What 20 Years of Inflation Costs a Structured Settlement

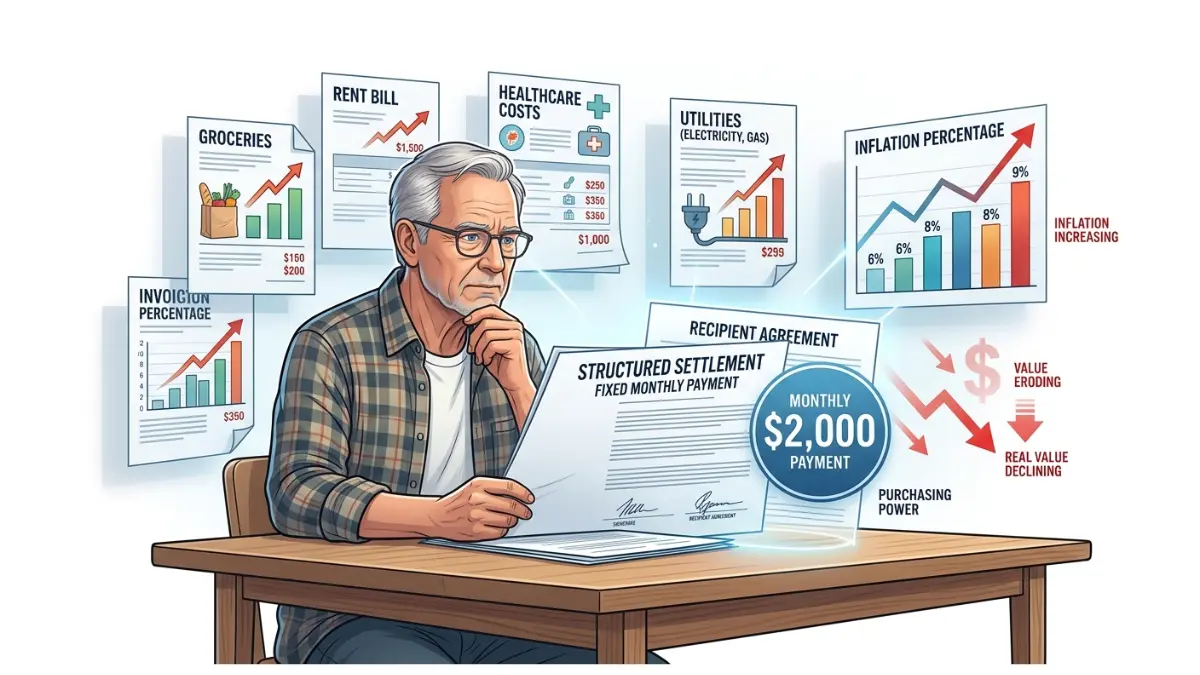

Structured settlement inflation is silently erasing your purchasing power — a $2,000 monthly payment started in 2006 is now worth just $1,126.

