Online vs Bank Mortgage: Which Saves You More in 2026?

Choosing between an online vs bank mortgage in 2026? We compare rates, closing speed, fees & borrower scenarios using live March 2026 data to help you pick the right lender.

In This Article

If you’re choosing between an online vs bank mortgage in 2026, here’s the direct answer: Online lenders typically close faster (22–30 days vs. 45+ days) and may offer slightly lower rates due to reduced overhead. But bank mortgages win for complex loans, HELOCs, and borrowers who value in-person guidance. The right choice depends entirely on your borrower profile — and this guide shows you exactly which fits yours.

The Online vs Bank Mortgage Landscape Has Completely Shifted in 2026

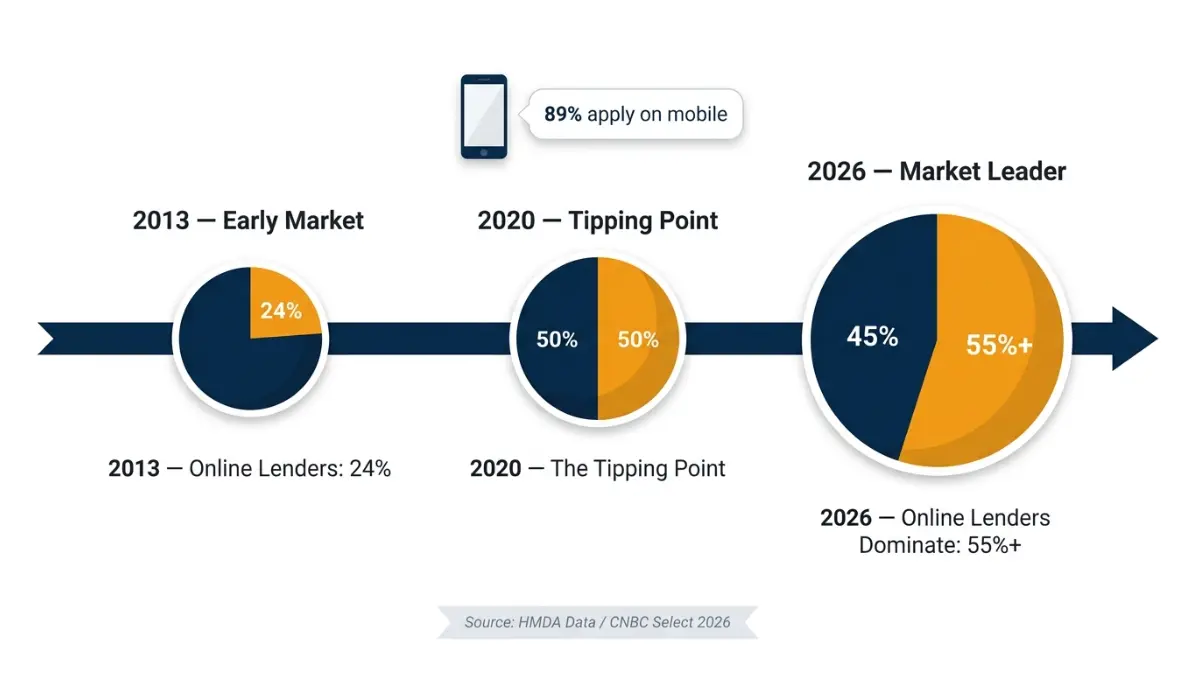

The mortgage market in 2026 looks nothing like it did five years ago. Online lenders now hold over 55% of the U.S. mortgage market — up from just 24% in 2013. That’s a seismic shift driven by speed, technology, and borrower demand for a frictionless digital experience.

Today, 89% of mortgage applications start on a mobile device, up from 73% in 2025. This means the typical American homebuyer is no longer walking into a bank branch — they’re comparing rates from their couch.

Here’s the 2026 reality check on rates right now:

| Loan Type | Average Rate (March 25, 2026) |

|---|---|

| 30-Year Fixed | 6.44% APR |

| 15-Year Fixed | 5.92% APR |

| 5-Year ARM | 6.80% APR |

| 30-Year Refi | 6.64% APR |

Source: NerdWallet/Zillow, March 25, 2026

With rates elevated — and rising due to geopolitical tensions — the difference between a well-chosen online lender vs. a traditional bank mortgage can translate to tens of thousands of dollars over the life of your loan. Use our mortgage calculator to see your exact monthly payment at today’s rates before you apply anywhere.

