Temporary Car Insurance: Cheapest Options (2026)

True temporary car insurance is rare — but 7 legitimate options exist in 2026, starting at $3/day. This expert guide matches your situation to the cheapest solution, fast.

In This Article

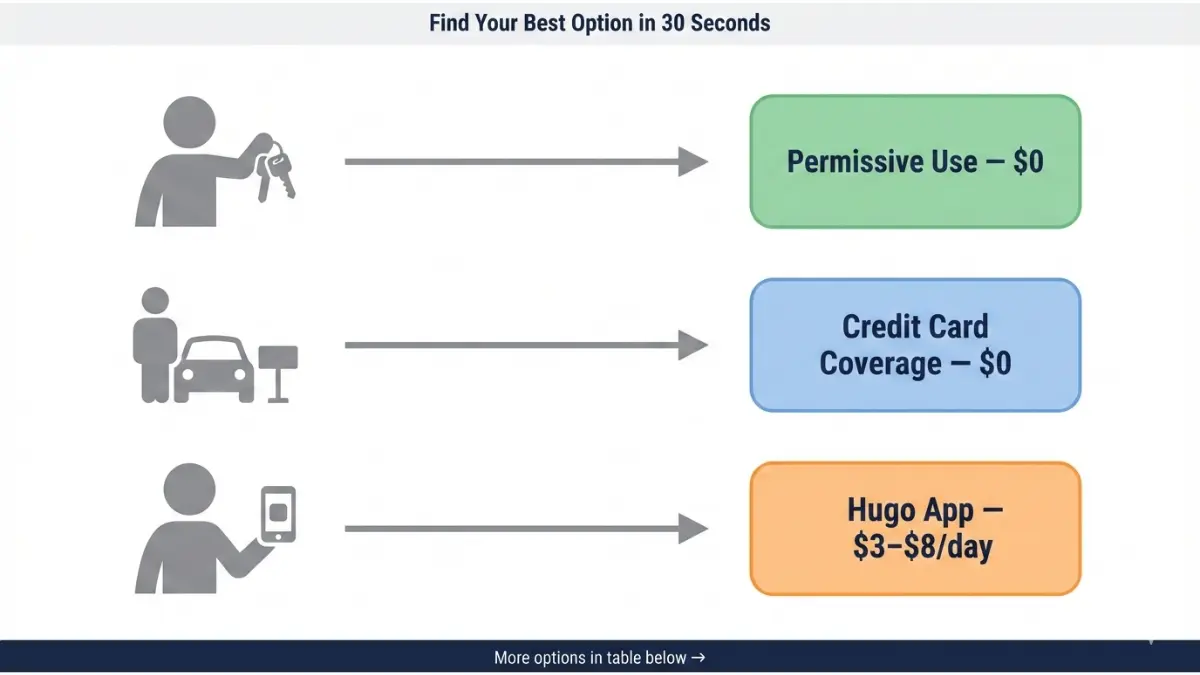

Temporary car insurance gives you short-term auto coverage — from a single day to a few months — without locking into a 6-month or annual policy. In 2026, true “temporary” policies are rare from major insurers, but seven legitimate, affordable options exist. The cheapest starts at $0 (credit card coverage) or $3/day (Hugo). You can get covered in 15 minutes or less.

