Fixed Rate vs Adjustable Rate Mortgage: Which Should You Choose? (2026 Guide)

Confused between fixed rate vs adjustable rate mortgage? See March 2026 rates, a break-even comparison table, and a 3-persona decision framework.

In This Article

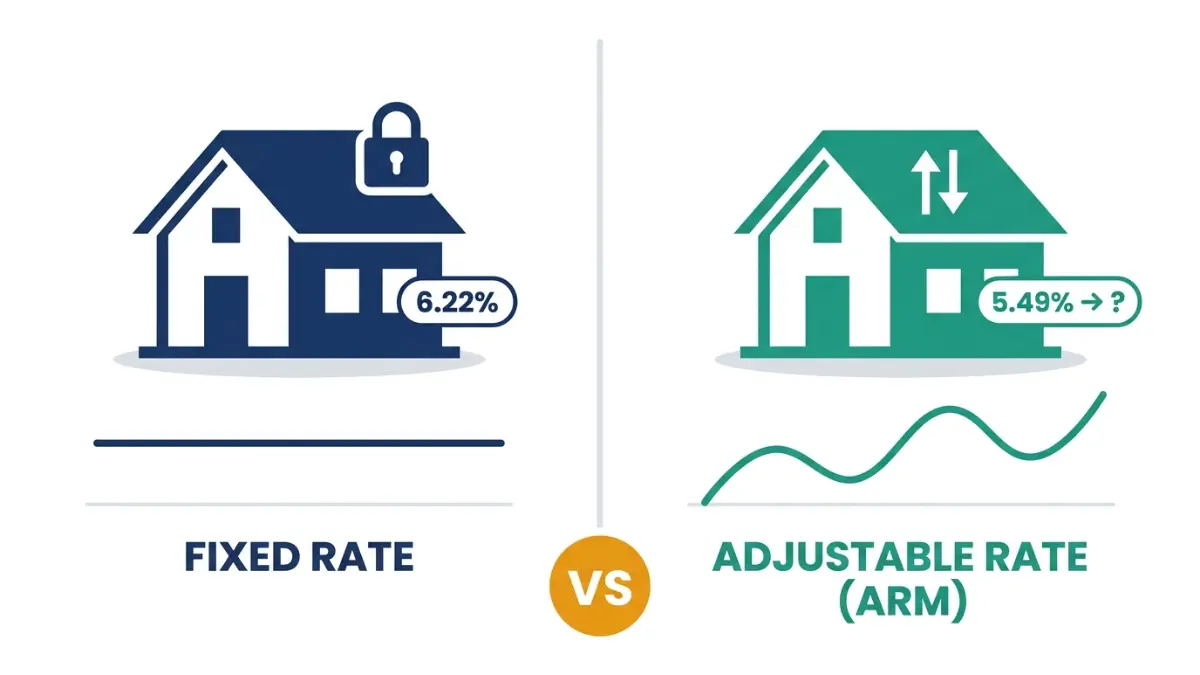

In March 2026, a 30-year fixed-rate mortgage averages 6.22% while a 5/1 ARM starts near 5.49%. That gap translates to roughly $185/month on a $400,000 loan. Choosing the wrong mortgage type could cost — or save — you tens of thousands of dollars. This guide breaks down every difference, with real 2026 numbers, so you can make the right call.

Fixed Rate vs Adjustable Rate Mortgage — The Core Difference

A fixed-rate mortgage locks in one interest rate for the entire life of your loan. Whether you choose a 15-year or 30-year term, your principal and interest payment never changes — no matter what happens in the economy.

An adjustable-rate mortgage (ARM) starts with a fixed introductory rate — typically for 3, 5, 7, or 10 years — then adjusts periodically based on a market index. Your payment can go up or down after the initial fixed period ends.

Use our mortgage calculator to instantly compare monthly payments across both loan types at today’s rates.

Side-by-Side Snapshot: Fixed Rate vs ARM (March 2026)

| Feature | Fixed-Rate Mortgage | Adjustable-Rate Mortgage (ARM) |

|---|---|---|

| Interest Rate | Locked for life | Fixed initially, then adjusts |

| Monthly Payment | Never changes | Can increase or decrease |

| Current Rate (30-yr / 5/1) | ~6.22% | ~5.49–5.64% |

| Best For | Long-term owners (7+ years) | Short-term owners (<7 years) |

| Risk Level | Low | Medium to High |

| Payment Predictability | 100% predictable | Uncertain after reset |

| Market Share (2026) | ~92% of U.S. mortgages | ~8% of U.S. mortgages |

Key Takeaway: Most U.S. homebuyers choose fixed-rate mortgages for predictability. But ARMs can offer real savings in the right situation — if you understand exactly when and why.

