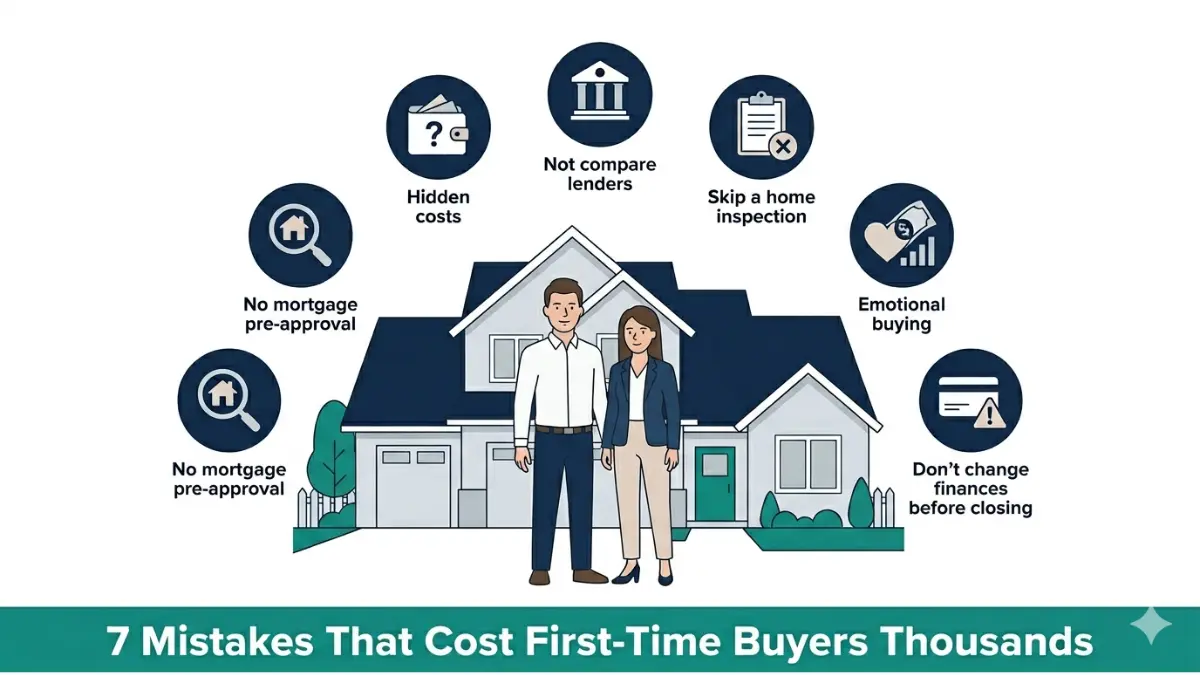

7 Biggest Mistakes First-Time Home Buyers Make (And How to Avoid Them)

First-time home buyers lose thousands from 7 completely avoidable mistakes. Get the 2026 expert breakdown, real cost data, loan comparison tables, and a readiness checklist.

In This Article

Most first-time home buyers lose $10,000–$30,000 through completely avoidable mistakes — before they unpack a single box. In 2026, with home prices near historic highs and first-time buyers at their lowest share of the market in decades, getting this right isn’t optional. Here are the 7 biggest mistakes and exactly how to avoid each one.

Why Most First-Time Home Buyers Lose Thousands Before They Even Move In

Buying your first home is the largest financial decision of your life. Yet most first-time buyers walk into it underprepared — and the market punishes that instantly.

According to the National Association of Realtors, first-time buyers now account for just 24% of all home purchases — the lowest level ever recorded. Rising prices, tighter credit, and fierce competition have compressed the margin for error to almost zero.

What the data tells us:

- The median U.S. home price in 2026 exceeds $420,000

- A 2025 Bankrate study found hidden homeownership costs average $21,409 per year beyond the mortgage

- Buyers who skip even one critical step risk loan denial, overpayment, or costly post-purchase repairs

This article exposes every major trap — and gives you the exact fix for each one. Use our Home Affordability Calculator before you read further to anchor your real buying power.