In This Article

Why your structured settlement is losing value right now

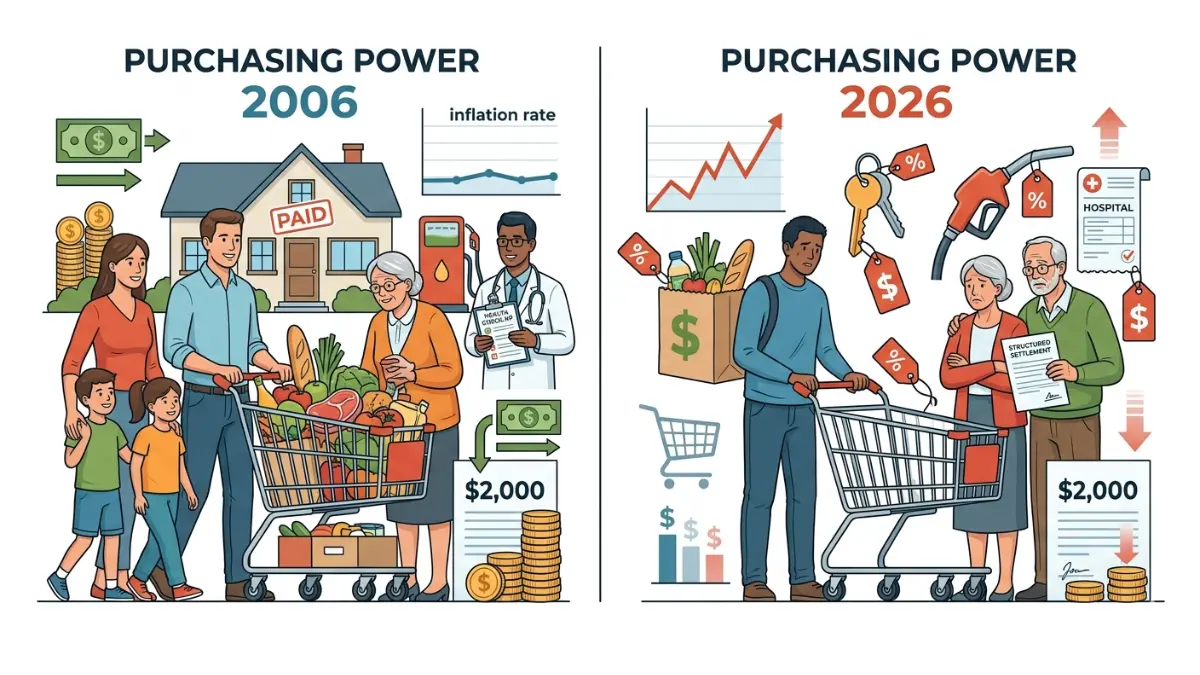

A $2,000 monthly structured settlement payment originated in 2006 delivers approximately $1,126 of real purchasing power in 2026 — a loss of $874 every single month.

That erosion does not appear on any statement, and no one calls to tell you about it.

The fixed-payment trap no one explains at settlement signing

Structured settlements are designed to provide financial security through a stream of guaranteed periodic payments, funded through a qualified annuity purchased at the time of your settlement.

