What the SSPA Requires for Structured Settlement Court Approval

Structured settlement court approval: a 40% federal penalty hangs over every transfer. Here’s what the SSPA and judges actually require.

In This Article

Why every structured settlement transfer requires a court’s approval

Every structured settlement transfer in the United States requires a judge’s approval before a single dollar changes hands.

This is not optional, not procedural, and not something a factoring company can legally waive on your behalf. The requirement is federal and state law — enforceable in all 50 states and Washington, DC — and understanding exactly what the court demands is the most protective step you can take before this process begins.

The law that made court approval mandatory in all 50 states

State Structured Settlement Protection Acts, reinforced by federal tax law, require judicial oversight of every structured settlement transfer without exception. Before exploring what the court requires, it helps to understand what structured settlements pay and cost over time — because the court’s job is to protect that long-term income on your behalf.

What you risk if the process is misunderstood

Most payees enter this process under financial pressure, accept the first offer they receive, and arrive at the court hearing without the documentation a judge will specifically examine. This article gives you the exact framework courts apply — so you walk into the hearing with the same information the buyer’s attorney already has.

ℹ️ Disclaimer: The structured settlement transfer information in this article is provided for educational purposes. Structured settlement transfers are regulated legal and financial transactions governed by state Structured Settlement Protection Acts and federal Internal Revenue Code Section 5891. Timelines, judicial standards, and document requirements vary by state and individual financial circumstance. Before signing any transfer agreement or appearing at a court hearing related to a structured settlement transfer, consult a licensed financial professional — such as a CFA or CFP — and a qualified attorney with structured settlement experience in your state.

What the SSPA actually requires before any transfer closes

The Structured Settlement Protection Act (SSPA) is a state consumer protection law that requires court approval before any structured settlement transfer can legally close — adopted in all 50 states and Washington, DC. Every SSPA statute requires a judge to find, in writing, that the transfer is in the financial best interest of the payee before issuing the qualifying order that allows the transfer to proceed.

The federal rule: IRC Section 5891 and why the 40% excise tax exists

IRC Section 5891 of the federal tax code imposes a 40% excise tax on any buyer who completes a structured settlement transfer without a court-issued qualifying order. The tax falls on the buyer — not the payee — meaning every legitimate factoring company has a direct financial incentive to complete the court process correctly and completely.

📊 Data Point: IRC Section 5891’s 40% excise tax on structured settlement transfers completed without a qualifying court order is assessed on the gross transfer amount and has been in force since 2002. It remains applicable for all 2026 tax year transfers. — Source: Internal Revenue Service, Structured Settlement Factoring Transactions

This dual-layer framework — state SSPA procedure plus federal excise tax enforcement — is what makes court oversight non-negotiable in every state, regardless of how detailed that state’s SSPA statute is.

What every state SSPA must require under the federal framework

Every state SSPA mandates three specific court findings before any transfer agreement can close: the transfer is in the payee’s best interest, the payee received independent professional advice, and the transfer does not violate any applicable statute or existing court order. Understanding how annuities fund your settlement payments clarifies why the annuity issuer and obligor are required parties to every SSPA court proceeding — their legal interests are also subject to judicial review.