Quick Cost Snapshot: All 7 Options at a Glance

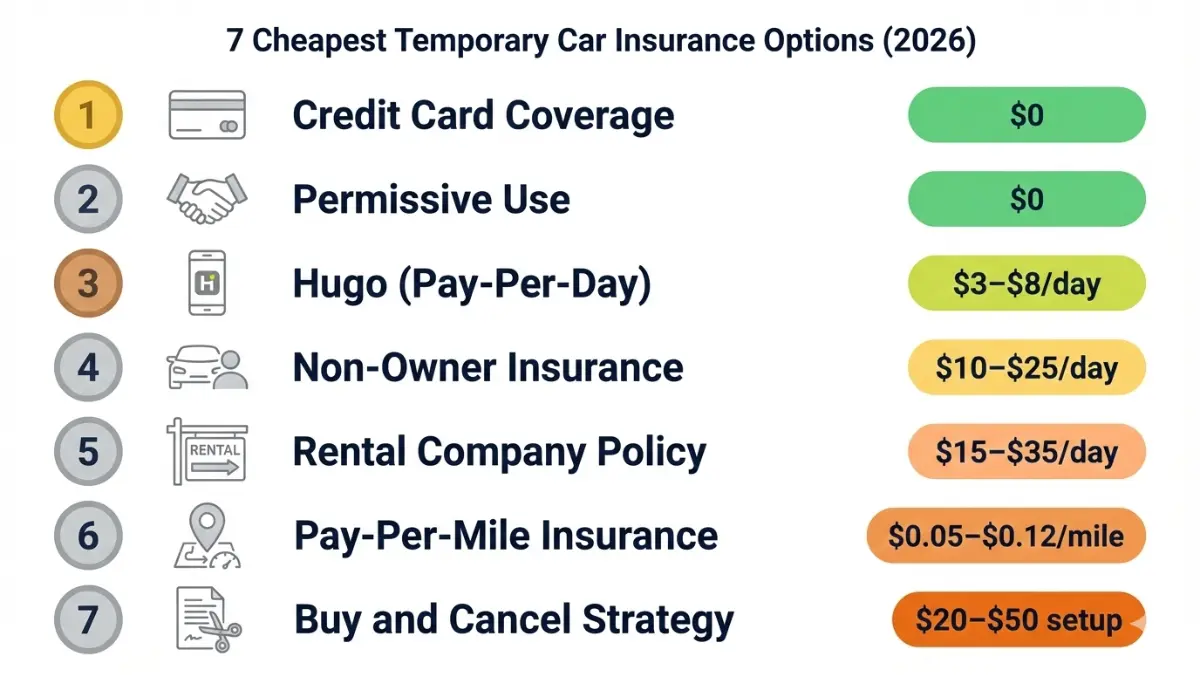

| Coverage Type | Est. Cost | Best For | Same-Day? |

|---|---|---|---|

| Credit card rental coverage | $0 (free perk) | Renting a car | ✅ Yes |

| Permissive use (friend’s policy) | $0 | Borrowing once | ✅ Yes |

| Hugo pay-per-day | $3–$8/day | Infrequent drivers | ✅ Yes |

| Non-owner car insurance | $15–$30/mo | No car, borrowing often | ✅ Yes |

| Rental company coverage | $15–$30/day | Renting short-term | ✅ Yes |

| Pay-per-mile insurance | $20–$50/mo base | Under 7,500 mi/year | ✅ Yes |

| Buy 6-month + cancel early | $29–$97/mo | Own a car temporarily | ✅ Yes |

⚠️ 2026 Scam Alert: Any website promising “instant 1-day personal vehicle insurance” outside of Hugo or a rental company is almost certainly a scam.

Does Temporary Car Insurance Actually Exist in 2026?

The honest answer: not in the way most people think.

No major U.S. insurer — GEICO, Progressive, State Farm, Allstate — sells a standalone 1-day or 1-week policy for your personal vehicle. Standard policies run 6 or 12 months minimum.

But you have seven legitimate workarounds that provide real, legal short-term coverage. Some cost nothing. Others cost a few dollars per day. All of them can be activated today.

The key is matching your specific situation to the right option — something every top competitor fails to do clearly.

Match Your Situation to the Cheapest Option

Don’t waste time reading about options that don’t apply to you. Find your situation below and go straight to the answer.

| Your Situation | Best Option | Avg. Cost |

|---|---|---|

| Renting a car this weekend | Credit card or rental company coverage | $0–$30/day |

| Borrowing a friend’s car once | Permissive use (their policy covers you) | $0 |

| Borrowing regularly for 1–3 months | Non-owner car insurance | $15–$30/mo |

| Just bought a car, driving it home | Your existing policy’s 30-day auto-transfer | $0 extra |

| College student, car stored at home | “Student Away” discount on parent’s policy | Save 15–30% |

| Military member deploying | USAA storage/deployment discount | Save up to 60% |

| Own a car, drive rarely | Hugo or pay-per-mile insurance | $3–$8/day |

| Between policies, need a bridge | Buy 6-month policy + cancel for prorated refund | $29–$97/mo |

Key Point: As the Insurance Information Institute explains, most standard auto policies already extend coverage to people who drive your car with your permission — a provision called permissive use. Many drivers don’t realize they’re already partially covered.

The 7 Cheapest Temporary Car Insurance Options — Ranked by Cost (2026)

#1 — Credit Card Rental Coverage (Often Free)

This is the most overlooked option in every competitor article. If you’re renting a car, check your credit card benefits before paying $15–$30/day to the rental company.

