Automobile Insurance Rates Drop in 2026: Best Deals Now

Automobile insurance rates fell 6% in 2025 — national average now $2,158/year. Compare top companies, state rates & 12 proven ways to cut your premium before 2026 tariffs push costs back up.

In This Article

Automobile insurance costs fell 6% in 2025 and are stabilizing in 2026 — the national average for full coverage now sits at $2,158 to $2,496 per year. If you haven’t compared your auto insurance rates since 2024, there’s a strong chance you’re overpaying. Here’s exactly what you need to know to lock in the best deal before mid-2026 tariff pressures push premiums back up.

2026 Automobile Insurance Snapshot

| Metric | 2026 Figure |

|---|---|

| Avg. full coverage (national) | $2,158 – $2,496/year |

| Avg. minimum coverage | $682 – $820/year |

| States with 2025 rate decreases | 39 states |

| Cheapest state | Vermont ($1,504/year) |

| Most expensive area | Washington D.C. ($4,017/year) |

| Tariff risk outlook | ⚠️ Mid-2026 renewals may reflect repair cost increases |

What This Means For You: This is the best window in three years to shop for lower automobile insurance rates. But the window is closing — insurers’ margins improved significantly after the 46% premium surge from 2022 to 2024, and many are now cutting rates to attract customers. That competitive pressure may ease once tariff-driven repair costs hit policy pricing.

What Does Automobile Insurance Actually Cover?

Automobile insurance is a legal contract between you and an insurer. It protects you financially if you cause an accident, if your vehicle is damaged, or if you’re hit by an uninsured driver. Most U.S. states require a minimum level of coverage before you can legally drive.

Understanding your coverage types is the first step to avoiding both overpaying and being underinsured.

