The 1982 Law Behind Tax-Free Structured Settlements

Structured settlement payments escape federal income tax because of one 1982 law—and a later rule decides who pays the 40% tax when you sell.

In This Article

The reason an injury settlement arrives as a stream of tax-free checks instead of one taxable lump sum traces back to a single federal law passed in 1982.

That statute turned a clever insurance workaround into a protected, tax-advantaged system that pays out billions of dollars to injured Americans every year.

This guide covers the structured settlement law history from its 1970s origins through the 2002 reforms that now shield people who sell their future payments.

You will learn what the 1982 law actually changed, why the payments escape federal income tax, and how to read a buyout offer without surrendering thousands of dollars in value.

The short version is simple. One law made the income tax-free, and a second law made selling it safer—everything else builds on those two pillars.

ℹ️ Disclaimer: This article explains structured settlement tax and transfer rules for educational purposes. How injury settlements are taxed under the Internal Revenue Code, and whether you can sell future payments, depend on your specific settlement and your state’s law—and any sale requires court approval in nearly every state. Consult a licensed attorney and a credentialed financial professional such as a CFA or CPA before keeping, modifying, or selling structured settlement payments.

What a structured settlement is and how it works

A structured settlement is a legal agreement that pays compensation from an injury claim as scheduled payments over time instead of one lump sum.

These payments are funded by an annuity that a life insurance company issues, and they are typically free of federal income tax.

How periodic payments replace a lump sum

After a personal injury, product liability, or wrongful death claim settles, the defendant’s insurer can fund a stream of periodic payments rather than writing a single check.

The schedule is fixed in advance—monthly income for life, larger sums on set future dates, or a blend—and it cannot be changed once a court approves it.

Comparing that fixed stream against other long-term income sources is easier with a tool that projects retirement income you may also be relying on.

Who funds the annuity behind the payments

The defendant or its insurer transfers the payment obligation to an assignment company through a process the tax code calls a qualified assignment.

That company owns the funding annuity and directs the payments to you, which means you do not personally own or control the underlying asset.

Because the payments are fixed, inflation quietly erodes their buying power over decades; running the numbers through an inflation impact tool shows how much a fixed $2,000 monthly payment loses in real value across 20 years.

💡 Expert Note (CFA): The detail most people overlook is ownership. You receive the payments, but the assignment company holds the annuity—so you cannot borrow against it the way you could a CD or brokerage account. That single fact is exactly why a lump-sum buyout starts to look tempting years later.