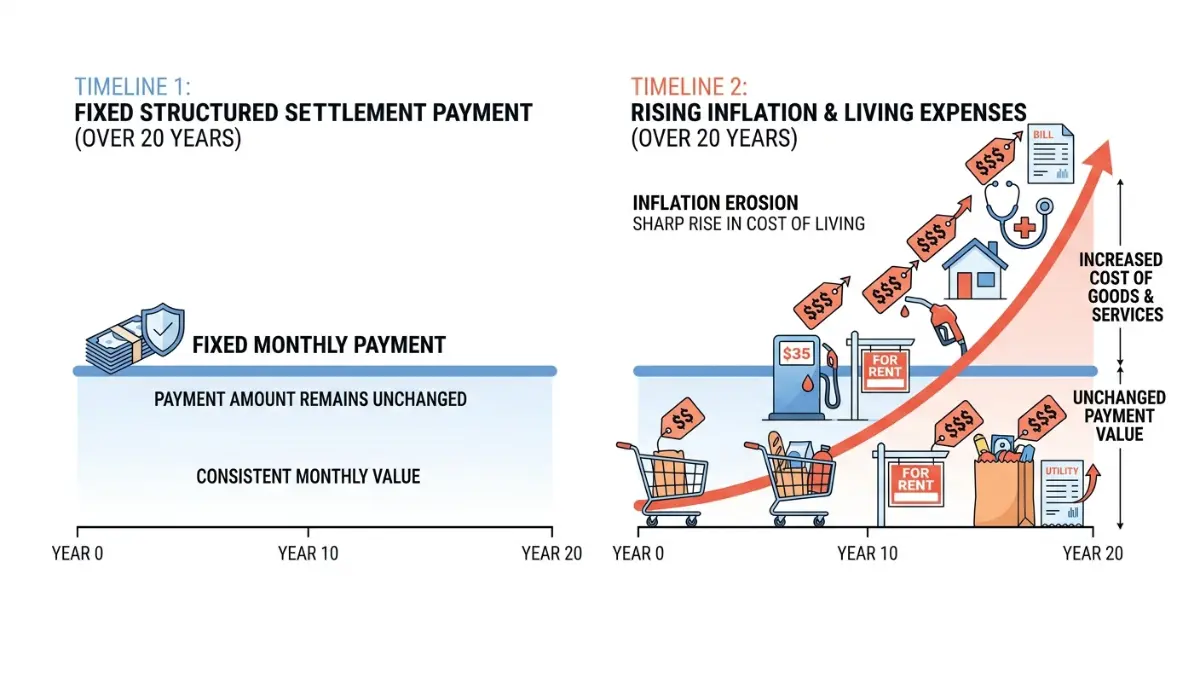

What the settlement documents do not prominently disclose is that every payment amount is permanently fixed in nominal dollars from the day the agreement is signed.

What the 2026 inflation environment means for long-term payment recipients

The 2026 inflation environment — with cumulative price increases since 2006 compounding the losses from the 2021–2023 surge — has accelerated the purchasing power erosion that long-term recipients are experiencing.

This article shows you exactly how much has been lost, how to calculate your own real payment value, what legal protections and options exist, and how to evaluate the sell-vs-hold decision correctly.

ℹ️ Disclaimer: The structured settlement and financial planning information in this article is intended for educational purposes only. The sale of structured settlement payment rights is a regulated transaction requiring state court approval under applicable Structured Settlement Protection Acts; legal requirements vary significantly by jurisdiction. Tax treatment of settlement proceeds under Internal Revenue Code Section 104 depends on the specific nature of your underlying claim. All purchasing power calculations use 2026 Bureau of Labor Statistics CPI-U data. Consult a licensed financial advisor and a qualified legal professional specializing in structured settlement transactions before making any financial decision based on this content.

Why structured settlement payments can’t keep up with inflation

Fixed annuity payments are established at settlement origination through a process called a qualified assignment — the defendant or insurer transfers the payment obligation to a life insurance company, which funds it through a single-premium annuity contract.

That annuity pays a predetermined nominal dollar amount on a fixed schedule for the life of the contract. It does not have a built-in inflation adjustment mechanism unless a cost-of-living rider was explicitly negotiated and included at the time of the original agreement.

How fixed payments are set at origination — and why they never adjust

The qualified assignment process is irrevocable. Once the life insurance company assumes the payment obligation, the nominal payment schedule is permanently locked — the settlement recipient, the original defendant, and even the courts cannot modify it.

This is fundamentally different from Social Security benefits, which carry a statutory COLA, or from TIPS (Treasury Inflation-Protected Securities), which adjust principal with the CPI. Your payment stream has no equivalent protection.

Do structured settlements keep up with inflation? The short answer.

No. A standard structured settlement without a COLA rider does not keep up with inflation under any circumstance.

The 2026 BLS CPI-U annual rate of 2.8% means every dollar of your fixed payment loses 2.8 cents of real value annually — and that loss compounds each year, regardless of market conditions or Federal Reserve policy.

📊 Data Point: The Bureau of Labor Statistics reported the 2026 CPI-U annual rate at 2.8%, continuing the post-2023 deceleration from the 9.1% peak recorded in June 2022. Settlements originated before 2021 now carry compound inflation losses from both the elevated period and the ongoing annual erosion. — Source: Bureau of Labor Statistics, CPI-U, Q1 2026.

A take-home pay calculator can help you see how much your effective monthly purchasing power compares to what your settlement pays — the gap is often larger than recipients expect.

How to calculate your structured settlement’s real purchasing power today

You can calculate the inflation-adjusted value of your settlement payment in four steps using publicly available BLS data.

You do not need a financial advisor to run this math — but you do need the result before you can make an informed decision about your options.

Step-by-step: applying BLS CPI-U data to your settlement payment

- Locate your origination date. Find your original settlement agreement and record the year your payments began — this is your baseline year.

