Term Life Insurance 2026: From $26/mo + Rate Calculator

Discover 2026 term life insurance rates starting at $26/month. Compare costs by age, coverage amounts, and term lengths. Calculate how much protection your family needs today.

In This Article

Protect your family’s financial future for less than a streaming subscription. Term life insurance provides affordable death benefit coverage for 10-30 years, with 2026 rates starting at just $26 monthly for healthy 30-year-olds. This complete guide reveals exactly how much coverage you need, what you’ll pay, and strategies top advisors use to maximize protection while minimizing costs.

What Is Term Life Insurance? (2026 Complete Answer)

Term life insurance is temporary coverage that pays a death benefit to your named beneficiaries if you die during a specified policy term. Unlike permanent life insurance policies that build cash value, term life focuses purely on affordable protection for periods typically ranging from 10 to 30 years.

Here’s how term life works in three simple steps:

1. Choose Your Coverage & Term

Select a death benefit amount (typically $250,000-$2 million) and term length (10, 20, or 30 years) based on your family’s needs.

2. Pay Fixed Premiums

Your monthly premium stays level throughout the entire term—no surprise increases if your health changes.

3. Protection When It Matters

If you die during the policy term, your beneficiaries receive the full death benefit tax-free to cover expenses and replace lost income.

2026 Average Term Life Insurance Costs by Age

| Age | $500K Coverage (20-year) | $1M Coverage (20-year) |

|---|---|---|

| 30 | $26-$31/month | $42-$50/month |

| 40 | $37-$46/month | $62-$84/month |

| 50 | $98-$124/month | $168-$215/month |

| 60 | $247-$315/month | $472-$590/month |

Source: 2026 industry rate data from multiple insurers for healthy, non-smoking applicants

The bottom line: Term life insurance costs significantly less than whole life insurance policies because it doesn’t include cash value accumulation or lifelong coverage. This makes it ideal for families needing maximum protection during peak financial responsibility years—like paying off a mortgage, raising children, or building retirement savings.

According to the National Association of Insurance Commissioners, term life policies account for the majority of life insurance purchases specifically because they balance affordability with substantial death benefit protection. When integrated with proper financial planning tools, term life insurance becomes a cornerstone of family financial security.

2026 Term Life Insurance Rates—Complete Cost Breakdown

Understanding exactly what you’ll pay is critical to making smart coverage decisions. Term life insurance premiums vary based on five primary factors, with some creating dramatic cost differences.

How Much Does Term Life Insurance Cost by Age?

Age is the single biggest rate driver. Every decade you wait increases premiums by approximately 50-70% for the same coverage amount.

Real 2026 Rates—$500,000 Coverage, 20-Year Term:

| Age Group | Male (Monthly) | Female (Monthly) | Annual Difference |

|---|---|---|---|

| 25-29 | $23 | $19 | $48 saved |

| 30-34 | $26 | $22 | $48 saved |

| 35-39 | $31 | $26 | $60 saved |

| 40-44 | $43 | $37 | $72 saved |

| 45-49 | $67 | $57 | $120 saved |

| 50-54 | $110 | $91 | $228 saved |

| 55-59 | $181 | $148 | $396 saved |

| 60-64 | $295 | $235 | $720 saved |

Key insight: Women consistently pay 15-20% less than men for identical coverage due to longer life expectancy. A 40-year-old woman saves approximately $72 annually compared to a same-age male.