Cards from Chase Sapphire, Capital One Venture, and American Express Platinum provide collision damage waiver (CDW) coverage as a free perk. Coverage typically includes:

- Damage to the rental vehicle

- Theft protection

- Towing costs

Limitations: Most cards exclude liability coverage (injuries to others), certain vehicle types (trucks, RVs, luxury cars), and international rentals. Always read the fine print. The Consumer Financial Protection Bureau has a clear guide on exactly what credit card auto coverage includes and excludes.

Expert Tip: Pay for the rental with your card — many cards require this for coverage to activate.

#2 — Permissive Use (Your Friend’s Policy Covers You)

If you’re borrowing someone’s car with their permission, their insurance policy likely covers you — even if you’re not listed on it. This is called permissive use and is standard in most U.S. auto policies.

- You’re covered for liability, collision, and comprehensive (same as the car owner’s coverage)

- Coverage typically reduces if you’re a “regular” driver of the vehicle

- If you drive the car frequently, the insurer can deny claims

Bottom Line: For one-time or very occasional borrowing, permissive use is your cheapest (free) solution. For anything more regular, look at a non-owner policy instead.

#3 — Hugo Pay-Per-Day Insurance ($3–$8/day)

Hugo is the only legitimate pay-per-day car insurance option for personal vehicles in the U.S. as of 2026. It operates in 13 states and lets you buy coverage in 3, 7, 14, or 30-day increments.

How it works:

- Download the Hugo app and set up an account

- Buy days of coverage in advance — as few as 3 days at a time

- Pause coverage on days you don’t drive (saves money)

- Resume without any reactivation fee

2026 Cost Estimate: $3–$8/day depending on your state, driving record, and vehicle type.

Important Limitations:

- State-minimum liability coverage only — no full coverage option

- Not available for financed or leased vehicles (lenders require continuous full coverage)

- Currently available in: TX, CA, GA, IL, OH, PA, TN, MO, IN, WI, VA, AZ, SC

If you drive infrequently and own your car outright, Hugo is genuinely the cheapest temporary solution available.

#4 — Non-Owner Car Insurance ($15–$30/month)

Non-owner car insurance covers you as a driver, not a specific vehicle. It’s ideal if you borrow cars regularly but don’t own one yourself.

Best providers for non-owner policies in 2026:

| Provider | Avg. Monthly Cost | Availability |

|---|---|---|

| GEICO | $15–$25/mo | All 50 states |

| Travelers | $18–$28/mo | All 50 states |

| State Farm | $20–$30/mo | All 50 states |

| Progressive | $22–$32/mo | All 50 states |

What it covers:

- Bodily injury liability

- Property damage liability

- Optional: uninsured motorist, medical payments

What it doesn’t cover: Damage to the vehicle you’re driving (that’s covered by the car owner’s policy).

Non-owner insurance is also required in some states to reinstate a suspended license after a DUI or serious violation — making it valuable beyond just temporary coverage. Also consider reviewing your options in our comprehensive cheap insurance guide for additional strategies to reduce overall insurance costs.

#5 — Rental Company Daily Coverage ($15–$30/day)

Rental companies offer their own daily coverage at the counter. It’s convenient but can be expensive — adding $450+ to a two-week rental.

Coverage types offered:

- CDW/LDW (Collision/Loss Damage Waiver): Covers rental vehicle damage — typically $10–$15/day

- Liability Supplement: Covers injury/property damage to others — $7–$15/day

- Personal Accident Insurance: Medical coverage for you/passengers — $3–$7/day

When it’s worth buying: Only if your credit card doesn’t offer rental coverage and your personal auto policy doesn’t extend to rentals. Always check those two sources first — you could be paying for duplicate coverage.

#6 — Pay-Per-Mile Insurance ($20–$50/month base + per-mile rate)

Pay-per-mile insurance charges a low monthly base rate plus a small rate per mile driven — typically $0.05–$0.10 per mile.

Best for: Drivers who drive under 7,500 miles per year — commuters who work from home, urban residents, retirees, or seasonal drivers.

Top 2026 providers:

- Mile Auto — Tracks mileage via odometer photo (no tracking device required); ~$29–$59/mo base

- Nationwide SmartMiles — Strong coverage options; available in most states

- Metromile (now Lemonade) — Full digital management; telematics-based

Savings potential: Drivers under 5,000 miles/year can save 30–50% versus a standard 6-month policy, according to the National Association of Insurance Commissioners 2026 data.

#7 — Buy a 6-Month Policy + Cancel Early (Prorated Refund)

This is the most common workaround used by Americans needing short-term coverage for their own vehicle. Here’s how to do it without getting penalized.

