What Is PMI on a Mortgage — And 7 Proven Ways to Avoid It in 2026

PMI adds $100–$400/month to your mortgage — and pays your lender, not you. Discover 7 proven strategies to avoid or eliminate private mortgage insurance in 2026.

In This Article

PMI — private mortgage insurance — is a monthly fee lenders charge when your down payment is under 20% on a conventional loan. It protects the lender, not you. In 2026, PMI costs between 0.46% and 1.50% of your loan amount annually, adding $100–$400+ to your monthly payment. Here’s exactly how it works — and how to legally eliminate it.

What Is PMI on a Mortgage?

Private mortgage insurance (PMI) is a policy that conventional mortgage lenders require when a borrower puts down less than 20% of the home’s purchase price. Before you take your first payment personally, understand one critical fact: PMI protects the lender — not you.

If you default, the insurance reimburses your lender for a portion of their losses. You pay every month for coverage that benefits someone else.

PMI applies exclusively to conventional conforming loans — mortgages backed by Fannie Mae and Freddie Mac. It does not apply to government-backed loans like VA or USDA loans, which have their own fee structures.

According to the Consumer Financial Protection Bureau (CFPB), lenders must automatically cancel PMI once your loan balance reaches 78% of the original purchase price — but you can request removal even earlier at 80%.

Before using our mortgage calculator to estimate your full payment, it’s worth understanding exactly what you’re paying and why.

PMI vs. MIP vs. VA Funding Fee — What’s the Difference?

| Insurance Type | Loan Type | Who Pays | Cancelable? |

|---|---|---|---|

| PMI (Private Mortgage Insurance) | Conventional | Borrower | ✅ Yes, at 20% equity |

| MIP (Mortgage Insurance Premium) | FHA | Borrower | ⚠️ Often life-of-loan |

| VA Funding Fee | VA Loan | Borrower (one-time) | N/A — one-time upfront |

| USDA Guarantee Fee | USDA | Borrower | N/A — annual fee |

For a detailed comparison, see our guide on VA Loan vs. FHA Loan — especially if you’re a veteran considering your options.

Does PMI Protect You?

No. PMI provides zero financial protection to the borrower.

If you lose your job and can’t make payments, PMI doesn’t help you. It pays the lender to recover losses after foreclosure. This is why eliminating PMI as fast as possible is one of the smartest financial moves a homeowner can make.