- Determine your payment amount. Note the exact monthly (or periodic) payment amount stated in your settlement documents.

- Apply the compound deflator. Divide your payment amount by (1 + the 20-year average annual CPI-U rate) raised to the power of years since origination. Using the 2026 BLS 20-year compound average of 2.9% annually: Real Value = Nominal Payment ÷ (1.029)^years elapsed.

- Compare to your current expenses. Run the real value figure against your budget calculator to quantify the monthly shortfall between what your settlement pays and what your actual cost of living now requires.

The inflation calculator on this site performs this calculation automatically — enter your payment amount and settlement year to see the real-dollar result immediately.

A worked example: what $2,000/month is worth in 2026 real dollars

Consider a recipient receiving $2,000/month from a settlement originated in 2006 — a 20-year-old payment schedule.

Applying the 2026 BLS compound CPI-U deflator: $2,000 ÷ (1.029)^20 = $2,000 ÷ 1.771 = $1,129 in real 2026 purchasing power. That recipient has lost $871 per month — $10,452 per year — silently, without any statement or notification.

💡 Expert Note (CFA): In my practice, recipients are consistently shocked by this number. They know inflation exists — but because their bank account shows $2,000 arriving every month, they don’t feel the loss. The compound deflator makes it visible. The shock of seeing $871/month evaporated is the moment when real financial planning for settlement recipients usually begins.

What 20 years of inflation actually costs a structured settlement

The number that matters is not the annual CPI-U rate. It is the compounded, cumulative real dollar loss across the full life of a fixed payment schedule.

The 20-year purchasing power table below quantifies that loss at three common payment levels, using the 2026 BLS CPI-U 20-year compound rate of 2.9% annually.

The 20-year purchasing power table: $1,000, $2,000, and $3,000/month

A $2,000/month fixed payment from a 20-year-old settlement now delivers approximately $1,126 in real purchasing power. By year 20, the recipient is effectively receiving 43.7 cents for every dollar their settlement was designed to pay.

| Settlement Age | $1,000/mo Nominal | Real Purchasing Power | $2,000/mo Nominal | Real Purchasing Power | $3,000/mo Nominal | Real Purchasing Power |

|---|---|---|---|---|---|---|

| 1 year | $1,000 | $972 | $2,000 | $1,943 | $3,000 | $2,915 |

| 5 years | $1,000 | $866 | $2,000 | $1,732 | $3,000 | $2,598 |

| 10 years | $1,000 | $751 | $2,000 | $1,501 | $3,000 | $2,252 |

| 15 years | $1,000 | $650 | $2,000 | $1,300 | $3,000 | $1,951 |

| 20 years | $1,000 | $563 | $2,000 | $1,126 | $3,000 | $1,689 |

Source: Finance Authority Hub calculations using 2026 BLS CPI-U 20-year compound average of 2.9% annually. Real values expressed in equivalent 2026 purchasing power. Verify current CPI-U figures at bls.gov/cpi.

Use the compound interest calculator to model your specific payment amount at different origination years and inflation rates.

Why compound inflation hits fixed payments harder than linear math suggests

Most recipients mentally calculate their loss by multiplying the annual rate by the number of years: 2.9% × 20 = 58%. That is linear math — and it significantly understates the actual damage.

Compound math produces the correct answer: (1.029)^20 − 1 = 77.1% cumulative erosion, not 58%. A settlement recipient thinking “I’ve lost about half” has materially underestimated the problem by nearly 20 percentage points.

📊 Data Point: The Federal Reserve’s H.15 statistical release shows that structured settlements originated between 2004 and 2008 were priced during a period when 10-year Treasury yields averaged 4.2%–5.1% — and long-term inflation expectations were anchored near 2.5%. The subsequent post-2020 inflation surge was not modeled into the annuity pricing for those contracts. — Source: Federal Reserve H.15 Selected Interest Rates, federalreserve.gov/releases/h15, 2026.