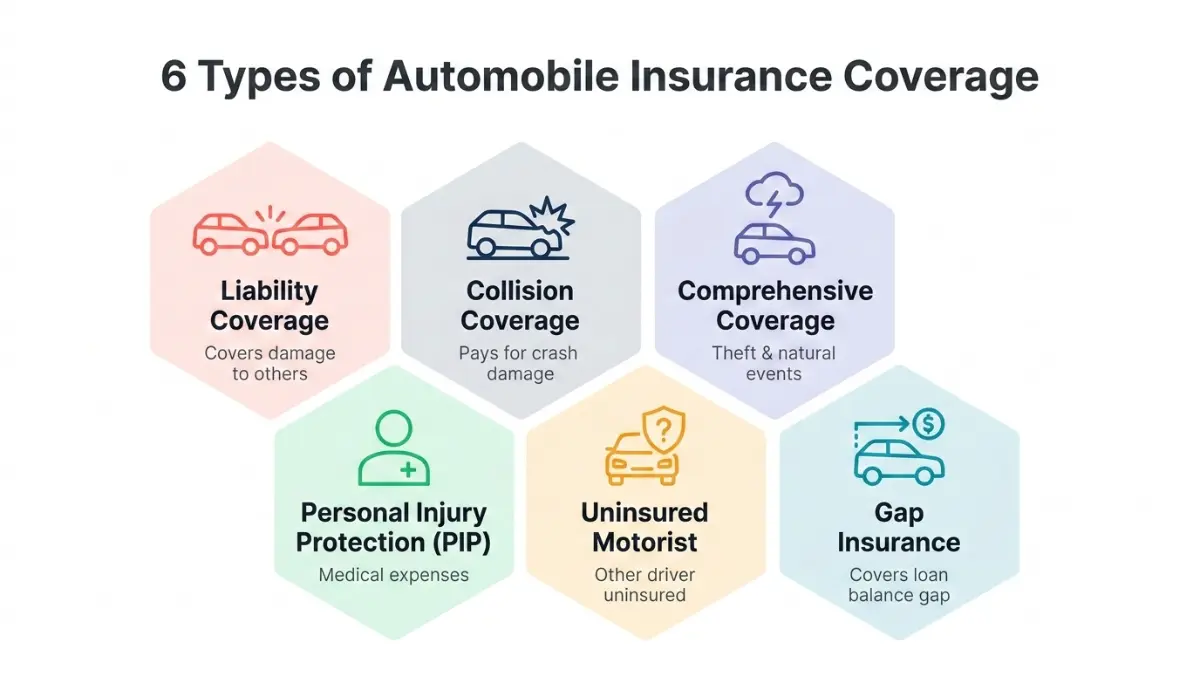

The 6 Core Coverage Types — Quick Reference

| Coverage Type | What It Pays For | Required? |

|---|---|---|

| Liability | Damage or injury you cause to others | Yes — 49 states |

| Collision | Your vehicle after an accident | If financed or leased |

| Comprehensive | Theft, weather, vandalism, fire | If financed or leased |

| Personal Injury Protection (PIP) | Your medical bills regardless of fault | Required in 12 no-fault states |

| Uninsured Motorist | Accidents involving uninsured drivers | Required in ~22 states |

| Gap Insurance | Loan balance if your car is totaled | Optional — critical for new car buyers |

For a deeper breakdown of gap coverage and when it’s worth buying, see our guide to gap insurance and what it actually covers.

Liability-Only vs. Full Coverage — Which Is Right for You?

Full coverage includes liability, collision, and comprehensive. It makes sense if your car is newer, financed, or worth more than $10,000.

Liability-only is the legal minimum and costs far less — averaging $682 to $820 per year nationally. A common rule: if your car is worth less than 10 times your annual premium, dropping to liability-only may save you money.

For a detailed breakdown of what liability car insurance covers in your state — and what it doesn’t — read our full liability insurance guide before making a decision.

What This Means For You: Don’t pay for full coverage on a car worth $3,000. But don’t drop comprehensive on a financed vehicle either — your lender won’t allow it.