The 7 Biggest Mistakes First-Time Home Buyers Make in 2026

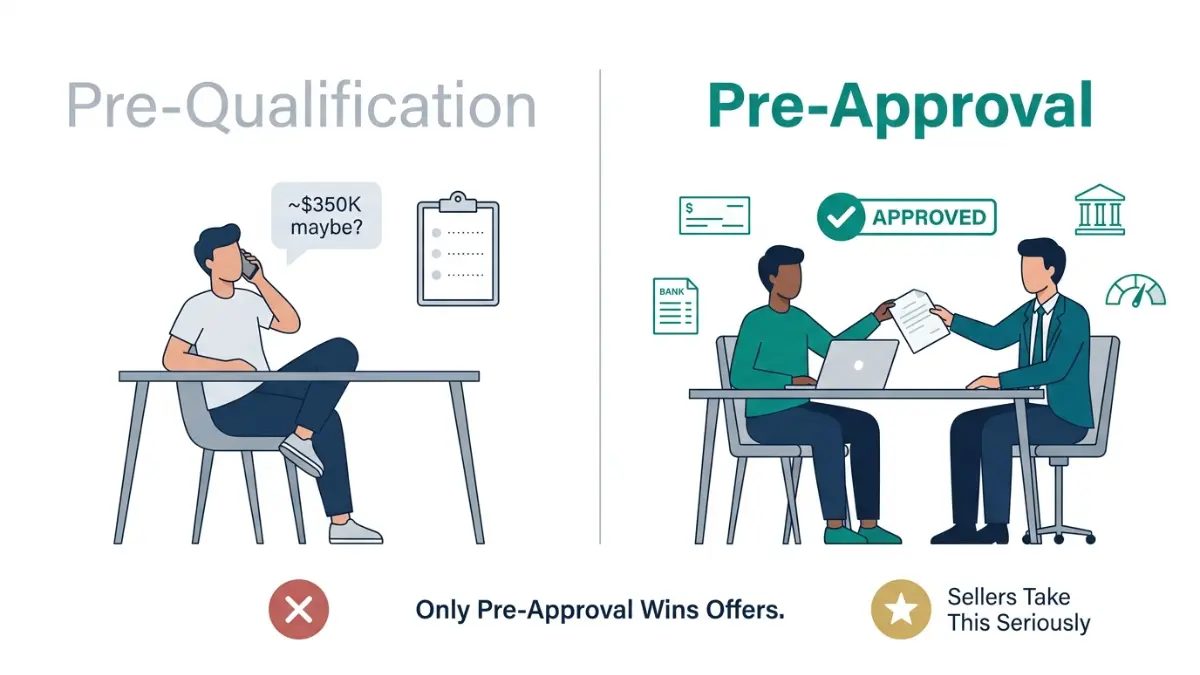

Mistake #1: House Hunting Before Getting Mortgage Pre-Approval

What It Costs You: Lost offers in competitive markets. Many sellers outright reject non-pre-approved buyers.

Too many first-time home buyers start browsing Zillow and Redfin before ever speaking to a lender. It feels exciting — but it’s a critical mistake. Pre-approval tells you exactly what you can borrow, signals seriousness to sellers, and can lock in your interest rate.

Pre-Qualification ≠ Pre-Approval. This distinction costs buyers thousands:

| Pre-Qualification | Pre-Approval | |

|---|---|---|

| Credit Check | No | Yes (hard pull) |

| Income Verified | No | Yes |

| Seller Confidence | Low | High |

| Rate Lock Available | No | Yes |

The Fix:

- Get pre-approved before your first showing — not after

- Submit applications to 3+ lenders within a 45-day window (multiple hard inquiries in this window count as one under FICO rules)

- Use our Mortgage Calculator to estimate monthly payments before you apply

For a full walkthrough, read our Mortgage Pre-Approval 2026 Guide.

