Retirement Planning Your 30s: 2026 Expert Guide

Your 30s are the most powerful decade for building retirement wealth. Get exact benchmarks, account strategies, and catch-up frameworks backed by Federal Reserve data and 21 CFPs.

In This Article

Your 30s represent the most powerful decade for building retirement wealth—yet 73% of Americans in this age group feel behind on savings. Here’s the truth: whether you’re starting from zero or playing catch-up, the strategies you implement now will determine your financial freedom for the next 40+ years. This guide provides the exact framework, benchmarks, and action steps backed by Federal Reserve data and certified financial planners.

Why Your 30s Are the Most Critical Decade for Retirement Planning

The average 30-something faces a perfect storm: $30,000+ in student debt, rising housing costs, and the pressure to fund retirement simultaneously. Traditional advice to “just save 15%” ignores the competing financial realities of mortgages, childcare, and emergency funds.

But here’s what makes your 30s uniquely powerful: you still have 30-35 years until retirement, giving your money three decades of compound growth potential. A dollar invested at 30 becomes approximately $7.61 by age 65 (assuming 7% annual returns), compared to just $4.32 if you wait until 40. Understanding what compound interest really means transforms how you view every contribution.

The Federal Reserve’s latest Survey of Consumer Finances reveals the median retirement savings for Americans in their 30s sits between $18,880 and $45,000—far below recommended targets. This creates both a wake-up call and an opportunity: you’re not alone if you’re behind, and catching up is mathematically achievable.

In 2026, you’re also navigating updated IRS contribution limits, a post-Tax Cuts and Jobs Act landscape, and an interest rate environment that affects everything from high-yield savings to mortgage rates. This guide addresses these current realities with actionable strategies, not generic platitudes.

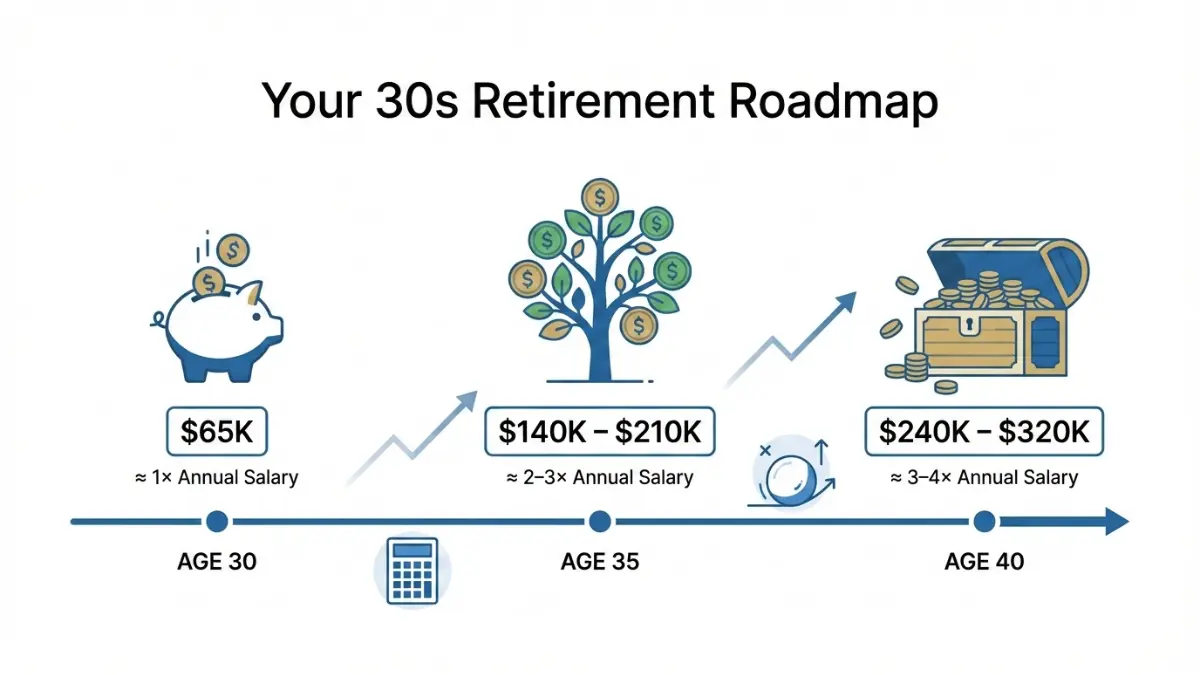

Retirement Savings Benchmarks: Where You Should Be

Financial planners use salary multipliers as guideposts. According to comprehensive retirement savings by age research, here’s where you should aim:

Age 30 Target: 1× your annual salary

If you earn $65,000, aim for $65,000 in retirement accounts by 30.