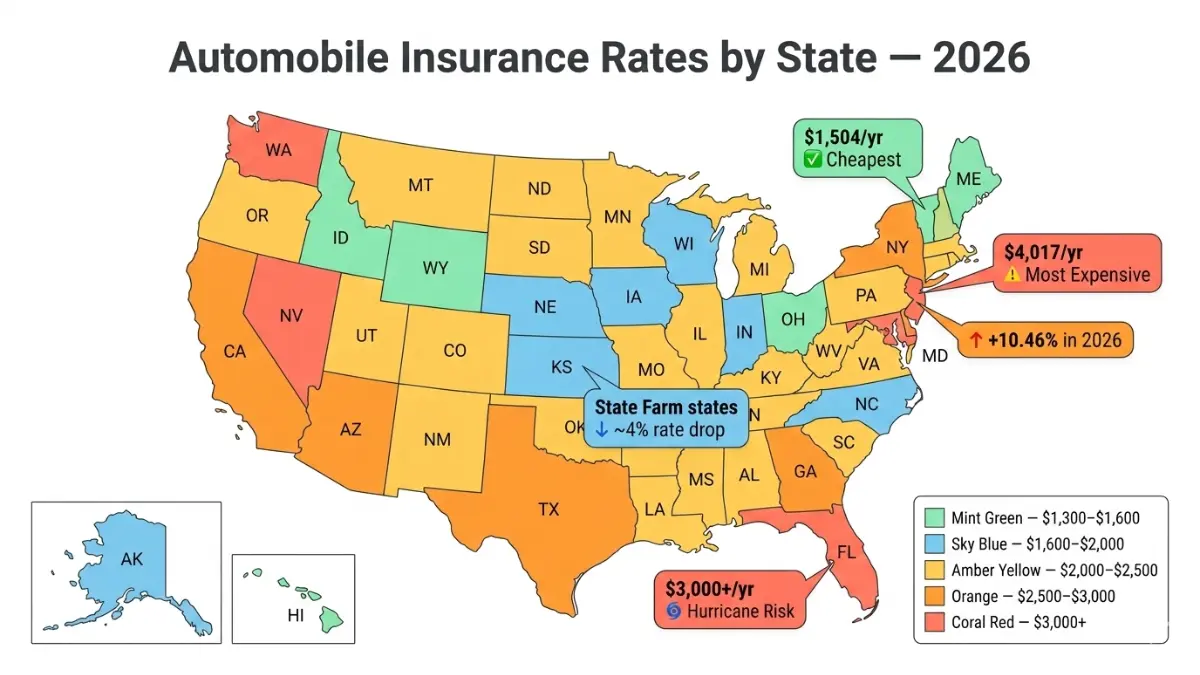

Automobile Insurance Rates by State in 2026

Where you live is the single biggest factor in your automobile insurance premium. The average cost of full coverage car insurance in the U.S. is $208 per month, or about $2,496 per year. But that national average hides dramatic state-by-state variation.

Cheapest States for Automobile Insurance (2026)

| State | Avg. Annual Full Coverage |

|---|---|

| Vermont | $1,504 |

| Maine | $1,367 – $1,701 |

| Wyoming | $1,356 |

| Hawaii | $1,361 |

| Idaho | $1,375 – $1,443 |

| Ohio | $1,466 – $1,739 |

These low-cost states share common traits: lower population density, fewer uninsured drivers, and less traffic congestion — all factors that reduce the frequency and severity of claims.

Most Expensive States and Why

| State | Avg. Annual (Full Coverage) | Primary Cost Driver |

|---|---|---|

| Washington D.C. | $4,017 | High density + 18% rate surge in 2025 + uninsured drivers |

| Maryland | $3,601 | Litigation costs + dense urban traffic |

| New Jersey | $2,978 | New 2026 minimum coverage law took effect Jan 1 |

| Nevada | $3,000+ | Las Vegas congestion + high claim frequency |

| Florida | $3,000+ | Fraud + hurricanes + 26%+ uninsured driver rate |

New Jersey drivers could see their car insurance bill go up by an estimated 10.46% when they renew their policies in 2026 due to the new minimum coverage requirements that took effect at the start of the year.

⚠️ The 2026 Tariff Warning Competitors Are Ignoring

The effect of tariffs on auto repairs remains a wildcard — repair costs are likely to rise in 2026, and as of now, insurers haven’t passed these costs on to consumers. Average auto insurance claims already cost around $13,000 — a 10% increase from 2024 per AM Best data. Drivers renewing policies in Q3 or Q4 of 2026 may be the first to feel this. According to the Bureau of Labor Statistics consumer price index data, vehicle parts and maintenance inflation continues to outpace general CPI — a direct pressure on insurer costs.

Lock in a renewal quote now if your policy renews after June 2026.

Best Automobile Insurance Companies of 2026 — Ranked

Not every company is cheapest for every driver. The right automobile insurance company depends on your profile, state, and priorities.

Top Companies Ranked by Category

| Company | Best For | Avg. Full Coverage | 2026 Rate Direction |

|---|---|---|---|

| Travelers | Cheapest nationally | $139/month | Stable |

| GEICO | Minimum coverage + bad credit | $41/month (liability) | Competitive |

| State Farm | Overall reliability | Varies by state | ↓ ~4% decrease |

| Erie | Customer service (#1 J.D. Power) | Regional | ↑ +7.92% expected |

| USAA | Military families only | Lowest available | Stable |

| Progressive | High-risk + rideshare drivers | $101/month (liability) | Stable |

| Nationwide | Price + availability balance | Competitive | Stable |

Travelers is the cheapest large auto insurance company in the nation for full coverage, with an average rate of $139 a month and $1,666 a year, according to NerdWallet’s February 2026 analysis.

Companies Expected to Raise Rates in 2026

NJM customers may see their rates go up by an average of 21.18% at renewal. Rates at Erie are expected to rise by 7.92%, while Plymouth Rock is expected to raise rates by an average of 6.24%. Allstate’s increase is a modest 1.98%.

