How Courts Value and Split Your Structured Settlement in Divorce

Structured settlement in divorce: courts in 41 states can divide yours — and the discount rate gap can cost $85,000.

In This Article

Your structured settlement may be at risk when divorce is filed

The payments arrive every month without fail — compensation for a serious injury, income that many settlement holders depend on for ongoing medical care, housing costs, or daily living expenses.

When a divorce filing arrives, those payments can become a legal target.

What this article answers that most divorce guides skip

Most legal resources tell readers that settlements “may” be divisible marital property and leave it there. This article, written by a CFA with 28 years of capital markets experience, explains exactly when they are, how courts assign a specific dollar value to future payments, and what happens to the IRS protection that currently keeps those payments tax-free.

These are the three questions that determine whether you leave divorce court with your income stream intact — or fractured.

Why the source and timing of your settlement changes everything

A structured settlement in divorce is not a single legal issue — it is simultaneously a property law question, a financial valuation problem, and a tax planning challenge.

Understanding how structured settlements work and what they pay is the foundational step before any divorce-related division strategy can be evaluated.

ℹ️ Disclaimer: The legal and financial information in this article is intended for general educational purposes only. Structured settlement classification, valuation, and division in divorce proceedings are governed by federal tax law, state family law statutes, and the specific terms of the original settlement agreement — all of which vary by jurisdiction and individual circumstance. This article does not constitute legal advice, tax advice, or personalized financial planning guidance. Consult a licensed divorce attorney for legal questions and a Certified Divorce Financial Analyst (CDFA) or Certified Public Accountant (CPA) for financial valuation and tax questions before making any decision related to a structured settlement in divorce proceedings.

Is your structured settlement marital property or separate property?

Whether your spouse can legally claim your settlement payments depends on a question courts ask first: what specific losses was the settlement designed to compensate?

Courts in all 50 states apply a damages-source analysis to classify assets as marital or separate property before dividing anything.

Why the purpose of your settlement changes its legal status

Three damages categories produce materially different classification outcomes in divorce proceedings.

| Damages Type | Typical Classification | Marital Property Risk |

|---|---|---|

| Pain and suffering — physical injury | Separate property | Low |

| Lost wages earned during the marriage | Marital property | High |

| Medical expenses paid from joint funds | Contested | High |

| Future medical costs post-settlement | Separate property | Low–Medium |

| Punitive damages | Jurisdiction-dependent | Medium |

Source: State equitable distribution and community property frameworks, 2026

📊 Data Point: Forty-one states apply equitable distribution principles, giving judges broad discretion over asset division based on fairness factors. The remaining nine community property states — including California, Texas, and Arizona — apply a presumptive 50/50 split rule. — Source: National Center for State Courts, family law framework review, 2026.

How depositing settlement funds into a joint account can cost you everything

Commingling — depositing settlement checks into a shared bank account — can legally convert a separate-property settlement into a marital asset subject to full court division.

Courts in equitable distribution states have consistently held that even partial commingling shifts the burden of proof to the settlement holder to trace and segregate funds from the marital estate.

⚠️ Warning: If structured settlement payments have been deposited into a joint account at any point during the marriage, consult a divorce attorney immediately. The commingling analysis is time-sensitive — the longer the pattern continues, the harder the separate-property claim becomes to sustain in court.