What low-rate origination periods did to long-term settlement value

Settlements structured between 2009 and 2019 — the post-financial-crisis, low-rate era — were priced with forward inflation assumptions near 1.8%–2.0% annually.

The actual realized CPI-U compound rate through 2026 has run approximately 50 basis points above those assumptions for every year since 2020, creating a permanent compounding gap between the settlement’s original pricing and the inflation environment recipients are actually living in.

The investment calculator can model what the cumulative purchasing power loss from your specific origination year would be worth had it been preserved in an inflation-adjusting vehicle — useful context for any sell-vs-hold evaluation.

COLA riders, inflation protection, and what your settlement actually includes

Most structured settlement recipients do not know whether their agreement includes a cost-of-living adjustment provision — and most attorneys did not routinely recommend one during the low-inflation era of 2009–2019.

Before evaluating any sell-vs-hold decision, you need to know whether your settlement already has partial inflation protection built in.

What a COLA rider does — and why most structured settlements don’t have one

A COLA rider is a provision negotiated at settlement origination that automatically increases your periodic payments by a fixed annual percentage — typically 1%–3% — to partially offset the effects of inflation on your fixed annuity income.

At a 3% annual COLA, a $2,000/month payment becomes $2,688/month after 10 years and $3,612/month after 20 years — nearly matching the inflation-equivalent amount needed to preserve full purchasing power. FINRA’s investor education resource on fixed annuity products explains why this provision must be specified at origination and cannot be added to an existing contract.

💡 Expert Note (CFA): In my experience reviewing client settlement documents, COLA riders were underutilized in settlements executed before 2010. Attorneys and structured settlement brokers operated in a low-inflation environment and treated the rider as an optional add-on rather than essential income protection. The result is a generation of recipients who are now absorbing the full weight of post-2020 inflation with no built-in buffer.

The savings calculator can help model the compounding difference between a COLA-protected payment stream and your current fixed schedule.

How to find out if your settlement includes inflation protection

Pull your original settlement agreement — specifically the annuity contract or qualified assignment document — and search for the phrases “cost-of-living adjustment,” “COLA,” “inflation rider,” or “annual increase.”

If none of those terms appear, your settlement pays a flat nominal amount for its full duration with no inflation protection of any kind.

What state structured settlement protection acts mean for your options

If you determine your settlement has no COLA rider, you have limited options for modifying the agreement itself — the qualified assignment is legally irrevocable.

What Structured Settlement Protection Acts (SSPAs) govern is a different action: the sale of your payment rights to a factoring company. That sale is legal in most states but requires court approval — a judge must find it is in your best interest. An ROI calculator can help you run preliminary numbers on any offer before involving a court or attorney.

Should you sell your structured settlement because of inflation?

Selling your structured settlement payments to a factoring company is a permanent, legally governed transaction — and inflation alone is rarely a sufficient reason to proceed without first running a complete financial analysis.

The four factors below are the same framework I use with clients who bring me a factoring offer and ask whether they should sign it.

The four factors that determine whether selling makes financial sense

Before contacting any factoring company, evaluate your situation against these four tests:

- Your monthly expense gap. Calculate the difference between your current real settlement purchasing power (from your Section 3 calculation) and your actual monthly expenses. If the gap is under $300/month, selling a long-payment stream at a steep discount may cost more than the problem it solves.

- The factoring company’s discount rate. Reputable factoring companies in 2026 offer lump sums at effective discount rates of 9%–18% of present payment value. Higher rates mean a significantly lower lump sum — a 15% discount rate on a 10-year payment stream reduces your total payout by 43%–51% compared to simply receiving your payments as scheduled.

- Your remaining payment schedule. The fewer payments remaining, the less total purchasing power you stand to lose to inflation — and the less financial benefit a lump sum provides over waiting.

- What you would do with the lump sum. A CD calculator can show you current guaranteed rates on FDIC-insured certificates of deposit; if those rates cannot outpace the factoring discount over your remaining schedule, you may be trading a known income stream for a lump sum that performs worse.