Age 35 Target: 2-3× your annual salary

At $70,000 income, target $140,000-$210,000 saved.

Age 40 Target: 3-4× your annual salary

Earning $80,000 means aiming for $240,000-$320,000 by decade’s end.

These benchmarks assume you started saving in your early 20s at 10-15% of income. But what if you’re starting later or behind schedule?

The Catch-Up Framework

The Bureau of Labor Statistics reports the median salary for 25-34 year-olds is approximately $58,500. If you’re 32 with $10,000 saved (below the 1× target), here’s your catch-up math:

Contributing $600/month from age 32-40 with 7% average returns yields approximately $75,000—bringing your total to $85,000, putting you on track for the 3× multiplier by 40. The key isn’t perfection; it’s consistent progress.

Use tools like our mortgage affordability calculator when balancing home buying with retirement contributions—competing goals require strategic prioritization, not choosing one over the other entirely.

Which Retirement Accounts Should You Use? Complete 2026 Comparison

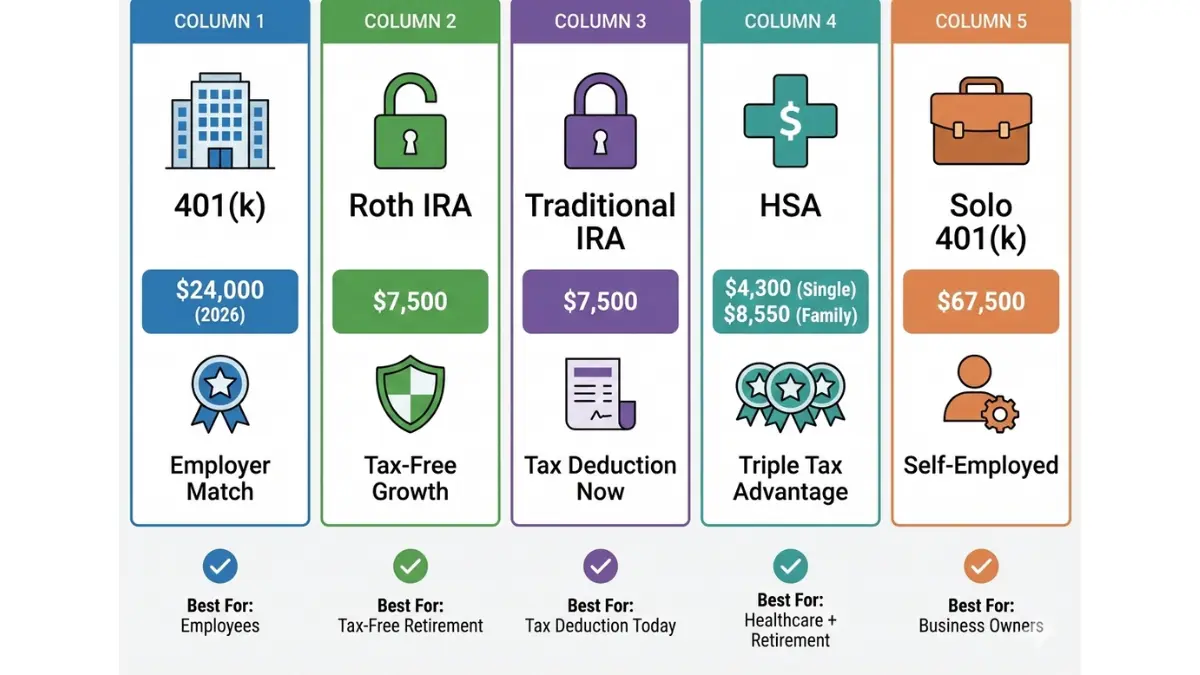

401(k) Plans: Your Foundation

2026 Contribution Limit: $24,000 (up from $23,500 in 2025)

Key Advantage: Employer match—typically 3-6% of salary

Tax Treatment: Traditional contributions reduce taxable income now; you pay taxes in retirement

Start here, especially if your employer offers matching. A 6% match on $70,000 salary equals $4,200 in free money annually. Not contributing enough to capture the full match means leaving money on the table. Our 401(k) explained guide breaks down exactly how employer matching works.

