Health Insurance Plans 2026: Don’t Pay $752/Mo

Health insurance premiums jumped 21% in 2026 — the average Silver plan now costs $752/mo. Here’s how to pick the right plan and pay less.

In This Article

The average American is now paying $752 per month for a Silver health insurance plan in 2026 — that’s $9,024 per year. And premiums jumped 21% in just one year. But millions of people are overpaying because they picked the wrong plan type, missed a subsidy, or never compared options.

This guide breaks down every type of health insurance plan, real 2026 costs by age, and the exact steps to stop overpaying — fast.

What Are Health Insurance Plans — and Why Are Costs Surging in 2026?

Health insurance plans are contracts between you and an insurer that cover medical expenses in exchange for a monthly premium. In 2026, those premiums hit record highs.

Silver plan premiums rose from $621/month in 2025 to $752/month in 2026 — a 21% jump nationwide. This is the sharpest single-year increase most American families have seen in nearly a decade.

Why Costs Exploded in 2026

Three forces collided at once:

- Enhanced ACA subsidies expired on December 31, 2025. Since 2021, these subsidies had lowered premiums for over 21 million enrollees. They are now gone.

- Insurer premium hikes of 23% were applied before subsidies, making unsubsidized plans dramatically more expensive.

- Year-round low-income enrollment ended — the safety net for missing open enrollment is gone.

What This Means For You: If you were auto-renewed into your 2025 plan, you may now be paying hundreds more per month without realizing it. Log into healthcare.gov immediately to review your current plan and compare alternatives.

If you are managing healthcare costs alongside other major financial commitments, use our debt consolidation calculator to see how your full household budget stacks up.

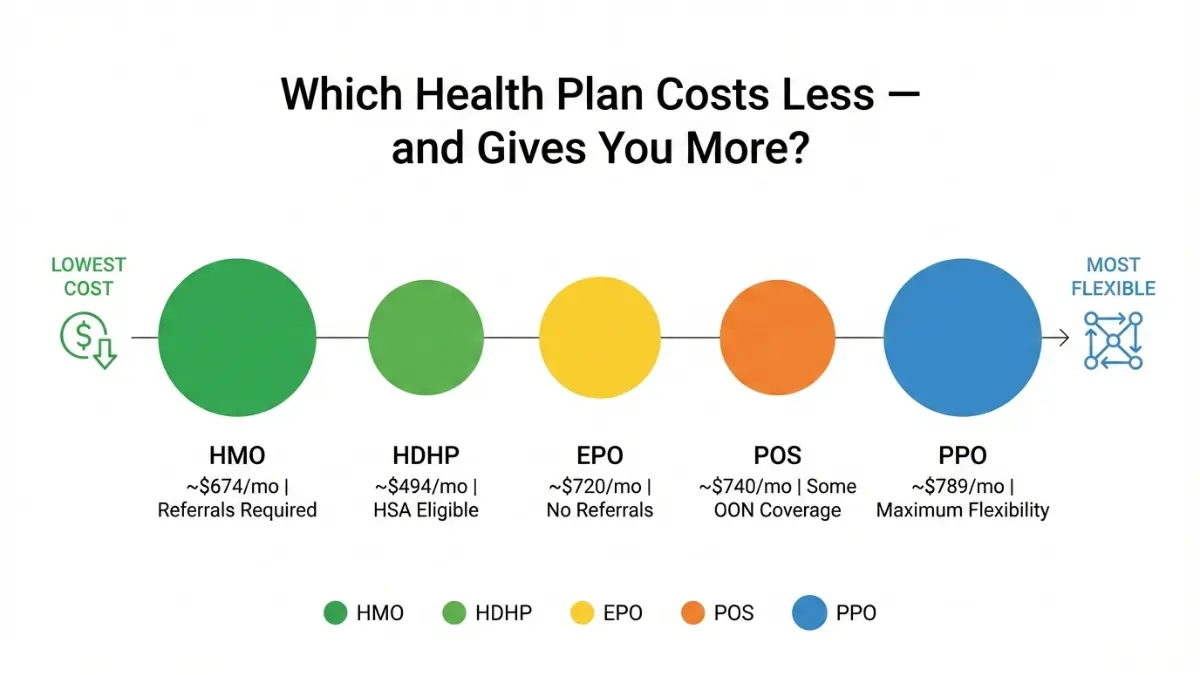

5 Types of Health Insurance Plans Explained (HMO, PPO, EPO, POS, HDHP)

Not all health insurance plans work the same way. The plan type you choose directly determines your monthly cost, flexibility, and out-of-pocket exposure. Healthcare.gov’s official plan types guide outlines the core differences — here’s what that means in plain numbers.