What discount rates from factoring companies actually mean for your offer

A factoring company’s discount rate functions as the company’s required rate of return — it is applied to the present value of your entire remaining lump-sum buyout as a compound annual rate.

At a 12% discount rate applied to 15 years of $2,000/month remaining payments, the present value of those payments is approximately $167,000 at 0% return. The factoring company’s 12% discount produces a lump-sum offer near $116,000–$124,000 — compared to $360,000 in total nominal payments if held. The investment calculator can model whether that lump sum, invested at current market rates, delivers equivalent or superior total value.

What the CFPB says about your rights before you sign anything

The Consumer Financial Protection Bureau provides specific consumer guidance for structured settlement recipients evaluating factoring transactions. Review the CFPB’s guidance for structured settlement recipients before responding to any factoring offer.

The CFPB’s guidance specifically flags: the right to an independent review period before signing, the requirement for court approval in most states, and the obligation of the factoring company to disclose the discount rate and effective annual percentage rate in writing.

⚠️ Warning: State court approval under your applicable Structured Settlement Protection Act is not a formality — judges have denied factoring transactions when the lump sum offered was deemed insufficient or the recipient’s stated financial need did not justify the long-term income loss. Consult both a licensed financial advisor and a structured settlement attorney before submitting any court petition.

Taking control of your structured settlement in an inflationary environment

Your structured settlement is a fixed-income asset in an inflationary world — and the gap between what your payments say and what they actually buy widens every year you do nothing.

The three actions below are the starting point I recommend to every settlement recipient who discovers, often for the first time, how much real value their payments have lost.

The three things every structured settlement recipient should do this year

Do these in sequence — each one informs the next.

- Pull your original settlement agreement and search for the COLA rider. Look for “cost-of-living adjustment,” “annual increase,” or “COLA” in the annuity contract attached to your qualified assignment. If it does not appear, your settlement has no inflation protection.

- Run the Section 3 calculation on your specific payment. Use the inflation calculator with your actual payment amount and settlement origination year to produce your real purchasing power figure. Write it down — you need this number for every conversation that follows.

- Assess your long-term income adequacy. Use the retirement calculator to model whether your settlement income — at its declining real value — will cover your projected expenses over the full remaining term.

If step 3 reveals a material gap, that is when professional consultation becomes the right next step — not before.

When to call a financial advisor vs. a settlement attorney

Call a licensed financial advisor first if your question is: “Does selling my payments make financial sense compared to holding them and managing the inflation gap with other assets?”

Call a structured settlement attorney first if your question is: “What is the legal process for selling my payments in my state, and what court petition requirements apply to my specific agreement?” The social security calculator is a useful companion tool if your settlement income supplements Social Security — a retirement planner or CFP can help you optimize the combined fixed-income picture across both sources.

✅ Pro Tip: Before meeting with any professional, download and complete the Section 3 calculation, note your remaining payment count, and verify whether a COLA rider exists in your documents. This 30-minute preparation step saves an average of one to two billable advisory hours and produces a far more productive first conversation.

Structured settlement and inflation: your questions answered

1. Does inflation reduce structured settlement payments?

Structured settlement inflation does not reduce the nominal dollar amount of your payments — it reduces what those dollars buy. The 2026 Bureau of Labor Statistics CPI-U annual rate of 2.8% erodes the real value of every fixed payment by that amount each year. Over 20 years at a 2.9% compound average, a $2,000/month payment loses approximately $874 of real purchasing power monthly. Consult a licensed financial advisor to model your specific situation.

2. What is a cost-of-living adjustment in a structured settlement?

A COLA rider in a structured settlement is a provision negotiated at origination that automatically increases periodic payments by a fixed annual percentage — typically 1%–3% — to partially offset inflation. It must be written into the original settlement agreement and funded through the annuity at origination; it cannot be added retroactively to an existing qualified assignment. Most settlements executed before 2015 do not include a COLA rider.

