Debt in 2026: What It Is, Types & How to Break Free

Americans now owe a record $18.8 trillion. This guide covers every debt type, warning signs you’re in danger, and the 5 strategies experts use to break free in 2026.

In This Article

What Is Debt? The $18.8 Trillion Reality in 2026

Debt is money you borrow from a lender — a bank, credit card company, or institution — with a legal obligation to repay it, usually with interest, by an agreed date.

That definition sounds simple. The reality in 2026 is anything but. According to the Federal Reserve Bank of New York’s Household Debt and Credit Report, total U.S. household debt hit a record $18.8 trillion in Q4 2025 — rising $191 billion in a single quarter. That’s $105,056 in debt for the average American household.

Debt at a Glance — 2026

| Metric | 2026 Data |

|---|---|

| Total U.S. Household Debt | $18.8 trillion (record high) |

| Avg. Debt Per Household | $105,056 |

| Credit Card Debt | $1.28 trillion |

| Mortgage Debt | $13.17 trillion |

| Student Loan Debt | $1.66 trillion |

| Auto Loan Debt | $1.67 trillion |

Debt is not inherently bad. A mortgage builds equity. A student loan builds earning power. But when debt spirals — especially high-interest credit card debt at 22%+ APR — it becomes a wealth-destroying trap. Use our Debt Consolidation Calculator to calculate exactly what your debt is costing you every month.

This guide breaks down every type of debt, the warning signs you’re in danger, and the five proven strategies to break free in 2026.

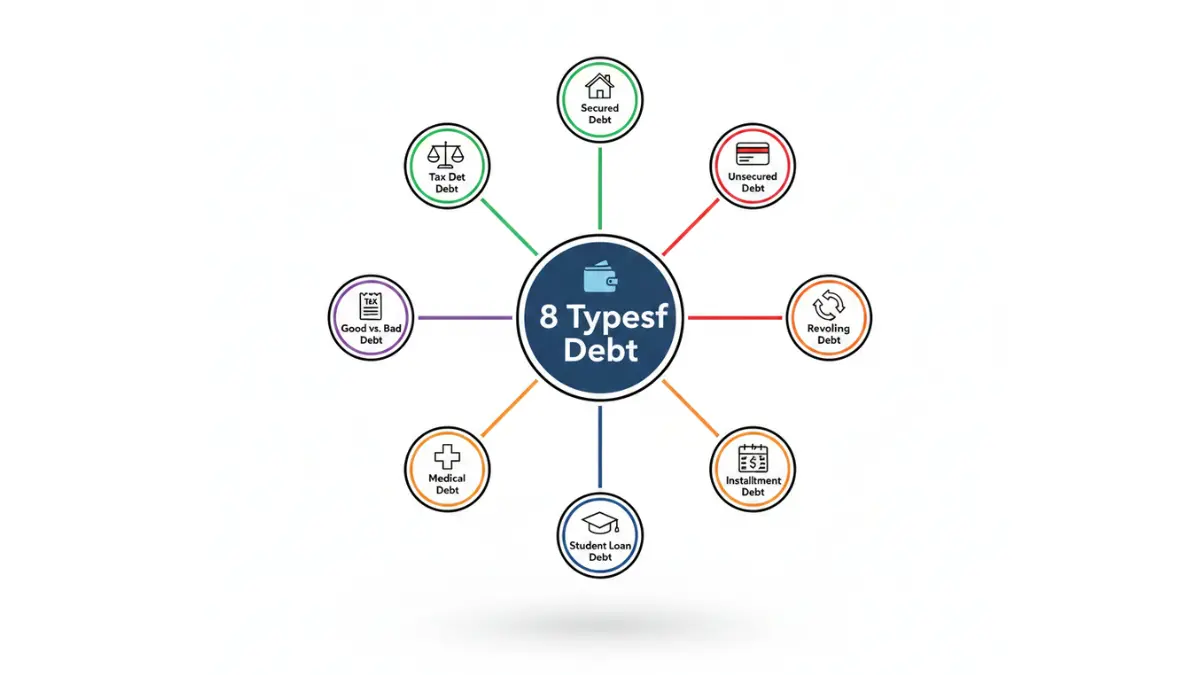

8 Types of Debt Every American Carries in 2026

Understanding your debt type is the first step to eliminating it. Not all debt works the same way — and not all debt is equally dangerous.

Secured Debt

Backed by collateral — the lender can seize your asset if you stop paying.