What Is an Online Mortgage Lender?

An online mortgage lender is a financial institution that processes home loans entirely — or primarily — through digital platforms. No branch visits. No paper stacks. Applications, approvals, document uploads, and even closings happen online.

- Examples: Rocket Mortgage, Better.com, SoFi, loanDepot, Rate

- Key distinction: Most are non-bank institutions — they originate loans but don’t offer checking or savings accounts

- Because they don’t need a full banking license, online lenders can have more flexible credit requirements and are not bound by as many federal regulations as traditional banks

What Is a Bank Mortgage?

A bank mortgage is a home loan originated directly through a federally chartered or state-chartered bank — think Wells Fargo, Chase, Bank of America, or your local community bank. They offer mortgages alongside their full suite of financial products (checking, savings, HELOCs, credit cards).

- Advantage: Relationship discounts for existing customers (typically 0.25% rate reduction)

- Advantage: Face-to-face guidance for first-time buyers and complex transactions

- Advantage: In-house underwriting with FDIC backing and regulatory oversight dating back decades

Before diving deeper, if you’re still deciding whether buying makes sense at all, our rent vs. buy calculator can run the numbers for your specific situation.

Online vs Bank Mortgage — The 2026 Head-to-Head Comparison

This is the comparison no competitor gives you with real 2026 data. Side by side. No fluff.

The Master Comparison Table

| Factor | Online Mortgage Lender | Bank Mortgage |

|---|---|---|

| Interest Rates | Often competitive; lower overhead may reduce rates | Existing customer discounts (0.25%) possible |

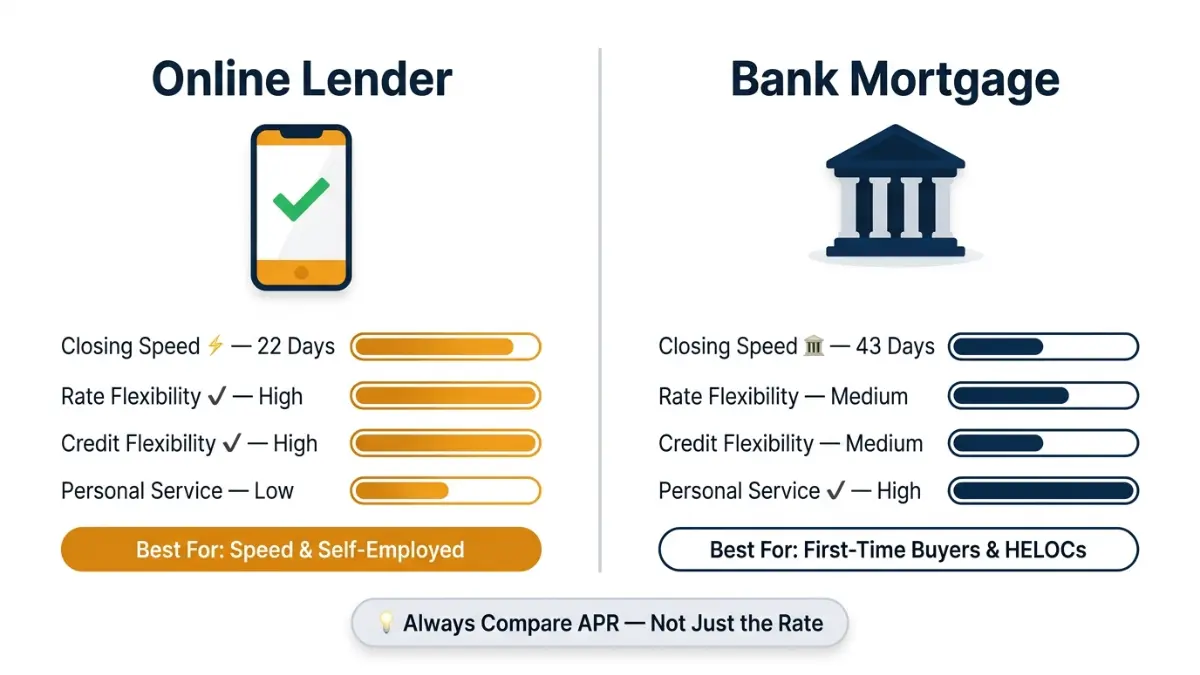

| Closing Time | 15–30 days (Rocket avg: 22 days) | 30–50 days (industry avg: 43 days) |

