What a Florida Structured Settlement Sale Involves

Florida structured settlement sales need court approval, and the payout runs well below face value. See the 45–90 day process and what you keep.

In This Article

Selling a structured settlement in Florida is not a quick sale — it is a court-approved legal process built to protect you.

If a medical bill, mounting debt, or a sudden expense has you eyeing those future payments, you have probably seen ads promising fast cash. What those ads rarely explain is that a Florida judge must approve the transfer before any money changes hands.

That court step is not red tape. It exists because the people receiving these payments are often injury or disability recipients whose income was structured to last for years.

This guide walks through what actually happens: the approval steps in order, how long it realistically takes, what you receive after the discount, and the federal tax rule that quietly works in your favor.

We do not buy or sell settlements. So the numbers here are not a pitch — they are the math, the law, and the tradeoffs, laid out plainly.

ℹ️ Disclaimer: Selling or transferring structured settlement payment rights in Florida is a regulated insurance and legal transaction governed by the Florida Structured Settlement Protection Act and federal tax law. The information here is educational and reflects 2026 rules, which vary by court, county, and your individual settlement. Consult a Florida-licensed attorney and an independent tax or financial professional before agreeing to any transfer.

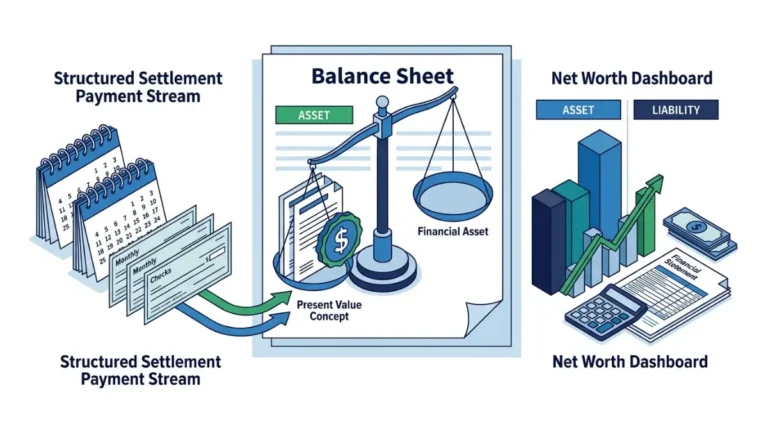

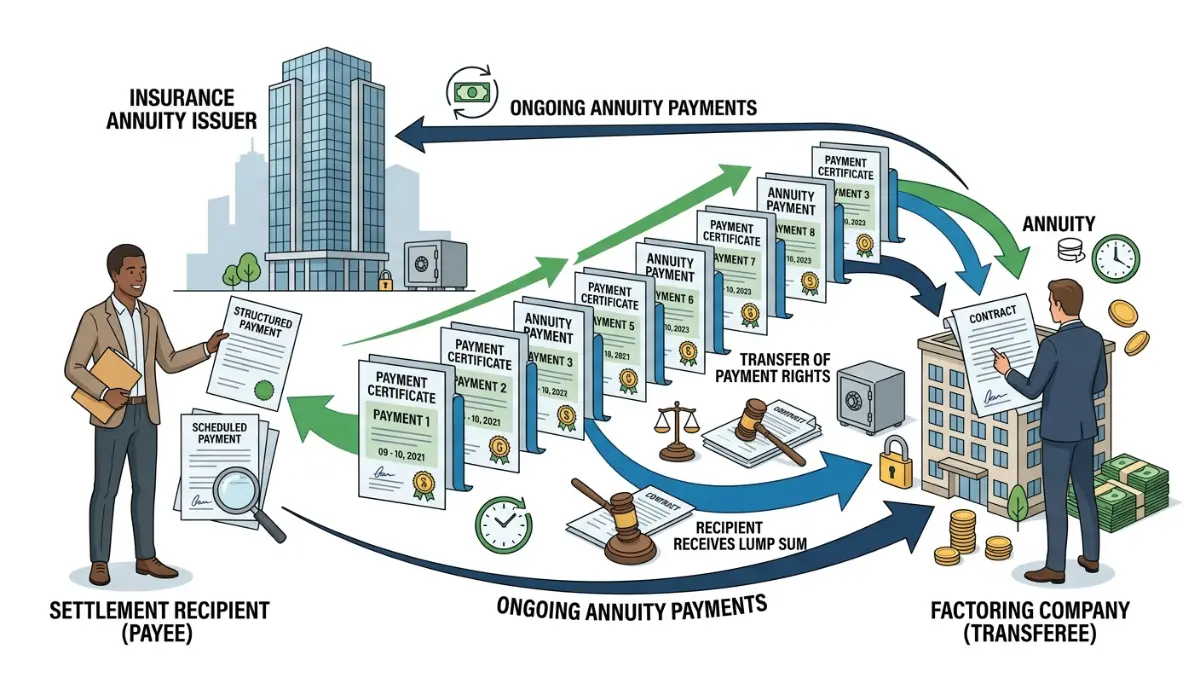