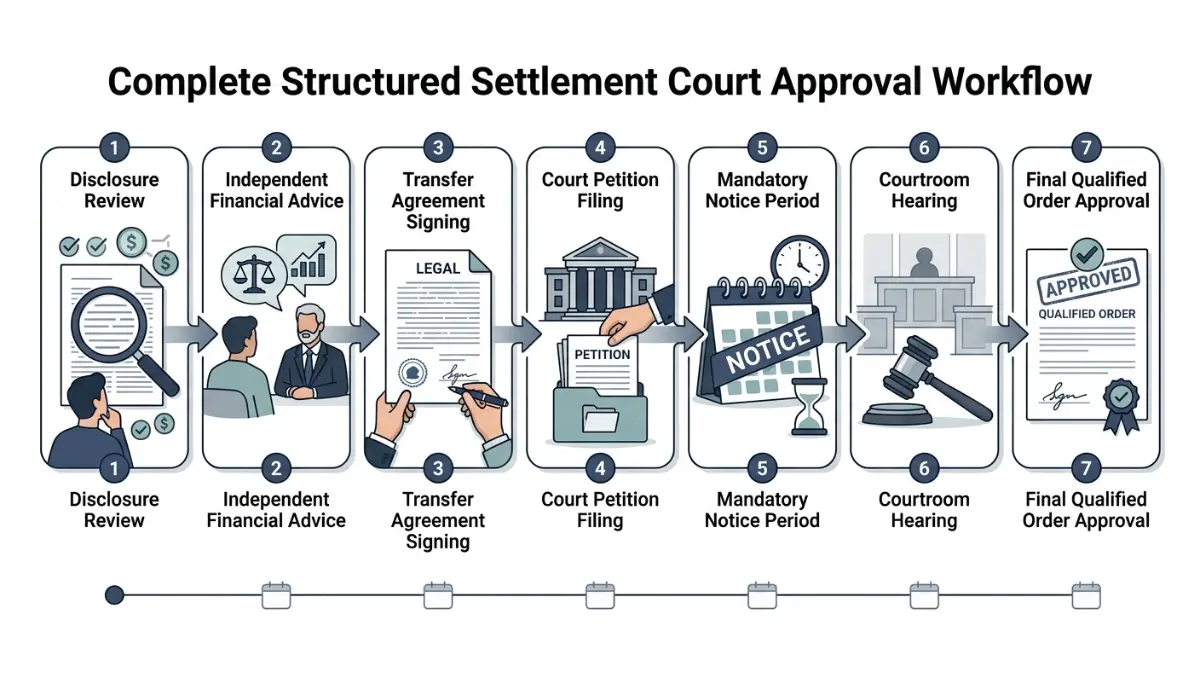

How the structured settlement court approval process works, step by step

The court approval process for a structured settlement follows seven steps, with a total timeline ranging from 20 to 90 days depending on your state’s SSPA notice and hearing requirements.

Steps 1–3: Before the petition is filed (buyer obligations and your rights)

- Receive the buyer’s written disclosure — including the discount rate applied, the gross advance amount, and the net advance amount — before signing anything. This disclosure is legally required under state SSPA statutes and must precede your signature on the transfer agreement.

- Obtain independent professional advice from a financial or legal professional who has no financial relationship with the buyer. Most state SSPAs require this advice be provided in writing specifically before the transfer agreement is signed.

- Execute the transfer agreement only after completing steps 1 and 2. Once signed, the financial terms — including the discount rate — are locked and cannot be renegotiated.

💡 Expert Note (CFA): In reviewing transfer agreements for clients, the single most costly mistake I see is signing at Step 3 before genuinely completing Step 2. By the time the petition is filed, the discount rate the client accepted determines every dollar they will receive — and the buyer has no legal obligation to revisit it.

Steps 4–7: The petition, notice period, hearing, and qualified order

- Buyer files the court petition, naming you, the annuity issuer, and the obligor as required parties.

- Mandatory notice period runs — typically 20 to 60 days depending on your state’s SSPA.

- Court hearing convenes — the judge reviews your financial need, the transfer terms, and whether the best interest standard is satisfied.

- Qualified order issued — the court’s written approval satisfies both the state SSPA and federal IRC Section 5891, and the transfer legally closes.

What to bring to your structured settlement court hearing

Bring these documents — the judge may request any of them:

- Original settlement agreement and the court order that established it

- Signed transfer agreement and the buyer’s written SSPA disclosure statement

- Documentation of your stated financial need — medical bills, bank statements, or creditor notices

- Written confirmation that you received and reviewed independent professional advice

Use a budget calculator to document your monthly income and expense gap before the hearing — concrete numbers carry more weight than verbal descriptions alone. For the broader picture of the full process of selling structured settlement payments, including what happens after the qualified order is issued, see our dedicated guide.

What judges evaluate: the best interest standard explained

The SSPA best interest standard is the legal threshold every state court must satisfy before approving a structured settlement transfer. Courts deny petitions regularly — and the grounds follow a consistent pattern that every payee should understand before the hearing date.