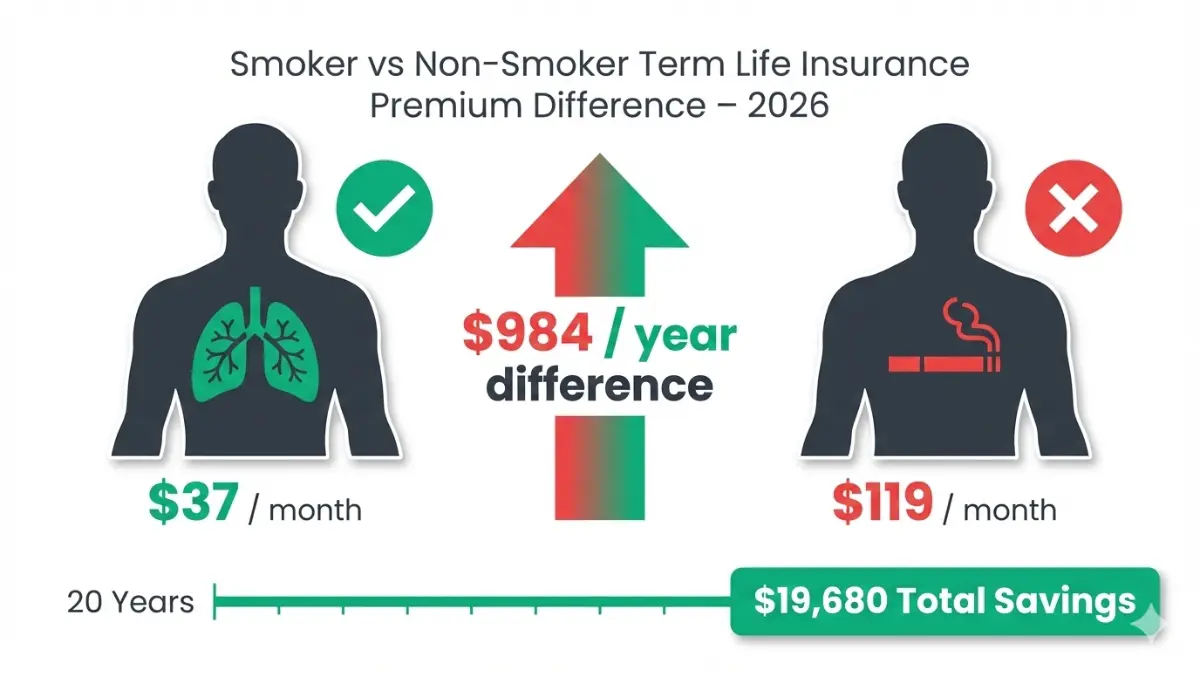

Smoker vs Non-Smoker: Save $4,000+ Annually

Tobacco use creates the most dramatic premium impact outside of age.

$500,000 Coverage, 40-Year-Old, 20-Year Term:

- Non-smoker: $37/month ($444/year)

- Smoker: $119/month ($1,428/year)

- Annual difference: $984 ($19,680 over 20 years)

For $1 million coverage, smokers pay an additional $2,400+ annually. Many insurers offer reconsideration rates if you quit smoking for 12+ months—potentially saving thousands in future premiums.

Case Study: Sarah, 35, switched from smoking to vaping while applying for coverage. By postponing her application six months and fully quitting, she qualified for non-smoker rates, saving $1,488 annually on her $750,000 policy.

Health Class Impact on Premiums

Insurers categorize applicants into health classes affecting final rates:

Health Class Tiers (40-year-old, $500K, 20-year term):

- Preferred Plus: $31/month (top 10% health)

- Preferred: $37/month (top 25% health)

- Standard Plus: $46/month (top 50% health)

- Standard: $58/month (average health)

- Substandard: $78-$145/month (health conditions present)

Factors improving your health class rating include:

- BMI within normal range (18.5-24.9)

- Blood pressure below 130/85

- Cholesterol under 200 mg/dL

- No diabetes or controlled with medication

- No dangerous hobbies (skydiving, rock climbing)

According to IRS guidance on life insurance, death benefits paid to beneficiaries are generally not includable in gross income, making term life an exceptionally tax-efficient wealth transfer tool.

What This Means For You

Getting quotes in your early 30s versus early 40s saves approximately $15,000 over a 20-year term for $500,000 coverage. If you’re considering coverage, sooner is financially advantageous—especially while qualifying for preferred health ratings. Use our mortgage calculator to determine if mortgage protection should be included in your coverage amount.

How Much Term Life Insurance Do You Need in 2026?

Buying too little coverage leaves your family financially vulnerable. Buying too much wastes premium dollars. Here’s the strategic framework financial advisors use to calculate optimal coverage.

The 10-12x Income Rule Explained

Financial planners recommend term life insurance coverage equal to 10-12 times your annual gross income as a starting baseline. This multiple ensures beneficiaries can invest the death benefit conservatively (4-5% returns) and replace your income indefinitely.

Income Replacement Examples:

- $50,000 salary → $500,000-$600,000 coverage

- $75,000 salary → $750,000-$900,000 coverage

- $100,000 salary → $1,000,000-$1,200,000 coverage

- $150,000 salary → $1,500,000-$1,800,000 coverage

However, the income-multiple approach is just your starting point. Comprehensive needs analysis requires four additional calculations.