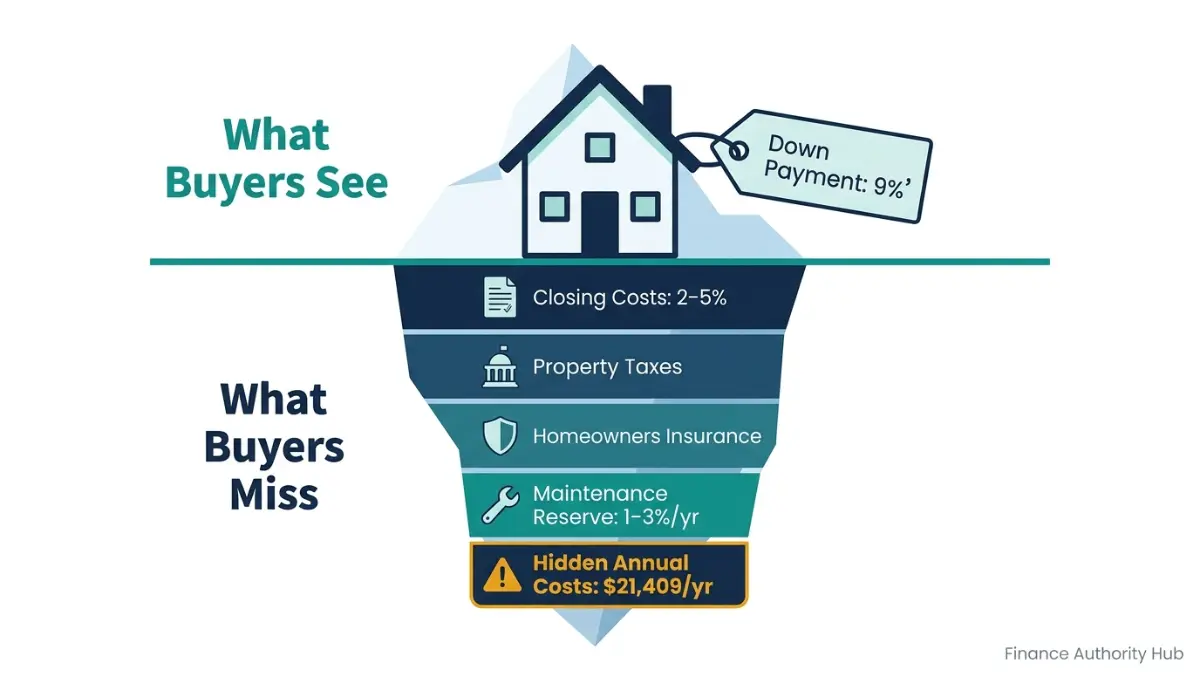

Mistake #2: Budgeting Only for the Down Payment

What It Costs You: Financial shock at closing — and for years after.

Most first-time home buyers fixate on the down payment and forget the full financial picture. The mortgage is just one piece. Here’s the complete all-in cost breakdown every first-time buyer needs to see:

| Cost Category | Typical Amount |

|---|---|

| Down Payment (median 2024, per NAR) | 9% of purchase price |

| Closing Costs | 2–5% of loan amount |

| Moving Expenses | $1,000–$5,000 |

| Home Inspection Fee | $300–$600 |

| Annual Hidden Costs (Bankrate 2025) | $21,409/year |

| Maintenance Reserve (recommended) | 1–3% of home value/year |

On a $400,000 home, that’s up to $20,000 in upfront costs beyond your down payment — plus $21,000+ annually.

The Fix:

- Budget for all-in costs, not just the down payment

- Read our detailed breakdown of Home Loan Closing Costs 2026 before you close

- Set aside a maintenance reserve of 1–3% of your home’s value each year from day one

Mistake #3: Going With the First Lender You Find

What It Costs You: $1,500–$3,000+ over the life of the loan, per Consumer Financial Protection Bureau research.

Many first-time home buyers accept the first mortgage offer they receive — often from their personal bank. This is one of the most expensive mistakes in the home buying process.

Even a 0.25% difference in interest rate on a $350,000 loan saves over $17,000 in total interest on a 30-year mortgage.