How Each Mortgage Actually Works — The Full Mechanics

How a Fixed-Rate Mortgage Works

Your interest rate is set at closing and stays the same for the loan’s entire term. The most common terms are 30 years and 15 years, though 10-, 20-, and 25-year options exist.

- 30-year fixed: Lower monthly payment, more interest paid over time

- 15-year fixed: Higher monthly payment, significantly less total interest, faster equity building

- Important: Even if the Fed cuts rates, your fixed-rate payment does not change. You’d need to refinance to benefit — use our mortgage refinance calculator to model whether refinancing makes financial sense for you.

How an Adjustable-Rate Mortgage Works

ARMs use a hybrid structure. Here’s what the numbers mean:

- 5/1 ARM: Fixed rate for 5 years, adjusts once every year after

- 7/6 ARM: Fixed rate for 7 years, adjusts every 6 months after

- 10/1 ARM: Fixed rate for 10 years, adjusts once annually after

After the fixed period, your rate is recalculated based on a benchmark index — most commonly SOFR (Secured Overnight Financing Rate), published daily by the New York Federal Reserve. Your lender adds a fixed margin (typically 2–3.5%) on top of SOFR to determine your new rate.

ARM Rate Caps Decoded: What “2/1/5” Actually Means

ARM loans have built-in limits on how much your rate can rise. You’ll often see caps listed as three numbers, like 2/1/5:

| Cap | Meaning | Example on a $400K Loan |

|---|---|---|

| First number (2) | Max rate increase at first adjustment | Rate can’t jump more than 2% in Year 6 |

| Second number (1) | Max increase at each subsequent adjustment | Rate can’t rise more than 1% per year after |

| Third number (5) | Max lifetime rate increase | Rate can never be more than 5% above your starting rate |

So if your 5/1 ARM starts at 5.49%, the worst-case scenario under 2/1/5 caps is a rate of 10.49% over the life of the loan. Always stress-test this scenario before signing.

The Consumer Financial Protection Bureau’s ARM explainer provides additional guidance on understanding your ARM documentation and cap structures.

The 2026 Rate Environment — Why Timing Matters Right Now

As of the week ending March 19, 2026, the 30-year fixed-rate mortgage averaged 6.22% — nearly half a percentage point lower than a year ago, when it stood at 6.67%. The 15-year fixed averaged 5.54%.

The 5/1 ARM is currently running around 5.49–5.64%, meaning the fixed-to-ARM spread is approximately 0.6–0.7 percentage points.

Why Rates Are Staying Elevated in 2026

The conflict in Iran has pushed oil prices higher, reigniting inflation concerns. As inflation rises, the likelihood of near-term Fed rate cuts diminishes.

- The Federal Open Market Committee (FOMC) held rates steady at its March 17–18 meeting

- The 10-year Treasury yield has risen due to oil price shocks and risk premiums

- The mortgage-to-Treasury spread sits at approximately 2%, reflecting lender risk assessment

What the Forecasts Say

Fannie Mae’s Economic and Strategic Research Group projects 30-year fixed mortgage rates will average around 6.1% in the first quarter of 2026. The Mortgage Bankers Association similarly expects rates to hold in the low-to-mid 6% range throughout 2026, 2027, and 2028.

Nobody is forecasting a return to sub-5% rates in the foreseeable future.

What This Means for Your ARM Decision

Rate cuts from the Federal Reserve affect adjustable-rate mortgages directly but impact fixed-rate mortgages only indirectly. That means:

- If the Fed cuts rates in late 2026 or 2027, ARM holders benefit at reset time

- If inflation persists (which is the current risk), ARM holders face upward pressure at adjustment

- The narrow fixed-ARM spread of ~0.6% makes the risk/reward of an ARM less compelling than in years when the spread was 1.5–2%

What This Means For You: Locking in a fixed rate near 6.2% today may look like a smart long-term decision, especially compared to 7%+ rates from late 2023–2024. The spring 2026 buying window is materially more affordable than the last two years.

You can track how your estimated monthly payment changes across different rate scenarios using our amortization calculator.