| Application | 100% digital; upload docs instantly | In-person or hybrid; some still paper-heavy |

| Customer Service | Phone, chat, evenings/weekends | Branch hours; dedicated loan officers |

| Loan Variety | Broad: FHA, VA, jumbo, non-QM, bank statement | Broad: conventional, jumbo, FHA, VA, HELOC |

| Credit Flexibility | More flexible; non-QM products available | More rigid; strict conventional guidelines |

| Fees | Generally lower origination fees | May include relationship perks but higher base fees |

| Best For | Speed-focused, digital-savvy, self-employed, refi | First-time buyers, complex loans, HELOC seekers |

Which Has Lower Mortgage Rates — Online or Bank?

This is the most Googled sub-question — and the honest answer is: it depends.

Unlike online banking — where fewer overhead costs consistently mean lower fees — digital mortgage lenders aren’t necessarily cheaper by default. Rates always vary by lender.

What actually drives your rate:

- Credit score (700+ gets the best pricing)

- Loan-to-value ratio (lower LTV = better rate)

- Loan type (VA and FHA often beat conventional)

- Points paid at closing

- Lender competition — which is why you must compare at least 3 lenders

Shopping around for a mortgage could save borrowers up to an average of $44,000 over the life of a 30-year loan, according to Realtor.com analysis.

What This Means For You: On a $400,000 30-year loan at 6.44% APR, a 0.25% rate reduction saves you approximately $18,200 over 30 years. Always compare APR — not just the interest rate — to account for origination fees and points. Use our APR calculator to run this comparison instantly.

Which Closes Faster?

This is where online lenders win clearly.

Online lenders close approximately 20% faster than brick-and-mortar banks, according to the Federal Reserve. Rocket Mortgage averages 22 days — nearly half the industry standard of 43 days.

In a competitive seller’s market where your offer needs a financing contingency, closing speed can be the difference between getting the home and losing it.

Who Should Choose an Online Mortgage Lender in 2026?

Online mortgages aren’t for everyone — but for these borrower types, they’re often the clear winner.