The Fix:

- Get quotes from at least 3 lenders: a national bank, a credit union, and an online lender

- Compare APR — not just the interest rate. Our APR vs Interest Rate guide explains the difference

- Review loan estimates side-by-side. The CFPB’s mortgage comparison tool makes this straightforward

Mistake #4: Skipping the Home Inspection to Win a Bidding War

What It Costs You: $5,000–$50,000+ in unexpected repairs after closing.

In hot markets, some buyers waive the home inspection to make their offer more competitive. Real estate professionals consistently flag this as the single highest-risk decision a first-time buyer can make.

The American Society of Home Inspectors (ASHI) reports that 86% of inspected homes have at least one defect identified during the process. Common findings include:

- Faulty electrical panels or wiring

- Roof damage requiring full replacement ($8,000–$25,000)

- Plumbing leaks and water damage

- Foundation cracks or settling

- HVAC systems near end of life

The Fix:

- Never waive the inspection outright — instead, offer a “as-is” inspection for informational purposes only to reassure sellers while protecting yourself

- If the seller refuses any inspection, treat that as a serious red flag

- Budget inspection costs ($300–$600) as a non-negotiable line item

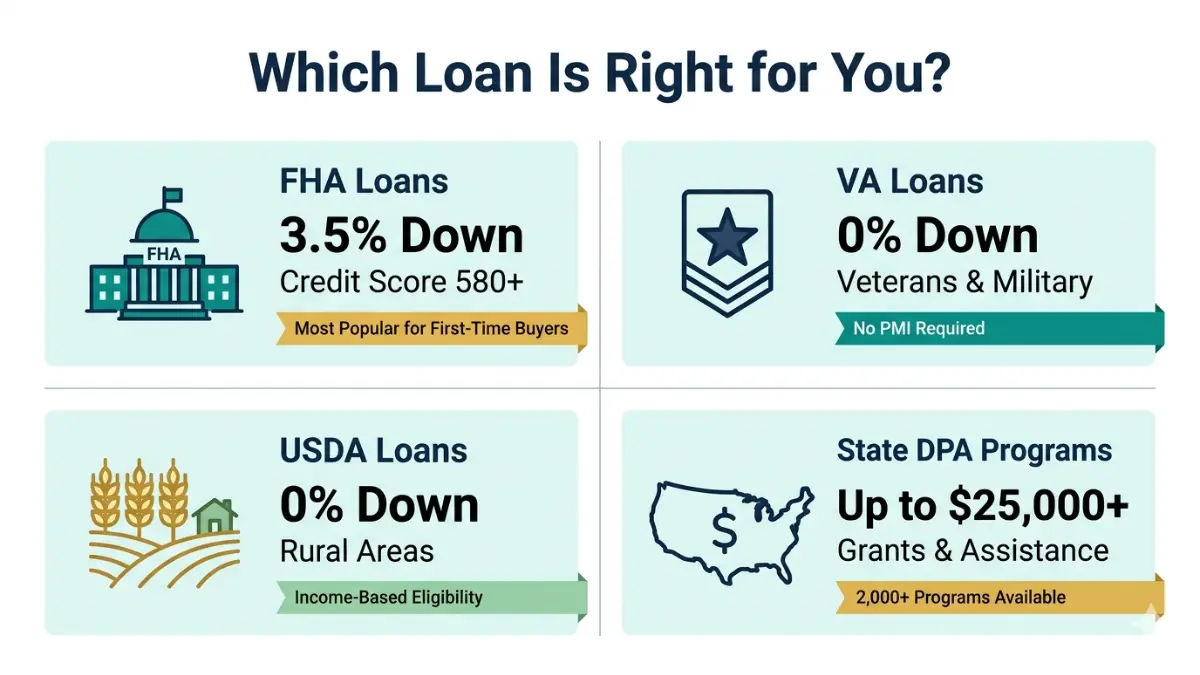

Mistake #5: Not Knowing About Down Payment Assistance Programs

What It Costs You: Up to $25,000+ in free money left unclaimed.