Quick Comparison Table: All 5 Plan Types (2026)

| Plan Type | Avg Monthly Cost | Referral Required? | Out-of-Network Coverage? | Best For |

|---|---|---|---|---|

| HMO | ~$674/mo | ✅ Yes | ❌ No (emergencies only) | Budget-focused, coordinated care |

| PPO | ~$789/mo | ❌ No | ✅ Yes (partial) | Flexibility, frequent travelers |

| EPO | ~$720/mo | ❌ No | ❌ No (emergencies only) | Balance seekers, specialist access |

| POS | ~$740/mo | ✅ Sometimes | ✅ Yes (higher cost) | Moderate users wanting some flexibility |

| HDHP + HSA | ~$494/mo | ❌ No | Varies | Healthy adults, tax savers |

HMO (Health Maintenance Organization)

HMO plans have the lowest premiums but require you to use a specific network. You must choose a Primary Care Physician (PCP) who coordinates all your care and provides specialist referrals. Best for: Families who stay local and want predictable costs.

PPO (Preferred Provider Organization)

PPO plans offer maximum flexibility — see any doctor, any specialist, no referral needed. You pay more monthly, but partial out-of-network coverage protects you. Best for: People who travel frequently or have preferred specialists outside a local network.

EPO (Exclusive Provider Organization)

EPO plans sit between HMO and PPO in cost. No referrals needed, but you must stay in-network except in emergencies. Best for: Those who want specialist access without the high PPO premium.

HDHP + HSA (High-Deductible Health Plan with Health Savings Account)

This is the biggest 2026 change you need to know. As of January 1, 2026, all Bronze and Catastrophic marketplace plans are now eligible to be paired with a Health Savings Account (HSA). This is a new law — and it opens a powerful tax savings opportunity for millions of Americans.

2026 HSA Contribution Limits (IRS-verified):

- Individual: $4,400/year tax-free

- Family: $8,750/year tax-free

- Age 55+ catch-up: additional $1,000/year

Contributions to an HSA are pre-tax, grow tax-free, and withdraw tax-free for qualified medical expenses. That is a triple tax advantage. See the IRS Publication 969 for the full official rules.

What This Means For You: A healthy 30-year-old switching from a $789/mo PPO to a $494/mo Bronze HDHP saves $3,540/year in premiums — and can stash up to $4,400 into an HSA, reducing their taxable income further.

If you want to understand how health insurance fits into your broader financial plan, explore our insurance cost guide for a full picture.