The 5 factors most SSPA statutes require judges to weigh

| Factor | What the Judge Examines | What Strengthens Your Case |

|---|---|---|

| Financial need | Documented emergency vs. stated need | Medical records, creditor notices, bank statements |

| Purpose of funds | Protective or productive use vs. discretionary spending | Written explanation with supporting documentation |

| Discount rate | Reasonableness relative to the 2026 market range | Evidence you obtained two or more competing offers |

| Independent advice | Whether genuinely received and understood | Written acknowledgment from the advising professional |

| Dependent impact | Effect on financially dependent household members | Post-transfer monthly budget showing remaining income plan |

💡 Expert Note (CFA): Judges may ask whether you understand what the discount rate costs you numerically. At a 15% rate on a 20-year, $10,000-per-year payment stream, your lump sum is roughly $13,000 lower than at a 9% rate. Knowing that gap — and being able to explain it — signals the court that you made an informed decision rather than an uninformed one.

The most common grounds on which judges deny structured settlement transfers

Courts deny structured settlement transfers based on four consistent patterns:

- Undocumented need — a financial emergency is stated but not supported by bills, records, or bank statements

- Unread independent advice — an acknowledgment was signed but the payee cannot explain what the advisor communicated

- Above-market discount rate — the rate applied exceeds what the court finds commercially reasonable in the 2026 market

- Discretionary purpose — funds are intended for a use that the judge finds does not justify permanent loss of long-term income

⚠️ Warning: A denied petition is not final — but re-filing adds months to your timeline and additional legal fees. Addressing denial grounds before your first hearing costs significantly less than correcting them in a second proceeding.

If a personal loan might address your financial need at lower total cost, use a loan calculator to compare total borrowing cost against the income you would permanently surrender. For a complete breakdown of what it costs to sell structured settlement payments, see our dedicated cost guide. Review the CFPB’s guidance on evaluating high-stakes financial decisions before agreeing to any terms.

What the court approval process will actually cost you in 2026

The discount rate is the single largest financial cost of any structured settlement transfer — larger than court fees, attorney costs, and processing charges combined. In 2026, factoring companies apply discount rates ranging from 9% to 18% when converting future payment streams to a lump sum today.

Discount rates and present value: the real cost of your lump sum

A $10,000 annual payment for 15 years has a present value of approximately $65,000 at a 9% discount rate — and approximately $52,000 at a 15% rate. That $13,000 gap reflects the real cost of accepting a higher rate without obtaining competing offers first.

📊 Data Point: The 9%–18% discount rate range cited in this section represents a representative analytical range based on available 2026 structured settlement market data. This is not a guaranteed offer range. Verify the specific rate in any transfer agreement with a licensed financial professional before signing, and request the present-value calculation in writing.

For a detailed explanation of how the discount rate determines your lump sum and how to evaluate competing offers side by side, see our full guide. Use a compound interest calculator to model what your lump sum could earn over time — it gives the court a more complete picture of your long-term financial plan.

Court filing fees, attorney costs, and buyer charges in 2026

| Cost Category | Typical 2026 Range | Key Consideration |

|---|---|---|

| Court filing fees | $150 – $500 | Varies by state and county court |

| Independent legal representation | $500 – $2,500 | Optional but strongly recommended |

| Buyer processing and admin fees | $0 – $750 | Request itemized disclosure before signing |

| Net proceeds as % of face value | ~45% – 75% | Depends on discount rate and payment stream length |

Source: Representative 2026 ranges. Verify all fees in writing with your buyer before executing the transfer agreement.

Federal tax rules and state SSPA laws that govern every transfer

IRC Section 5891 imposes a 40% federal excise tax on any buyer who completes a structured settlement transfer without a court-issued qualifying order — calculated on the gross transfer amount, not the net. This penalty is the mechanism that makes court compliance financially non-negotiable for every legitimate factoring company operating in the United States.

How IRC Section 5891 protects you even if your state’s SSPA has gaps

The federal excise tax functions as a floor of consumer protection across all 50 states. Even in states with less procedurally detailed SSPA statutes, the 40% penalty ensures no legitimate buyer bypasses judicial oversight.