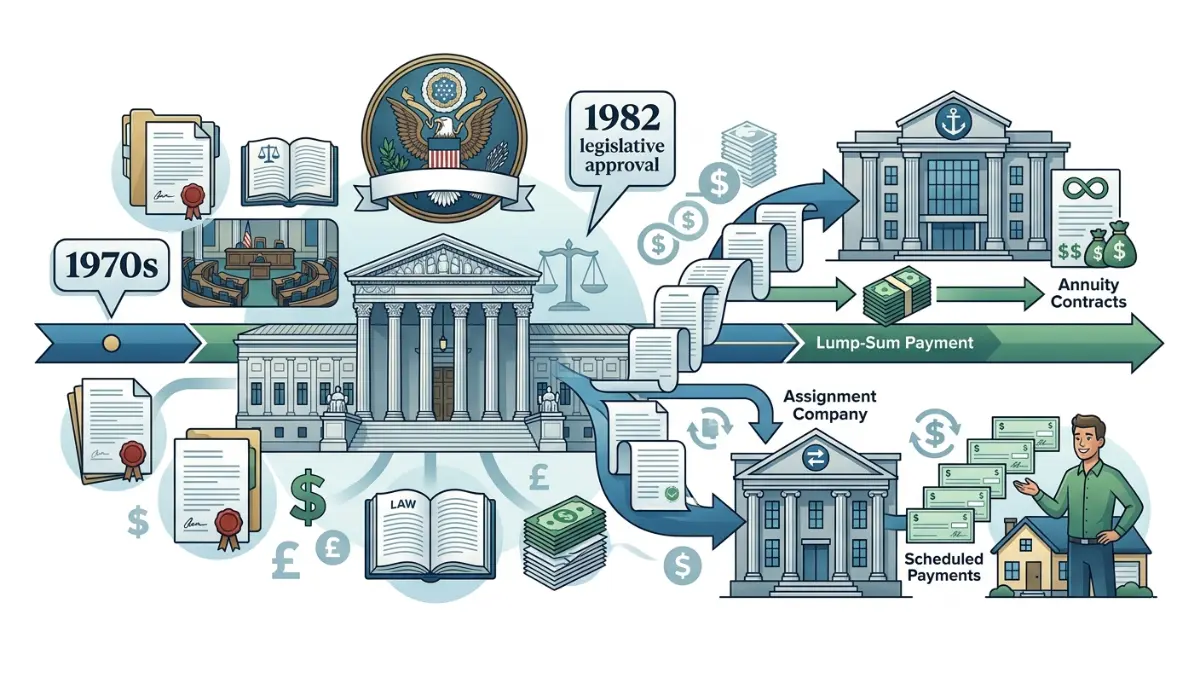

The 1982 law that created the industry

The Periodic Payment Settlement Act of 1982, also known as Public Law 97-473, is the federal law that established the tax framework for structured settlements and effectively created the modern industry.

Before it, the tax-free status of these payments rested on shaky ground—a few favorable IRS rulings and no statute behind them.

What the Periodic Payment Settlement Act of 1982 did

Structured settlements existed informally in the mid-1970s, and the IRS blessed their tax treatment in a 1979 ruling, but insurers wanted certainty written into law.

Congress delivered it in 1982 by amending the Internal Revenue Code so that Section 104(a)(2) excludes not just lump sums but periodic payments from a physical injury from gross income.

What IRC Section 130 and a qualified assignment mean

The same law added IRC Section 130, which lets a defendant hand the payment obligation to a third-party assignment company without that company owing tax on the money it receives to fund the annuity.

This qualified assignment mechanism is the plumbing that lets insurers exit a case cleanly while the injured party keeps a guaranteed, tax-free stream—and it remains the dominant funding method today.

📊 Data Point: The Periodic Payment Settlement Act of 1982 amended IRC §104(a)(2) and created IRC §130 — Source: Public Law 97-473, Internal Revenue Code.

Why structured settlement payments are tax-free

Payments from a personal physical injury or wrongful death structured settlement are tax-free because IRC Section 104(a)(2) excludes them from your gross income.

That exclusion is the single biggest financial advantage these settlements carry, but it does not cover every dollar.

What IRC Section 104(a)(2) excludes

Compensation tied to a physical injury or physical sickness—medical costs, pain and suffering, and the income replacement built into the award—reaches you completely free of federal income tax.

The guiding question is what each payment was meant to replace, and physical-injury compensation is the clearest exclusion, as laid out in the IRS guidance on how settlement and judgment payments are taxed.

What parts of a settlement are still taxable

Not everything in a settlement is shielded, and assuming otherwise can produce a surprise tax bill.

Punitive damages, interest that accrues on the award, and amounts allocated to lost wages in an employment-type claim are generally taxable as ordinary income.

| Settlement component | Taxable? |

|---|---|

| Physical injury or sickness compensation | No |

| Pain and suffering from physical injury | No |

| Punitive damages | Yes |

| Interest on the award | Yes |

| Lost wages in employment claims | Yes |

Estimating the bill on the taxable slices is simpler with an income tax estimate tool before you sit down with a professional.

If you later reinvest a taxable lump sum, future profits may be taxable too, and a capital gains tax estimate helps you plan for that ahead of time.

Selling payments and the 2002 law that protects you

You can sell your future structured settlement payments for a lump sum today, but a 2002 federal law and your state’s courts stand between you and a bad deal.

That protection exists because, in the industry’s early years, some buyers pressured injured people into trading decades of payments for pennies on the dollar.