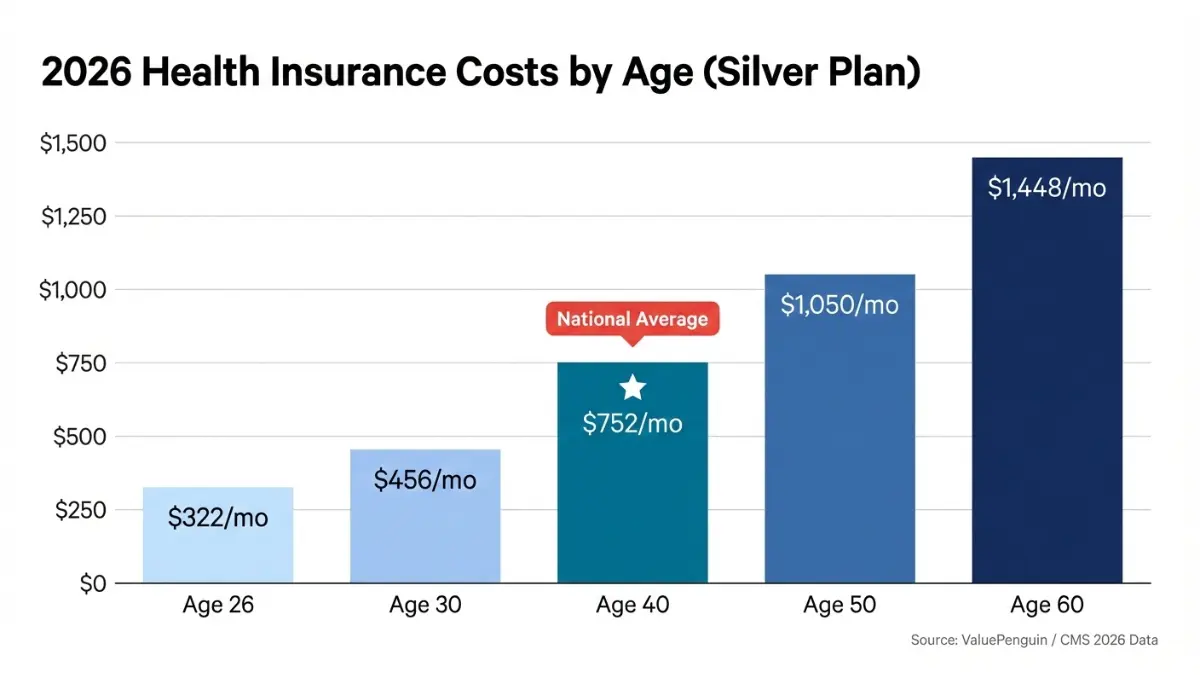

How Much Do Health Insurance Plans Cost in 2026? (By Age + Plan Tier)

Cost is the #1 question Americans have when shopping for health insurance plans. Here is the answer — by age and by metal tier — with real 2026 data.

Silver Plan Cost by Age (2026 National Averages)

| Age | Monthly Premium | Annual Cost |

|---|---|---|

| 26 | ~$322/mo | ~$3,864/yr |

| 30 | ~$456/mo | ~$5,472/yr |

| 40 | $752/mo | $9,024/yr |

| 50 | ~$1,050/mo | ~$12,600/yr |

| 60 | ~$1,448/mo | ~$17,376/yr |

Source: ValuePenguin 2026 Average Health Insurance Cost Analysis

Monthly Cost by Metal Tier (Age 40, Silver Benchmark)

| Metal Tier | Avg Monthly Cost | Deductible (Approx.) | OOP Maximum |

|---|---|---|---|

| Bronze | ~$494/mo | ~$7,000 | Up to $9,200 |

| Silver | ~$752/mo | ~$3,000–$5,000 | Up to $9,200 |

| Gold | ~$903/mo | ~$1,500 | Up to $9,200 |

| Platinum | $1,000+/mo | ~$500 | Lowest OOP |

State Variation Is Massive

Premiums are not equal across the country:

- Cheapest state: Maryland (~$480/mo Silver for age 40)

- Most expensive state: Vermont (~$1,224/mo Silver for age 40)

- National average: $752/mo Silver

That is a $744/month difference based purely on where you live. Always check your state marketplace before assuming the national average applies to you.

The ACA Subsidy Question: Do You Qualify?

Even after the enhanced subsidies expired, base federal subsidies still exist. For 2026:

- Individual income $15,650–$62,600 → likely eligible for premium tax credits

- Family of 4, income up to $128,600 → may qualify for significant subsidy

Use your home affordability calculator to model how health insurance premiums affect your overall housing and budget capacity — especially relevant for first-time buyers and self-employed professionals.