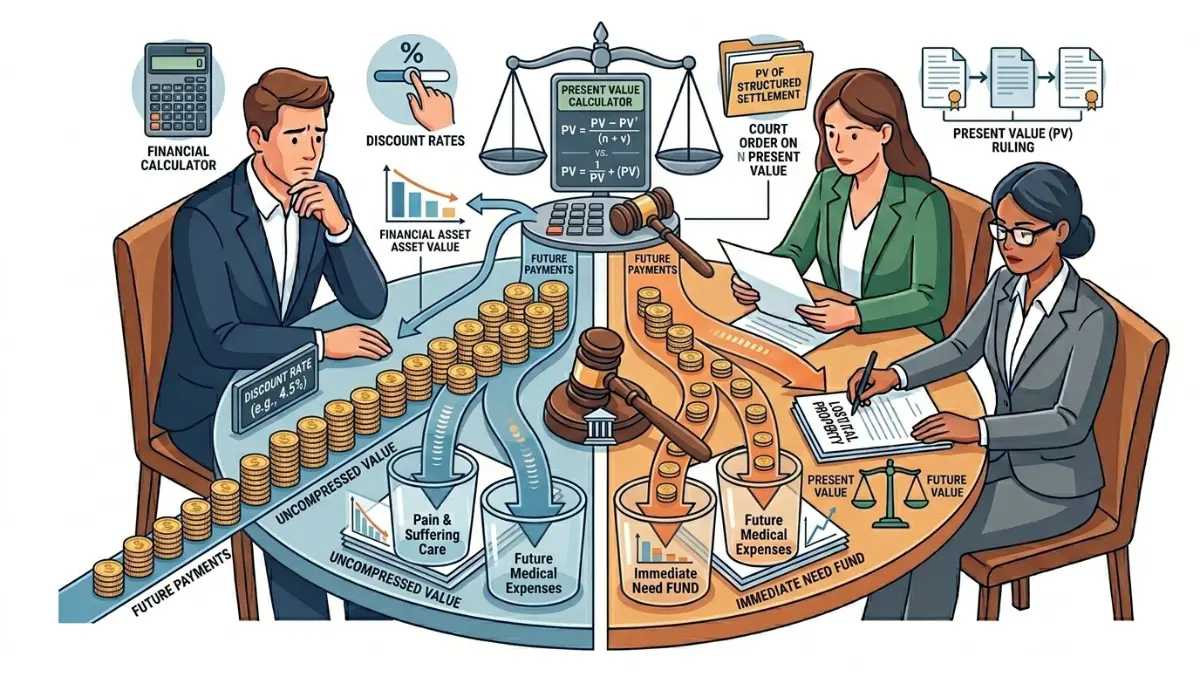

How courts calculate what your structured settlement payments are worth

Knowing that your settlement may be divisible is only part of the problem. The more consequential fight is over how much it is worth — and that number can shift by tens of thousands of dollars depending on who runs the calculation.

The three methods courts use to divide structured settlement payments

Courts apply one of three mechanisms when dividing a structured settlement annuity in divorce proceedings:

- Lump-sum property offset — The settlement holder keeps all future payments; the spouse receives other marital assets of equal calculated present value. This is the most common approach and the most likely to preserve the original tax exclusion intact.

- Direct payment stream division — A court order allocates a fixed percentage of each future payment to the spouse as each payment arrives. This is legally complex, rarely preferred by courts, and creates tax complications for both parties.

- Deferred distribution — Payments are divided when received rather than at the time of divorce. Courts use this approach when present-value disputes cannot be resolved before the case closes.

The lump-sum vs. structured settlement comparison covers the financial tradeoffs of each approach — a critical reference before any offset negotiation begins.

Use the savings calculator to model what a proposed lump-sum offset would grow to under 2026 investment return assumptions, giving you an independent comparison point before accepting any offer.

Why the discount rate is the most important number in your case

Every lump-sum offset requires calculating the present value of future payments — and the discount rate applied to that calculation is the single variable with the greatest impact on the outcome.

📊 Data Point: For a 20-year structured settlement paying $3,000 per month, the difference between a 4.5% AFR-based discount rate and a 7.0% market-based rate produces a calculated present-value gap exceeding $85,000. — Source: IRS Applicable Federal Rate (AFR) table, Revenue Ruling published monthly, IRS.gov, 2026.

Opposing attorneys routinely advocate for the highest defensible discount rate in order to reduce the settlement’s present value — and therefore reduce the offset required from other marital assets.

For the step-by-step mechanics behind how courts calculate structured settlement discount rates, the dedicated guide explains the AFR methodology in full detail.

💡 Expert Note (CFA): In 28 years of financial advisory work, I have seen opposing counsel use discount rates from 5% to 9% on identical payment streams — all technically defensible — producing a spread exceeding $100,000 on a single asset. Without a credentialed financial expert present to challenge the rate selection, courts will typically accept whichever figure was submitted first.