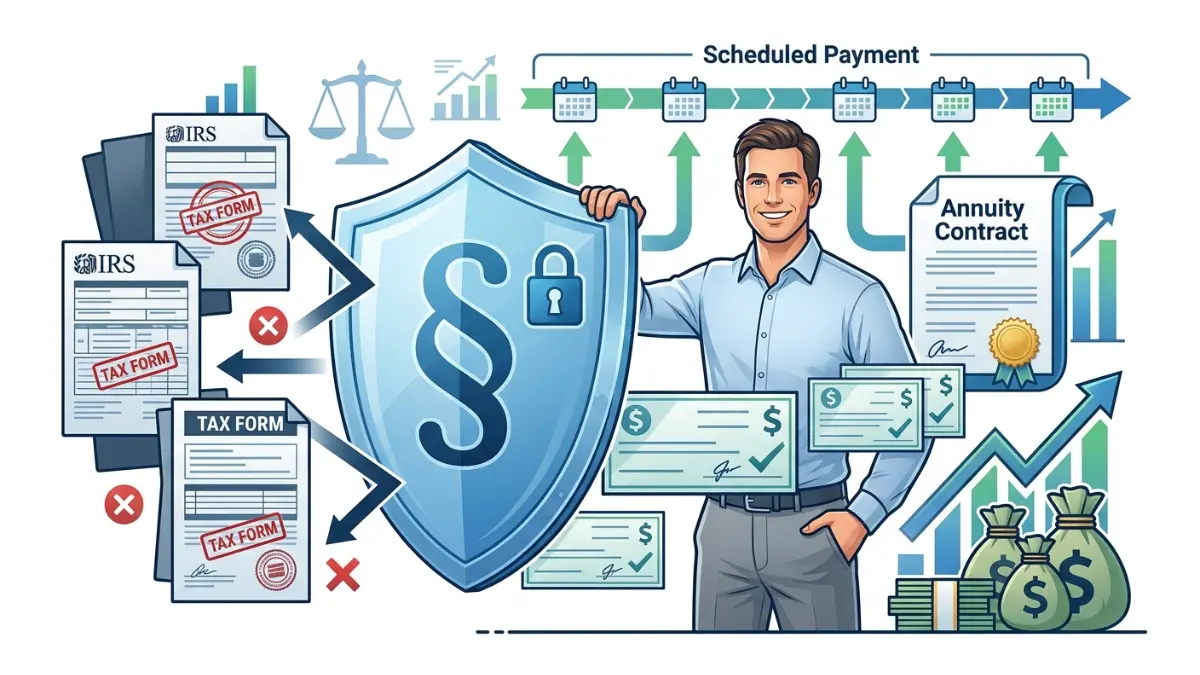

What the Structured Settlement Protection Act requires

The Structured Settlement Protection Act framework requires a judge to approve any transfer of payments through what the law calls a qualified order.

The court must find that the sale is in your best interest, which means a buyer cannot simply hand you a contract and walk away with your future income.

How the 40% excise tax under IRC Section 5891 works

Congress added IRC Section 5891 in 2002, imposing a 40% excise tax on the buyer’s profit—the factoring discount—on any transfer that lacks court approval.

The tax falls on the company buying your payments, not on you, and it disappears once a judge approves the deal, so it works as a strong incentive to route every transaction through a court.

📊 Data Point: Selling without a court-approved qualified order triggers a 40% excise tax on the buyer’s factoring discount — Source: IRC §5891, reported on IRS Form 8876.

Regulators enforce this. A CFPB enforcement action against a firm that steered consumers into bad transfers shows what happens when companies sidestep the best-interest standard.

⚠️ Warning: If a buyer tells you to skip court approval, or offers to “help you avoid” the 40% tax for a fee, treat it as a red flag and walk away. The court process is the protection, not an obstacle to get around.

Should you sell your structured settlement?

Selling makes sense in a few specific situations and is a costly mistake in many others, and the deciding factor is the discount rate baked into the offer.

A lump-sum offer is always smaller than the total of your future payments, because the buyer profits on the gap.

What the discount rate really costs you

The discount rate is the true interest rate you pay to access your money early, and offers vary widely between companies, which is why comparison matters.

Treat that rate the way you would a loan’s APR—the higher it is, the more future value you surrender. A compound interest tool shows what your payments could grow to if you keep them, while an investment return tool shows the return you would need to replace the value you sell.

The questions to ask before you sign

Run the numbers before any conversation with a buyer.

- What is the total dollar value of the payments I am selling versus the cash offered today?

- What specific, time-sensitive need does the lump sum solve that my monthly payments cannot?

- Have I collected quotes from at least three buyers to compare their discount rates side by side?

- Will losing this income affect public benefits or my monthly cash flow? A budget planning tool makes that trade-off concrete.

- Has a licensed attorney reviewed the contract before it reaches a judge?

The CFPB’s consumer guidance on giving up settlement payments for a lump sum warns that these offers can be risky and that a vague reason like “I want flexibility” rarely survives a judge’s best-interest review.