Best for: Anyone with employer access, particularly those in the 22-24% tax bracket who benefit from immediate deductions.

Roth IRA vs. Traditional IRA: The 2026 Decision

2026 Contribution Limit: $7,500 for both types

Income Limits (Roth): Phase-out begins at $161,000 (single) / $240,000 (married filing jointly)

The fundamental difference: Traditional IRAs provide tax deductions now but you pay taxes on withdrawals in retirement. Roth IRAs offer no deduction now but provide completely tax-free withdrawals after age 59½.

For most 30-somethings, Roth IRAs represent superior value. You’re likely in a lower tax bracket now than you’ll be at retirement, making tax-free growth incredibly valuable over 30+ years. A $7,500 annual Roth IRA contribution from age 30-60 at 7% returns grows to approximately $748,000—completely tax-free.

The IRS provides complete IRA contribution rules that update annually.

Health Savings Accounts (HSA): The Triple Tax Advantage

2026 Contribution Limit: $4,300 (individual) / $8,550 (family)

Unique Benefit: Tax-deductible contributions, tax-free growth, tax-free withdrawals for qualified medical expenses

HSAs are the most tax-advantaged accounts available—better than 401(k)s or IRAs because they offer three tax benefits instead of two. After age 65, you can withdraw for non-medical purposes penalty-free (though you’ll pay income tax, similar to traditional IRAs).

Best for: Anyone with a high-deductible health plan who can afford to save beyond emergency funds.

Solo 401(k) & SEP-IRA: For Freelancers

If you’re self-employed or have side income, these accounts offer significantly higher contribution limits. A Solo 401(k) allows up to $24,000 in employee contributions plus an additional 20% of net self-employment income as employer contributions, with a combined limit of $67,500 in 2026.

Best for: Freelancers, gig workers, side hustlers with 1099 income seeking higher contribution limits than standard IRAs.

Account Prioritization Strategy

Step 1: Contribute to 401(k) up to employer match

Step 2: Max out Roth IRA ($7,500)

Step 3: Return to 401(k), increase toward $24,000 limit

Step 4: If eligible, contribute to HSA

Step 5: Consider taxable brokerage accounts

The 401(k) vs IRA prioritization guide provides detailed scenarios for different income levels and situations.