What selling a structured settlement in Florida really means

When you sell, you are not cashing out a savings account — you are transferring the right to your future payments to a company in exchange for a smaller amount today.

Who is involved: payee, transferee, and the annuity issuer

You are the payee — the person entitled to the periodic payments.

The buyer is the transferee, almost always a factoring company that purchases those payments at a discount. A separate insurance company funds the original settlement and keeps paying — just to the buyer instead of you for whatever you sold.

That structure is why a sale is irreversible once a judge signs off. You are handing over a contractual income stream, not borrowing against it.

Why a judge must approve it

Florida requires court approval under the Florida Structured Settlement Protection Act, codified at Florida Statutes section 626.99296.

The law’s stated purpose is to protect recipients, because many settlements come from personal injury, workers’ compensation, or wrongful death cases and were designed to replace income for years.

A fixed payment also loses buying power over time, so it helps to estimate how inflation erodes a fixed payment stream before deciding anything.

And if those payments were meant to carry you long term, it is worth checking how that income fits a full retirement plan rather than treating it as idle cash.

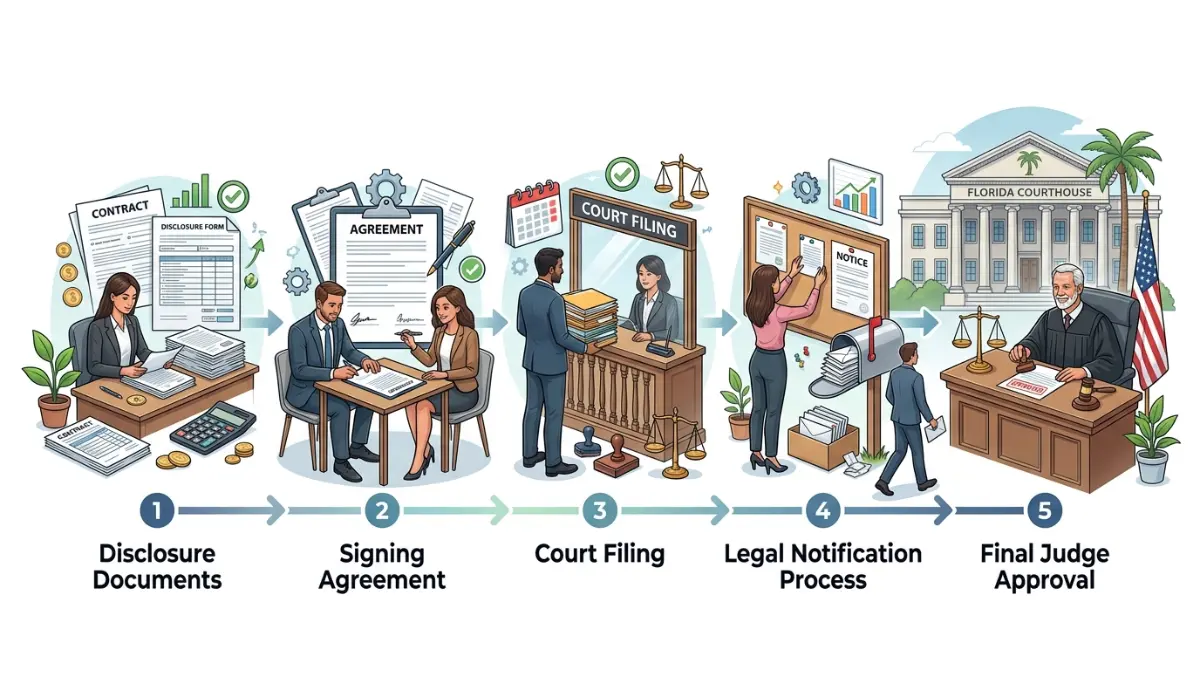

The Florida court approval steps, in order

Selling a structured settlement in Florida follows five steps set out in state law, and a judge signs the final order.

