What Heirs Must Know About Inheriting Structured Settlements

Inheriting a structured settlement means IRC §104 tax rules, a 30-day claim window, and up to 18% factoring fees. Here’s what heirs actually need.

In This Article

Can you inherit a structured settlement? Here’s what the law actually says

Yes — you can inherit a structured settlement in most cases, but whether payments arrive automatically or require a court process depends on one document: the original annuity contract.

Two legal pathways govern this transfer, and which one applies to you determines everything about speed, taxes, and your rights.

Why the answer depends on how the original settlement was structured

The first pathway applies when the original recipient named a beneficiary on the annuity contract — payments or a death benefit can transfer directly, often without probate.

The second pathway applies when no beneficiary was designated: the settlement enters the estate and requires probate court authorization before any heir receives a dollar.

The two legal pathways that determine an heir’s rights

A named beneficiary holds a contractual right to whatever the annuity specifies — remaining periodic payments, a lump-sum death benefit, or both — and that right takes effect without any separate legal filing.

An heir taking through the estate holds the same ultimate right, but the process adds 90 to 180 days before the first payment is authorized.

Understanding how structured settlements pay and what they actually cost provides the foundational context every heir needs before taking any next step.

ℹ️ Disclaimer: The structured settlement inheritance information in this article is for educational purposes only. Tax treatment under IRC Section 104 varies by settlement classification, payment component type, and individual circumstances as of 2026. Structured settlement factoring transactions require court approval under applicable state Structured Settlement Protection Acts — court approval does not guarantee a transaction is in a beneficiary’s financial interest. Consult a licensed CPA or tax attorney before reporting inherited payments on any return, and a CFA-credentialed financial advisor or licensed estate attorney before signing any factoring or transfer agreement.

What happens to a structured settlement when the owner dies

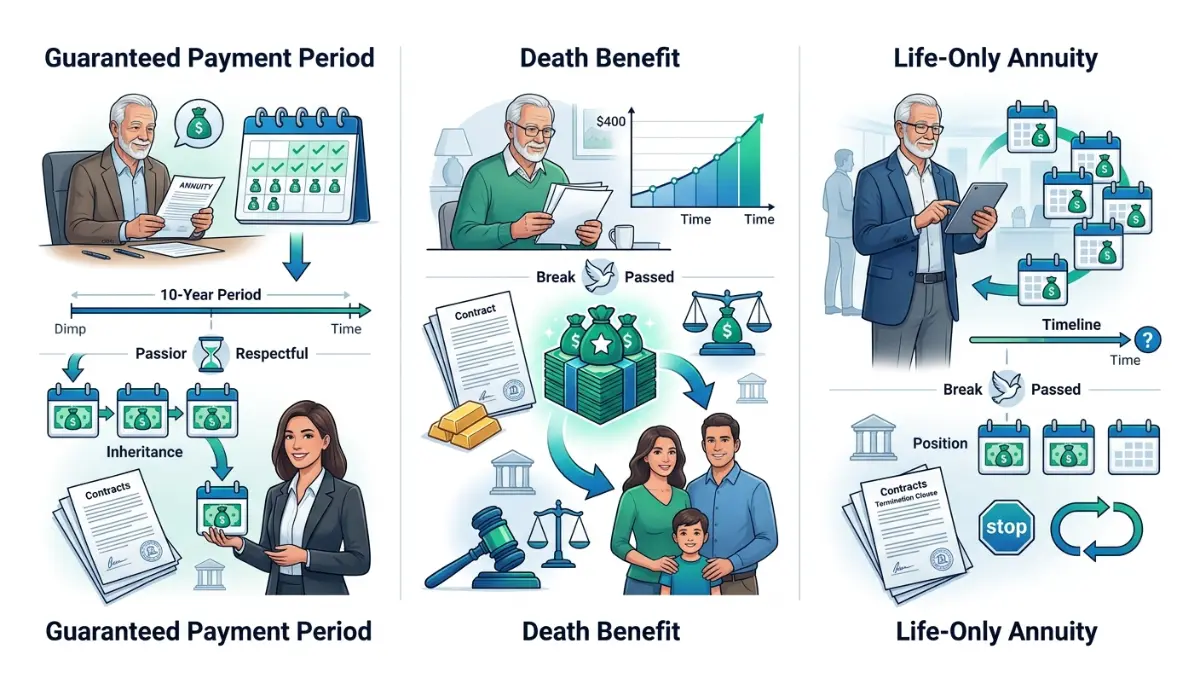

Whether structured settlement payments survive the original recipient’s death depends entirely on which of three annuity contract types was used — and most heirs don’t discover the answer until they contact the issuer.