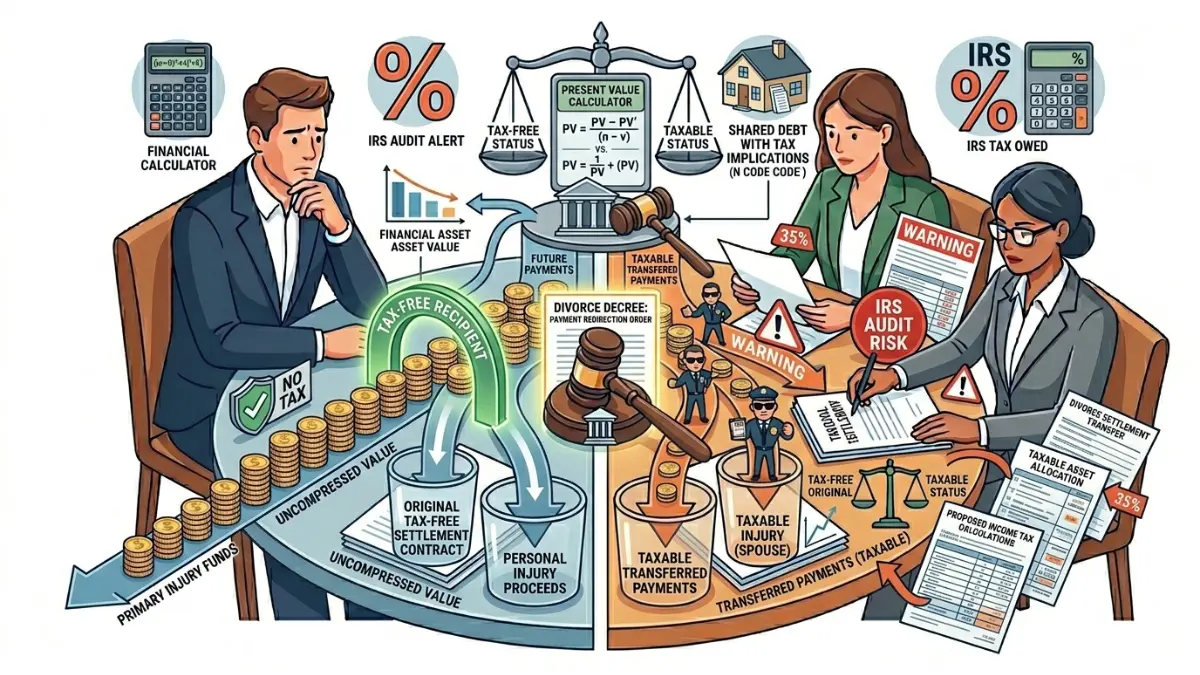

Tax consequences of splitting a structured settlement in divorce

Dividing a structured settlement in divorce does not just raise property questions — it can trigger a federal tax event that permanently eliminates one of the settlement’s most valuable protections.

What IRC Section 104(a)(2) protects — and its limits in divorce

Under IRC Section 104(a)(2), personal physical injury settlement payments are fully excluded from federal gross income — but only for the original recipient named in the settlement agreement.

That protection does not automatically extend to a spouse who receives payments under a divorce court order.

📊 Data Point: IRS Publication 4345 (2026 edition) confirms that the Section 104(a)(2) exclusion applies specifically to the recipient named in the original settlement. Amounts paid to a spouse by court order may be taxable to that spouse as ordinary income. — Source: IRS Publication 4345 on the taxability of settlement proceeds, IRS.gov, 2026.

The full question of whether structured settlement payments are taxable — including every scenario where the exclusion applies and where it does not — is the essential baseline before any divorce-related division arrangement is agreed to.

When a divorce transfer triggers a taxable event

Taxable events in a structured settlement divorce case arise when settlement payment rights are assigned or redirected to a non-injured spouse by court order.

The receiving spouse may owe ordinary income tax on every dollar received — a liability that can eliminate the full financial value the arrangement was expected to provide.

⚠️ Warning: Before agreeing to any arrangement that routes structured settlement payments to your spouse, obtain a written Section 104 tax analysis from a licensed CPA. The tax liability on transferred payments can eliminate the financial benefit both parties were expecting from the transfer.

Use the income tax calculator to estimate what transferred settlement payments could cost a receiving spouse in federal taxes at 2026 income levels.

If a factoring sale or lump-sum settlement purchase is part of the divorce agreement, the capital gains tax calculator can model the tax exposure on any sale proceeds before they are committed to in writing.

💡 Expert Note (CFA): The single most expensive mistake I have seen settlement holders make in divorce is agreeing to a payment stream division without first obtaining a Section 104 analysis. The receiving spouse ends up with taxable ordinary income they cannot shelter, and the settlement holder loses the offset credit for assets surrendered expecting the other side to be tax-free.