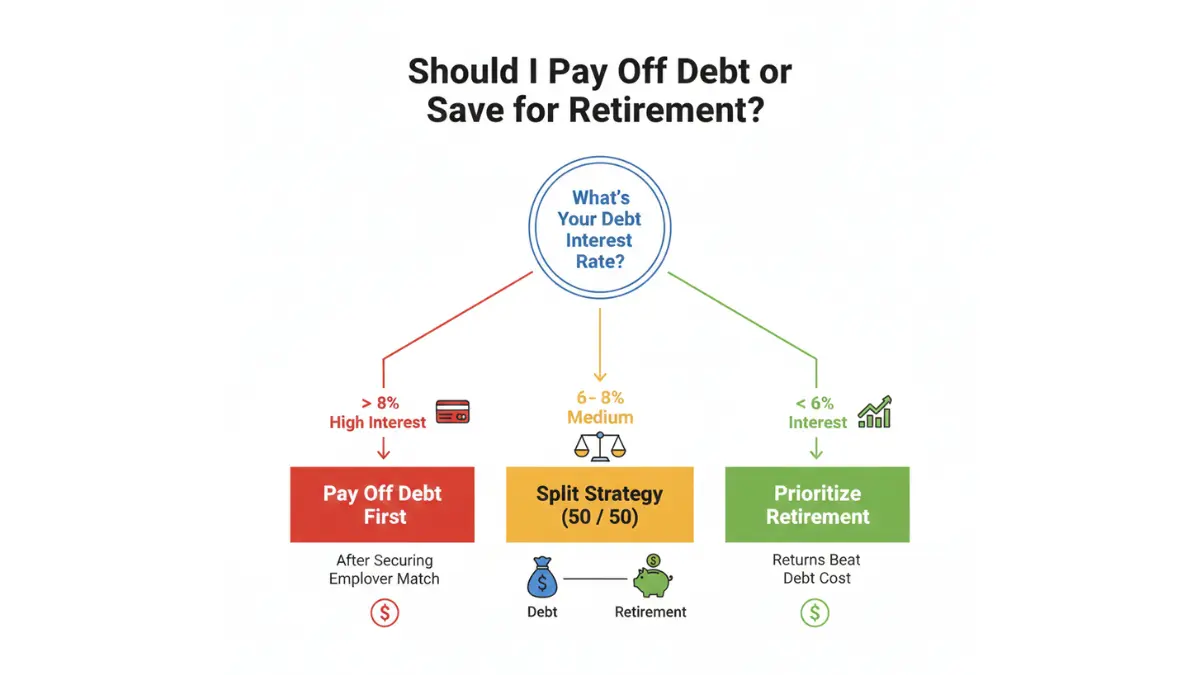

Should I Pay Off Debt or Save for Retirement?

This represents the most common dilemma for 30-somethings. The mathematical answer depends on interest rates, but behavioral factors matter too.

The Interest Rate Decision Matrix

High-Interest Debt (>8%): Pay off aggressively after securing employer match. Credit card debt at 18-24% APR mathematically beats any investment return expectation.

Medium-Interest Debt (6-8%): Split strategy—contribute enough to get full employer match, then divide remaining funds 50/50 between debt and retirement.

Low-Interest Debt (<6%): Prioritize retirement. With expected 7-10% investment returns, the math favors investing. Many mortgages and student loans fall into this category.

Student loans averaging 5% interest create a genuine dilemma. Running the numbers: $40,000 in student debt at 5% costs $2,000/year in interest. That same $2,000 invested annually at 7% returns grows to approximately $189,000 over 30 years. The opportunity cost is significant.

However, behavioral finance matters. If debt stress prevents sleep or causes significant anxiety, the psychological relief of debt freedom has real value. As explored in our debt payoff strategies guide, combining mathematical optimization with emotional wellbeing produces the best long-term outcomes.

The CFPB provides resources for understanding student loan options and repayment strategies that can inform your decision.