The Decision Framework — Which Mortgage Is Right for You?

This is the section every competitor skips. Instead of vague “it depends” advice, here’s a persona-based decision matrix built on real borrower scenarios.

The 3 Borrower Profiles

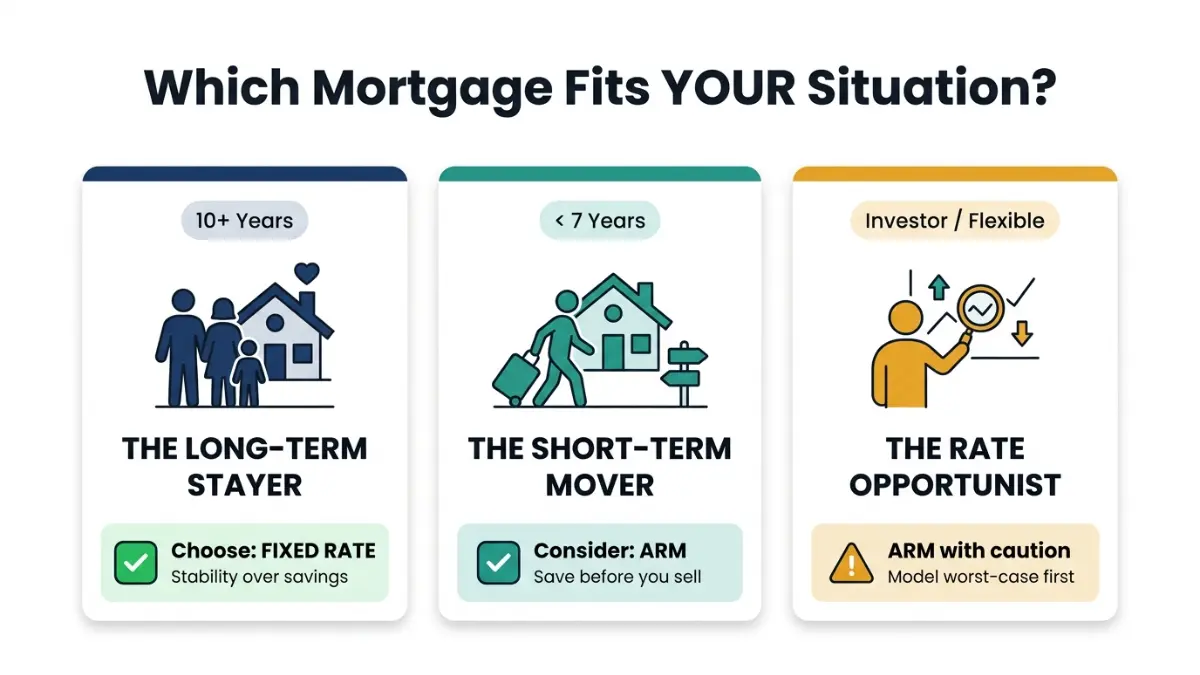

🏠 Profile 1: The Long-Term Stayer (10+ years in the home)

- You want payment stability and no surprises

- Your income is steady and not expected to dramatically increase

- You’re buying your forever home or plan to raise a family here

- → Choose: Fixed-Rate Mortgage

This is especially true for first-time homebuyers. Most mortgage lenders agree that a fixed-rate loan is optimal for a first-time buyer — predictable payments help with budgeting and reduce default risk.

Before you commit, check how much home you can actually afford using our home affordability calculator.

🔄 Profile 2: The Short-Term Mover (plan to sell or refinance in under 7 years)

- You’re relocating for work in 4–6 years

- You’re buying a starter home with plans to upgrade

- You’re confident you’ll sell or refinance before the ARM resets

- → Choose: 5/1 or 7/1 ARM

Because interest rates on ARMs tend to be lower than those on fixed-rate loans during the initial fixed-rate phase, adjustable-rate loans are a strong option for borrowers who don’t plan to stay beyond the fixed-rate period.

📈 Profile 3: The Rate Opportunist (investor or financially sophisticated buyer)

- You’re buying an investment property or high-value non-conforming loan

- You have financial flexibility to absorb a payment increase

- You believe rates will fall before your ARM resets

- → Consider: ARM, but model worst-case scenario first

Fixed-rate home loans represent roughly 92% of all U.S. mortgages — a testament to their reliability. About 8% of borrowers opt for ARMs, and ARMs remain most popular for higher loan size (nonconforming) loans.