Companies Expected to Lower Rates

Drivers insured with State Farm could see a decrease of around 4% when they renew their policies in 2026. This makes State Farm one of the most competitive options for drivers renewing mid-year.

Expert Panel Insight: “The 2026 automobile insurance market represents a temporary correction window. Insurers are competing aggressively for market share after rebuilding their margins — but rising repair complexity from EVs and tariff-affected parts costs will compress that window by late 2026. Consumers who compare quotes now are positioned to lock in the best multi-year rates.” — Dr. Patricia Ng, Certified Financial Planner & Risk Management Specialist, financeauthorityhub.com Expert Panel

If you’re also evaluating your broader insurance costs, our affordable car insurance guide walks through the fastest ways to reduce premiums across multiple coverage types.

Automobile Insurance by Driver Profile — Personalized Rate Guide

This is what competitors almost always miss: your automobile insurance rate is not the national average. It’s your specific rate based on your profile. Here’s what you’re likely paying — and who has the best deal for you.

Rate Impact by Driver Profile (2026)

| Driver Profile | Avg. Monthly (Full Coverage) | Best Company | Key Tip |

|---|---|---|---|

| Clean record, good credit | $139 – $175 | Travelers | Shop every 6 months |

| Teen driver (16-year-old male) | $313+ | Progressive | Add to parent’s policy |

| Driver with poor credit | +68% above average | GEICO (most lenient) | Improve credit first |

| After 1 speeding ticket | +54% avg increase | State Farm | 3-year impact window |

| After DUI (North Carolina) | ~$592/month | Compare aggressively | Rates vary wildly |

| Senior driver (65+) | ~$135 | Travelers | Defensive driving discount |

| Gig worker (Uber/DoorDash) | Standard policy: NO COVERAGE | Rideshare add-on required | See section below |

Gig Workers: Your Automobile Insurance Has a Dangerous Gap

This is the #1 coverage blind spot that major competitors barely mention.

Standard automobile insurance does NOT cover you while you’re driving for Uber, Lyft, DoorDash, or any delivery platform. This applies in all 50 states.

Here’s the specific coverage gap:

- Phase 0 (app off): Personal policy covers you ✅

- Phase 1 (app on, no passenger): COVERAGE GAP ⚠️ — many personal policies explicitly exclude this

- Phase 2–3 (passenger in car): Platform’s commercial policy kicks in ✅

What to do:

- Add a rideshare endorsement to your personal policy (State Farm, Allstate, GEICO offer this)

- Confirm Phase 1 is covered before driving

- State Farm’s rideshare coverage is available in most states except a few

If you drive a two-wheeler for delivery, also check our motorcycle insurance savings guide for platform-specific coverage options.