Legal tools courts use — and why QDROs don’t apply to your annuity

The most common error in structured settlement divorce cases is assuming a QDRO can divide the annuity. It cannot — and understanding why determines the entire legal strategy.

Why a QDRO cannot divide a structured settlement annuity

A Qualified Domestic Relations Order (QDRO) applies exclusively to ERISA-qualified retirement plans — 401(k) accounts, pension plans, and similar employer-sponsored vehicles.

Structured settlement annuities are not ERISA-governed, cannot be reached by a QDRO, and fall instead under state Structured Settlement Protection Acts and the contract terms of the original settlement agreement.

Before agreeing to any reassignment of payment rights, review the CFPB’s consumer guidance on structured settlement payment rights to understand which federal protections remain in place regardless of what a divorce court orders.

The anti-assignment problem: how the original settlement agreement limits court power

Most structured settlement agreements contain anti-assignment clauses — contractual provisions prohibiting the transfer of payment rights without the annuity issuer’s explicit written consent.

Divorce courts cannot unilaterally override these clauses, and annuity issuers are rarely willing to grant consent to redirect payments to a non-injured party.

This is the primary legal reason the lump-sum property offset — keeping the annuity intact while the spouse receives other marital assets of equal present value — is the most viable and most tax-efficient resolution in most structured settlement divorce cases.

The court approval process for structured settlements explains in detail what a divorce judge can and cannot order regarding existing payment rights — important context before any negotiation begins.

⚠️ Warning: The SEC has flagged secondary-market factoring transactions that are aggressively marketed to settlement holders during divorce proceedings. Review SEC investor information on secondary-market structured settlement transactions before accepting any offer to purchase your payment rights during an active divorce case.

| Legal Mechanism | Available in Divorce | Preserves Tax-Free Status | Anti-Assignment Risk |

|---|---|---|---|

| QDRO | No | N/A | N/A |

| Lump-sum property offset | Yes | Yes — annuity remains with original recipient | None |

| Direct payment assignment to spouse | Rarely | No — receiving spouse may owe taxes | High |

| Deferred distribution order | Yes | Partially | Medium |

| Factoring sale during proceedings | Yes — court approval required | No — proceeds are taxable | None |

Source: State Structured Settlement Protection Acts framework, 2026

How your state’s property laws determine who keeps the payments

The state where your divorce is filed does not just set the courtroom venue — it determines the legal standard applied to every dollar of your settlement.

Community property states: the 50/50 presumption and its exceptions

In nine community property states — California, Texas, Arizona, Nevada, New Mexico, Idaho, Louisiana, Washington, and Wisconsin — assets acquired during marriage are presumed equally owned by both spouses.

For structured settlements, the 50/50 presumption applies to portions compensating marital losses, such as wages lost during the marriage. However, amounts compensating for the injured spouse’s own physical harm retain separate-property protection even in community property jurisdictions.

📊 Data Point: California Family Code § 780 specifies that damages recovered for personal physical injury remain the separate property of the injured spouse — unless commingled with community property. — Source: California Family Code, 2026.

Equitable distribution states: what “fair” actually means for settlement payments

In the 41 equitable distribution states, courts divide marital assets based on factors including length of marriage, each spouse’s financial need, earning capacity post-divorce, and medical dependency — giving judges wide discretion to award a structured settlement in full to the injured spouse when circumstances justify it.

An injured spouse demonstrating ongoing medical dependency on settlement payments holds a measurably stronger retention argument in an equitable distribution state than in a community property jurisdiction.

The workers’ comp structured settlement guide covers how disability-replacement payments are classified differently from personal injury proceeds — a critical distinction, as many states treat workers’ comp payments as income substitution rather than injury compensation.

Use the inflation calculator to show how the real purchasing power of fixed settlement payments erodes over a 15- or 20-year horizon — a factor courts weigh when assessing the long-term equity of any proposed offset arrangement.