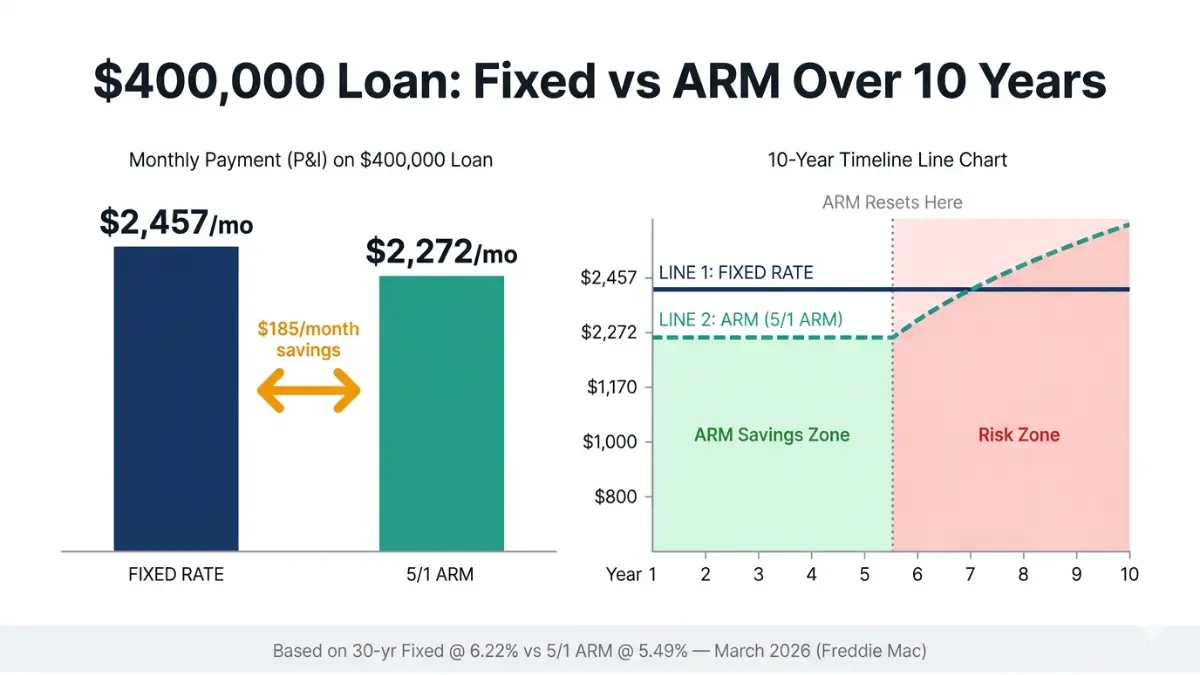

The Break-Even Scenario: $400,000 Loan, Fixed vs 5/1 ARM

| 30-Year Fixed (6.22%) | 5/1 ARM (5.49%) | |

|---|---|---|

| Monthly Payment (P&I) | ~$2,457 | ~$2,272 |

| Monthly Savings with ARM | — | ~$185 |

| Total Savings Over 5 Years | — | ~$11,100 |

| Year 6 Risk (rate resets to 7.22%) | No change | Payment jumps ~$290/month |

| Break-even (savings erased by) | — | ~Year 9–10 if rate stays elevated |

Bold Rule of Thumb: If the ARM rate is less than 1% lower than the fixed rate, the risk/reward rarely justifies choosing an ARM for most borrowers. At today’s ~0.6–0.7% spread, most long-term buyers are better served by locking in the fixed rate.

Use our refinance calculator to model the cost of switching from an ARM to a fixed rate if rates climb after your adjustment period.

Quick Decision Checklist

- ✅ How long will you stay in the home?

- ✅ Can your budget handle a payment jump of $300–$500/month?

- ✅ Is your income likely to grow before the ARM resets?

- ✅ Are you buying a primary home or an investment property?

- ✅ Is your debt-to-income ratio comfortable? (Check it with our debt-to-income ratio calculator)

- ✅ Do you have 6+ months of emergency savings if your ARM resets high?