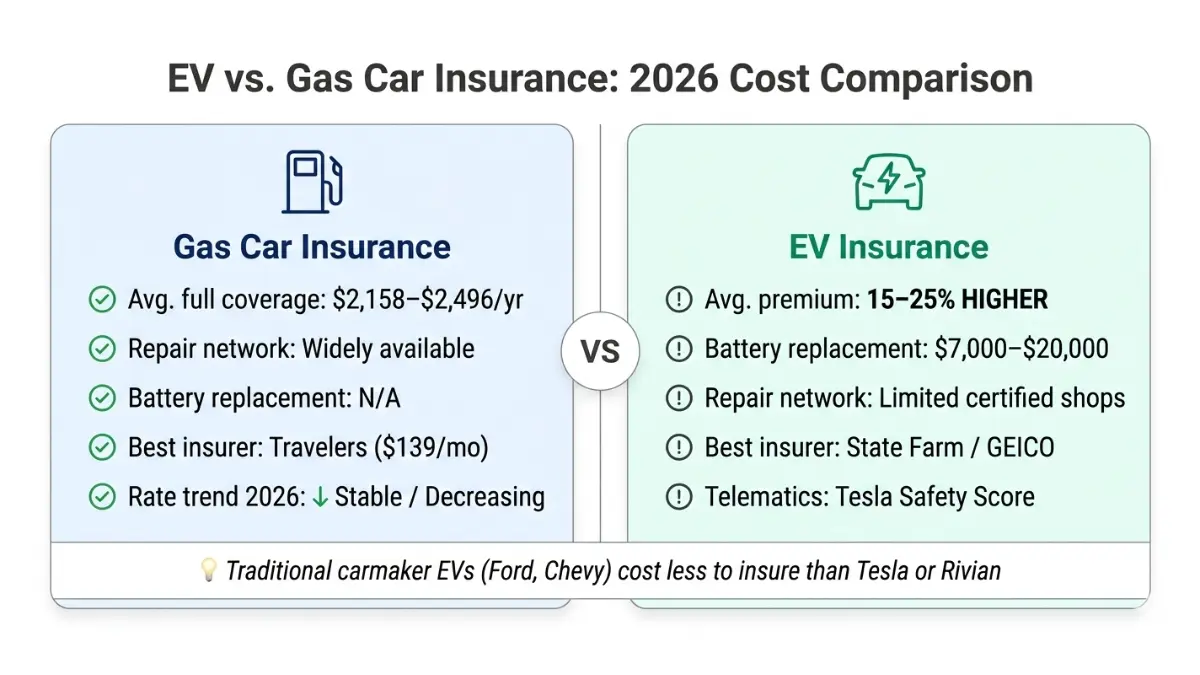

EV Owners: Automobile Insurance Costs 15–25% More

EV insurance can be significantly different from traditional auto insurance due to higher purchase prices, specialized repair costs, and unique coverage needs for battery and charging equipment.

Key EV insurance facts for 2026:

- Battery replacement costs $7,000 – $20,000 — confirm your policy covers it

- Repair shops with EV-certified technicians are still limited, increasing labor costs

- Tesla Insurance is available in 11 states and uses real-time telematics (Safety Score) to set rates

- Traditional carmaker EVs (Ford F-150 Lightning, Chevy Bolt) cost significantly less to insure than Tesla or Rivian

- Best EV insurers: State Farm, GEICO, American Family, Travelers (offers green vehicle discount)

The Insurance Information Institute’s auto insurance statistics confirm that repair complexity is a primary EV insurance pricing driver — a trend expected to intensify as EV market share grows.