The five steps from disclosure to signed order

- Receive a written disclosure statement at least 10 days before you sign, showing the payments being sold, their present value, the lump sum offered, all fees, and the effective discount rate.

- Sign the transfer agreement with the factoring company once you understand those terms.

- The buyer files an application in the circuit court of the Florida county where you are domiciled.

- The buyer gives notice to all interested parties — including the annuity issuer and, where relevant, dependents — at least 20 days before the hearing.

- You attend the hearing, where the judge applies the best-interest test and, if satisfied, signs the order authorizing the transfer.

Section 626.99296 sets each of these requirements, and skipping any one of them makes the transfer legally ineffective.

Do you have to appear in court?

In most Florida transfers, yes — the payee is expected to attend, often briefly, so the judge can confirm you understand the deal.

Some counties allow appearance by phone or video, but plan on taking part.

✅ Pro Tip: Bring the disclosure statement and a short list of exactly what the money is for. Judges weigh whether a sale meets a real, documented need, and a clear answer moves your hearing along.

How long it takes in Florida

In Florida, a structured settlement transfer usually takes about 45 to 90 days from the court application to a signed order, and parts of it cannot be rushed.

| Stage | Typical time | What drives it |

|---|---|---|

| Disclosure and signing | A few days to 2 weeks | Your review of the terms |

| Filing the application | About 1 week | Buyer prepares court paperwork |

| Notice to interested parties | 20+ days | Statutory minimum before the hearing |

| Hearing and signed order | Varies by county | Court docket scheduling |

| Funding after approval | 1 to 3 weeks | Processing and order entry |

Timeline reflects the procedural requirements of Florida Statutes section 626.99296; court scheduling varies by county.

Typical timeline: 45 to 90 days

The biggest fixed delay is the 20-day notice the buyer must give interested parties before the hearing. That window is a legal floor, not a target a fast-moving company can shrink.

What slows a transfer down

A crowded county circuit court docket can add weeks to the hearing date.

An objection from an interested party, or missing paperwork, can also push the hearing later.

⚠️ Warning: “Cash now” ads usually describe a cash advance against a pending transfer, not the court timeline. Those advances carry their own costs, and you still need the judge’s approval before the full sale closes.

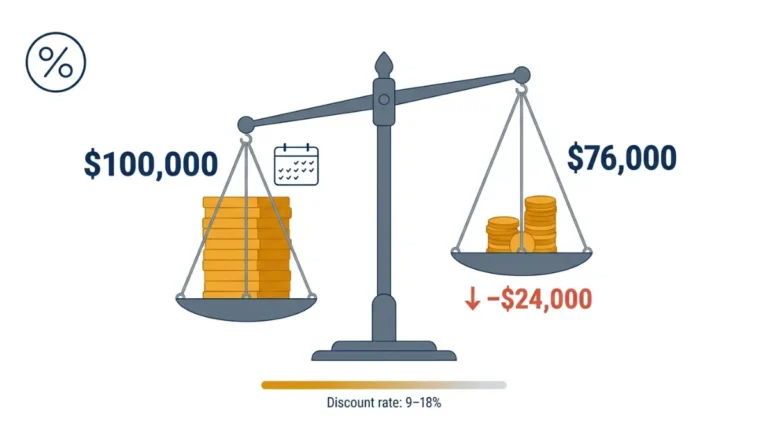

What you’ll actually receive, and the discount

The discount rate is the percentage a factoring company uses to shrink your future payments down to a smaller lump sum you can take today.

The amount you are offered is the present value of those payments — what they are worth now, not their full face total.

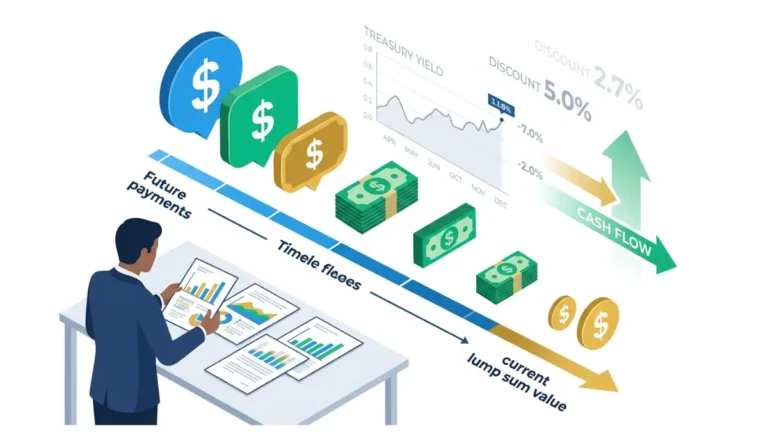

📊 Data Point: The IRS Section 7520 rate, used to value annuity and future-payment interests, is 5.0% for June 2026 — Source: IRS, June 2026.