Complete Coverage Calculation Formula

Total Coverage Needed = (Annual Income × 10) + Outstanding Debts + Future Goals – Existing Assets

1. Income Replacement Component

Annual gross income × 10-12 years = Base coverage

2. Debt Coverage

- Mortgage balance: $______

- Auto loans: $______

- Student loans: $______

- Credit card debt: $______

- Personal loans: $______

3. Future Goal Funding

- College costs (per child): $100,000-$150,000

- Final expenses: $15,000-$30,000

- Emergency reserve: $25,000-$50,000

4. Subtract Existing Assets

- Current life insurance: $______

- Retirement accounts (50% value): $______

- Savings/investments: $______

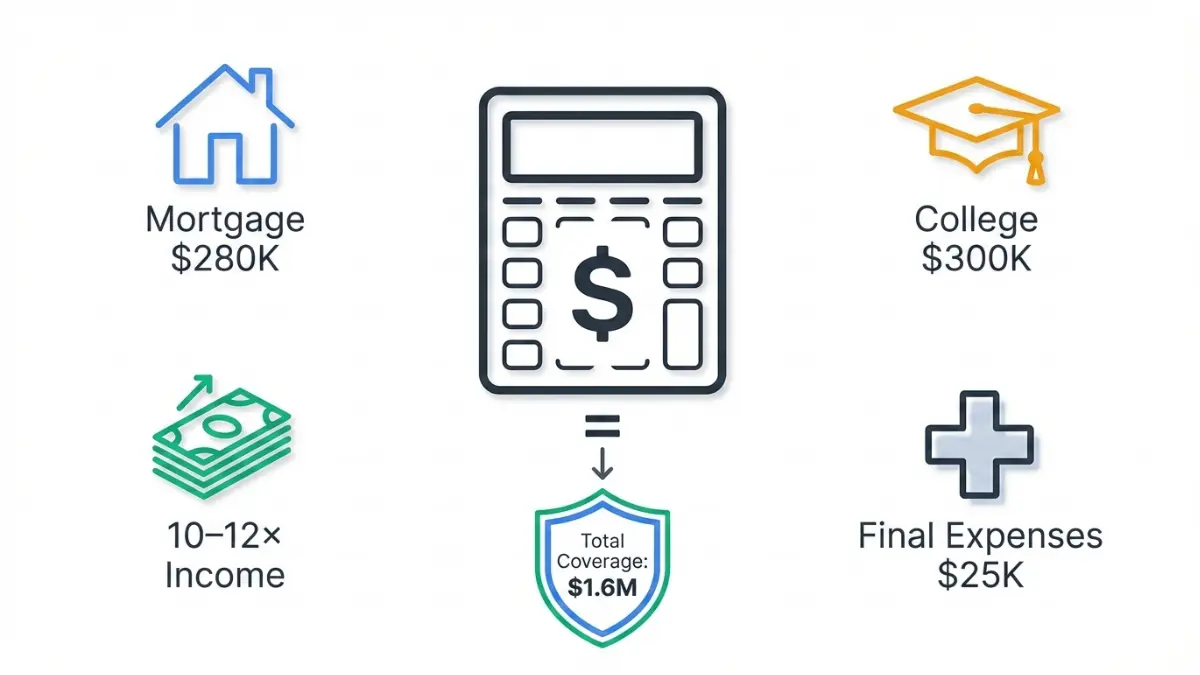

Real Example—Family of Four:

Michael, 38, earns $85,000 annually. His wife Jennifer stays home with their two children, ages 6 and 9.

- Income replacement: $85,000 × 12 = $1,020,000

- Mortgage balance: $280,000

- Auto loan: $18,000

- College fund needed: $300,000 (2 children)

- Final expenses: $25,000

- Emergency reserve: $40,000

- Subtract existing $50K employer policy: -$50,000

- TOTAL NEEDED: $1,633,000

Michael purchased a $1.75 million, 25-year term policy for $147/month—providing comprehensive protection through his children’s college years and mortgage payoff.

Life Stage Coverage Recommendations

Young Professionals (20s-Early 30s)

- Minimum coverage: $250,000-$500,000

- Primary needs: Student loan protection, future family planning

- Average premium: $15-$35/month

Growing Families (30s-40s)

- Recommended coverage: $750,000-$2,000,000

- Primary needs: Mortgage, childcare, college funding

- Average premium: $45-$155/month

Peak Earning Years (Late 40s-50s)

- Recommended coverage: $500,000-$1,500,000

- Primary needs: College costs, final mortgage years, business protection

- Average premium: $110-$285/month

According to financial research from the National Association of Insurance Commissioners, most American families are underinsured by 30-40%, leaving significant financial gaps if the primary earner dies unexpectedly.