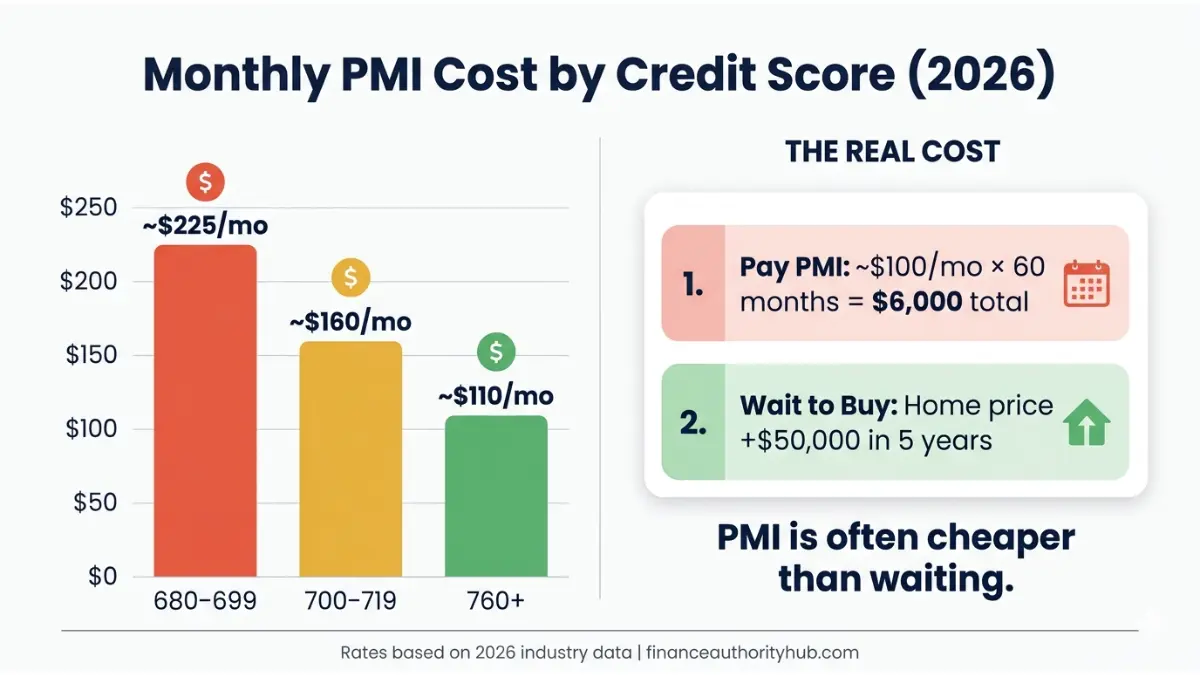

How Much Does PMI Cost in 2026?

PMI rates in 2026 range from 0.46% to 1.50% of your original loan amount per year, based on current data from Bankrate and NerdWallet. Your exact rate depends on three key factors: credit score, loan-to-value (LTV) ratio, and loan type.

PMI Cost by Credit Score and Down Payment — 2026 Matrix

This table is what your lender won’t hand you upfront:

| Down Payment | Credit Score | Loan Amount | Est. Annual PMI | Est. Monthly PMI |

|---|---|---|---|---|

| 5% | 760+ | $350,000 | ~$1,295–$1,610 | ~$108–$134 |

| 5% | 700–719 | $350,000 | ~$1,925–$2,450 | ~$160–$204 |

| 5% | 680–699 | $350,000 | ~$2,415–$2,975 | ~$201–$248 |

| 10% | 760+ | $350,000 | ~$945–$1,190 | ~$79–$99 |

| 10% | 700–719 | $350,000 | ~$1,365–$1,715 | ~$114–$143 |

| 15% | 760+ | $350,000 | ~$560–$875 | ~$47–$73 |

Key takeaway: A credit score difference of 80 points can nearly double your monthly PMI cost. Use our credit score calculator to understand your current score tier before applying.

The “PMI vs. Waiting to Buy” Math — What No One Tells You

Most buyers assume avoiding PMI by waiting to save 20% down is the smart move. The math often says otherwise.

Real-world example:

- Home price today: $350,000

- PMI at 10% down: ~$100/month

- Saving period to reach 20% down: 4–5 years

- Home price appreciation at 3%/year: +$43,000–$56,000 added to purchase price

PMI over 5 years = ~$6,000 total. The cost of waiting = potentially $50,000+ more in purchase price.

PMI, in the right situation, is a calculated investment — not just a penalty. Use our home affordability calculator to model your specific numbers before deciding.

The 4 Types of PMI — Which One Are You Paying?

Most buyers don’t realize there are four distinct PMI structures. Choosing — or being assigned — the wrong type can cost thousands over the life of your loan.

PMI Types Side-by-Side

| PMI Type | How It’s Paid | Cancelable? | Best For |

|---|---|---|---|

| Borrower-Paid (BPMI) | Monthly premium added to mortgage payment | ✅ Yes — at 80% LTV | Most buyers; most common type |

| Lender-Paid (LPMI) | Built into a permanently higher interest rate | ❌ No — rate is permanent | Buyers selling/refinancing within 5–7 years |

| Single-Premium (SPMI) | One lump sum paid at closing | ✅ If you sell or refinance | Cash-rich buyers wanting zero monthly PMI |

| Split-Premium | Part paid upfront + reduced monthly premium | ✅ Partial | Buyers wanting lower monthly cost |

What This Means For You: LPMI feels cheaper month-to-month because there’s no separate PMI line item on your statement. But since the cost is baked into your interest rate permanently, you can never cancel it by building equity. BPMI costs more monthly — but it disappears once you hit 20% equity. For most long-term homeowners, BPMI is the better deal.