Factoring companies apply their own, higher discount rate on top of that benchmark, so a real offer usually lands well below the present value the federal valuation rate would suggest.

Federal regulators have warned for years that these lump sums come in far below the value of the payments, with commissions and fees that can reach 7% or more, as laid out in a joint regulator alert on selling income streams.

Consider a payee owed $50,000 across the next 10 years. After a double-digit discount rate and fees, a typical offer might land near $30,000 to $35,000 in cash — a gap of $15,000 or more.

Before accepting any figure, it helps to model what a lump sum might grow to if invested and to see how steady payments compound over time. You can also compare the return on keeping versus cashing out.

💡 Expert Note (CFA): In my work with clients weighing a buyout, the number that flips the decision is rarely the headline lump sum — it is the effective annual cost of the discount. On many offers I have reviewed, that cost runs in the low double digits, a rate you would never knowingly accept on a loan.

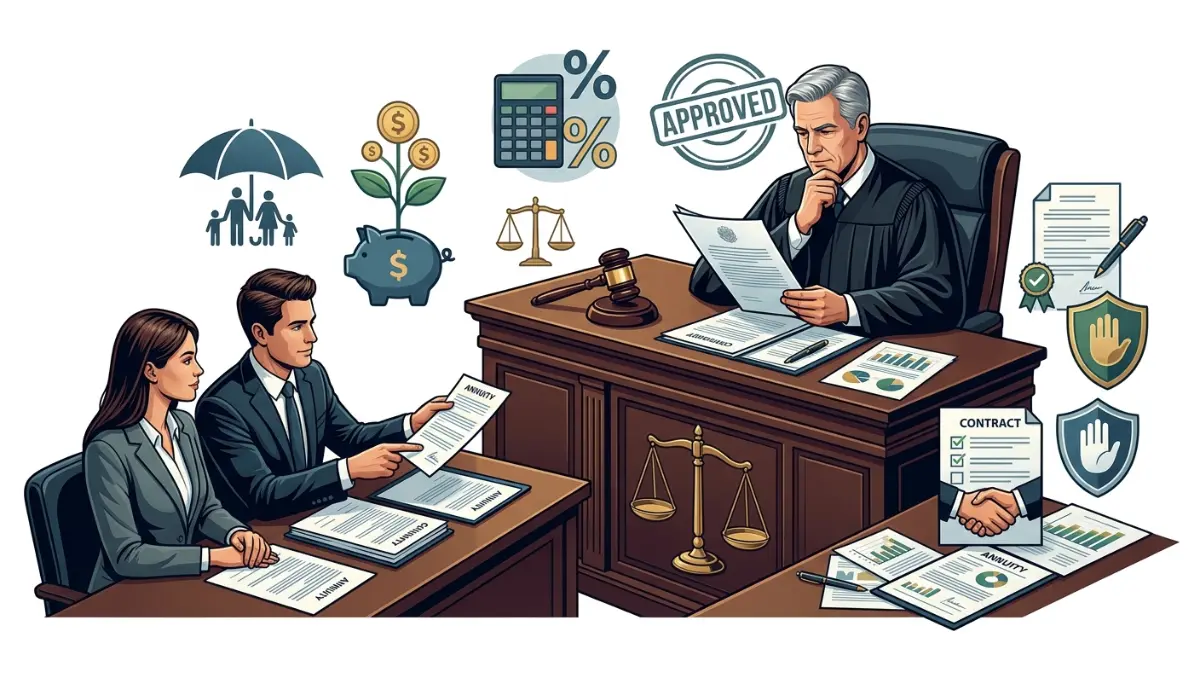

The best-interest test, red flags, and the 40% tax rule

Before signing the order, a Florida judge has to decide the sale is actually in your best interest — and one federal tax rule makes that approval matter even more.

What “best interest of the payee” means

Under Florida law, the judge weighs your financial welfare, the support of any dependents, your reason for selling, and whether you understand the terms.

The judge can deny the transfer, attach conditions, or approve it. A denial is not rare when the stated need looks thin or the discount looks predatory.