Full Pros, Cons & Global Perspective

Fixed-Rate Mortgage — Pros & Cons

| ✅ Pros | ❌ Cons |

|---|---|

| Rate locked for entire loan life | Higher starting rate than ARM |

| Completely predictable monthly payment | No automatic benefit if rates fall |

| Best for long-term ownership | Refinancing required to access lower rates |

| Simpler to understand and manage | Higher qualifying payments when rates are elevated |

| Dominant in U.S. market — widely available | Slightly harder to qualify during high-rate periods |

Adjustable-Rate Mortgage — Pros & Cons

| ✅ Pros | ❌ Cons |

|---|---|

| Lower introductory interest rate | Payment uncertainty after fixed period |

| Lower initial monthly payments | Can increase significantly at each adjustment |

| Ideal for short-term homeowners | Cap structures can be complex |

| Benefits directly from Fed rate cuts | Requires active monitoring and planning |

| Often easier to qualify | Risk of payment shock if rates rise sharply |

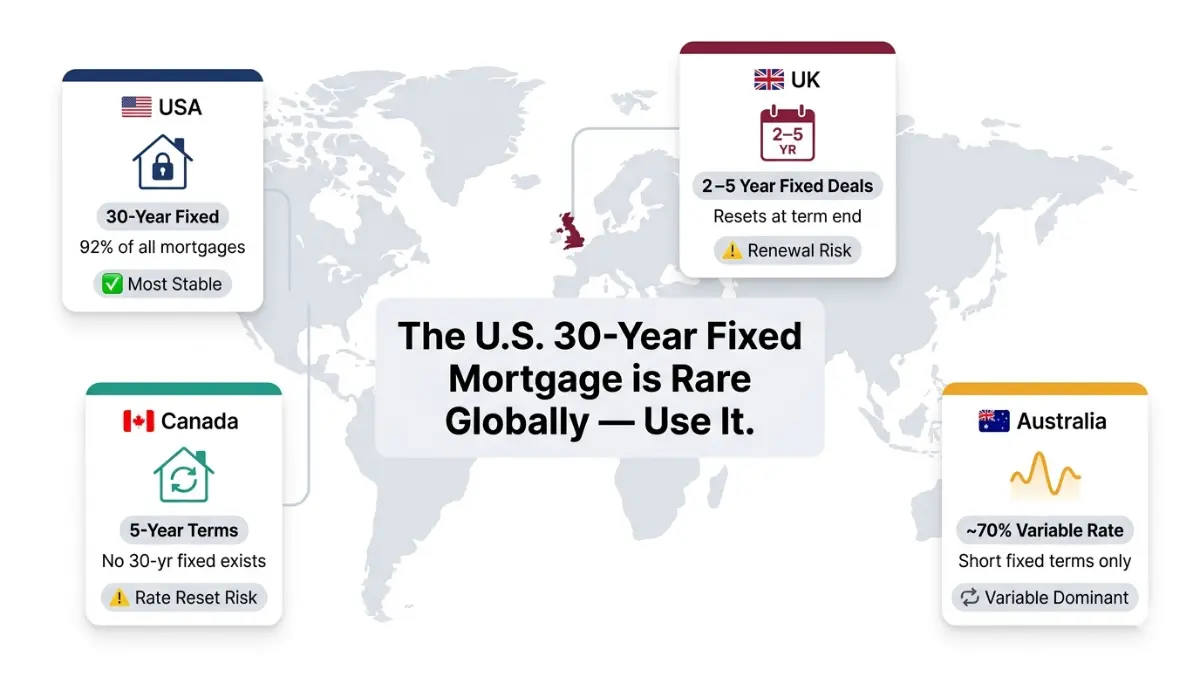

A Global Perspective: The U.S. Fixed-Rate Advantage

Most American homebuyers don’t realize how unusual the U.S. 30-year fixed-rate mortgage is globally.

- 🇬🇧 United Kingdom: Most mortgages are 2–5 year fixed “deals” that expire and must be renegotiated. Tracker mortgages (UK’s variable equivalent) move directly with the Bank of England base rate — far closer to an ARM structure than U.S. fixed loans.

- 🇨🇦 Canada: The standard mortgage term is 5 years with mandatory renewal after. There is no true 30-year fixed-rate product. At renewal, borrowers face whatever the prevailing rate is — exposing them to significant rate risk.

- 🇦🇺 Australia: Variable-rate mortgages dominate the market, making up approximately 70% of loans. Fixed terms typically max out at 1–5 years before reverting to variable.