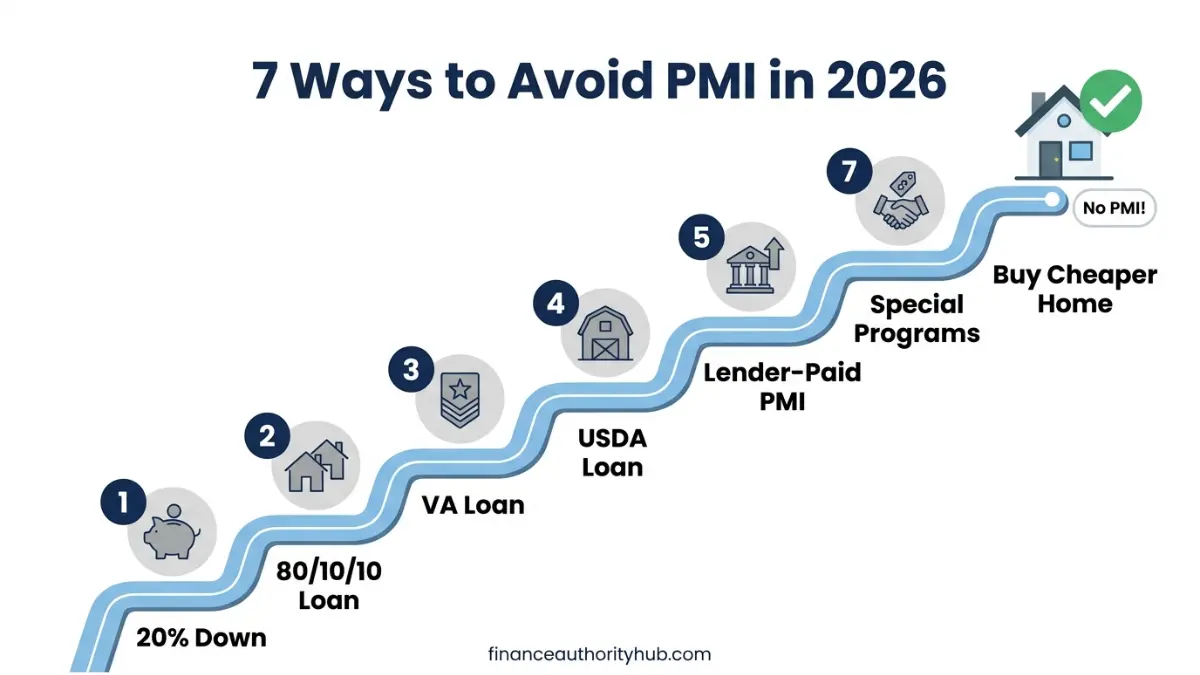

7 Proven Ways to Avoid PMI in 2026

This is the core of what most homebuyers are searching for. Here are seven fully actionable strategies — ranked from simplest to most strategic.

1. Put 20% Down — The Clean Slate Approach

The most direct route: put down at least 20% of the home’s purchase price, and PMI is never triggered.

- On a $350,000 home: $70,000 down eliminates PMI entirely

- Benefit: lower monthly payment + better interest rate + immediate equity

- Challenge: requires significant savings — use our down payment calculator to set a savings timeline

2. The 80/10/10 Piggyback Loan

A piggyback loan lets you avoid PMI with only 10% cash down. Here’s the structure:

- First mortgage: 80% of home value (PMI threshold not triggered)

- Second mortgage (HELOC or home equity loan): 10% of home value

- Your cash: 10% down payment

Real math on a $350,000 home:

- First mortgage: $280,000 at 6.8% = ~$1,828/month

- Second mortgage: $35,000 at ~8.5% = ~$298/month

- Zero PMI

Important caveat: The second loan carries a higher interest rate. Run the math carefully — compare the combined payment against a single loan with PMI. Our loan-to-value calculator helps you model both scenarios.