For stay-at-home parents, calculate replacement costs for childcare ($15,000-$30,000/year), housekeeping, cooking, transportation, and educational support—often totaling $400,000-$750,000 in coverage needs. Our home affordability calculator helps determine if your current mortgage requires dedicated protection coverage.

Types of Term Life Insurance—Which Is Right for You?

Not all term policies function identically. Understanding the four main term life insurance structures helps you select coverage matching your specific protection timeline and budget.

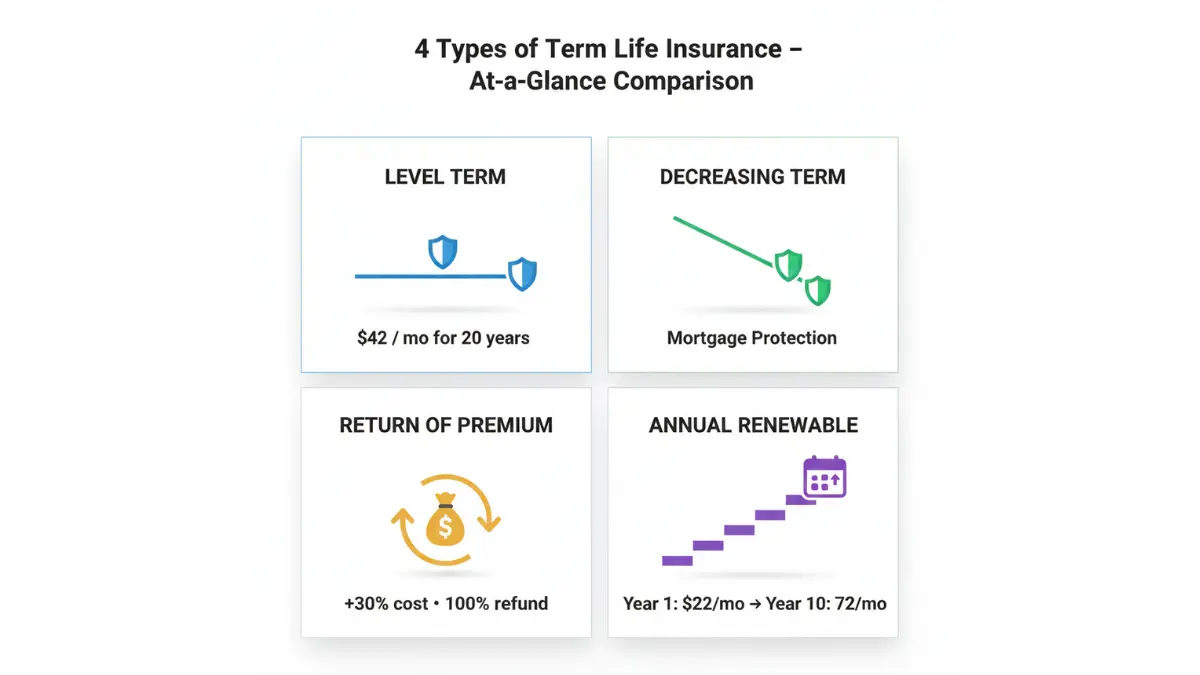

Level Term Life Insurance (Most Popular)

Level term maintains constant premiums and death benefits throughout the entire policy term—10, 15, 20, 25, or 30 years. This is the simplest, most straightforward term life insurance option.

Best for: Mortgage protection, income replacement, predictable budgeting

Example: $500,000 coverage, 20-year level term

- Years 1-20: $42/month premium, $500,000 death benefit

- Premium never increases during term

- Death benefit never decreases

Advantages:

- Predictable budgeting (no premium surprises)

- Highest death benefit for premium dollar

- Easiest to understand and compare

Decreasing Term Life Insurance

Death benefit decreases annually while premiums stay level. Often used for specific debts that decline over time, like mortgages.

Best for: Mortgage protection specifically, business loan coverage

Example: $300,000 coverage, 15-year decreasing term

- Year 1: $300,000 death benefit

- Year 8: $160,000 death benefit

- Year 15: $20,000 death benefit

- Premium: $28/month (fixed)

When it makes sense: If your primary coverage goal is strictly mortgage payoff, decreasing term costs 20-30% less than level term. However, for most families, level term provides more versatile protection.