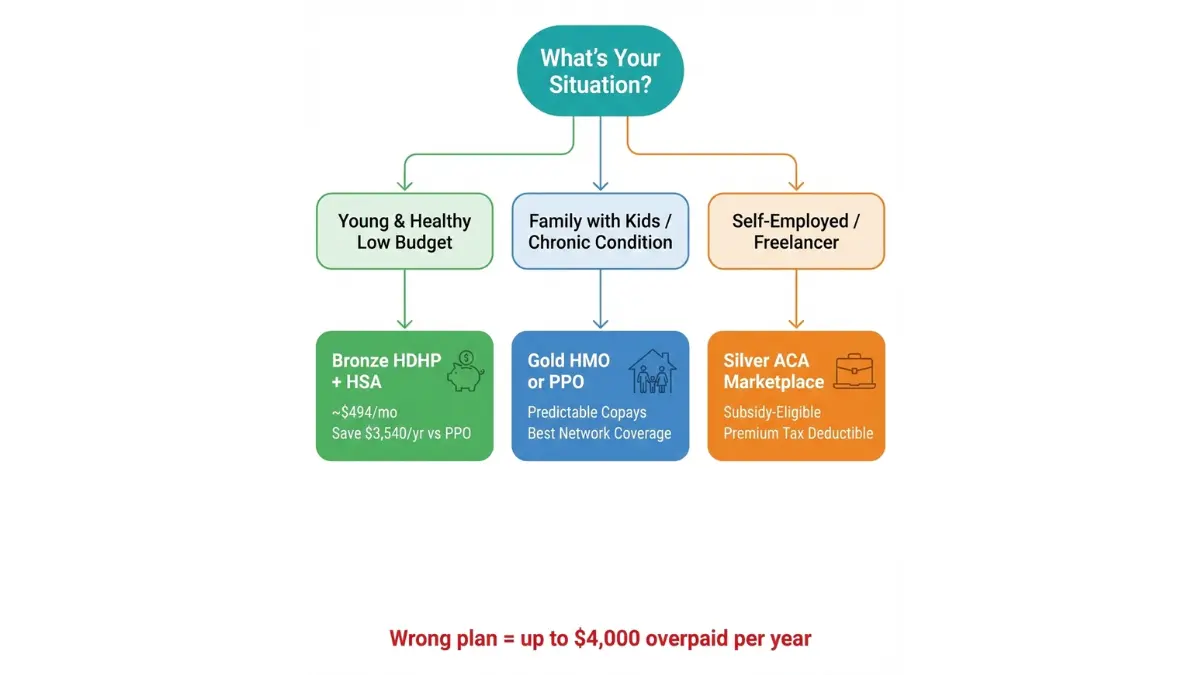

Which Health Insurance Plan Is Right for You? (By Life Situation)

This is the decision framework that NerdWallet, Bankrate, and Investopedia don’t give you. Instead of generic advice, here is a direct match between your life situation and the optimal health insurance plan type in 2026.

Life Situation → Best Plan Match

| Your Situation | Best Plan Type | Key Reason |

|---|---|---|

| Young, healthy, low budget | Bronze HDHP + HSA | Lowest premium; HSA builds tax-free savings |

| Freelancer / self-employed | Silver ACA Marketplace | Subsidy-eligible; premium is 100% tax-deductible |

| Family with children | PPO or EPO Gold | No specialist referrals; predictable copays |

| Senior under 65 | HMO (Anthem or BCBS) | HMO premiums run 16–26% below national average for this age group |

| Managing chronic condition | Gold HMO | Low out-of-pocket maximums protect high utilizers |

| Frequent traveler | PPO | Out-of-network partial coverage is essential |

| High earner, no subsidy | HDHP + HSA | Maximize triple tax benefit; reduce taxable income |

Real Case Example: Maria, Freelance Designer, Age 34

Maria earns $45,000/year working independently. She was auto-renewed into a Silver PPO at $752/month for 2026. After checking her subsidy eligibility, she qualified for a premium tax credit that reduced her Silver plan cost to approximately $210/month. She also switched to a Silver HMO for better coordinated care, dropping her premium further.

Annual savings vs. auto-renewal: ~$6,500.

5 Questions to Ask Before Choosing a Plan

- Are my current doctors in-network? Verify before you enroll — networks change every year.

- How often do I actually use healthcare? Low users benefit from HDHP; high users benefit from Gold.

- Do I have recurring prescriptions? Check formulary tiers before choosing.

- Can I fund an HSA? If yes, a Bronze HDHP may save thousands annually.

- What is my out-of-pocket maximum tolerance? Never ignore this number — it is your worst-case scenario.

If you are comparing health insurance costs alongside life insurance needs, our term life insurance guide and dental insurance 2026 guide are natural complements to read together.

What This Means For You: The single most expensive mistake in 2026 is accepting auto-renewal. Insurance companies auto-renew you into last year’s plan — which may now cost $100–$400 more per month due to subsidy expiry. Always actively re-compare during open enrollment.