📊 Data Point: Federal law imposes a 40% excise tax on the discount in a structured settlement factoring transaction — but it does not apply when the transfer is approved in advance by a court “qualified order” — Source: IRS, Internal Revenue Code section 5891.

That is why the Florida court order is not a formality. It is also what keeps a 40-percent federal tax off your deal, as explained in the IRS guidance on the factoring excise tax, so the signed qualified order protects both sides of the transaction.

Red flags and safer alternatives

The Consumer Financial Protection Bureau has penalized companies for steering sellers toward “independent” advisors the buyer secretly paid, detailed in the CFPB’s action against a structured settlement buyer.

Regulators also publish a plain checklist of what to weigh before giving up settlement payments.

If the real goal is clearing debt, the math often favors alternatives over a steep discount. You can weigh a debt consolidation plan instead, map a payoff timeline for credit card balances, or compare the true cost of a short-term loan.

For a decision this large and this permanent, a Florida-licensed attorney and an independent tax professional are worth the consultation fee before you sign anything.

Frequently asked questions

Quick answers to what Florida payees ask most before selling.

1. Can you sell a structured settlement in Florida?

Yes. You can sell some or all of your structured settlement payments in Florida, but only with court approval. A judge must find the sale is in your best interest before any factoring company can legally buy your future payments and pay you a discounted lump sum.

2. Does selling a structured settlement require court approval in Florida?

Always. Florida law makes a structured settlement transfer ineffective without a judge’s approval. The court reviews the deal, the discount, and your reasons, then approves, denies, or conditions it. No legitimate buyer can complete a Florida purchase without that signed court order.

3. How long does the Florida court approval process take?

Most Florida structured settlement transfers take about 45 to 90 days from the court application to a signed order. A required 20-day notice period before the hearing sets the floor, and a busy county court docket can push the timeline longer than three months.

4. How much will I get if I sell my structured settlement?

Less than the total of your future payments. A structured settlement buyer applies a discount rate, so a lump sum often lands well below face value — sometimes 50 to 70 cents on the dollar after fees, depending on timing, payment type, and the offer itself.

5. What is the “best interest” standard a Florida judge uses?

It is the legal test a judge applies before approving a structured settlement transfer. The judge weighs your financial welfare, the support of any dependents, your reason for selling, and whether you understand the terms and the discount you are agreeing to accept.

6. Do I have to pay taxes when I sell my structured settlement?

Usually the seller owes no income tax on a qualifying injury structured settlement, and a court-approved transfer avoids the 40% federal excise tax that would otherwise apply to the buyer’s discount. Outcomes depend on how your original settlement was structured.

7. Can I sell only part of my structured settlement?

Yes. Many payees sell only a portion of a structured settlement — a few years of payments, or part of a future lump sum — and keep the rest. Partial sales still need court approval, and they preserve some long-term income for you.

8. Do I need a lawyer to sell a structured settlement in Florida?

A lawyer is not legally required, but it is wise. Florida encourages payees to get independent professional advice before a structured settlement transfer, and the judge will ask whether you received it. Independent counsel helps you read the discount and the terms clearly.

9. What is a disclosure statement and when do I get it?

It is a written summary the buyer must give you before you sign a structured settlement transfer. It shows the payments being sold, their present value, the lump sum offered, all fees, and the effective discount rate — typically at least 10 days before signing.

10. Can a Florida judge deny my structured settlement transfer?

Yes. A Florida judge can reject a structured settlement transfer when the sale does not serve your best interest — for example, if the discount is steep, the stated need is weak, or dependents would be harmed. The judge may also approve it with conditions.

11. What are the warning signs of a bad structured settlement buyer?

Watch for pressure to sign quickly, vague or shifting fee disclosure, and an “independent” advisor the buyer actually pays. A trustworthy structured settlement company explains the discount plainly, encourages outside advice, and never rushes you toward a court date you do not understand.

Before you sign: your next step

A structured settlement sale is permanent, and the court process exists to confirm it is the right call — not to slow you down for its own sake.

If the pressure is short-term, look at the cheaper paths first. You can build a monthly budget around your current payments or project how an emergency fund could grow before trading years of guaranteed income for a discounted check.

If selling still makes sense, get independent advice, read every line of the disclosure, and let the judge’s best-interest review work in your favor.

The lump sum will always look bigger than the payments feel. The math, and the law, are there to help you see the real difference.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.