Step-by-step:

- Purchase a standard 6-month policy from a no-cancellation-fee insurer

- Pay monthly (don’t pay in full — harder to get refunded)

- Cancel when you no longer need coverage

- Receive a prorated refund for unused premium

Cancellation fee comparison — 2026:

| Insurer | Cancellation Fee | Refund Policy |

|---|---|---|

| GEICO | $0 | Full prorated refund |

| Nationwide | $0 | Full prorated refund |

| Progressive | $0 | Full prorated refund |

| Allstate | ~$50 | Prorated minus fee |

| Farmers | Varies | Short-rate penalty may apply |

Expert Tip: “Always choose an insurer with $0 cancellation fees when you need temporary coverage. A $50 fee on a 1-week policy can increase your effective cost by 179%.” — MoneyGeek data, 2026.

If you’re also navigating broader debt and budget pressures alongside insurance costs, our debt consolidation calculator can help you see where insurance fits into your overall financial picture.

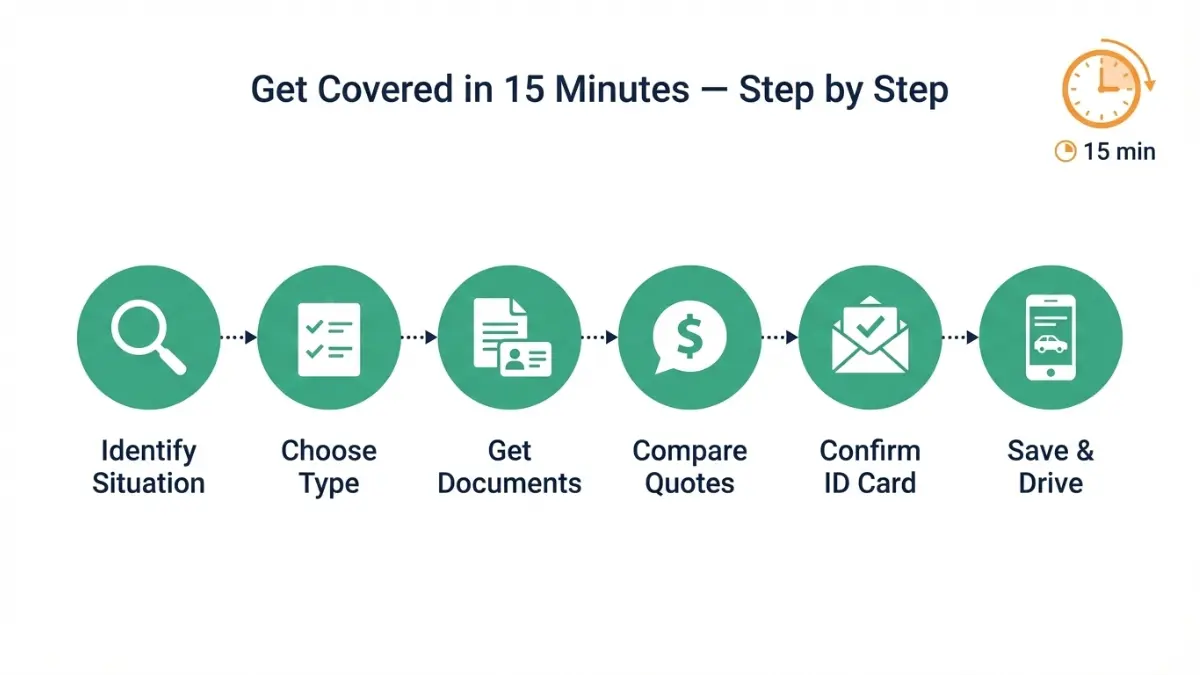

How to Get Temporary Car Insurance Today — In 15 Minutes

No competitor gives you a step-by-step same-day guide. Here it is.

What you need ready before you start:

- Driver’s license number

- Vehicle VIN (if applicable)

- Current home address

- Payment method (credit or debit card)

- Proof of prior insurance (if available — lowers your rate)

6 Steps to Get Covered Right Now:

- Identify your situation — Use the scenario matrix in Section 2

- Choose your coverage type — Credit card, non-owner, Hugo, or buy-and-cancel

- Get at least 3 quotes — Use GEICO, Progressive, and Nationwide for the fastest online quotes

- Confirm same-day digital ID card delivery — Most major insurers email it within minutes

- Screenshot or download your insurance card — A policy number alone is NOT proof of insurance in most states

- Verify your coverage start time — Some policies activate immediately; others at 12:01 AM the next day

Critical: Never assume coverage has started. Confirm the exact activation time with your insurer before driving. If you’re also carrying other insurance products, see how bundling could lower your overall premium in our car insurance cost-cutting guide.