💡 Expert Note (CFA): The first number to compute is the effective annual rate hidden in the offer—not the headline cash amount. Once you express a buyout that pays roughly 55 cents on the dollar as the double-digit rate it actually represents, many “emergencies” look cheaper to solve with a debt consolidation comparison and a short repayment plan than with a permanent sale of tax-free income.

✅ Pro Tip: Price the alternative first. A personal loan, a home equity option you may already qualify for, or trimming expenses often costs far less than the lifetime discount on a settlement sale.

Frequently asked questions about structured settlement law

1. What law created structured settlements?

The Periodic Payment Settlement Act of 1982, also called Public Law 97-473, created the legal framework for the modern structured settlement industry. It amended the tax code so that periodic injury payments, not just lump sums, are excluded from federal income tax, giving insurers and injured parties the certainty earlier IRS rulings lacked.

2. Why are structured settlement payments tax-free?

Structured settlement payments are tax-free because IRC Section 104(a)(2) excludes compensation for physical injury or sickness from gross income. This covers medical costs, pain and suffering, and the income-replacement portion of the award. Punitive damages, interest, and lost-wage allocations in employment claims remain taxable as ordinary income.

3. What is a qualified assignment under IRC Section 130?

A qualified assignment, authorized by IRC Section 130, lets a defendant transfer the obligation to make structured settlement payments to a third-party assignment company. That company funds an annuity and owes no tax on the money it receives to do so. It is the dominant method used to fund structured settlements today.

4. Can you sell a structured settlement?

Yes, you can sell a structured settlement, in whole or in part, to a factoring company for a discounted lump sum. Nearly every state and federal law require a judge to approve the transfer first. You always receive less cash than the total value of the future payments you give up.

5. What is the 40% excise tax on structured settlements?

The 40% excise tax under IRC Section 5891 applies to a buyer who acquires structured settlement payments without court approval. It equals 40% of the factoring discount, which is the buyer’s profit. The tax falls on the purchasing company, not the seller, and it disappears once a judge approves the transfer.

6. Do you need court approval to sell a structured settlement?

Yes. Selling structured settlement payments requires court approval in nearly every state. A judge reviews the transfer and must find that it serves your best interest before it becomes valid. This safeguard exists to stop companies from buying decades of future payments for a small fraction of their real value.

7. What discount rate do structured settlement buyers charge?

Discount rates on a structured settlement buyout vary widely between companies and are often expressed as a cash offer rather than a percentage. Convert any offer into an effective annual rate and compare quotes from at least three buyers, because that rate determines how much lifetime value you ultimately surrender.

8. Is selling a structured settlement a good idea?

Selling a structured settlement can make sense for a specific, documented need such as a home down payment or urgent medical costs. It is usually a mistake when the income is essential to your budget or the discount is steep. Always compare the cash offer against the total payments you give up.

9. What is the Structured Settlement Protection Act?

The Structured Settlement Protection Act framework, adopted federally in 2002 and mirrored by state laws, requires court approval before any sale of structured settlement payments. A judge must issue a qualified order finding the transfer is in the seller’s best interest, protecting injured people from predatory buyout offers.

10. When did structured settlements start in the US?

Structured settlements began in the United States in the mid-1970s, when insurers started paying injury awards over time. The IRS validated their tax-free treatment in a 1979 ruling, and the Periodic Payment Settlement Act of 1982 wrote that treatment into law, launching the structured settlement industry as it exists now.

11. Are structured settlement annuities safe?

Structured settlement annuities are generally safe because they are issued by regulated life insurance companies and backed by state guaranty associations up to set limits. The payments are fixed and guaranteed, though inflation reduces their buying power over time, and the underlying annuity is owned by the assignment company rather than you.

What the 1982 law means for you today

Two laws define every structured settlement decision you will ever make. The 1982 Act made your payments tax-free, and the 2002 protections made selling them safer and court-supervised.

That history matters because it tells you the system was built to favor steady, protected income—and that walking away from it should clear a high bar.

If you are keeping your payments, model how they fit your long-term plan with a savings projection tool, or weigh them against tax-advantaged retirement options you may also hold.

If you are leaning toward a sale, gather three quotes, convert each into an effective rate, and have an attorney review the contract before a judge ever sees it.

The 1982 law gave injury victims a durable financial foundation. Protecting it is usually worth far more than any quick lump sum.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.