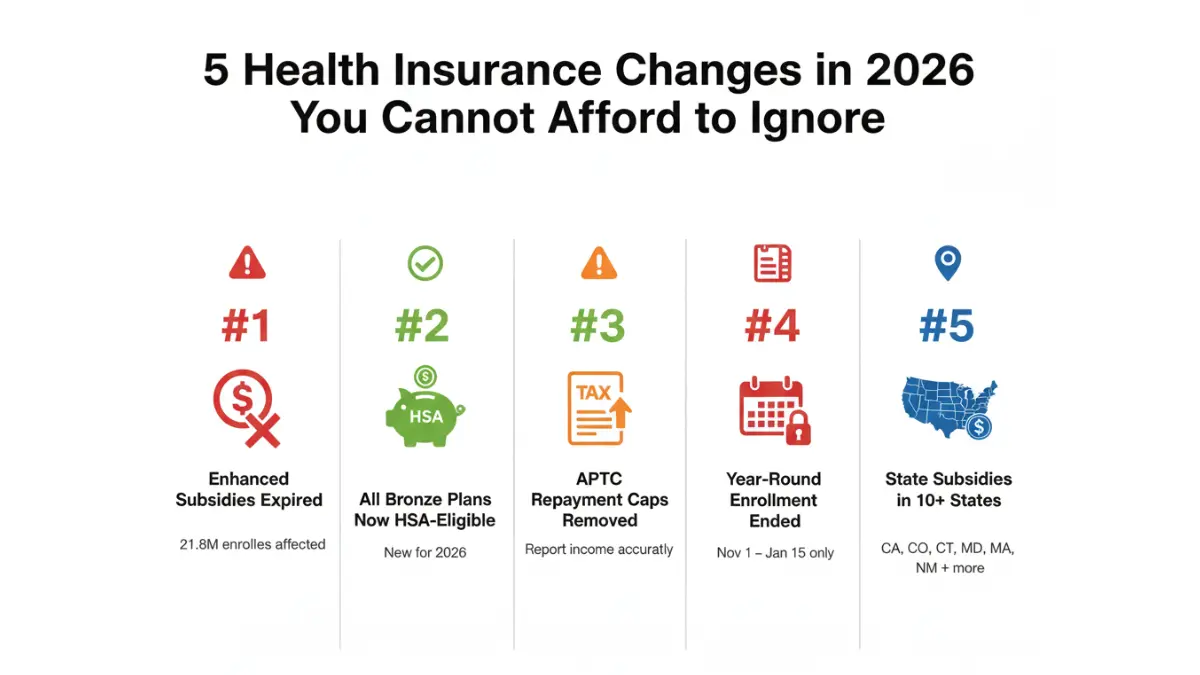

5 Critical 2026 Health Insurance Changes That Will Cost You — Unless You Act

This is what every competitor missed. These five 2026 changes are already affecting American families right now — and most people have no idea.

Change #1: Enhanced Subsidies Expired — 21.8 Million Enrollees Affected

The American Rescue Plan’s enhanced premium tax credits officially ended December 31, 2025. Insurers raised pre-subsidy premiums by a weighted average of more than 23% nationwide — the largest overall increase since 2018. If you had a subsidized plan, your base federal subsidy still applies, but the enhanced top-up is gone.

Action: Log into healthcare.gov and re-check your subsidy amount for 2026. Do not assume last year’s figures carry over.

Change #2: All Bronze and Catastrophic Plans Now HSA-Eligible

Starting January 1, 2026, all individual market Bronze and Catastrophic plans are considered HDHPs and eligible to be paired with an HSA, even if they don’t meet the traditional minimum deductible requirement. This affects 35% of marketplace plans — up from just 4% in 2025.

Action: If you are on a Bronze plan, open an HSA immediately. Contribute up to $4,400 individually ($8,750 family) and deduct it from your taxable income. This is newly available money for millions of Americans.

Change #3: APTC Repayment Caps Removed

Through 2025, if you overestimated your income and received too many advance premium tax credits (APTC), the repayment was capped. Starting with the 2026 tax year, that cap is gone. You must repay the full excess amount when you file taxes.

Action: Be precise when reporting income on your marketplace application. If income changes during the year, update your application promptly. Consult a tax professional if you have variable freelance or gig income.

Change #4: Year-Round Low-Income Enrollment Eliminated

The special enrollment period that allowed individuals below 150% of the federal poverty level to enroll year-round is now ended. Everyone — regardless of income — must enroll during open enrollment (November 1 – January 15 in most states).

Action: Mark your calendar now. Miss open enrollment and you need a qualifying life event (job loss, marriage, new baby, move) to enroll outside this window.