- Examples: Mortgages, auto loans, home equity loans

- Average interest rate: 6–8% (mortgage), 7–10% (auto)

- Risk level: Medium — you lose the asset, but rates are lower

If you carry a mortgage, use our Mortgage Calculator to track your payoff timeline. Before buying, our Home Affordability Calculator shows exactly what you can afford without overextending.

Unsecured Debt

No collateral required — but interest rates are punishing.

- Examples: Credit cards, personal loans, medical bills

- Average APR on credit cards: 22–22.8% in 2025

- Risk level: High — default leads to collections, lawsuits, and credit destruction

Read our deep-dive on APR vs. Interest Rate to understand exactly what you’re being charged.

Revolving Debt

A reusable credit line — borrow, repay, borrow again.

- Example: Credit cards, HELOCs

- Danger: Balances carry over monthly and compound fast

- Total U.S. revolving credit card debt: $1.28 trillion (Q4 2025)

Installment Debt

Fixed payments over a set term — ends when fully repaid.

- Examples: Mortgages, car loans, student loans, personal loans

- More predictable than revolving debt

Student Loan Debt

- Total outstanding: $1.66 trillion

- Delinquency rate: 9.6% (90+ days, Q4 2025)

- Federal repayment options available through StudentAid.gov

For students navigating financial aid, see our Financial Aid 2026 Guide.

Medical Debt

- Affects 100 million Americans

- Often unexpected, often negotiable

- Medical debt under $500 has been removed from credit reports

Tax Debt

- Owed to the IRS when you underpay or fail to file

- Accrues penalties and interest daily

- IRS payment plans available; see our EFTPS 2026 Guide

Good Debt vs. Bad Debt

| Debt Type | Good or Bad? | Why |

|---|---|---|

| Mortgage | ✅ Good | Builds equity, tax-deductible interest |

| Student Loan (low rate) | ✅ Good | Increases earning potential |

| Auto Loan (reasonable rate) | ⚠️ Neutral | Depreciating asset |

| Credit Card Debt | ❌ Bad | 22%+ APR, no asset value |

| Payday Loan | ❌ Dangerous | 300–400% effective APR |

Payday loans are among the most destructive forms of debt. Read our full breakdown in The Payday Loan Trap: Real Costs in 2026 before ever considering one.