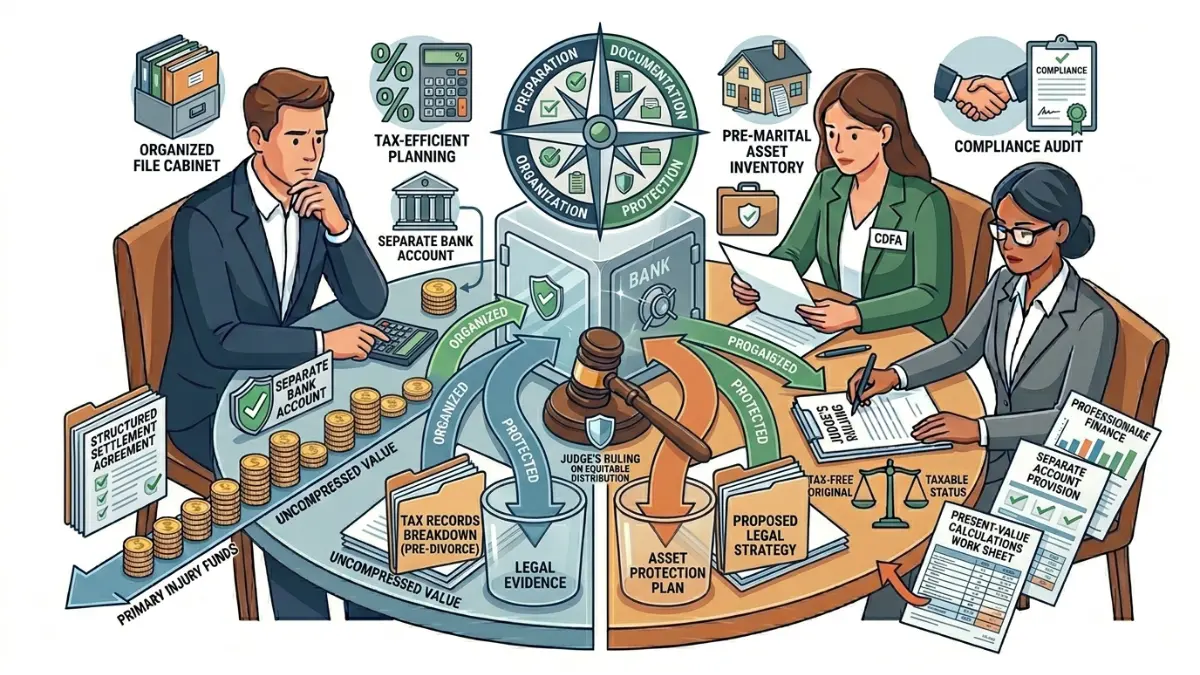

How to protect your structured settlement before and during divorce

The settlement holders who walk out of divorce court with their payment stream fully intact almost always did the same thing before the case advanced: they documented their position early and brought the right financial professional into the room before attorneys began negotiating.

Four documentation steps that strengthen your separate-property claim

A defensible separate-property argument in a structured settlement divorce rests on four specific evidentiary foundations:

- Maintain a dedicated settlement account. A bank account used exclusively for structured settlement deposits — with no marital funds ever mixed in — is the strongest single piece of evidence for separate-property classification. Open one now if you do not already have one.

- Preserve the original damages breakdown. Retain the settlement agreement, the attorney’s closing letter, and any damages allocation document showing what each payment compensates — pain and suffering vs. lost wages vs. medical costs. This document is what your attorney needs most.

- Document all commingling precisely. Pull bank statements for every account where settlement funds were deposited and flag every instance of fund mixing with marital money. Your attorney needs this inventory before the first negotiation session.

- Engage a CDFA before attorneys negotiate. A Certified Divorce Financial Analyst provides an independent present-value calculation, models the after-tax cost of each division scenario, and challenges opposing counsel’s discount-rate assumptions before any baseline number is locked in.

✅ Pro Tip: Contact a CDFA before your attorney enters the first settlement negotiation. A CDFA’s present-value model gives your attorney a defensible number — rather than a number to accept under pressure.

When to bring in a Certified Divorce Financial Analyst before attorneys negotiate

The financial valuation of a structured settlement in divorce is not a legal question — it is a financial modeling question that requires a credentialed analyst to answer correctly.

💡 Expert Note (CFA): I have seen settlement holders accept lump-sum offset offers 30% to 40% below the defensible present value of their payment stream because no financial expert was present to challenge the discount rate. A CDFA engagement — typically $2,500 to $7,500 for a complete divorce financial analysis — is almost always recovered many times over through improved negotiation outcomes.

Before any factoring company approaches you during proceedings, read FINRA’s alert on aggressive structured settlement purchasing tactics — these firms specifically target settlement holders experiencing financial pressure, and divorce is among the highest-risk moments for a below-market sale.

The risks of selling structured settlement payments during an active divorce are compounded by property division proceedings and should only be evaluated with both a divorce attorney and a financial advisor present.