Return-of-Premium (ROP) Term Life Insurance

ROP policies refund 100% of premiums paid if you outlive the term. This transforms term life into a “zero-cost” insurance product if you survive.

Cost difference: ROP premiums cost approximately 30-50% more than standard term

Example: $500,000 coverage, 30-year ROP term

- Standard term: $55/month ($19,800 total over 30 years)

- ROP term: $78/month ($28,080 total over 30 years)

- Refund if you survive: $28,080

Financial analysis: The $23/month difference ($8,280 over 30 years) invested at 6% annual returns would grow to $24,789—significantly exceeding the premium refund. ROP only makes sense for ultra-conservative savers who wouldn’t otherwise invest the difference.

Annual Renewable Term (ART)

Coverage renews yearly with escalating premiums based on your current age. No medical underwriting required for renewal.

Best for: Short-term coverage needs (1-5 years), bridge coverage between jobs

Example: $250,000 annual renewable term, 40-year-old

- Year 1: $22/month

- Year 5: $38/month

- Year 10: $72/month

- Year 15: $145/month

Caution: By year 20, annual renewable term becomes prohibitively expensive compared to level term purchased initially.

Critical Policy Riders to Consider

Accelerated Death Benefit Rider (Usually included at no cost)

Allows access to 50-100% of death benefit if diagnosed as terminally ill (less than 12-24 months to live). Provides funds for medical care, hospice, or final wishes.

Waiver of Premium Rider ($0.50-$2.00 per $1,000 coverage)

If you become totally disabled for 6+ months, the insurer waives future premiums while keeping coverage active. Critical protection for high-earning professionals.

Child Term Rider ($50-$75 annually per family)

Covers all children in household (typically $10,000-$25,000 each) until age 25. Children can convert to individual permanent policies at age 25 without medical underwriting.

Conversion Option (Standard feature)

Allows converting term life to permanent insurance (whole life or universal life) without medical exam, typically during the first 10-20 years. Essential flexibility if health deteriorates.

According to research from the National Association of Insurance Commissioners, conversion features prove valuable for 15-20% of policyholders whose health changes significantly during their term, making new underwriting impossible or prohibitively expensive.

When evaluating your overall debt strategy, term life insurance ensures debts don’t transfer to surviving family members if you die unexpectedly.