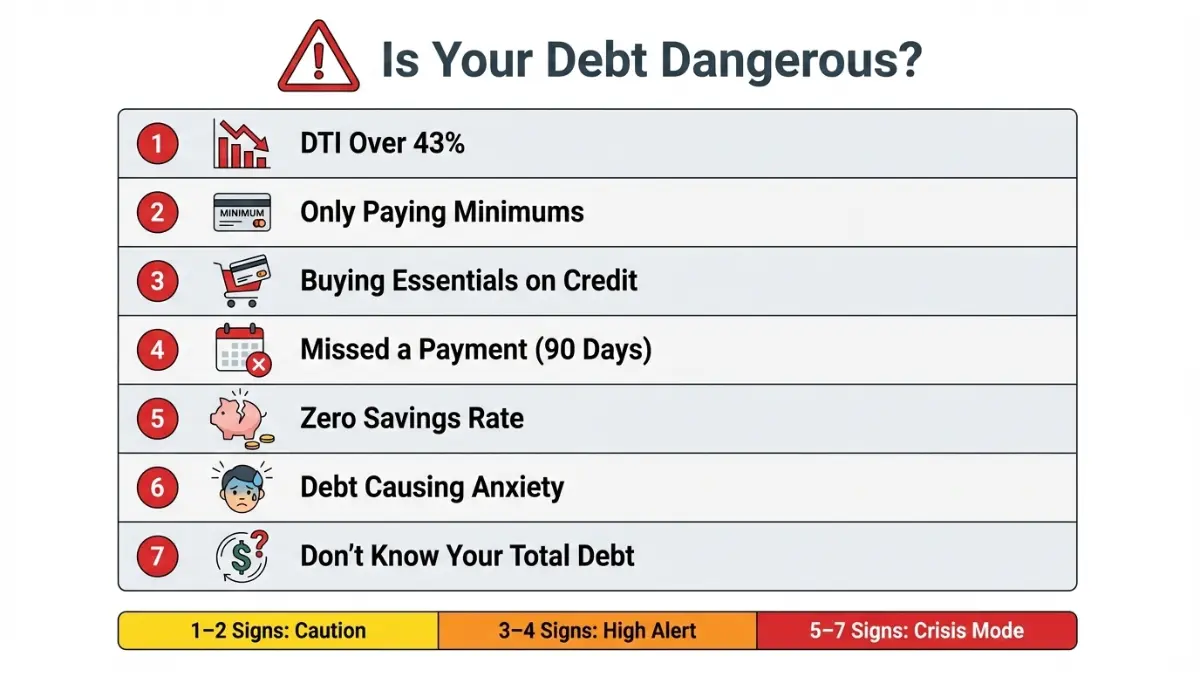

7 Warning Signs Your Debt Is Becoming Dangerous

This section is what Investopedia, NerdWallet, and Bankrate all skip. Yet it’s what millions of Americans need most. Check how many of these apply to you right now.

1. Your debt-to-income (DTI) ratio exceeds 43% Lenders consider 43% the danger threshold. Above this, you’re spending nearly half your income before buying food. Calculate yours free at our Debt Consolidation Calculator.

2. You’re making only minimum payments Paying the minimum on a $6,500 credit card balance at 22% APR takes over 20 years to repay and costs $8,000+ in interest alone.

3. You’re using credit cards for daily essentials Groceries and gas on a card you can’t pay off monthly = you’re borrowing to survive. This is a red flag.

4. You’ve missed a payment in the last 90 days According to Federal Reserve data on consumer delinquency rates, serious delinquencies on credit cards are at levels not seen since the Great Financial Crisis.

5. Your savings rate is zero If every dollar goes to debt payments, you have no emergency buffer — meaning any unexpected expense goes back onto the credit card. A vicious cycle.

6. Debt stress is affecting your sleep or mental health Financial anxiety is the #1 source of stress for American adults. If debt is keeping you up at night, that’s a clinical signal — not just anxiety.

7. You don’t know your total debt balance If you can’t name the exact number you owe across all accounts, you’re avoiding the problem. Avoidance makes debt worse.

Danger Level Score

| Signs You Identified | Alert Level | Action |

|---|---|---|

| 1–2 | 🟡 Caution | Review budget, build emergency fund |

| 3–4 | 🟠 High Alert | Start a debt payoff plan this week |

| 5–7 | 🔴 Crisis Mode | Seek credit counseling immediately |

What This Means For You: The CFPB’s debt relief guide is the most unbiased resource for understanding your options at each alert level. It’s free, government-backed, and has no conflicts of interest.

How to Break Free from Debt in 2026: 5 Proven Strategies

The FTC’s official guide on getting out of debt confirms that no single strategy works for everyone. Your best path depends on how much you owe, your interest rates, and your psychology.

Here are the five proven methods — with a real decision framework.

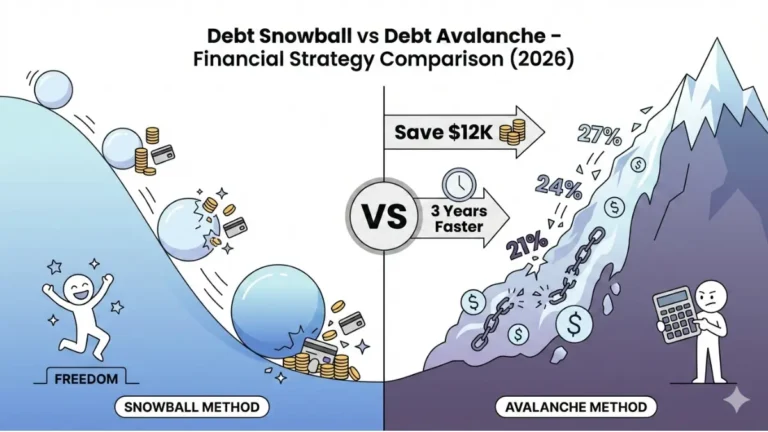

Strategy 1: Debt Snowball Method

Best for: People who need early motivation to stay on track.

- List debts from smallest balance to largest

- Pay minimums on all, throw every extra dollar at the smallest

- When it’s gone, roll that payment to the next

Real Example: Mark, 31, had 4 debts totaling $22,000. Using the snowball, he wiped out 2 small debts in 4 months. The momentum kept him going. Done in 26 months.

Strategy 2: Debt Avalanche Method

Best for: Mathematically-minded people who want to minimize interest paid.

- List debts from highest interest rate to lowest

- Throw extra money at the highest-rate debt first

- Saves the most money over time

See our full comparison at Snowball vs. Avalanche: Which Wins?