Frequently asked questions about structured settlements in divorce

1. Is a personal injury structured settlement considered marital property?

A personal injury structured settlement is generally classified as separate property when it compensates for physical pain and suffering. Portions compensating for lost wages earned during the marriage or medical expenses paid from joint funds may be marital property. The original damages breakdown document is controlling. Consult a divorce attorney for jurisdiction-specific guidance.

2. Can my spouse legally claim my structured settlement?

Yes, under certain conditions. If settlement funds were classified as marital property or commingled with joint accounts, a spouse may have a valid claim. In a structured settlement in divorce case, the settlement’s source and deposit history are the two most determinative factors. Consult a licensed divorce attorney immediately to assess your exposure.

3. How do courts calculate the present value of a structured settlement?

Courts apply a discount rate to the future payment stream to produce a single present-value figure. The IRS applicable federal rate (AFR) — published monthly at IRS.gov — is the 2026 benchmark most courts accept. A higher discount rate lowers the calculated present value. Consult a CDFA for a litigation-quality independent valuation.

4. Are structured settlement payments taxable after a divorce?

The original recipient’s payments remain excluded under IRC Section 104(a)(2) when structured as compensation for personal physical injury. A spouse receiving structured settlement payments by court order in a divorce case may not qualify for the same exclusion and could owe ordinary income tax on those amounts. Verify with a licensed CPA before agreeing to any transfer.

5. Can a structured settlement annuity be transferred in a divorce?

Direct transfer of annuity ownership is prohibited by anti-assignment clauses in the original settlement agreement and by state Structured Settlement Protection Acts. Courts generally cannot compel the issuer to redirect payments. A lump-sum property offset — keeping the annuity intact while the spouse receives other assets — is the most legally viable alternative. Consult a divorce attorney.

6. Does a QDRO apply to structured settlement annuities?

No. A Qualified Domestic Relations Order applies only to ERISA-qualified retirement plans such as 401(k) accounts and pensions. Structured settlement annuities are not ERISA-governed and cannot be divided by QDRO. In a structured settlement divorce case, courts must use alternative mechanisms — property offsets or deferred distribution. Consult a divorce attorney for options in your state.

7. What happens if I commingled my structured settlement funds with marital assets?

Commingling — depositing structured settlement checks into a joint account — can convert a separate-property settlement into a marital asset subject to full court division in a structured settlement divorce proceeding. The extent depends on state law, duration of mixing, and whether funds can be traced back to the original settlement. Consult a divorce attorney immediately.

8. Can I sell my structured settlement during divorce proceedings?

Yes, but the sale requires court approval under state Structured Settlement Protection Acts, and the proceeds become a marital asset subject to division. Selling during a structured settlement divorce case may also weaken your separate-property claim. Consult both a licensed divorce attorney and a financial advisor before initiating any sale or factoring arrangement.

9. How does a workers’ compensation settlement differ from a personal injury settlement in divorce?

Workers’ compensation settlements compensating for lost wages or reduced earning capacity are frequently classified as marital property because they substitute for marital income. Personal injury pain-and-suffering awards receive stronger separate-property protection in most states. The classification of a workers’ comp structured settlement in divorce varies significantly by jurisdiction. Consult a divorce attorney in your state.

10. Can a divorce decree change the terms of an existing structured settlement?

A divorce court cannot override anti-assignment provisions in the original agreement or compel the annuity issuer to modify payment terms. Courts can compensate a spouse through other marital assets without altering the structured settlement in divorce. Modifying the actual payment stream requires the annuity issuer’s written consent. Consult a licensed divorce attorney before negotiating any modification.

11. Should I hire a financial expert to value my structured settlement in divorce?

Yes. A Certified Divorce Financial Analyst (CDFA) or CFA with structured settlement experience independently calculates the present value of your payment stream, challenges opposing counsel’s discount-rate assumptions, and models the after-tax cost of each proposed division structure. The CDFA fee of $2,500 to $7,500 is typically recovered through improved negotiation outcomes in a structured settlement divorce case.

A structured settlement in divorce is a winnable case — but only for readers who understand three things before negotiations begin: what the court is legally authorized to divide, how the present value is calculated and who controls the discount rate, and what happens to the tax exclusion if the wrong structure is agreed to.

Document your position early. Bring in a CDFA before the first settlement session. Never accept a present-value figure without an independent calculation from a credentialed financial analyst.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.