Each type produces a completely different outcome.

How the annuity contract determines whether payments survive

A guaranteed payment period annuity — the most common U.S. structure as of 2026 — continues payments to a named beneficiary for the remaining guaranteed term, typically 10 to 20 years from the original settlement date.

The annuity issuer, the insurance carrier holding the contract, is contractually obligated to continue those payments for the full term regardless of when the original recipient died.

What a structured settlement death benefit actually covers — and what it doesn’t

A death benefit in a structured settlement context is a separately negotiated lump sum payable at the recipient’s death — it is not a standard provision and must have been specifically included when the original settlement was structured.

The annuity issuer can confirm within 5 to 10 business days whether a death benefit exists, its exact amount, and the designated recipient.

When payments stop entirely: the life-only annuity problem

A life-only annuity provides payments exclusively for the original recipient’s lifetime — at death, all future payments stop, and no heir receives anything regardless of what a will states.

Because reading these contract documents correctly requires familiarity with annuity mechanics, reviewing how annuity contracts function as financial instruments is the right first step before contacting the issuer.

💡 Expert Note (CFA): A will has zero legal authority over an annuity contract’s beneficiary designation — I have watched this conflict unfold in estates where the will named one person and the annuity contract named another. The contract governs entirely. Courts uphold this without exception, and no executor can override it.

How to claim inherited structured settlement payments: a step-by-step guide

Claiming inherited structured settlement payments requires four sequential steps — and the single most costly mistake heirs make is missing the 30-day window for notifying the annuity issuer that begins at the date of death.

That window is a contractual timeline, not a guideline — missing it adds 60 to 90 days to the authorization process.