This is the gap that shocks most first-time buyers: over 2,000 federal, state, and local down payment assistance programs exist in the U.S. — and most buyers never check if they qualify.

Here’s the loan landscape every first-time buyer needs to understand:

| Loan Type | Min. Down Payment | Who Qualifies | Key Benefit |

|---|---|---|---|

| FHA Loan | 3.5% | Credit score 580+ | Low barrier to entry |

| VA Loan | 0% | Veterans & military | No PMI required |

| USDA Loan | 0% | Rural areas, income limits | Zero down in eligible zones |

| Conventional (3%) | 3% | Credit score 620+ | Avoid upfront MIP |

| State DPA Programs | Varies | Income & location-based | Grants up to $25,000+ |

The Fix:

- Visit HUD’s official homebuyer resource page to find programs in your state

- Review FHA loan options at HUD’s FHA loan center

- Read our complete Down Payment Help Guide 2026 — it covers 8 assistance programs in detail

Mistake #6: Letting Emotions Override Financial Logic

What It Costs You: Overpaying, buying in the wrong location, or ignoring deal-breaking defects.

Buying a first home is deeply emotional — and that emotion is exactly what makes buyers vulnerable. First-time buyers often fall in love with aesthetics (countertops, paint colors, staging) and ignore structural realities and neighborhood fundamentals.

The 85% Rule — used by experienced buyers — states: if a home meets 85% of your must-have criteria, submit an offer. No home is 100% perfect, and chasing perfection costs opportunities.

Your Head + Heart Checklist:

- ✅ Does the location meet your 5-year lifestyle plan?

- ✅ Is the price justified by comps in the neighborhood?

- ✅ Can you handle the total monthly cost comfortably? (Use our Mortgage Calculator to confirm)

The Fix:

- Research neighborhood fundamentals: school ratings, commute times, crime data, future development plans

- Separate cosmetic issues (fixable) from structural issues (expensive)

- Check your Debt-to-Income Ratio before emotionally committing — lenders cap DTI at 43–50% for most loan types

Mistake #7: Making Major Financial Changes Before Closing

What It Costs You: Loan denial — even after your offer is accepted.

This mistake destroys deals at the finish line. Between pre-approval and closing day, lenders re-verify your financial profile. Any significant change can trigger a denial or delay.

The 60-Day Pre-Close Financial Freeze Rule (most competitors never explain this clearly):

- ❌ No new credit cards or loans — even a store card the week before closing

- ❌ No large undocumented deposits — lenders will question the source

- ❌ No job changes — especially switching from salaried to self-employed

- ❌ No large purchases — a new car can raise your DTI above approval thresholds

- ❌ No co-signing for anyone else’s loan during this period

The Fix:

- Treat the 60 days before your application — and the 30 days after pre-approval — as a financial lockdown period

- Pay all bills on time; even one late payment can lower your score at the worst moment

- Learn what lenders actually check in our Credit Score to Buy a House 2026 guide