📊 Data Point: IRC Section 5891’s 40% excise tax is assessed on the transferee (buyer) based on the gross transfer amount for any structured settlement transfer completed without a qualifying court order. The rate has not changed since the provision’s enactment and remains in force for 2026. — Source: Internal Revenue Service, Structured Settlement Factoring Transactions

State SSPA timeline variations: what changes depending on where you live

State SSPA timelines vary — which directly determines when you receive your lump sum:

| State Tier | Required Notice Period | Approx. Total Timeline |

|---|---|---|

| Tier 1 — Streamlined (e.g., TX, FL) | 20 – 30 days | 20 – 40 days total |

| Tier 2 — Standard (e.g., IL, CO) | 30 – 45 days | 36 – 60 days total |

| Tier 3 — Extended (mandatory counseling required) | 45 – 90 days | 60 – 90+ days total |

Note: State SSPA statutes are subject to legislative change. Verify your state’s current requirements with a licensed legal professional before proceeding.

Before finalizing any transfer, confirm whether your structured settlement proceeds are taxable — the transfer structure can affect tax treatment in ways the buyer’s disclosure will not explain.

The steps to take before signing any transfer agreement

A structured settlement transfer is a permanent financial decision — and three specific actions taken before any petition is filed will define your outcome both in court and at the negotiating table.

Three questions to ask any buyer before agreeing to transfer terms

Require written answers to each of these before executing the transfer agreement:

- What is your discount rate — and can you provide the present-value calculation that produced it?

- What is the total net amount I will receive after every court, processing, and attorney fee is deducted?

- How many petitions have you filed in my state’s specific courts, and what was the most recent court outcome?

Buyers who hesitate to answer these in writing are signaling something important about how they operate.

Your next step: connect with a licensed financial professional

💡 Expert Note (CFA): The clients who navigate structured settlement transfers most successfully treat the process as a financial negotiation — not a formality. They obtain competing offers, understand the discount rate in present-value terms, and arrive at the hearing with a written financial plan that demonstrates the transfer serves their long-term interest. Judges consistently distinguish between a prepared payee and an uninformed one — and so do the buyers setting the discount rate.

Compare verified structured settlement buyers before agreeing to any terms — the 2026 discount rate market range is wide enough that the right comparison can meaningfully change your net proceeds. Understand the full financial case for keeping vs. selling your settlement before committing to any terms.

Use a retirement calculator to model the long-term income impact of surrendering your periodic payments — this calculation frequently changes how much of the settlement a client decides to sell. For additional consumer resources, the CFPB’s free financial decision tools are available at no cost before your hearing date.

Frequently asked questions about structured settlement court approval

1. What is structured settlement court approval?

Structured settlement court approval is the mandatory judicial review required before any structured settlement transfer legally closes. Every state’s Structured Settlement Protection Act requires a judge to find the transfer serves the payee’s financial best interest before issuing the qualifying order. This requirement applies in all 50 states and Washington, DC.

2. Is court approval required to sell structured settlement payments?

Yes — structured settlement court approval is required in all 50 states and Washington, DC under state SSPA statutes. Without a court-issued qualifying order, the buyer faces a 40% federal excise tax under IRC Section 5891. No legitimate factoring company will attempt a transfer without pursuing court approval first. The process is mandatory, not optional or negotiable.

3. What does SSPA stand for in structured settlements?

SSPA stands for Structured Settlement Protection Act — a state consumer protection law adopted in all 50 states and Washington, DC. It requires judicial review of every structured settlement transfer before it closes, protecting payees from exploitative discount rates and financially harmful terms. Federal IRC Section 5891 reinforces state SSPA requirements with a 40% excise tax penalty on non-compliant buyers.

4. How long does court approval take for a structured settlement?

Structured settlement court approval typically takes 20 to 90 days from petition filing to the judge’s qualifying order. States with streamlined procedures complete the process in approximately 20 to 35 days. States requiring extended notice periods or mandatory counseling sessions can take 60 to 90 days or longer. Confirm your state’s current timeline with a licensed financial or legal professional.