The Borrower Persona Decision Matrix

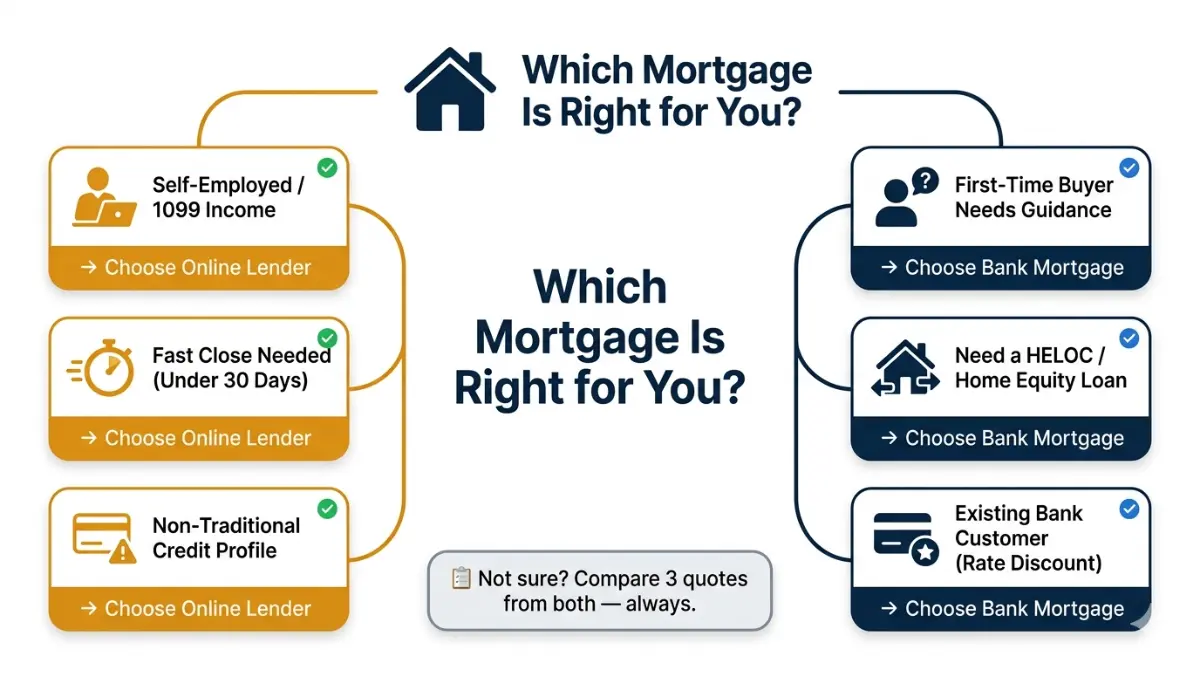

| Borrower Type | Recommended Choice | Primary Reason |

|---|---|---|

| Self-employed | Online lender | Bank statement & non-QM loan products |

| Fast-timeline buyer | Online lender | 22-day average close |

| Complex credit history | Online lender | Flexible underwriting |

| Refinancing existing loan | Online lender | Lower costs, faster processing |

| VA/FHA loan (competitive rates) | Shop both | Navy Federal Credit Union leads on APR |

| First-time buyer (needs guidance) | Bank or credit union | Face-to-face support |

| HELOC or home equity loan | Bank | Deposit-based relationship products |

| Jumbo loan / high-net-worth | Bank | Portfolio lending, concierge service |

Self-Employed Borrowers: Online Wins

Traditional banks demand 2 years of tax returns showing consistent income. Many self-employed borrowers show variable income on paper — even if their actual cash flow is strong.

Online lenders are more willing to work with unconventional borrowers — self-employed workers, foreign nationals, real estate investors, and those who’ve experienced a bankruptcy or foreclosure.

Bank statement loans — where lenders use 12–24 months of deposits instead of tax returns — are primarily an online lender product.

Speed-Focused Buyers: Online Wins

If you’re in a competitive market — think Austin, Phoenix, Miami — where sellers want clean, fast offers, an online mortgage pre-approval backed by an AI underwriting engine can deliver verified approval in 1–2 hours versus 3–5 days at a traditional bank.

Rocket’s Overnight Underwrite and Better.com’s AI engine now deliver verified approvals in 1–2 hours versus 3–5 days in 2025, and 67% of borrowers now expect same-day approval.

Is an Online Mortgage Safe?

Yes — as long as you verify the lender. Always confirm:

- The lender is NMLS-licensed (check the NMLS Consumer Access database)

- They are registered in your state

- They have a Better Business Bureau rating and J.D. Power scores

The Consumer Financial Protection Bureau (CFPB) maintains a rate exploration tool and lender complaint database that every mortgage applicant should consult before committing.

Who Should Choose a Bank Mortgage in 2026?

Banks aren’t obsolete. For specific borrower profiles, a traditional bank mortgage delivers advantages that no digital-only lender can match.

First-Time Homebuyers: Banks Often Win

Buying your first home involves more decisions than just the rate. Property type, loan structure, down payment assistance programs, escrow setup, title insurance — it’s a lot. A dedicated loan officer at a local bank or credit union who sits across the table from you can simplify this process dramatically.

Online-only mortgage lenders may offer low interest rates and flexible credit requirements, but they don’t always offer the personal service that can be an important priority for first-time homebuyers seeking insight about their options.

Many national banks also offer proprietary first-time buyer programs:

- Bank of America: Home Grant up to $7,500 for closing costs

- Chase: Down payment assistance in select markets

- Wells Fargo: Homebuyer Access® grant programs

Pair this with our down payment calculator to understand exactly how much you need to save before approaching any lender.

HELOC and Home Equity Loans: Banks Win

This is one area where online lenders simply can’t compete at scale. HELOCs require deposit relationships to fund them — a structural advantage for banks.

If you already own a home and want to tap equity for renovations or debt consolidation, check your current home equity position first with our home equity calculator, then approach your existing bank as the first call.

Existing Banking Customers: The Relationship Discount

Traditional banks offer the convenience of consolidated financial services — managing mortgages, checking, savings, and credit cards in one place, while online lenders specialize solely in mortgages.

If you have $100,000+ in deposits at a large bank, ask specifically about:

- Rate relationship discounts (typically 0.125%–0.25% off)

- Waived origination fees for loyal customers

- Priority processing for preferred clients

These benefits don’t show up on comparison websites. You have to ask directly.

For borrowers managing existing debt before applying, run your numbers through our debt-to-income ratio calculator — lenders require a DTI below 43% for most conventional loans. Our article on debt-to-income ratio for home loans explains exactly how to optimize this number before you apply.