7-Step Implementation Roadmap

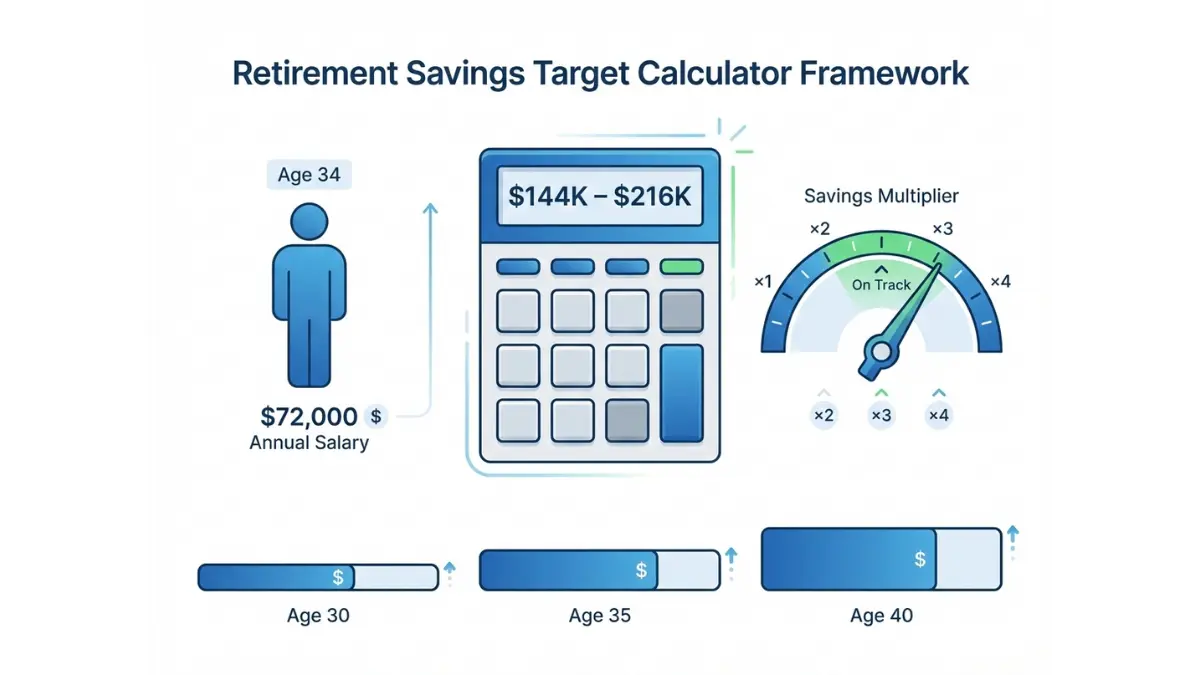

Step 1: Calculate Your Specific Target (15 minutes)

Determine where you should be based on age and income using the multipliers above. If you’re 34 earning $72,000, your target is $144,000-$216,000 (2-3× salary). Calculate your gap, then determine monthly contributions needed to close it.

Step 2: Audit Current Accounts (20 minutes)

List all retirement accounts—old 401(k)s from previous employers, IRAs, any existing savings. Calculate your current total. Many people discover “forgotten” accounts worth thousands.

Step 3: Open or Optimize Accounts (30 minutes)

If you lack a 401(k), start with a Roth IRA at a low-cost provider. If you have a 401(k), verify you’re capturing the full employer match. Best investment apps for beginners offers vetted platforms for opening retirement accounts.

Step 4: Automate Contributions (30 minutes)

Set up automatic transfers so contributions happen before you see the money. Automation removes willpower from the equation. If saving $500/month feels impossible, start with $200 and increase by $50 every three months.

Step 5: Choose Investments (45 minutes)

Within your accounts, select actual investments. Target-date funds (like “Target 2055”) automatically adjust risk as you age. Low-cost index funds tracking the S&P 500 offer simple diversification. Our guide on index funds vs mutual funds explains the cost differences.

Step 6: Build Emergency Buffer (Ongoing)

Before aggressively maximizing retirement, establish 3-6 months expenses in a separate emergency fund. This prevents retirement account raids during unexpected expenses.

Step 7: Annual Increase Strategy (Once yearly)

When you receive a raise, immediately increase retirement contributions by half the raise amount. A 4% raise means increasing contributions by 2%, leaving 2% for lifestyle improvement. This painless escalation strategy compounds dramatically over decades.

Security, Compliance & Realistic Expectations

Account Protections

Retirement accounts enjoy significant regulatory protection. SIPC insurance protects brokerage accounts up to $500,000 against firm failure (not market losses). Bank-held retirement funds receive FDIC insurance up to $250,000. The Securities and Exchange Commission provides investor protection resources and fraud prevention guidance.

Understanding Returns

Historical S&P 500 returns average 10% annually, but this includes significant volatility. Conservative planning uses 7% real returns (after inflation). Some years deliver 25% gains; others show 20% losses. What matters is time in the market—30-year periods have never produced negative returns historically.

Tax Considerations

Required Minimum Distributions (RMDs) begin at age 73 for traditional 401(k)s and IRAs, forcing taxable withdrawals whether you need money or not. Roth accounts have no RMDs, providing greater flexibility. Early withdrawals before 59½ typically incur 10% penalties plus income tax, with limited exceptions for first-home purchases and education expenses.

Behavioral Reality

Retirement accounts provide the framework—your behavior determines success. The greatest risk isn’t market crashes; it’s stopping contributions during downturns or withdrawing early for non-emergencies. Consistent contributions through market cycles, disciplined spending, and avoiding lifestyle inflation matter more than perfect account selection.

Frequently Asked Questions

1. How much should I have saved by age 35?

Target 2-3 times your annual salary. At $70,000 income, aim for $140,000-$210,000. The Federal Reserve reports median savings of $18,880-$45,000 for 30-somethings, indicating most people are behind benchmarks but catching up remains achievable.