3. VA Loan — Best Option for Veterans

If you served, this is the most powerful mortgage available. VA loans through the U.S. Department of Veterans Affairs require:

- 0% down payment

- Zero monthly PMI — ever

- One-time funding fee (often rolled into the loan; some veterans qualify for an exemption)

Bottom line: A veteran buying a $350,000 home saves ~$100–$200/month in PMI versus a conventional loan with 10% down. See our full VA Loan vs. FHA Loan comparison for eligibility details.

4. USDA Loan — For Rural and Suburban Buyers

USDA Rural Development loans offer:

- 0% down payment

- No monthly PMI

- Small annual guarantee fee (~0.35%) — significantly cheaper than PMI

- Geographic and income eligibility requirements apply

If your target home is in a qualifying area, USDA loans can be dramatically cheaper than conventional loans with PMI.

5. Lender-Paid PMI (LPMI)

With LPMI, your lender pays the PMI premium in exchange for a slightly higher interest rate — typically 0.25%–0.375% higher.

- Pros: No PMI line item on your monthly statement; simpler budget math

- Cons: Rate is permanent — you cannot cancel it by reaching 20% equity; only eliminated by refinancing or selling

LPMI makes sense if: You plan to sell or refinance within 5–7 years before the rate premium outweighs the PMI cost savings.

6. Special Lender Programs With No PMI

Several lenders offer low-down-payment mortgages that waive PMI for qualifying borrowers:

- Bank of America Affordable Loan Solution: 3% down, no PMI (income limits apply; homebuyer counseling required)

- NACA Program: 0% down, no PMI, no closing costs (for low-to-moderate income buyers)

- Credit union portfolio loans: Some offer no-PMI at 10–15% down for members with strong profiles

Check eligibility requirements carefully — income and geographic limits often apply.

7. Buy a Less Expensive Home

If 20% down on your target home is out of reach, consider whether a lower-priced home would allow you to hit that threshold with your current savings.

- Example: You have $60,000 saved for a down payment. On a $350,000 home, that’s 17% — PMI required. On a $280,000 home, that’s 21% — no PMI.

- Use our home affordability calculator to find your no-PMI price range.

Also worth reviewing: our credit score to buy a house guide — because a higher score also reduces your PMI rate if you end up paying it.