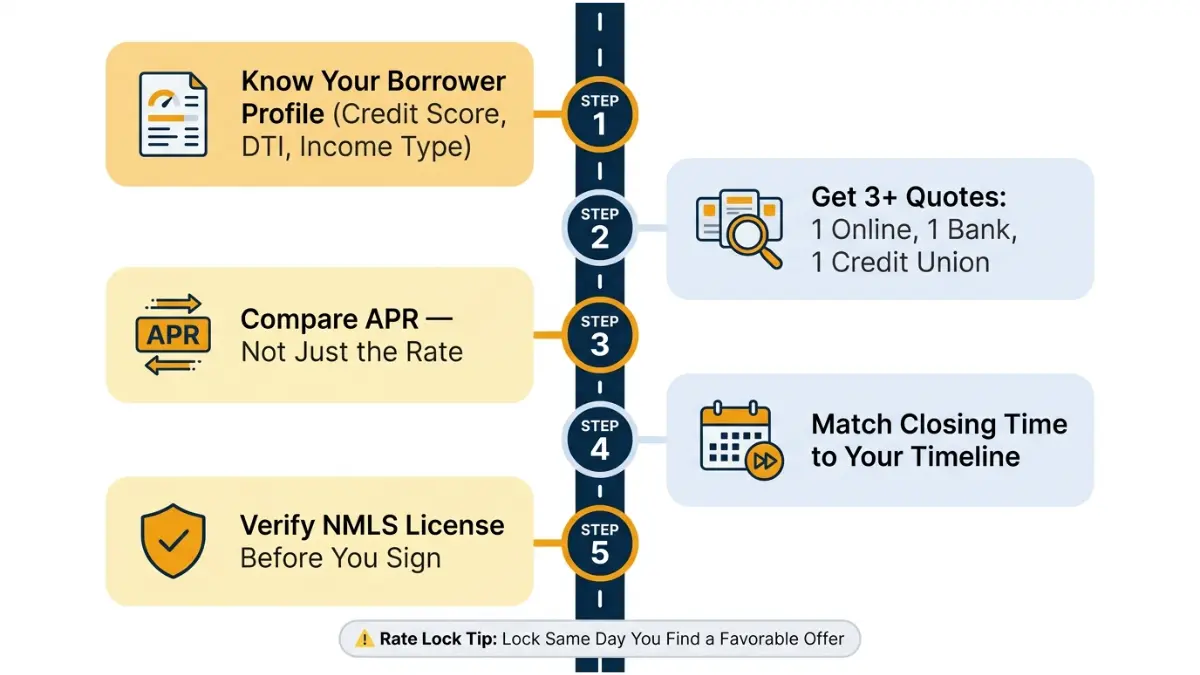

How to Choose the Right Mortgage Lender — A 5-Step 2026 Framework

This is the step no competitor gives you. Not a pros-and-cons list — a decision system built for today’s market.

Step 1: Know Your Borrower Profile

Before comparing a single rate, know these five numbers:

- Credit score (pull free at AnnualCreditReport.gov)

- Debt-to-income ratio (keep below 43%)

- Down payment percentage (3%, 5%, 10%, or 20%)

- Income type (W-2, 1099, self-employed, mix)

- Timeline (need to close in 30 days vs. 90 days)

Your credit score alone determines which lenders will offer you the best pricing. If yours needs work, read our guide on credit score requirements to buy a house in 2026 before applying.

Step 2: Get Quotes from at Least 3 Lenders

Always compare quotes from:

- 1 major online lender (Rocket, Better.com, SoFi)

- 1 national bank (Chase, Wells Fargo, Bank of America)

- 1 credit union or community bank (Navy Federal consistently leads on APR)

Submit all applications on the same day so rate changes don’t distort your comparison. Multiple mortgage inquiries within a 45-day window count as a single hard pull under FICO scoring — so there’s no credit penalty for shopping around.

Step 3: Compare APR — Not Just the Interest Rate

The interest rate is the headline. APR is the truth.

APR includes:

- Interest rate

- Origination fees

- Discount points

- Mortgage insurance (if applicable)

Our APR vs. interest rate guide explains exactly why two lenders quoting the same rate can cost you thousands of dollars differently.

Step 4: Evaluate Closing Time vs. Your Timeline

- Buying in a competitive market? Prioritize online lenders for speed.