5. How much does structured settlement court approval cost?

Court filing fees typically range from $150 to $500. Independent legal representation adds $500 to $2,500. Buyer processing and admin fees range from $0 to $750. Together, these transaction costs reduce your structured settlement net lump sum by an additional 2% to 5% beyond the discount rate applied.

6. What does a judge look for in a structured settlement transfer?

Under the SSPA best interest standard, judges evaluate documented financial need, whether independent professional advice was genuinely received and understood, the commercial reasonableness of the discount rate, the payee’s age and dependent circumstances, and statutory compliance. Courts are not rubber stamps.

7. Can a judge deny a structured settlement transfer?

Yes — judges deny structured settlement transfers that fail the best interest standard. Common grounds include undocumented financial need, a commercially unreasonable discount rate, evidence of buyer pressure, and failure to demonstrate genuine receipt of independent professional advice. A denied petition can be re-filed after addressing the court’s stated deficiencies.

8. What is the best interest standard for structured settlements?

The best interest standard is the legal threshold every SSPA court must clear before approving a structured settlement transfer. A judge must affirmatively find the transfer serves the payee’s — and any dependents’ — financial best interest, weighing documented need, purpose of funds, available alternatives, and the discount rate. Approval is never automatic.

9. Do I need a lawyer for structured settlement court approval?

Legal representation is not universally required for structured settlement court approval but is strongly recommended. The buyer’s attorney represents the buyer, not you. An independent attorney or licensed financial professional can review the transfer agreement, evaluate the discount rate, and represent your interests at the hearing. Self-represented payees are permitted in most states, but professional guidance consistently improves outcomes.

10. What is IRC Section 5891 and how does it affect my structured settlement?

IRC Section 5891 is the federal tax provision imposing a 40% excise tax on any structured settlement transfer completed without a court-issued qualifying order. The tax falls on the buyer, not the payee. It is the primary mechanism ensuring every legitimate factoring company pursues court approval.

11. What happens if a structured settlement is transferred without court approval?

A buyer who completes a structured settlement transfer without a qualifying court order faces a 40% federal excise tax on the gross transfer amount under IRC Section 5891. The transfer may also be void under state SSPA law. No legitimate factoring company accepts this risk.

12. How many times can I sell my structured settlement payments?

There is no federal statutory limit on structured settlement transfers, but each transfer requires separate court approval under the applicable state SSPA. Some states apply heightened judicial scrutiny to repeat transfers. Each transfer carries its own discount rate, costs, and net proceeds calculation. Judges in repeat-transfer cases often apply a stricter best interest analysis.

13. What documents do I need for structured settlement court approval?

Required documentation for structured settlement court approval typically includes the original settlement agreement, the proposed transfer agreement, the buyer’s written disclosure statement showing the discount rate and net advance, documentation of financial need, and written confirmation that independent professional advice was received. Specific requirements vary by state.

14. Can I sell all of my structured settlement payments at once?

Yes — a full transfer of all remaining structured settlement payments can be petitioned in a single court proceeding. However, judges scrutinize full transfers more carefully than partial ones, since a complete transfer eliminates all future income security for the payee. The best interest standard is applied more stringently in these cases.

15. What is a discount rate in a structured settlement transfer?

The discount rate is the annualized rate a factoring company uses to calculate the present value of your future structured settlement payments — determining your lump sum today. In 2026, discount rates typically range from 9% to 18%. A higher rate means a lower offer. Obtain at least two competing offers before accepting any rate.

16. What are the most common reasons a judge denies a structured settlement transfer?

The most documented denial grounds for structured settlement court approval are failure to prove genuine financial need with documentation, failure to demonstrate genuine receipt of independent professional advice, a discount rate the court finds commercially exploitative, and a stated purpose for funds that does not justify permanent income loss. Each denied petition can be re-filed.

17. Are proceeds from a structured settlement transfer taxable?

Under current federal tax law, lump-sum proceeds from a structured settlement transfer are generally excluded from gross income for the original payee, consistent with the tax-exempt status of the underlying personal injury settlement. Tax treatment depends on your specific settlement terms and individual circumstance.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.