2026 Temporary Car Insurance Scams — Red Flags & Real Consequences

This section doesn’t exist in any meaningful depth on competitor sites. It should — and now it does.

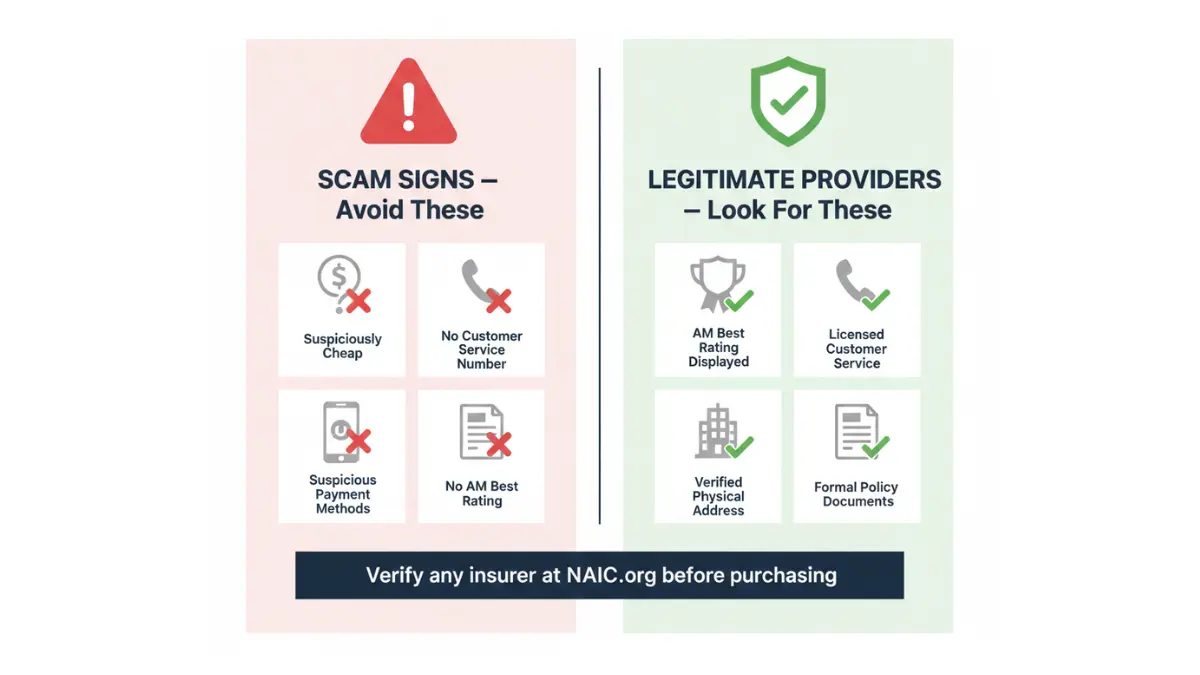

Red Flags: How to Spot a Fake Temporary Insurance Provider

Watch for these warning signs before entering your payment information:

- Promises “instant 1-day personal vehicle coverage” outside of Hugo — no legitimate U.S. insurer offers this

- No AM Best rating or state license number displayed

- Prices below $2/day for full coverage on a personal vehicle

- Payment via Venmo, Zelle, or cryptocurrency only

- No physical address or customer service phone number

- No formal policy documents — just a “confirmation email”

If a site offers you daily personal auto insurance at suspiciously low rates, it is almost certainly collecting your payment and personal data without providing real coverage. You would be driving uninsured.

What Happens If You Drive Without Insurance — Even for One Day?

Driving uninsured is illegal in 49 states. The penalties are severe and lasting.

| State | Minimum Fine (1st Offense) | License Suspension? | SR-22 Required After? |

|---|---|---|---|

| California | $100–$200 + fees | Possible | Yes |

| Texas | $175–$350 | Yes | Yes |

| Florida | $150–$500 | Yes (up to 3 years) | Yes |

| New York | $150–$1,500 | Yes | Yes |

| Illinois | $500–$1,000 | Yes | Yes |

Beyond fines: if you cause an accident while uninsured, you’re personally liable for all damages — medical bills, vehicle repair, legal costs — which can run into hundreds of thousands of dollars.