- Buying with a 60-day closing window? Shop both — use closing time as a tiebreaker, not the primary filter.

- Refinancing? Online lenders typically win on cost and speed.

Use our mortgage refinance calculator to determine if refinancing makes financial sense at today’s rates before committing to any lender.

Step 5: Verify Every Lender Before You Sign

Red flags to avoid:

- No NMLS license number visible on their website

- No physical address or verifiable contact information

- Rates dramatically below every competitor (too good to be true)

- Pressure to sign quickly before “the rate expires”

Always verify licensure at the NMLS Consumer Access database and cross-check complaints at the CFPB complaint portal.

2026 Pro Tip: With mortgage rates at 6.44% and geopolitical instability pushing rates upward week-by-week, lock your rate the day you find a favorable offer. Rate lock periods typically run 30–60 days. Don’t float without a clear strategy.

Frequently Asked Questions — Online vs Bank Mortgage

1. Is an online mortgage safer than a bank mortgage?

Yes — provided the lender is NMLS-licensed and state-registered. Online lenders are regulated by state financial authorities and the CFPB. Always verify the license number on the lender’s website before submitting any application.

2. Do online lenders have better mortgage rates than banks?

Not automatically. If an online lender offers even a quarter of a percent lower rate, that could save thousands of dollars over the life of a loan. But this only applies if you compare correctly — using APR, not just the advertised interest rate.

3. How fast can I get approved for an online mortgage in 2026?

Many online lenders now deliver conditional approvals in 1–2 hours using AI underwriting. Full verified approval typically takes 24–72 hours. Closing averages 15–30 days — compared to 30–50 days at traditional banks.

4. Can I get an FHA or VA loan from an online lender?

Yes. You can apply for just about any type of mortgage online, including FHA loans, VA loans, conventional loans, and jumbo mortgages. Our comparison of VA loan vs. FHA loan options details which government-backed program offers better value for your situation.

5. What credit score do I need for an online mortgage?

Most online lenders accept scores as low as 580 for FHA loans and 620 for conventional loans. Some non-QM products from online lenders go as low as 500. Banks typically require 620–640 minimum for conventional loans.

6. Are online mortgage lenders regulated?

Yes. They must be licensed in every state where they originate loans, registered with the NMLS, and comply with federal laws including RESPA, TILA, and ECOA. The CFPB supervises non-bank mortgage lenders at the federal level.

7. What is the average closing time for online vs bank mortgages?

Online lenders average 22–30 days. Traditional banks average 30–50 days. Credit unions typically fall in the 30–40-day range. In competitive markets, that 10–20 day difference can determine whether your offer is accepted.

8. Can self-employed borrowers get better terms from an online lender?

In most cases, yes. Online lenders offer bank statement loans, 1099 loans, and profit-and-loss statement mortgages that aren’t standard bank products. These are specifically designed for income that doesn’t fit a traditional W-2 template.

9. What’s the current average 30-year mortgage rate in 2026?

As of March 25, 2026, the national average 30-year fixed mortgage APR is 6.44% (NerdWallet/Zillow). The 15-year fixed averages 5.92% APR. Rates have risen recently due to geopolitical tensions — see our guide on the lowest mortgage rates by state in 2026 to find the best rate in your market.

10. Should a first-time buyer use an online lender or a bank?

First-time buyers who need guidance, hand-holding through paperwork, or down payment assistance programs often benefit more from a bank or credit union. Digital-savvy first-time buyers with strong credit and W-2 income can save time and potentially money with an online lender. Read our full first-time homebuyer guide for 2026 before deciding.

11. What documents do I need to apply for a mortgage online?

Prepare these before starting any application:

– Last 2 years of federal tax returns (W-2 or 1099)

– Last 2–3 months of bank statements

– Last 30 days of pay stubs

– Photo ID (government-issued)

– Social Security number

– Property address and purchase agreement (if applicable)

– Proof of assets (investment accounts, retirement funds)

Self-employed borrowers should also prepare 2 years of business returns and a year-to-date profit-and-loss statement.

Expert Review: This article was reviewed by Laura M. Bennett, CFP®, Senior Financial Advisor and member of the financeauthorityhub.com expert panel, for accuracy and compliance with current 2026 lending standards.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, mortgage, or investment advice. Mortgage rates, lender terms, and market conditions change frequently. Always consult a licensed mortgage professional before making any home financing decision. Individual results will vary based on credit profile, loan amount, and lender.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.