Strategy 3: Debt Consolidation

Best for: People with multiple high-interest debts and decent credit.

- Combine multiple debts into one lower-rate loan

- Reduces monthly payment and total interest

- Critical warning: Don’t accumulate new debt while consolidating

Run the numbers first with our Debt Consolidation Calculator. Our full guide at Debt Consolidation: Save $3,500 shows exactly how this works step by step.

Strategy 4: Balance Transfer (0% APR Card)

Best for: People with credit card debt and a credit score above 670.

- Transfer high-interest balance to a 0% APR card

- Pay zero interest for 12–21 months

- Must pay off before the promo period ends or rates spike

Read our vetted list of 0% APR Cards That Eliminate $8K+ in Debt. Also understand the cost of APR first with our APR Complete Guide.

Strategy 5: Debt Management Plan (DMP)

Best for: People overwhelmed by multiple debts who need a structured, supervised payoff.

- Offered by nonprofit credit counseling agencies

- Agencies negotiate reduced interest rates with creditors (often down to 6–8%)

- One monthly payment, paid off in 3–5 years

- Does not damage credit like debt settlement

Strategy Comparison Table

| Strategy | Best For | Est. Payoff Time | Credit Impact | Typical Cost |

|---|---|---|---|---|

| Snowball | Motivation-driven | 2–5 years | None | Free |

| Avalanche | Interest savings | 2–5 years | None | Free |

| Consolidation | Multiple high-rate debts | 2–7 years | Slight dip then improves | Loan fees |

| Balance Transfer | Credit card debt | 12–21 months | Slight dip | 3–5% transfer fee |

| DMP | Overwhelmed borrowers | 3–5 years | Slight dip | ~$25–$50/month |

What 2026’s High-Rate Environment Means for Your Debt

2026 is not a forgiving environment for debt. Here’s what’s happening right now — and what it means for your wallet.

The Numbers That Matter:

- Credit card APR: 22–22.8% — near a 40-year high

- Student loan delinquency: 9.6% of balances 90+ days late

- Total household debt: $18.8 trillion — up $740 billion in 2025 alone

- 71% of U.S. adults say debt payments prevent them from building savings

The K-Shaped Economy: Higher-income Americans are accumulating assets while lower-income households spiral deeper into high-interest debt. This divide — what economists call a “K-shaped recovery” — makes proactive debt management more urgent than ever.