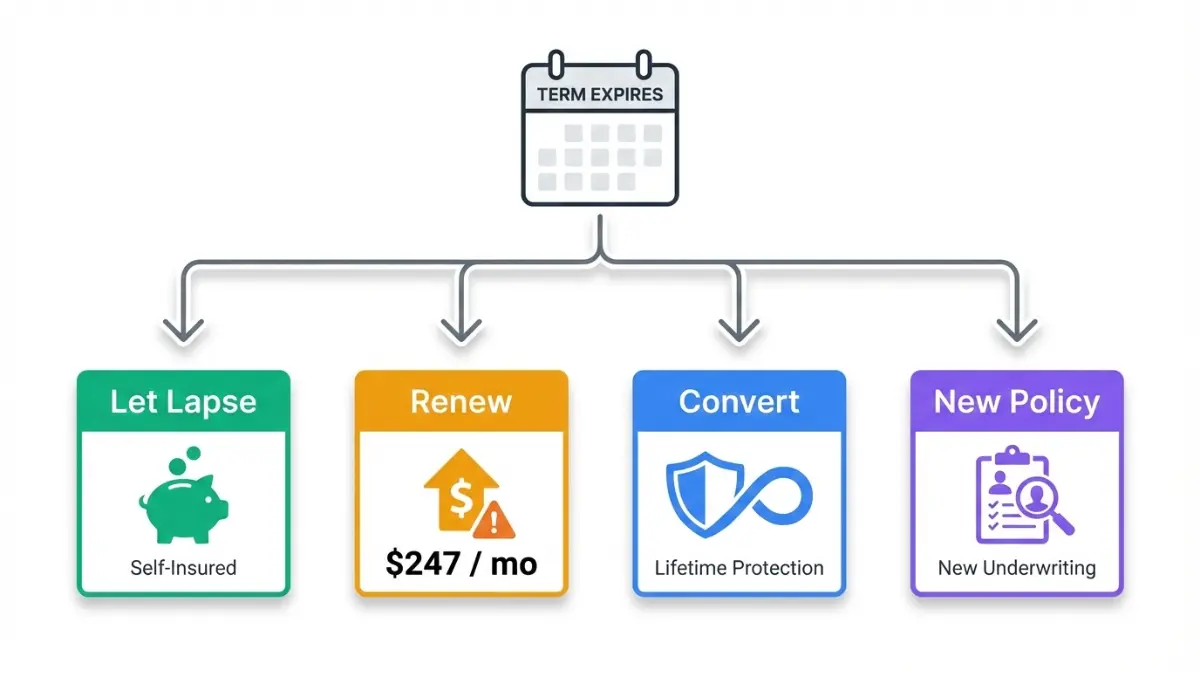

What Happens When Your Term Life Insurance Expires?

Most term life insurance policyholders outlive their coverage period—which is actually the goal. However, understanding your options before expiration prevents costly mistakes and potential coverage gaps.

The 4 Options When Your Term Ends

Option 1: Let the Policy Lapse

Best if: You’ve accumulated sufficient assets, paid off major debts, and children are financially independent.

What happens: Coverage ends. No death benefit. No premium refunds (unless ROP rider). No further obligations.

Financial checkpoint: You should have net assets (retirement accounts, investments, home equity) exceeding $500,000-$1 million to safely self-insure at this stage. Reference our retirement savings guide to verify if you’re adequately funded.

Option 2: Renew Your Existing Term Policy

Best if: You need 1-5 additional coverage years and health has significantly declined.

Cost shock example: $55/month 20-year premium converts to $247/month annual renewable at age 60—a 349% increase.

How renewal pricing works:

- Year 21: Based on age 60 annual renewable rates

- Year 22: Based on age 61 annual renewable rates

- Increases continue annually until age 95 (typical maximum)

When renewal makes sense: Terminal illness diagnosis, major health event making new underwriting impossible, or short-term need (2-3 years) while paying off final debts.

Option 3: Convert to Permanent Life Insurance

Best if: You want lifelong coverage without new medical underwriting.

Conversion mechanics:

- Available typically during years 1-20 of term (check your policy)

- No medical exam or health questions required

- Must convert before term expiration date

- Premiums based on your age at conversion (not original issue age)

Cost comparison—40-year-old converting $500K at age 55:

- Original term premium: $55/month (ending at age 60)

- Conversion to whole life: $385/month (lifetime coverage + cash value)

- New term at age 55: $181/month (if still healthy)

Strategic conversion timing: Years 10-15 of your term provide the sweet spot—you’ve gained a decade of affordable coverage while still having 10-15 years remaining for conversion eligibility.

Case Study: Mark, 52, was diagnosed with Type 2 diabetes during year 18 of his 20-year term. Unable to qualify for new coverage, he converted $300,000 of his $750,000 term to whole life insurance at $290/month—guaranteeing his wife receives at least $300,000 regardless of when he dies. His total cost over years 18-20: $6,960 versus losing all coverage.

Option 4: Apply for New Term Life Insurance

Best if: You’re still in good health and need extended coverage.

Cost reality check: New coverage will cost more due to increased age, but often less than renewal.

Age 60 comparison—$500K coverage, 10-year term:

- Renewing old policy: $247/month (annual renewable)

- New 10-year level term: $168/month (if healthy)

- Annual savings: $948

Application timeline: Start shopping 12-18 months before current policy expires. This allows time for medical exams, underwriting reviews, and policy delivery without gaps.

Term Life vs Whole Life Insurance—2026 Comparison

| Feature | Term Life | Whole Life |

|---|---|---|

| Coverage duration | 10-30 years | Lifetime (to age 121) |

| Monthly cost (40-yr-old, $500K) | $37-$55 | $385-$485 |

| Cash value growth | None | Yes (3-5% annually) |

| Premium changes | Fixed during term | Fixed for life |

| Death benefit | Fixed | Fixed (+ dividends) |

| Best for | Temporary needs, budget-conscious | Estate planning, permanent needs |

| Loans against policy | Not available | Available (at 5-8% interest) |

Financial advisor consensus: For 90% of families, maximum death benefit protection via term life insurance plus investing premium savings into retirement accounts produces superior long-term wealth compared to whole life policies.

According to IRS Publication 559, life insurance death benefits paid to beneficiaries are generally received tax-free, making term life one of the most tax-efficient wealth transfer vehicles available—whether term or permanent coverage.