2. Should I max my 401(k) or Roth IRA first?

Contribute enough to your 401(k) to capture full employer match, then max your Roth IRA ($7,500), then return to maximizing your 401(k). This prioritizes free money first, then tax-free growth.

3. Is it too late to start retirement planning at 35?

No. Starting at 35 with $600/month contributions yields approximately $450,000 by 65 (at 7% returns). That’s enough to generate $18,000/year in retirement using the 4% withdrawal rule, supplementing Social Security benefits.

4. Can I withdraw Roth IRA contributions early?

Yes—Roth IRA contributions (not earnings) can be withdrawn anytime tax and penalty-free. However, this should be a last resort as it permanently reduces retirement savings and eliminates years of compound growth.

5. What if I lose my job? What happens to my 401(k)?

You have four options: leave it with your former employer, roll it into an IRA, roll it into your new employer’s plan, or cash out (strongly discouraged due to taxes and penalties). Rolling to an IRA typically provides the most investment options and lowest fees.

6. Should I pay off my mortgage or save for retirement?

Most mortgages have interest rates below 6%, making retirement savings mathematically superior (expected 7-10% returns). However, consider your age—those 10+ years from retirement might prioritize mortgage payoff for peace of mind.

7. How much will I need total to retire comfortably?

Financial planners suggest 10-12× your final salary. Retiring at $100,000 annual salary requires $1-1.2 million. The 4% withdrawal rule suggests this generates $40,000-$48,000 annually, supplementing Social Security for total retirement income.

8. What’s the penalty for early 401(k) withdrawal?

Generally 10% penalty plus income tax on the full amount. A $20,000 withdrawal in the 22% bracket costs $2,000 penalty plus $4,400 tax—$6,400 lost to penalties and taxes, leaving just $13,600.

9. Can I have both a 401(k) and IRA?

Yes. You can contribute up to $24,000 to a 401(k) and $7,500 to an IRA in 2026, totaling $31,500 annually. Income limits affect IRA tax deductions but not your ability to contribute.

10. Should I work with a financial advisor?

For straightforward situations (standard 401(k) and IRA), DIY management works fine with education. Complex situations—high income, multiple accounts, tax optimization, estate planning—benefit from fee-only CFP® advisors who don’t earn commissions.

11. What if the market crashes right before I retire?

Mitigate sequence-of-returns risk by shifting toward bonds and cash 5-10 years before retirement. Keep 2-3 years of expenses in safe investments so you’re not forced to sell stocks during downturns.

12. How do I choose investments within my retirement accounts?

Target-date funds automatically adjust risk based on retirement date—simple and effective for most investors. Low-cost index funds tracking the total stock market offer broader diversification. Avoid individual stock picking and high-fee actively managed funds.

Important Legal Disclaimer

⚠️ IMPORTANT DISCLAIMER: The information provided in this article is for educational and informational purposes only and does not constitute professional financial, investment, tax, or legal advice. financeauthorityhub.com and its authors are not licensed financial advisors, certified public accountants, or attorneys.

Before making any financial decisions regarding retirement planning, investment allocation, tax strategies, or debt management, consult with a qualified financial advisor, tax professional, or attorney licensed in your jurisdiction.

Key Disclaimers:

• No Guaranteed Returns: Past investment performance does not guarantee future results. All investments carry inherent risk, including potential loss of principal. Historical 7-10% average stock market returns are not guaranteed for future periods.

• Individual Circumstances Vary: Retirement strategies must be customized to your income, debt load, goals, risk tolerance, and timeline. Generic guidance cannot replace personalized advice from qualified professionals.

• Tax Implications: Retirement account rules, contribution limits, and tax treatments are subject to change. Verify current IRS guidance at IRS.gov/retirement-plans and consult tax professionals for your specific situation.

• Market Risk: Investment values fluctuate. Market downturns can result in significant temporary or permanent losses. Diversification and asset allocation do not guarantee profit or protect against loss.

• Data Accuracy: All financial figures, contribution limits, and tax information are accurate as of January 2026 but may become outdated as regulations change.

• No Liability: financeauthorityhub.com assumes no liability for financial decisions made based on this content. Users rely on this information at their own risk.

Affiliate Disclosure: Some links may represent affiliate relationships. See our Privacy Policy and Terms of Service for complete disclosures.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.