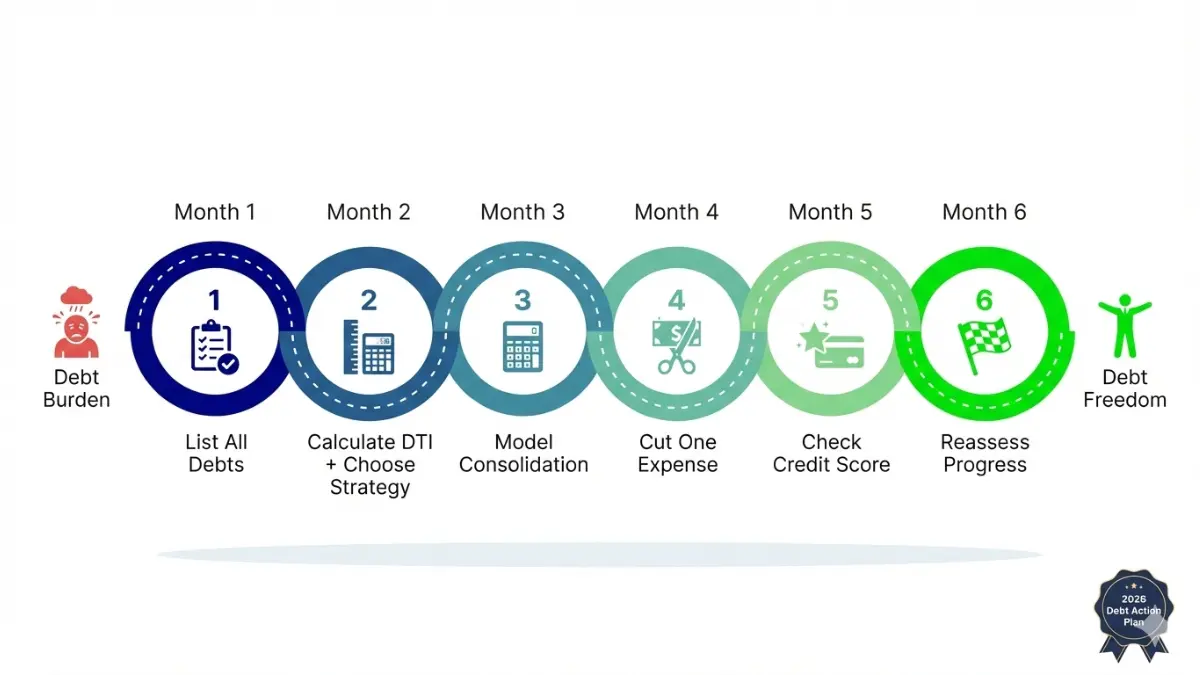

2026 Debt Action Timeline

| Month | Action Step |

|---|---|

| Month 1 | List every debt: balance, rate, minimum payment |

| Month 2 | Calculate DTI; choose snowball or avalanche |

| Month 3 | Open a Debt Consolidation Calculator; model consolidation |

| Month 4 | Cut one discretionary expense; redirect to debt |

| Month 5 | Check credit score — see our Credit Score Guide |

| Month 6 | Reassess: Are you ahead of schedule? |

One More Key Tool: If you’re approaching retirement and still carrying debt, the math changes significantly. Our Retirement Savings by Age Guide helps you balance debt repayment with retirement contributions.

Debt FAQs: 11 Questions Americans Are Asking in 2026

Q1: What is debt in simple terms?

Debt is money you borrow and must repay — usually with interest. It includes mortgages, credit cards, student loans, and personal loans.

Q2: What are the main types of debt?

The main types are secured, unsecured, revolving, installment, student loan, medical, tax, and good vs. bad debt. Each carries different interest rates and risks.

Q3: What is good debt vs. bad debt?

Good debt (mortgages, low-rate student loans) builds wealth or income. Bad debt (high-interest credit cards, payday loans) drains it. See our full Credit Card Debt Escape Strategies guide.

Q4: What is a dangerous debt-to-income ratio?

A DTI above 43% is considered risky by most lenders. Above 50% signals a debt crisis that requires immediate action.

Q5: How do I get out of debt fast?

Start with the snowball or avalanche method. If you have multiple high-rate debts, consolidation or a 0% balance transfer can accelerate your timeline. See: How to Pay Off Debt Fast.

Q6: Does debt consolidation hurt my credit score?

Temporarily yes — a hard inquiry drops your score a few points. But long-term, reducing your credit utilization and making on-time payments improves your score significantly.

Q7: What is the debt snowball method?

Pay off your smallest debt first while paying minimums on the rest. When it’s gone, roll that payment to the next smallest. It builds momentum.

Q8: What is the debt avalanche method?

Pay off your highest-interest debt first. It saves more money than snowball but requires more patience.

Q9: What happens if I don’t pay my debt?

Late fees begin immediately. After 30 days, it hits your credit report. After 90–180 days, accounts go to collections. After that, you may face lawsuits, wage garnishment, or bankruptcy.

Q10: What is a debt management plan?

A nonprofit-administered plan that consolidates your payments and negotiates lower interest rates with creditors. Takes 3–5 years. Does not settle debt for less than owed.

Q11: How much debt does the average American carry in 2026?

The average U.S. household carries $105,056 in total debt, including mortgage, auto, student loans, and credit cards, according to Q4 2025 Federal Reserve data.

Quick-Reference Glossary

| Term | Definition |

|---|---|

| Debt | Money borrowed that must be repaid with interest |

| Secured debt | Debt backed by collateral (house, car) |

| Unsecured debt | Debt with no collateral (credit cards, personal loans) |

| APR | Annual Percentage Rate — true yearly cost of borrowing |

| Revolving debt | Credit you can borrow, repay, and borrow again (credit cards) |

| Installment debt | Fixed payments over a set term (mortgages, car loans) |

| DTI | Debt-to-income ratio — monthly debt payments ÷ gross income |

| Delinquency | Missed or late payment, typically 30+ days overdue |

| Default | Failure to repay debt per agreed terms |

| Consolidation | Combining multiple debts into one loan, ideally at a lower rate |

⚠️ Disclaimer: This article is for educational and informational purposes only. It does not constitute financial, legal, or professional advice. Debt situations vary widely based on individual circumstances. Always consult a qualified, licensed financial advisor before making decisions about debt management, consolidation, or relief programs. External links to government websites are provided for reference and do not imply endorsement.

Was this article helpful? Explore more at financeauthorityhub.com — your trusted source for expert-verified financial guidance.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.