3. How much purchasing power does a structured settlement lose over 20 years?

A structured settlement fixed at $2,000/month loses approximately $874 per month in real purchasing power over 20 years, based on the 2026 BLS compound CPI-U average of 2.9% annually. The 20-year nominal payment totals $480,000, but the inflation-adjusted equivalent value of those payments is approximately $322,000 in 2026 purchasing power. Consult a licensed financial advisor to calculate your specific payment amount and origination year.

4. Can I sell my structured settlement if inflation is hurting my finances?

Yes — in most U.S. states, you can sell some or all future structured settlement payments to a licensed factoring company, but state court approval is required under Structured Settlement Protection Acts. The process typically takes 45–90 days. The factoring company must disclose its effective discount rate, which typically ranges from 9%–18% of present payment value. Consult both a licensed financial advisor and a settlement attorney before proceeding.

5. Are structured settlement payments taxable?

Physical injury structured settlement payments are excluded from federal gross income under Internal Revenue Code Section 104(a)(2), as clarified in IRS Publication 4345 on settlement taxability. This exclusion applies to the periodic payments themselves, not to earnings on any lump sum received as an alternative. Workers’ compensation and non-physical-injury settlements may have different treatment. Consult a licensed tax professional for your specific settlement classification.

6. What is the current inflation rate affecting fixed income in 2026?

The Bureau of Labor Statistics reported the 2026 CPI-U annual rate at approximately 2.8%, continuing the deceleration from the 9.1% peak recorded in 2022. For structured settlement recipients evaluating long-term purchasing power loss, the more relevant figure is the 20-year compound average — which runs approximately 2.9% annually when the post-2020 inflation surge is incorporated into the full calculation period. Verify current figures at bls.gov/cpi before running any calculations.

7. Do structured settlements keep up with inflation?

Standard structured settlements do not keep up with inflation. Payments are fixed in nominal dollars through an irrevocable qualified assignment to a life insurance company and have no automatic adjustment mechanism. A 2.8% annual CPI-U rate — the 2026 BLS figure — erodes a fixed payment by approximately 43.7% in real value over 20 years. Only settlements with a negotiated COLA rider provide any built-in inflation offset.

8. What happens to a structured settlement during a period of high inflation?

During high inflation, structured settlement recipients experience accelerated purchasing power erosion. The 2021–2023 period, when CPI-U peaked above 9%, compressed the real value of fixed payments more rapidly than any period since the early 1980s. According to 2026 BLS compound data, recipients whose settlements originated before 2021 have absorbed cumulative real losses exceeding 22%–28% just from the post-COVID inflation surge — on top of the baseline erosion already accumulating.

9. How do I calculate the real value of my structured settlement payment?

Divide your nominal monthly structured settlement payment by the compound inflation factor for your settlement’s age: (1 + average annual CPI-U rate) raised to the power of years since origination. Using the 2026 BLS average of 2.9%, a settlement originated 15 years ago carries a deflator of (1.029)^15 = 1.538. A $2,000/month payment is worth $1,300 in today’s real purchasing power. Use the income tax calculator to model any tax implications if you are evaluating a lump-sum sale.

10. Is selling a structured settlement a good financial decision in 2026?

Whether selling structured settlement payments makes sense in 2026 depends on: your monthly expense shortfall relative to real purchasing power, the factoring company’s discount rate (typically 9%–18%), the number and schedule of your remaining payments, and whether a lump sum invested at current rates outperforms holding. In my experience, most recipients benefit more from a professional financial analysis than from an immediate sale decision. Consult a licensed financial advisor and settlement attorney before proceeding.

11. What is a structured settlement factoring company?

A structured settlement factoring company purchases your right to future settlement payments in exchange for an immediate lump sum, applied at a discount rate reflecting the company’s required return — typically 9%–18% of the payment stream’s present value. The transaction must be approved by a state court under your applicable Structured Settlement Protection Act. Factoring companies vary significantly in rates, transparency, and customer service; compare at least three offers before agreeing to any terms.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.