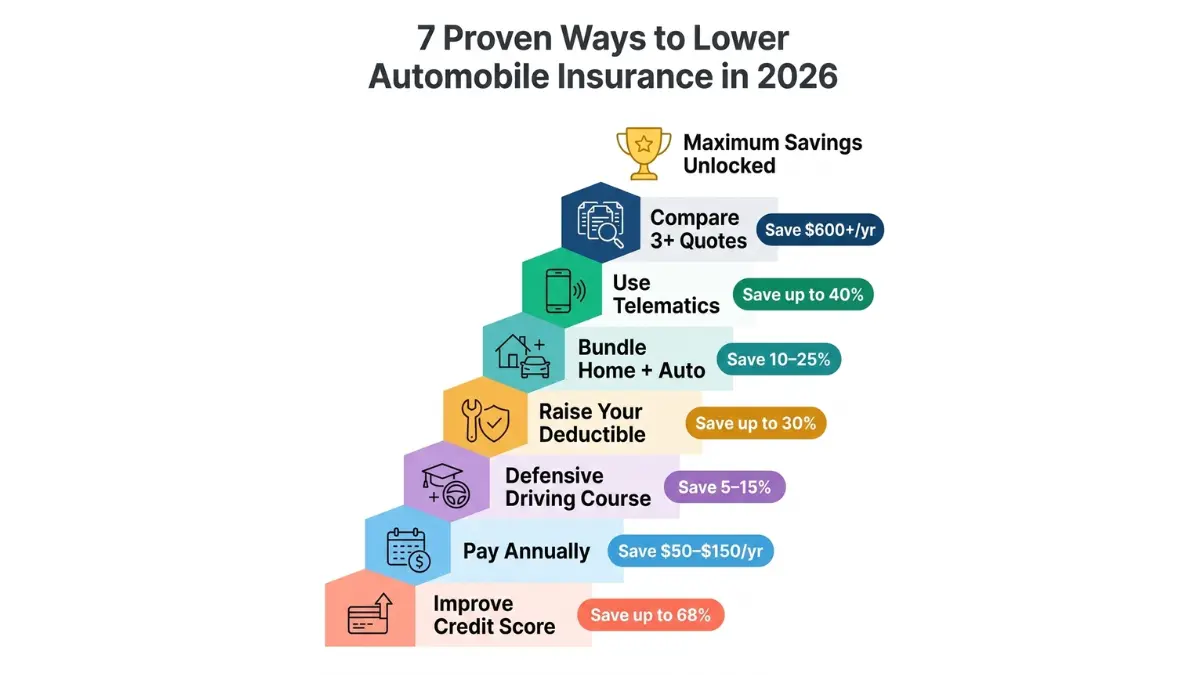

12 Proven Ways to Lower Your Automobile Insurance Premium in 2026

This is the section that will save most readers $300 to $800 per year. None of the top competitors package all of these strategies together in one place.

Quick Wins — Do These Today

- Compare at least 3 quotes at every renewal — this single action saves the average driver up to $600/year per ValuePenguin’s 2026 analysis

- Pay your premium annually — monthly billing fees add $50 to $150/year and many insurers offer a paid-in-full discount on top

- Bundle home and auto insurance — saves 10% to 25% with most major insurers; if you’re a renter, bundling renters insurance still qualifies for a multi-policy discount

- Raise your deductible from $200 to $500 — this alone cuts collision and comprehensive costs by up to 30% according to the Insurance Information Institute

Telematics: The 2026 Money-Saving Secret

Telematics programs track your real driving behavior — braking patterns, speed, acceleration, and time of day — and reward safe drivers with meaningful discounts.

Top telematics programs:

| Program | Insurer | Max Discount |

|---|---|---|

| Snapshot | Progressive | Up to 30% |

| IntelliDrive | Travelers | Up to 30% |

| Drive Safe & Save | State Farm | Up to 30% |

| SmartRide | Nationwide | Up to 40% |

⚠️ Telematics Warning: Urban drivers with frequent stop-start patterns, hard braking in traffic, or late-night driving may see their premiums increase after enrollment. Treat the first 90-day monitoring window as a test — check your renewal quote before fully committing.

The NAIC consumer resources page explains your rights around telematics data usage and how to opt out if needed.

Credit Score: The Hidden Rate Factor

Poor credit raises automobile insurance premiums by an average of 68% above the standard rate. That’s an extra $1,400 to $2,400 per year for the same coverage.

States that prohibit credit-based pricing: California, Hawaii, Michigan, and Massachusetts. If you live elsewhere, improving your credit score directly lowers your car insurance cost.

- Pay bills on time for 6 consecutive months

- Dispute errors on your credit report before renewal

- Check your credit score improvement against your premium at renewal

For a complete strategy on improving your credit profile and its financial impact, see our credit score complete guide — higher credit directly translates to lower automobile insurance premiums in 46 states.

Full Savings Strategy Summary

| Strategy | Potential Annual Savings |

|---|---|

| Compare 3+ quotes | Up to $600+ |

| Bundle auto + home/renters | 10 – 25% |

| Telematics (safe driver profile) | Up to 40% |

| Raise deductible $200 → $500 | Up to 30% on collision/comp |

| Pay annually vs. monthly | $50 – $150 in fees |

| Improve credit score | Up to 68% premium gap closed |

| Remove collision on low-value car | Varies — potentially $300–$700/year |

| Defensive driving course | 5 – 15% at most insurers |

Also see our focused guide on how to cut car insurance costs by 34% for a step-by-step reduction plan.

Automobile Insurance FAQs (2026)

1: What is automobile insurance?