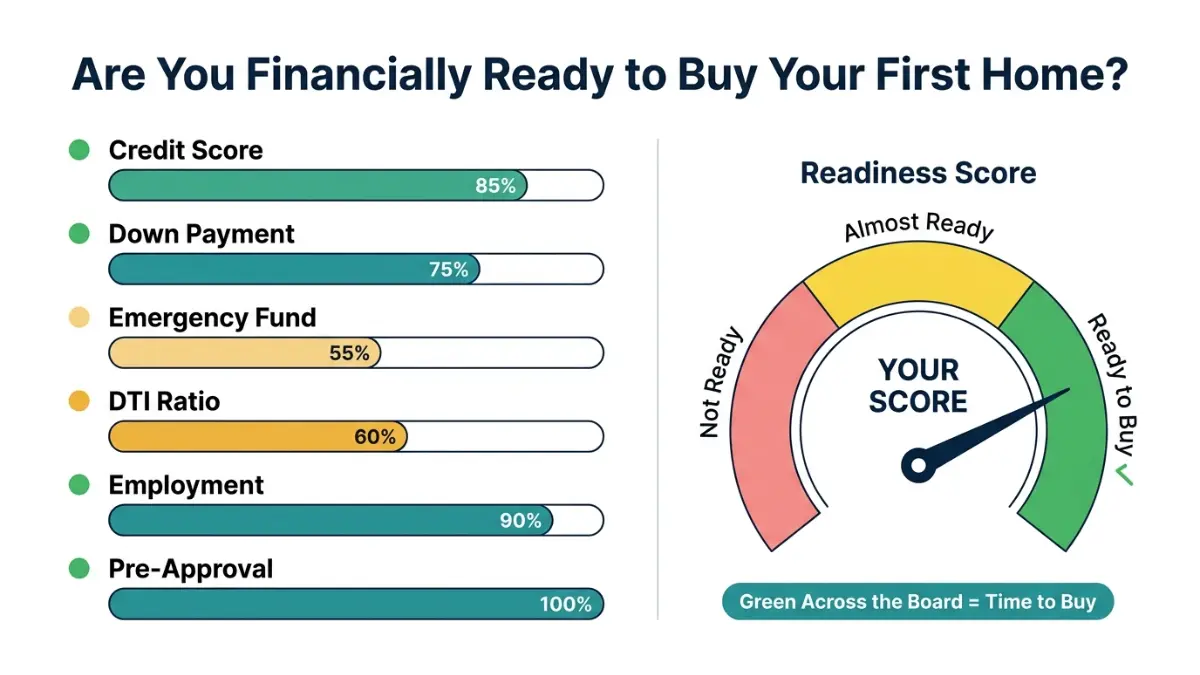

First-Time Home Buyer Checklist 2026 — Are You Actually Ready?

Before you put in a single offer, run through this readiness assessment:

| Readiness Criteria | Green ✅ | Yellow ⚠️ | Red ❌ |

|---|---|---|---|

| Credit Score | 740+ | 620–739 | Below 620 |

| Down Payment Saved | 10%+ | 3.5–9% | Under 3% |

| Emergency Fund | 6+ months expenses | 3–5 months | Under 3 months |

| Debt-to-Income Ratio | Under 36% | 36–43% | Over 43% |

| Stable Employment | 2+ years same employer | 1–2 years | Under 1 year |

| Pre-Approval Status | Approved | In process | Not started |

| Total Cost Budgeted | All-in costs covered | Down payment only | No budget set |

| Assistance Programs Checked | Yes, applied | Reviewed | Never checked |

Green across the board? You’re ready. Start with our Buy First Home 2026 Guide for your complete step-by-step roadmap.

Yellow or Red in multiple rows? Take 3–6 months to strengthen your position. It’s far better than a denied loan or a financial crisis 6 months into ownership.

What Finance Experts Say First-Time Buyers Get Most Wrong in 2026

Our expert panel at Finance Authority Hub consistently identifies the same patterns across thousands of first-time buyer situations.

Laura M. Bennett, CFP flags the hidden cost blindspot: “Most first-time buyers I counsel are prepared for the down payment but completely unprepared for year-one ownership costs — property taxes, insurance, and unexpected repairs can add $15,000–$25,000 in the first 12 months alone.”

Daniel Moreau, CPA/CFP emphasizes the pre-approval timeline: “Getting pre-approved early isn’t just about knowing your budget — it forces a credit review that often reveals fixable score issues. Buyers who pre-approve 6 months early consistently secure better rates than those who rush the process.”

Michael R. Thompson, CFA points to the assistance program gap: “Most buyers earning under $120,000 qualify for some form of down payment assistance. The HUD database alone lists thousands of programs by state. Leaving that money unclaimed is the most preventable mistake in real estate.”

The Consumer Financial Protection Bureau echoes this consensus — thorough preparation before and during the mortgage process is the single strongest predictor of a successful first home purchase.