How to Remove PMI You’re Already Paying

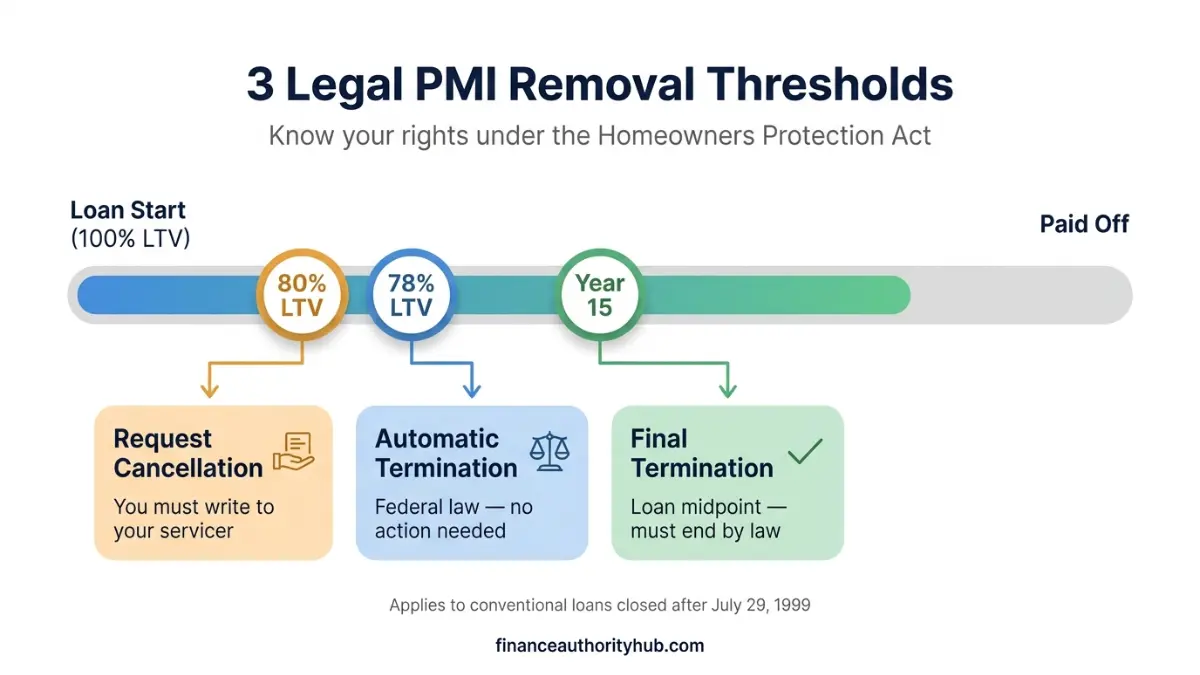

If you’re currently paying PMI, you have federal legal rights to cancel it — and most homeowners don’t know the full scope of those rights.

Your Federal Legal Rights Under the Homeowners Protection Act

The Homeowners Protection Act of 1998 (HPA), enforced by the CFPB, gives you three mandatory PMI cancellation rights on conventional loans closed after July 29, 1999.

Route 1 — Request Cancellation at 80% LTV

You can request PMI cancellation in writing once your balance reaches 80% of the original purchase price.

Requirements:

- Good payment history (no 30-day late payments in the past 12 months)

- No subordinate liens on the property

- Written proof that home value hasn’t declined below original value (lender may require appraisal at your cost)

Step-by-step process:

- Calculate when your balance will hit 80% LTV using our amortization calculator

- Write to your mortgage servicer (not your original lender) with your loan number and property address

- Include a written cancellation request stating you’ve reached 80% LTV

- Your servicer must respond and cancel within 30 days if all criteria are met

Route 2 — Automatic Termination at 78% LTV

Federal law mandates automatic PMI cancellation when your balance drops to 78% of the original purchase price — with no action required from you.

- You must be current on payments for automatic termination to apply

- If you’re behind, termination occurs after you bring the account current

- Your lender cannot charge you for this cancellation

Important: According to the CFPB’s HPA guidance, automatic termination is based on the original purchase price, not current appraised value. This distinction matters if your home has appreciated.

Route 3 — Final Termination at Loan Midpoint

Even if neither of the above thresholds is reached, PMI must legally end at the midpoint of your loan term:

- 30-year mortgage: PMI must terminate after year 15 (month 180)

- 15-year mortgage: PMI must terminate after year 7.5

- You must be current on payments

This rule most commonly applies to interest-only or balloon payment mortgages.

Route 4 — Refinance to Eliminate PMI

If your home has appreciated significantly, refinancing into a new conventional loan with an LTV of 80% or lower can permanently eliminate PMI.

- Check whether current home values push you past the 20% equity threshold

- Use our mortgage refinance calculator to model whether refinancing makes financial sense after accounting for closing costs

- Closing costs on a refinance typically run 2%–6% of the loan amount — ensure the monthly PMI savings justify the upfront expense

Also see our guide on refi rate drops in 2026 for current refinance rate context.

Route 5 — Appraisal-Based Early Cancellation

If your home has appreciated and you believe your equity has crossed the 20% threshold ahead of schedule:

- Request a new appraisal from a licensed appraiser (cost: $300–$700 typically)

- Submit the appraisal to your servicer alongside a written cancellation request

- Note: Most Fannie Mae and Freddie Mac guidelines require at least 2 years of payment history before allowing appraisal-based early cancellation, and 5 years if appreciation alone (not extra payments) pushed you past 80% LTV

This is particularly powerful in high-appreciation markets where home values have risen 15–25% since purchase.

Frequently Asked Questions About PMI

1. What is PMI on a mortgage?

PMI stands for private mortgage insurance. It’s a monthly fee required on conventional loans when the down payment is less than 20%. It protects the lender — not the borrower — in case of default.