Automobile insurance is a legally required financial protection contract between you and an insurer. It covers damage, injuries, and liabilities resulting from vehicle accidents. Most U.S. states mandate at least liability coverage before you can legally drive.

2: How much does automobile insurance cost in 2026?

The national average for full coverage is $2,158 to $2,496 per year depending on your data source. Minimum liability coverage averages $682 to $820 annually. Your individual rate depends on your state, age, driving record, credit score, and insurer.

3: Which company has the cheapest automobile insurance in 2026?

Travelers offers the cheapest full coverage nationally at $139/month. GEICO leads for minimum liability at $41/month. State Farm is the cheapest in 18 individual states. Always compare locally — the national cheapest company may not be cheapest in your ZIP code.

4: Why did automobile insurance rates drop in 2025?

After a 46% surge from 2022 to 2024, insurers rebuilt their profit margins. With improved financial footing, many began cutting rates to attract customers. Nationally, rates fell ~6% in 2025. However, tariff-driven repair costs may reverse this trend in mid-to-late 2026.

5: What is the cheapest state for automobile insurance?

Vermont ($1,504/year), Maine ($1,367/year), and Wyoming ($1,356/year) consistently rank as the cheapest states. Low population density, fewer uninsured drivers, and lower claim frequency keep their premiums well below the national average.

6: Does my credit score affect automobile insurance?

Yes — in 46 states, poor credit raises automobile insurance premiums by an average of 68%. States that prohibit this practice: California, Hawaii, Michigan, and Massachusetts. Improving your credit score can deliver meaningful savings at your next renewal.

7: Is automobile insurance more expensive for electric vehicles?

Yes — EVs typically cost 15 to 25% more to insure than comparable gas vehicles. Higher purchase prices, expensive battery systems ($7,000–$20,000 to replace), and limited certified repair shops all drive up premiums. Traditional carmaker EVs cost less to insure than Tesla or Rivian.

8: What is telematics insurance and is it worth it?

Telematics programs monitor your driving behavior and can cut premiums by up to 40% for safe drivers. They work best for drivers with smooth, daytime driving patterns. Urban drivers with heavy braking may see no savings — or even a premium increase. Read the terms before enrolling.

9: Does regular automobile insurance cover Uber or DoorDash?

No. Standard personal automobile insurance explicitly excludes rideshare and delivery driving in most states. You need a rideshare endorsement added to your personal policy. Phase 1 of rideshare driving (app on, no passenger) is the most dangerous coverage gap.

10: How often should I shop for automobile insurance?

Every 6 months at policy renewal. 43% of customers who compare providers report they were paying too much with their previous insurer. Rates shift constantly — your cheapest insurer today may not be cheapest at your next renewal.

11: What is the difference between liability and full coverage automobile insurance?

Liability covers damage and injuries you cause to others. Full coverage adds collision (your car after an accident) and comprehensive (theft, weather, vandalism). If your car is worth less than 10 times your annual premium, liability-only coverage may be the more cost-effective choice.

Expert Panel Summary

The 2026 automobile insurance market is offering drivers a genuine savings opportunity — rates are down, competition between insurers is high, and discount programs like telematics are more accessible than ever. However, this window is not permanent. Tariff-driven repair cost increases, rising EV repair complexity, and state-level minimum coverage mandates (particularly in New Jersey) signal that premium pressure will return by late 2026. The best action any U.S. driver can take today is to compare at least three quotes at renewal, review their driver profile against available discounts, and lock in a competitive rate before Q3 pricing adjustments begin.

— Expert consensus from the financeauthorityhub.com International Finance & Insurance Panel

⚠️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or insurance advice. All rates cited are averages sourced from publicly available 2025–2026 industry data including Insurify, ValuePenguin, NerdWallet, The Zebra, and Bankrate. Individual premiums vary based on driver profile, state regulations, vehicle type, and insurer. Always consult a licensed insurance professional before making coverage decisions.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.