What This Means For You

Action steps 2-3 years before term expiration:

- Assess remaining coverage needs (outstanding debts, dependent support, final expenses)

- Review current health status (has it improved, declined, or stayed stable?)

- Get new quotes if healthy (compare new term vs renewal costs)

- Evaluate conversion option (review your policy’s conversion period and permanent options)

- Check financial independence milestones (can you self-insure through assets?)

Smart planning prevents the panic of coverage expiration and potential family financial disaster if you die uninsured during the transition period.

How to Choose the Best Term Life Insurance in 2026

Selecting the right term life insurance policy requires evaluating more than just monthly premiums. Five critical factors separate quality coverage from policies that may fail when your family needs them most.

Top 5 Factors for Comparing Providers

1. Financial Strength Ratings

Insurers must remain financially stable for 20-30 years to pay your potential death benefit. Check ratings from multiple independent agencies:

Rating Agency Benchmarks:

- A.M. Best: Minimum A (Excellent) or higher

- Moody’s: Minimum A2 or higher

- S&P Global: Minimum A or higher

- Fitch: Minimum A or higher

Red flag: Any rating below B++ indicates financial instability risk. Your premium savings mean nothing if the insurer becomes insolvent before paying claims.

2. Claims Payment Ratio

The percentage of death claims paid versus contested or denied. Industry average is 98-99% claims paid.

What to research:

- Company’s claims payment history (available via state insurance department)

- Average claim processing time (should be 30-45 days)

- Customer complaints regarding denied claims

3. Conversion Options Quality

Not all conversion features are equal. Evaluate:

- Conversion period: Minimum 15-20 years is ideal

- Available permanent products: Whole life, universal life, or both?

- Conversion age limits: Some insurers restrict conversions after age 65

- Conversion rates: Pre-disclosed or negotiable at conversion?

4. Premium Stability History

Even “guaranteed level term” policies have nuances. Research:

- Has the company ever raised “guaranteed” rates due to actuarial adjustments?

- What percentage of policies reach term end without lapse?

- Are there hidden fees (policy administration, late payment)?

5. Underwriting Flexibility

Accelerated underwriting (no medical exam required):

- Available for coverage up to $500,000-$1,000,000

- Ages 18-60 typically qualify

- Decision in 24-48 hours vs 4-8 weeks

- Slightly higher premiums (5-10%) than fully underwritten

When accelerated underwriting makes sense:

- Excellent health (no medications, normal BMI)

- Need coverage quickly (job change, new mortgage)

- Extreme needle phobia or scheduling difficulties

Application Process: What to Expect

Phase 1: Initial Quote (15 minutes)

Provide basic information (age, health, coverage amount, term length). Receive preliminary premium estimate.

Phase 2: Formal Application (30-45 minutes)

Complete detailed application including:

- Medical history (past 10 years)

- Prescription medications (past 5 years)

- Family health history (parents, siblings)

- Occupation and income verification

- Driving record (DUI/DWI impacts rates)

- Lifestyle questions (tobacco, alcohol, dangerous hobbies)

Phase 3: Medical Exam (30-45 minutes)

Paramedical professional visits your home/office to collect:

- Height, weight, blood pressure

- Blood sample (cholesterol, glucose, liver/kidney function)

- Urine sample (drug screening, protein, nicotine)

- EKG if over age 50 or coverage exceeds $1 million

Exam preparation tips:

- Fast 8-12 hours beforehand (water okay)

- Avoid alcohol 48 hours prior

- Avoid caffeine 4 hours prior

- Get adequate sleep night before

- Postpone strenuous exercise 24 hours

Phase 4: Underwriting Review (2-6 weeks)

Insurer reviews your application, medical exam, and orders additional records:

- Attending Physician Statements (APS) from your doctors

- Prescription history check (MIB Group database)

- Motor vehicle record check

- Credit-based insurance score (in most states)

Phase 5: Decision & Policy Delivery (1-2 weeks)

You receive:

- Approved as applied: Policy issued at quoted premium

- Approved with rating: Higher premium due to health findings

- Postponed: Additional information/tests required

- Declined: Coverage denied (health risks too high)

According to guidance from the National Association of Insurance Commissioners, shopping with at least 3-5 insurers is essential because underwriting criteria vary significantly—one company’s “standard” rating might be another’s “preferred plus.”