2. How much does PMI cost per month in 2026?

PMI typically costs $50–$400+ per month depending on your loan size, credit score, and LTV ratio. On a $300,000 mortgage with 5% down and a 720 credit score, expect roughly $115–$200/month.

3. Does PMI go away automatically?

Yes. Under the Homeowners Protection Act, federal law requires automatic PMI cancellation when your balance reaches 78% of the original purchase price, provided you’re current on payments.

4. Can I cancel PMI before 78% LTV?

Yes. You can submit a written request to your servicer once your balance reaches 80% LTV. You must have good payment history and the home’s value must not have declined. No additional fees for cancellation are permitted under federal law.

5. Is PMI tax deductible in 2026?

No — not currently. The PMI deduction expired after tax year 2021 and has not been permanently reinstated as of March 2026. Do not factor potential PMI deductibility into your home-buying budget. Consult a tax professional for the latest updates.

6. What’s the difference between PMI and MIP?

PMI applies to conventional loans and is cancelable once you reach 20% equity. MIP applies to FHA loans — if you put down less than 10%, MIP typically lasts the entire loan term. The only way to eliminate FHA MIP early is to refinance into a conventional loan. See our FHA Loan vs. Conventional Loan guide for a full breakdown.

7. Can I avoid PMI with less than 20% down?

Yes. VA loans (0% down, no PMI for eligible veterans), USDA loans (0% down for qualifying rural areas), piggyback loans (80/10/10 structure), and certain lender programs all allow sub-20% down without monthly PMI.

8. Does a higher credit score lower PMI costs?

Significantly. A 760+ credit score can reduce your PMI rate by nearly 50% compared to a 680 score on the same loan. Improving your credit before applying can save thousands over the life of the PMI period. Review our credit score guide to understand which tier you’re in.

9. What is lender-paid PMI (LPMI)?

LPMI is when the lender covers PMI in exchange for a permanently higher interest rate — typically 0.25%–0.375% above standard rates. There is no monthly PMI charge, but the elevated rate is permanent. You cannot cancel LPMI by building equity; you can only eliminate it by refinancing or selling.

10. How do I request PMI removal?

Write to your mortgage servicer (not your original lender) with: your full loan number, property address, and a written cancellation request. State that your LTV has reached 80% and that you request immediate PMI cancellation per the Homeowners Protection Act. Your servicer must respond within 30 days.

11. Does PMI apply to refinances?

Yes. If you refinance a conventional loan and your new LTV exceeds 80%, PMI will be required on the new loan. If your home has appreciated and you’ve paid down your balance, use our home equity calculator to determine your current equity position before refinancing.

Expert Panel

“The most overlooked PMI strategy is the appraisal-based early cancellation. In markets that appreciated 15–20% since 2021, many homeowners are sitting on enough equity to eliminate PMI immediately — they just haven’t requested a new appraisal.” — Laura M. Bennett, CFP® | Senior Personal Finance Expert, financeauthorityhub.com

“LPMI is frequently pitched as a ‘no PMI’ loan. It isn’t — the cost is simply embedded in your rate forever. For buyers planning to stay 10+ years, borrower-paid PMI that cancels at 80% LTV is almost always the lower lifetime cost.” — Daniel Moreau, CPA/CFP® | Mortgage & Tax Strategy Expert, financeauthorityhub.com

Related Tools:

- Mortgage Calculator — Estimate your full monthly payment including PMI

- Mortgage Refinance Calculator — Model whether refinancing eliminates PMI profitably

- Home Equity Calculator — Find your current equity position

- Down Payment Calculator — Build your savings timeline to hit 20%

- Amortization Calculator — See exactly when your balance hits 80% and 78% LTV

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or mortgage advice. PMI rates, cancellation rules, and lending guidelines vary by lender, loan type, and state. Federal protections described apply to conventional residential mortgage loans closed on or after July 29, 1999. FHA and VA loans follow separate rules. Always consult a licensed mortgage professional or certified financial advisor for guidance specific to your situation.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.