Change #5: State Subsidies Offer a Lifeline in 10+ States

Several states stepped up to partially replace expired federal enhancements. If you’re in California, Colorado, Connecticut, Maryland, Massachusetts, or New Mexico, state-funded subsidies may offset some or all of the reduction in your federal subsidy.

Action: If you live in one of these states, visit your state marketplace (not just healthcare.gov) to see your full subsidy picture.

For a deeper look at how insurance costs interact with your 2026 financial health, explore our cheap insurance savings guide and our Medicare Advantage plans overview.

To review all open enrollment details directly from the federal government, visit KFF’s 2026 ACA Open Enrollment resource.

Frequently Asked Questions About Health Insurance Plans

1. What are the main types of health insurance plans?

The four primary types are HMO, PPO, EPO, and POS. A fifth category — HDHP — is defined by its deductible structure and is now paired with HSA savings accounts. Each type balances cost against provider flexibility differently.

2. How much does health insurance cost per month in 2026?

The national average Silver plan costs $752/month for a 40-year-old. Costs range from ~$322/month (age 26) to ~$1,448/month (age 60). Your actual cost depends on age, state, plan tier, and subsidy eligibility.

3. What is the cheapest type of health insurance plan in 2026?

Bronze HDHP plans average ~$494/month — the lowest premium tier. When paired with an HSA, the tax savings effectively reduce your net cost further. These are now HSA-eligible for all Bronze marketplace plans in 2026.

4. What changed in ACA marketplace plans for 2026?

Three major changes: enhanced subsidies expired (premiums up 23%), all Bronze/Catastrophic plans became HSA-eligible, and APTC repayment caps were removed. Year-round low-income enrollment also ended.

5. What is the difference between HMO and PPO health plans?

HMO: Lower cost (~$674/mo avg), requires referrals, network-only. PPO: Higher cost (~$789/mo avg), no referrals needed, partial out-of-network coverage. Choose HMO for savings, PPO for flexibility.

6. How do I know if I qualify for ACA health insurance subsidies in 2026?

Individual income between $15,650 and $62,600 likely qualifies for federal premium tax credits. Family of 4 up to ~$128,600 may also qualify. Use the official subsidy calculator at healthcare.gov to get your exact number.

7. What is a health insurance deductible?

The deductible is the amount you pay out-of-pocket before insurance begins sharing costs. Bronze plans average ~$7,000 deductible. Gold plans average ~$1,500. A lower deductible means higher monthly premiums.

8. Can I enroll in a health insurance plan outside of open enrollment?

Only if you have a qualifying life event — job loss, marriage, divorce, birth of a child, or moving states. This triggers a Special Enrollment Period (SEP) of 60 days. Otherwise, wait for November 1 open enrollment.

9. What is an HSA and which health insurance plans qualify?

An HSA (Health Savings Account) lets you save pre-tax dollars for medical expenses. In 2026, all Bronze and Catastrophic marketplace plans are now HSA-eligible. Contribution limits: $4,400 (individual), $8,750 (family).

10. What is the 2026 out-of-pocket maximum for health insurance plans?

For ACA-compliant plans in 2026, the out-of-pocket maximum is $9,200 for individuals and $18,400 for families. This is the most you will ever pay in a calendar year, regardless of your plan tier.

11. Is employer health insurance better than an ACA marketplace plan?

Employer plans are typically cheaper because your employer covers 50–70% of the premium. However, if your employer’s plan is unaffordable (costs more than ~9.02% of household income), you may qualify for marketplace subsidies instead. Always compare both options before assuming your employer plan is the better deal.

Expert Panel Statement

This article was reviewed and validated by the FinanceAuthorityHub.com International Expert Panel — 30 credentialed financial professionals across the United States, United Kingdom, Canada, and Australia. All data points are sourced from government agencies, peer-reviewed research, and verified marketplace filings as of February 2026.

⚠️ Disclaimer: This article is for educational and informational purposes only. It does not constitute financial, tax, or insurance advice. Health insurance eligibility, costs, and subsidy amounts vary by individual circumstances, income, state of residence, and plan year. Always consult a licensed insurance professional or certified navigator before making coverage decisions. Premium data referenced from CMS marketplace filings, ValuePenguin analysis, KFF research, and IRS publications — all current as of February 2026.

Explore more at FinanceAuthorityHub.com:

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.