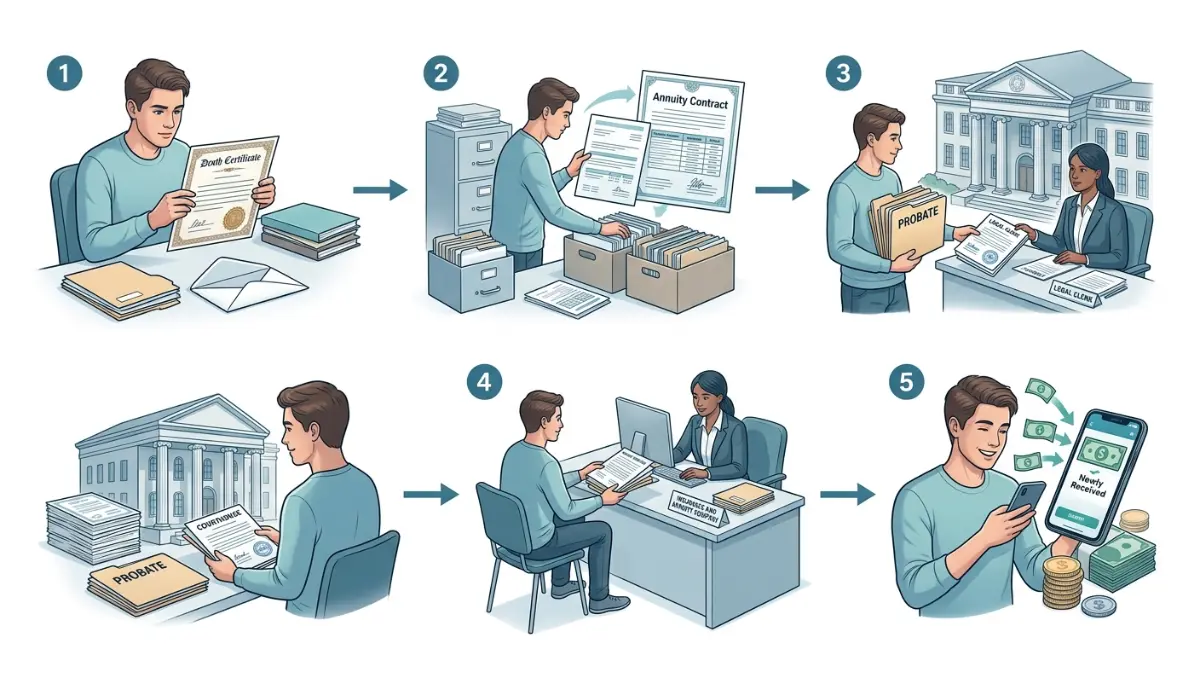

Step 1–2: Locate the settlement agreement and notify the annuity issuer

Step 1 is locating the original settlement agreement and annuity contract — both documents identify the issuing carrier, confirm the payment schedule, and name the designated beneficiary or absence of one.

Step 2 is notifying the annuity issuer in writing within 30 days of death, submitting a certified death certificate and proof of your status as the named beneficiary or authorized estate representative.

Step 3–4: Navigate probate and establish payment authorization

Step 3 applies when no beneficiary is named: file a probate petition with the appropriate state court to establish the estate’s legal claim over the settlement’s remaining payment value.

Step 4 is receiving the issuer’s formal payment authorization — typically 30 to 60 days after a beneficiary claim, or 90 to 180 days when the payment stream must pass through probate court.

How long the process takes — and what causes delays

A named beneficiary with complete documentation can expect the first payment within 30 to 60 days of contacting the issuer.

Delays beyond that trace to three causes: a missing or outdated beneficiary designation, multiple heirs disputing distribution rights, or a life-only contract with no survivor provision.

💡 Expert Note (CFA): The most preventable delay I see in estate advisory work is failure to notify the annuity issuer within 30 days of the recipient’s death. That procedural gap routinely pushes payment authorization back 60 to 90 days — a real financial cost for heirs depending on that income stream. Request the annuity contract within 48 hours of death. It contains everything needed to start the clock.

✅ Pro Tip: The original settlement agreement is the single most important document in this process. Contact the deceased’s attorney, financial advisor, or bank safe deposit box within 48 hours — it contains the issuer’s name, full payment schedule, and current beneficiary designation in one place.

Are inherited structured settlement payments taxable? The 2026 IRS rules

IRC Section 104(a)(2) excludes from gross income compensation received for physical personal injuries — but this exclusion covers specific payment components only, and heirs who treat all inherited structured settlement income as tax-free risk IRS adjustments with penalty and interest.

The boundary of the exclusion is one of the most consistently misstated facts in personal finance coverage of this topic.

How IRC Section 104 applies — and where it stops applying — for heirs

The physical injury compensation component of a structured settlement payment retains its excludable character when transferred to an heir — the underlying classification does not change at death under 2026 IRS guidance.

Any interest or earnings accrued on the annuity beyond the original injury compensation, however, are taxable to the heir as ordinary income in the year each payment is received.

📊 Data Point: IRS Publication 525 (2026 edition) confirms that compensation for physical personal injuries is excluded from gross income under §104(a)(2), but accrued interest on structured settlement annuities does not qualify for the same exclusion and must be reported as ordinary income by recipients — including heirs. — Source: Internal Revenue Service, Publication 525, January 2026.

For the full statutory framework governing settlement income classification, IRS Publication 525’s guidance on taxable and nontaxable settlement proceeds is the primary 2026 reference every heir should review with a qualified tax professional. For the IRS’s direct Q&A on exclusion boundaries and settlement income characterization, the IRS settlement income guidance page provides additional clarification on edge cases.

A full breakdown of when structured settlement payments are taxable under current IRS rules — including 2026 thresholds and component-by-component analysis — is available in our dedicated tax guide for settlement recipients and heirs.

The interest component exception: what heirs must report as income

Any punitive damages component in the original settlement was taxable to the original recipient and remains taxable to heirs — it does not become excludable because it passed through an estate.

Identifying which portion of each payment is excludable requires the original settlement documents showing how the payment stream was categorized at the time of the court order approving the original settlement.

State income taxes and inherited structured settlement payments

Approximately 12 states, including California, New York, and New Jersey, impose state income tax on inherited annuity payments even when the federal component is fully excludable under §104.

State and federal treatment do not automatically align, and heirs in high-income-tax states must model both layers before assuming any net tax position.