Check your state’s specific minimum coverage requirements directly at the NAIC State Insurance Map, which links to every state’s official insurance regulator.

The Coverage Gap Penalty — Don’t Let This Happen to You

A coverage gap of 30+ days signals risk to future insurers. When you reapply for coverage:

- Premiums increase 10–30% above standard rates

- Some insurers may decline to cover you

- The gap stays on your insurance history for 3–5 years

The fix is simple: never let coverage lapse. Even the cheapest non-owner policy at $15/month is worth maintaining to protect your insurance history. For a complete view of how insurance fits into your overall protection strategy, explore our comprehensive insurance overview.

Frequently Asked Questions about Temporary Car Insurance

Q1: Is temporary car insurance legal in the USA?

Yes. Any valid, state-compliant insurance policy is legal — whether it’s a 6-month policy you cancel after one week, a Hugo pay-per-day plan, or a non-owner policy. What’s illegal is driving without coverage.

Q2: Can I get temporary car insurance the same day?

Yes. GEICO, Progressive, Nationwide, and Hugo all offer same-day coverage with instant digital ID card delivery. Most policies activate within minutes of payment.

Q3: What is the cheapest temporary car insurance option in 2026?

The cheapest option depends on your situation. Credit card rental coverage is free if you already have an eligible card. Hugo is the cheapest for personal vehicle coverage at $3–$8/day. Non-owner policies average $15–$30/month.

Q4: Does getting temporary car insurance affect my credit score?

No. Purchasing or canceling a car insurance policy has no impact on your credit score. Insurers may perform a soft credit check when quoting you, which also doesn’t affect your score.

Q5: Can I cancel my car insurance the same day I buy it?

Yes, in most states. You’re entitled to a prorated refund of unused premium. Choose insurers with $0 cancellation fees — GEICO, Progressive, and Nationwide — to avoid penalties.

Q6: What is non-owner car insurance and do I need it?

Non-owner car insurance covers you as a driver when operating vehicles you don’t own. It’s worth getting if you borrow cars regularly, use car-sharing services frequently, or need to maintain continuous coverage to avoid a gap in your insurance history.

Q7: Does Hugo offer full coverage temporary car insurance?

No. As of 2026, Hugo provides state-minimum liability coverage only in 13 states. It does not offer collision, comprehensive, or full coverage, and it cannot be used on financed or leased vehicles.

Q8: Is pay-per-mile insurance a good temporary option?

Yes — if you drive fewer than 7,500 miles per year. Mile Auto and Nationwide SmartMiles are the top 2026 picks. For low-mileage drivers, pay-per-mile can cost 30–50% less than a standard policy.

Q9: Can a college student get temporary car insurance?

Yes. The most cost-effective option for most students is a “Student Away From Home” discount added to a parent’s existing policy. This can reduce the family’s premium by 15–30% while maintaining coverage when needed.

Q10: Will a temporary coverage gap raise my future insurance rates?

Yes. A gap of 30 or more days can raise your next premium by 10–30% and may cause some insurers to classify you as higher risk. Always maintain at least a minimal policy — even a $15/month non-owner plan — to preserve your insurance history.

Q11: How do I know if a temporary car insurance website is a scam?

Legitimate insurers display a valid AM Best rating, a state license number, a physical address, and formal policy documentation. Any site promising “instant daily personal vehicle coverage” outside of Hugo, or requesting payment via Venmo or Zelle, should be avoided entirely. Verify any insurer’s license through your state insurance department via the NAIC.

Expert Panel Summary

Our licensed insurance experts at financeauthorityhub.com consistently recommend starting with what you already have — your credit card’s rental coverage, your friend’s permissive use policy, or your existing insurer’s auto-transfer window — before purchasing new temporary coverage.

When new coverage is needed, Hugo for pay-per-day and non-owner policies from GEICO or Travelers represent the best 2026 value for most American drivers. Always avoid coverage gaps, always verify same-day activation, and always download your digital insurance card before driving.

If you’re also evaluating broader insurance needs, our guides on motorcycle insurance, holiday insurance, and renters insurance cover related coverage decisions with the same depth.

📌 Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or insurance advice. Insurance rates, availability, regulations, and provider offerings vary by state and individual circumstances. Always consult a licensed insurance professional before making coverage decisions. Data reflects available 2026 market information and is subject to change. financeauthorityhub.com is not affiliated with any insurance provider mentioned in this article.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.