blocked account is a court-ordered bank or investment account that holds a minor’s lump-sum settlement funds with restricted withdrawal access. Unlike a structured settlement annuity — which schedules periodic payments from a life insurer — a blocked account holds liquid assets subject to market conditions. Withdrawals require a separate court petition. The account releases to the minor’s full control at age 18.

9. Can a structured settlement for a minor be changed after court approval?

Modifying a structured settlement for a minor after judicial approval is possible but rarely granted. Courts require a new petition, documented evidence of changed financial circumstances, and a finding that the modification serves the minor’s interest. The original approval process is designed to produce a final protective arrangement — courts do not treat it as an adjustable starting point.

10. How much does a guardian ad litem cost in a structured settlement?

Guardian ad litem fees in a structured settlement for a minor typically range from $750 to $3,500 in 2026, depending on case complexity and jurisdiction. Fees are generally paid by the defendant or insurer as a settlement cost — not by the family. If the case requires a contested hearing or expert review of the annuity structure, GAL fees can exceed this range.

11. What is a qualified assignment in a minor’s structured settlement?

A qualified assignment transfers the periodic payment obligation in a structured settlement for a minor from the defendant to a third-party assignment company, which funds the annuity through a licensed life insurance carrier. The assignment removes the defendant’s ongoing payment liability. It must satisfy IRC Section 130 requirements for the payments to preserve their tax-free status under IRC Section 104.

12. Are structured settlement payments taxable income for a minor?

No. Structured settlement payments arising from a personal physical injury claim are excluded from the minor’s gross income under IRC Section 104(a)(2). The IRS does not treat these payments as taxable income regardless of the child’s age, payment frequency, or total benefit amount. The exclusion applies to the full payment stream as long as the underlying claim was for physical injury.

13. What happens if a minor dies before receiving all structured settlement payments?

If a minor with a structured settlement dies before collecting all scheduled payments, remaining payment rights pass to the named beneficiary or the minor’s estate, depending on the annuity contract terms. The tax treatment of payments received by an estate or alternate beneficiary depends on the specific contract and claim facts — a CPA and estate attorney should be engaged immediately.

14. Can an 18-year-old sell their structured settlement immediately?

Not without court approval. State Structured Settlement Protection Acts require a court order confirming the transfer is in the seller’s best interest before any sale of structured settlement payment rights takes effect — even after the recipient turns 18. Courts must weigh the seller’s age, financial situation, and the discount offered. The IRS imposes a 40% excise tax under IRC Section 5891 on any transfer that bypasses this process.

15. How long does a structured settlement for a minor last?

A structured settlement for a minor lasts exactly as long as the payment schedule the court approved at settlement. Structures range from defined-term arrangements — such as 10 or 20 annual payments — to lifetime annuities. Some are designed with milestone payments at educational transition ages. The payment structure is fixed at approval and cannot be extended or shortened without a new court petition.

16. What court approves a minor’s structured settlement?

A structured settlement for a minor is approved by the superior court or probate court in the county where the minor resides, depending on state procedural rules. In some jurisdictions, family court handles the petition. Your personal injury attorney files in the correct court as part of the settlement finalization — the family does not initiate this process independently.

17. What is the difference between a structured settlement and a custodial account for a minor?

A structured settlement for a minor delivers injury compensation through a scheduled annuity with court oversight and IRC Section 104 tax-free status on payments. A custodial account (UTMA or UGMA) holds assets the child legally owns, managed by an adult custodian until adulthood. Settlement payments carry no income tax; custodial account investment earnings are generally subject to the kiddie tax rules.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.