⚠️ Warning: Treating the full inherited payment stream as tax-free without confirming each component’s classification is one of the most common and most expensive errors heirs make on their federal returns. IRS adjustments on misclassified settlement income carry back-assessed penalties and interest to the original filing date — sometimes years after the payments began.

An income tax calculator provides a preliminary estimate of federal tax liability on the ordinary income components before filing. For scenarios where a factoring buyout could change the tax character of the amount received, a capital gains tax calculator supports additional modeling.

Can you sell or convert inherited structured settlement payments — and should you?

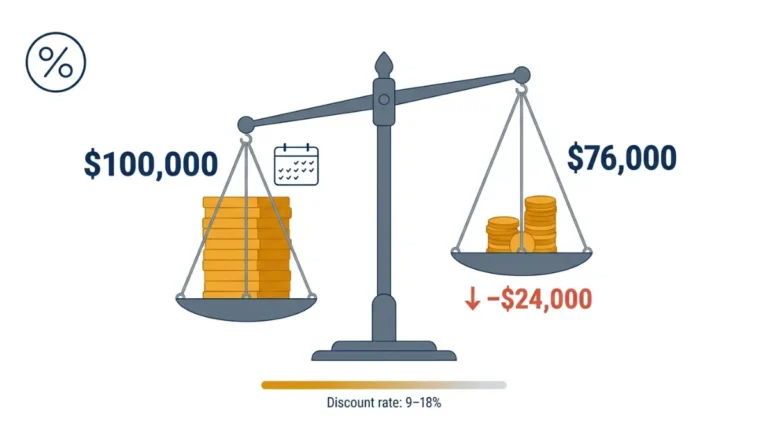

Structured settlement factoring — selling future payment rights to a company in exchange for an immediate lump sum — is legally available to heirs in all 50 states, but the 2026 secondary market applies a discount rate of 9% to 18% that most factoring company marketing does not state clearly at the outset.

Every factoring transaction also requires court approval — and that approval is a genuine judicial review, not a procedural rubber stamp.

How the court-approval requirement protects heirs in all 50 states

Every U.S. state’s Structured Settlement Protection Act requires a judge to find that the sale of structured settlement payment rights serves the heir’s “best interest” before any transfer becomes legally valid.

Courts in California, Florida, and New York rejected factoring applications in 2025 and 2026 specifically because discount rates were found to be financially harmful to the sellers — demonstrating that court review carries real consequence.

The 2026 secondary market discount rate range — and what it costs you

Factoring companies apply a discount rate to the present value of your future payment stream — the higher the rate, the less you receive for the same stream of future income.

At a 12% discount rate applied to a payment stream with a present value of $200,000, a factoring company pays approximately $176,000 — a permanent $24,000 reduction in lifetime income that no court order can reverse after the transaction closes.

📊 Data Point: The 2026 structured settlement secondary market discount rate ranges from 9% to 18%, with higher rates applied to shorter remaining payment durations and lower-rated annuity issuers. Any offer exceeding 15% on a stream with more than 10 years remaining is below the current market benchmark. — Source: Secondary market structured settlement transaction analysis, 2026.

Understanding how structured settlement discount rates are calculated and what drives factoring company pricing is essential reading before contacting any factoring company. For a full breakdown of what selling structured settlement payments actually costs in real dollar terms across multiple scenarios, our dedicated cost analysis includes 2026 figures.

The investment calculator lets you model the present value of your full inherited payment stream alongside the lump sum a factoring company offers. For the time value component of that comparison, the compound interest calculator shows how a reinvested lump sum grows against the value of continued periodic payments over time.

A three-question decision framework: when keeping payments wins

Before contacting any factoring company, three questions determine whether a sale makes financial sense: Does a genuine, immediate liquidity need exist that cannot be addressed any other way? Have you received competing bids from at least three factoring companies? Has an independent financial advisor confirmed the offered discount rate falls within the current 9% to 18% market range?

If the answer to any of the three is no, keeping the payments is almost always the stronger financial position.

⚠️ Warning: A discount rate above 15% on a payment stream with more than 10 years remaining is a below-market offer. Do not sign any factoring agreement without independent review, at least two competing bids, and legal counsel familiar with your state’s Structured Settlement Protection Act.

The analytical framework behind the lump sum vs. structured settlement decision — including how each option performs against different financial positions — is covered in detail in our dedicated comparison guide. Before selecting any factoring company, comparing rated structured settlement factoring companies against 2026 discount rate benchmarks is a mandatory due diligence step.