Red Flags to Avoid

❌ High-pressure sales tactics (“This rate expires today!”)

❌ Unrealistic promises (“No medical questions, guaranteed approval, $1M coverage!”)

❌ Unclear premium structure (Unable to provide guaranteed rate table)

❌ Excessive policy loans advertised (Suggests whole life being misrepresented as term)

❌ No independent ratings (Company refuses to disclose financial strength grades)

What This Means For You

Action steps for securing best coverage:

- Get 3-5 quotes minimum — Rates vary 30-50% between identical coverage

- Compare total premiums — Calculate (monthly premium × 12 × term length)

- Verify insurer ratings — Check A.M. Best, Moody’s, S&P for A or higher

- Read conversion provisions — Understand exactly what permanent products are available

- Bundle with existing policies — Some insurers offer 5-10% discounts for multiple policies

Use our comprehensive tools suite to model how life insurance premiums fit within your overall monthly budget planning strategy.

Frequently Asked Questions

1. Can I get term life insurance without a medical exam?

Yes. Many insurers offer accelerated underwriting for coverage up to $500K-$1M if you’re ages 18-60 and in good health. Approval happens in 24-48 hours versus 4-8 weeks. Premiums cost 5-10% more than fully underwritten policies.

2. Does term life insurance have cash value?

No. Term life insurance provides pure death benefit protection without any cash accumulation or investment component. This keeps premiums 70-90% lower than permanent policies with cash value.

3. How long should my term life insurance policy be?

Choose a term matching your longest financial obligation. 20-year term: Typical for mortgages and raising young children. 30-year term: Covers children from birth through college graduation. 10-15 year term: Pre-retirement debt protection or income replacement for older workers.

4. Can I cancel my term life insurance anytime?

Yes. Term life insurance has no cancellation penalties or surrender charges. Simply stop paying premiums and coverage ends. You receive no refund of past premiums unless you have a return-of-premium rider.

5. Is term life insurance tax-deductible?

No. Personal term life insurance premiums are not tax-deductible. However, death benefits paid to beneficiaries are generally received completely tax-free according to IRS regulations.

6. What’s the difference between term and permanent life insurance?

Term: Temporary coverage (10-30 years), no cash value, affordable premiums, expires at term end. Permanent: Lifetime coverage, builds cash value, 5-10x higher premiums, never expires if premiums paid.

7. Can I have multiple term life insurance policies?

Yes. Many people maintain multiple policies—employer group coverage plus individual term, or multiple individual policies purchased at different life stages. Total coverage across all policies combined should match your comprehensive needs analysis.

8. Does my employer term life insurance cover me after I leave?

Rarely. Employer group term life typically ends when employment terminates. Some policies offer conversion to individual coverage (at much higher cost) within 30 days. Critical: Never rely solely on employer coverage—maintain individual policy for portability.

9. What happens if I miss a premium payment?

Most policies include a 31-day grace period. If payment received within 31 days, coverage continues uninterrupted. After 31 days, policy lapses (terminates). Some insurers offer reinstatement within 2-5 years if you reapply and pass medical underwriting.

10. Can I convert term life to whole life insurance?

Yes, if your policy includes a conversion rider (most do). You can convert all or part of your term coverage to permanent insurance without medical exam, typically during the first 10-20 years. This is valuable if health deteriorates.

11. How quickly does term life insurance coverage start?

Coverage begins on your policy effective date—typically 1-2 days after your first premium payment clears and you’re approved. Some accelerated underwriting programs offer same-day or next-day coverage for healthy applicants.

Disclaimer

This article is for educational and informational purposes only and does not constitute financial, legal, or insurance advice. Term life insurance needs, coverage amounts, premium rates, and policy features vary significantly based on individual circumstances including age, health status, location, insurer, and selected policy options.

All rates, examples, and calculations presented are based on 2026 industry averages and may not reflect actual quotes you receive. Policy features, conversion options, riders, and availability vary by insurance company and state regulations.

Before purchasing term life insurance or making any coverage decisions, consult with licensed insurance professionals, certified financial planners, and legal advisors who can evaluate your specific situation and recommend appropriate solutions. Premium quotes are subject to underwriting approval and may differ from initial estimates based on medical exam results and application review.

The information provided does not guarantee coverage approval, specific premium rates, or claim payment. Always read your complete policy documents, understand all terms and conditions, and verify insurer financial strength ratings through independent rating agencies before finalizing any purchase.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.