7 First-Time Home Buyer Mistakes — Quick Reference

| # | Mistake | What It Costs | The Fix |

|---|---|---|---|

| 1 | No pre-approval before house hunting | Lost offers, wasted time | Pre-approve with 3+ lenders first |

| 2 | Budgeting only for down payment | $21K+/year cost shock | Calculate all-in costs from day one |

| 3 | Using just one lender | $1,500–$3,000+ overpaid | Compare at least 3 loan offers |

| 4 | Skipping home inspection | $5,000–$50,000+ in hidden repairs | Always inspect — never waive outright |

| 5 | Missing assistance programs | Up to $25,000+ unclaimed | Check HUD + your state programs |

| 6 | Emotional decision-making | Overpaying, wrong home | Use the 85% rule + DTI check |

| 7 | Financial changes before closing | Loan denial at the finish line | 60-day financial freeze before close |

Frequently Asked Questions — First-Time Home Buyers

Q1: What is the #1 mistake first-time home buyers make?

Skipping mortgage pre-approval before searching for homes. It’s the most common and most immediately costly mistake — it signals unpreparedness to sellers and leaves buyers without a clear budget anchor.

Q2: How much money should I save before buying a house in 2026?

Aim for at least 10–12% of the purchase price in liquid savings. That covers a 3.5–9% down payment, 2–5% in closing costs, a moving budget, and a starter emergency reserve. On a $400,000 home, plan for $40,000–$50,000 minimum.

Q3: What credit score do I need to buy a home for the first time?

FHA loans require a minimum 580 score for 3.5% down; some conventional loans accept 620+. But the best mortgage rates go to borrowers with scores above 740. Review our detailed Credit Score to Buy a House 2026 breakdown for exact thresholds by loan type.

Q4: Is it ever OK to skip the home inspection?

No. Even in competitive markets, a home inspection is your most important financial protection. Instead of waiving it entirely, offer an “informational only” inspection — it satisfies sellers while protecting you from hidden repair costs.

Q5: What’s the difference between pre-qualification and pre-approval?

Pre-qualification is a rough verbal estimate with no credit check. Pre-approval is a verified commitment based on your actual income, assets, and credit score. Only pre-approval carries weight with sellers.

Q6: How much are closing costs for first-time home buyers?

Closing costs typically range from 2–5% of the loan amount. On a $350,000 loan, that’s $7,000–$17,500. Some lenders offer no-closing-cost loans in exchange for a slightly higher rate. Read our Home Loan Closing Costs 2026 guide for a full itemized breakdown.

Q7: Can I buy a house with no down payment?

Yes — through VA loans (0% down for eligible veterans) and USDA loans (0% down in qualifying rural areas). Eligible first-time buyers can also access state-level down payment assistance programs. Visit HUD’s homebuyer page to find programs by state.

Q8: What is PMI and how do I avoid it?

Private Mortgage Insurance (PMI) is required on conventional loans when you put down less than 20%. It typically adds 0.5–1.5% of the loan amount annually to your payment. You can avoid it by putting 20% down, choosing a VA loan, or requesting cancellation once you reach 20% equity. Full guide: What Is PMI on a Mortgage.

Q9: How do I know if I’m financially ready to buy a home?

Use the Green/Yellow/Red readiness checklist in Section 3 above. The three most critical signals: credit score above 640, DTI below 43%, and at least 3–6 months of expenses in reserve beyond your down payment and closing costs.

Q10: Should I pay off debt before buying a house?

High-interest debt (credit cards, personal loans) directly raises your debt-to-income ratio and can reduce your loan approval amount. Paying down revolving debt before applying typically improves both your credit score and loan terms.

Q11: What first-time home buyer programs are available in 2026?

Federal programs include FHA loans, VA loans, and USDA loans. Over 2,000 state and local down payment assistance programs also exist. The HUD FHA loan center and your state housing finance agency are the best starting points.

⚠️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, mortgage, or legal advice. Interest rates, program eligibility, and market conditions referenced are subject to change. Always consult a licensed mortgage professional or certified financial advisor before making home purchase decisions. Finance Authority Hub is not a lender or mortgage broker.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.