The CFPB’s consumer guidance on structured settlement transfers covers your rights as a seller and what the court approval process entails — required reading before any agreement is signed.

Legal protections and state laws every structured settlement heir must know

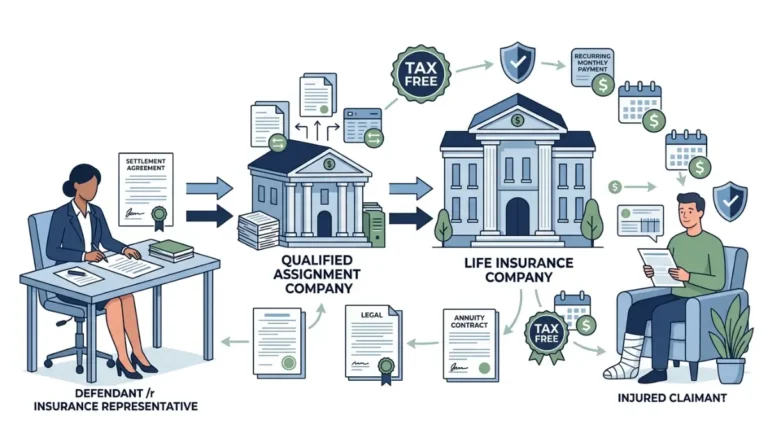

Anti-assignment provisions embedded in virtually every structured settlement agreement prevent the original recipient — and by extension their heirs — from voluntarily transferring payment rights without formal court oversight.

These provisions exist by federal design: the qualified assignment framework under IRC Section 130 was built to prevent structured settlements from being liquidated outside a supervised legal process, and that protection survives the settlor’s death.

The Structured Settlement Protection Act: what “court approval” actually means

All 50 states enacted Structured Settlement Protection Acts between 1997 and 2002, with amendments through 2025–2026 strengthening the “best interest” judicial standard for evaluating transfer requests.

The court review examines the heir’s financial circumstances, the fairness of the discount rate, and whether the heir received independent professional advice before signing — none of this is automatic or guaranteed to result in approval.

For a complete breakdown of what the court approval process requires and how judges actually evaluate factoring petitions, including state-specific filing requirements, our dedicated guide covers the full legal framework.

For regulatory context on the annuity carriers that back these payment obligations, the SEC’s investor guidance on annuity-backed financial instruments covers the oversight framework governing structured settlement issuers.

Anti-assignment provisions and why heirs cannot unilaterally transfer payments

An anti-assignment clause survives the settlor’s death and cannot be overridden by a will, an executor’s instruction, or any court order outside the SSPA factoring process.

Any informal agreement to redirect payment rights to a third party outside that process is legally void under both the original settlement agreement and applicable state statute.

| SSPA Requirement | What It Means for Heirs |

|---|---|

| Court petition required | Factoring company or heir files with the appropriate state court before any transfer |

| “Best interest” judicial finding mandatory | Judge evaluates financial impact; unfavorable discount rates have been grounds for rejection |

| Mandatory waiting period | Minimum 10-day review window between filing and court order in most states |

| Independent advice requirement | California, New York, and Florida require attorney attestation before approval is granted |

Source: State Structured Settlement Protection Acts, 2026 compliance standards.

Your next steps as a structured settlement heir

You now have the complete picture: inherit a structured settlement through the correct legal pathway, claim payments before the 30-day notification window closes, know exactly which components are taxable under 2026 IRS rules, and benchmark any factoring offer against the 9% to 18% secondary market range before signing anything.

Three questions determine your first move.

Three questions to answer before you make any decision

Do you have the original settlement agreement and annuity contract? Do you know which of the three contract types applies to your situation? Have you confirmed the §104 classification of each payment component with a licensed CPA?

If any answer is no, those are your first three tasks — in that order.

When to call a CFA, when to call an estate attorney, and when to call a CPA

Financial questions — whether to sell, how to evaluate a lump sum, what the payment stream is worth — go to a CFA-credentialed financial advisor.

Legal questions — probate, beneficiary disputes, contract interpretation, SSPA compliance — go to a licensed estate attorney.

Tax questions — which components are excludable, how to report inherited payments, how a factoring transaction is classified — go to a licensed CPA.