What This Means For You: The U.S. 30-year fixed-rate mortgage is a uniquely powerful financial product that barely exists in other developed countries. If you’re a U.S. homebuyer, the ability to lock a competitive rate for three decades is an extraordinary advantage — one worth taking seriously.

The U.S. Department of Housing and Urban Development (HUD) provides free resources for homebuyers navigating mortgage decisions, including guides on loan types and first-time buyer programs.

Also see our comparison of 15 vs 30 year mortgage and our deep-dive on lowest mortgage rates by state in 2026 to find the most competitive rates in your market.

Frequently Asked Questions

1. What is the main difference between a fixed rate and adjustable rate mortgage?

A fixed-rate mortgage keeps the same interest rate for the entire loan life. An ARM starts with a fixed introductory rate, then adjusts periodically based on a market index like SOFR. The core tradeoff is stability vs. initial savings.

2. Is a fixed or adjustable rate mortgage better in 2026?

For most buyers planning to stay 7+ years, a fixed rate is better given the narrow fixed-ARM spread of ~0.6% in March 2026. Short-term buyers or investors may still benefit from an ARM’s lower introductory rate — but model the worst-case reset scenario first.

3. What is a 5/1 ARM mortgage?

A 5/1 ARM offers a fixed interest rate for the first 5 years, then adjusts once annually based on current market rates and your loan’s cap structure. It’s the most common ARM type in the U.S. market.

4. What are ARM rate caps and how do they work?

ARM caps limit how much your rate can increase. A 2/1/5 cap structure means: a max 2% increase at first adjustment, max 1% at each subsequent adjustment, and a max 5% increase over the loan’s entire life. Always verify your specific loan’s cap structure before signing.

5. Can you refinance from an ARM to a fixed-rate mortgage?

Yes — and many borrowers do this before their adjustment period begins. Refinancing to a fixed rate can help shield you from higher monthly payments when the rate adjusts, making it easier to budget for housing costs. Use our mortgage refinance calculator to model the exact savings and break-even timeline.

6. What is SOFR and why does it affect my ARM?

SOFR (Secured Overnight Financing Rate) is the benchmark index most U.S. ARMs now use. Published daily by the New York Fed, it reflects the cost for banks to borrow overnight. When SOFR rises, your ARM rate rises at adjustment. It replaced LIBOR in 2023. Learn more at the New York Fed’s SOFR page.

7. Is an ARM a good idea for a first-time homebuyer?

Generally, no. First-time buyers benefit most from the payment predictability of a fixed-rate mortgage. The complexity, adjustment risk, and payment uncertainty of ARMs can put significant strain on first-time budgets. If you’re a first-time buyer, read our complete guide to buying your first home in 2026.

8. What happens if I can’t afford my ARM payment after it resets?

Your main options are: refinancing to a fixed-rate loan, requesting a loan modification from your servicer, or selling the home before payment shock worsens. The best protection is planning ahead — stress-test your budget against worst-case scenarios before you sign.

9. How much lower is an ARM rate vs. fixed rate in 2026?

As of March 19, 2026, the spread is approximately 0.6–0.7%: the 30-year fixed-rate mortgage averaged 6.22% (Freddie Mac) compared to a 5/1 ARM running around 5.49–5.64%. This is a historically narrow spread, reducing the ARM’s upfront advantage.

10. Does a fixed-rate mortgage protect you from rising interest rates?

Completely. Once your rate is locked, your principal and interest payment never increases — regardless of market conditions. This makes fixed-rate mortgages the safest choice in volatile or rising-rate environments like 2026.

11. Which mortgage type has lower monthly payments initially?

ARMs always start lower due to their introductory rate discount. On a $400,000 loan, a 5/1 ARM at 5.49% saves approximately $185/month compared to a 30-year fixed at 6.22% — roughly $11,100 in savings over the first 5 years. After the ARM resets, that advantage can reverse quickly if rates rise.

⚖️ Disclaimer: This article is for educational and informational purposes only. It does not constitute financial, mortgage, or investment advice. Mortgage rates change daily and individual circumstances vary. Always consult a licensed mortgage professional or financial advisor before making any borrowing decision. Rate data sourced from Freddie Mac PMMS (week of March 19, 2026) and Bankrate.

Related Tools: Mortgage Calculator · Home Affordability Calculator · Refinance Calculator · Amortization Calculator

Related Reading: 15 vs 30 Year Mortgage · Mortgage Pre-Approval Guide 2026 · APR vs Interest Rate

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.