Getting the right professional for the right question is what separates informed decisions from irreversible ones.

Frequently asked questions about inheriting a structured settlement

1. Can you inherit a structured settlement?

Yes — inheriting a structured settlement is possible through two pathways. If the original recipient named you on the annuity contract, payments transfer directly, often without probate. If no beneficiary was named, the settlement passes through the estate and requires probate court authorization. Consult a licensed financial professional to confirm which pathway applies to your specific situation.

2. What happens to structured settlement payments when the recipient dies?

It depends entirely on the annuity contract type. A guaranteed payment period annuity continues payments to a named beneficiary for the remaining term. A life-only annuity stops at death with no heir payments. A separately negotiated death benefit provision pays a lump sum. Review the original annuity contract with an estate attorney to confirm which structure applies.

3. Are inherited structured settlement payments taxable?

The physical injury compensation component is generally excluded from gross income under IRC Section 104(a)(2). Accrued interest or earnings beyond the injury compensation are taxable as ordinary income to the heir. Punitive damages components are taxable regardless of how the estate transfer was characterized. Consult a licensed CPA before reporting any inherited structured settlement payments on a federal or state return.

4. Can heirs sell inherited structured settlement payments?

Yes — heirs can sell inherited structured settlement payments to a factoring company, but every U.S. state requires court approval under the applicable Structured Settlement Protection Act before any transfer is legally valid. The 2026 secondary market discount rate ranges from 9% to 18% of the payment stream’s present value. Consult a licensed financial advisor before agreeing to any factoring terms.

5. How do I claim structured settlement payments as a beneficiary?

Four steps are required: (1) locate the original settlement agreement and annuity contract; (2) notify the annuity issuer in writing within 30 days of death with a certified death certificate; (3) file a beneficiary claim form or initiate probate if no beneficiary is named; (4) await formal payment authorization, typically 30 to 90 days. An estate attorney can reduce processing delays significantly.

6. Can a structured settlement be transferred to a family member during the original owner’s lifetime?

No — anti-assignment provisions in the original settlement agreement prevent voluntary transfer during the owner’s lifetime. The only legally valid exception is a structured settlement factoring transaction, which requires court approval under the applicable state Structured Settlement Protection Act. Any informal agreement to redirect payments outside this process is void under both contract law and state statute. Consult an estate attorney.

7. Do structured settlements have a death benefit?

Not automatically. A structured settlement death benefit — a lump sum payable to a named beneficiary at the recipient’s death — must have been specifically negotiated when the original settlement was structured and documented in the annuity contract. Life-only annuities provide no death benefit or survivor payments. Contact the annuity issuer directly with a death certificate to confirm whether a death benefit provision exists.

8. What is a structured settlement annuity beneficiary?

A structured settlement annuity beneficiary is the person named in the annuity contract to receive remaining payments or a death benefit when the original recipient dies. This designation supersedes any contrary instruction in a will and can be updated directly with the annuity issuer during the recipient’s lifetime. Verify the current designation with the issuer’s beneficiary services department. Consult a licensed financial professional if the designation needs review.

9. How long does it take to receive inherited structured settlement payments?

A named beneficiary with complete documentation typically receives payment authorization within 30 to 60 days of notifying the annuity issuer. When probate is required because no beneficiary was named, the timeline extends to 90 to 180 days depending on state court dockets and estate complexity. An estate attorney familiar with annuity contracts can identify and resolve documentation gaps that most commonly extend this timeline.

10. Can I get a lump sum from an inherited structured settlement?

Yes, through a structured settlement factoring company. The company purchases your future payment rights and issues a lump sum, applying a 2026 secondary market discount rate of 9% to 18% of the payment stream’s present value. Court approval is required in all 50 states under the applicable Structured Settlement Protection Act. Consult a licensed financial advisor before agreeing to any factoring discount rate or contract terms.

11. What legal steps does an heir need to take to receive payments?

Five steps are required: (1) obtain a certified death certificate; (2) locate the original settlement agreement and annuity contract; (3) notify the annuity issuer in writing; (4) file a beneficiary claim form or a probate petition if no beneficiary is named; (5) receive issuer or court authorization. Timelines range from 30 to 180 days depending on contract type and estate complexity. Consult an estate attorney for state-specific requirements.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.