Liability Car Insurance: The Limits That Can Legally Wipe You Out in 2026

Most drivers carry the legal minimum in liability car insurance — but 2026 accident costs can exceed those limits fast. Here’s what happens when they run out.

In This Article

What Is Liability Car Insurance?

Liability car insurance pays for injuries and property damage you cause to others when you’re at fault in an accident — up to your policy limits. It covers the other driver’s medical bills, vehicle repairs, lost wages, and legal costs. It does NOT cover your own injuries or vehicle damage. Almost every U.S. state legally requires it.

Here’s what most drivers don’t know: when your limits run out, you personally owe the rest. Courts can garnish your wages, freeze your savings, and place liens on your home. That’s the gap that can ruin you — and the one your insurer won’t warn you about.

How Liability Car Insurance Actually Works

Liability car insurance is split into two components, and understanding both is critical before you choose your limits.

Bodily Injury Liability (BIL) covers medical expenses, lost wages, pain and suffering, and even funeral costs for people you injure in an at-fault accident. It also covers your legal defense if you’re sued.

Property Damage Liability (PDL) pays to repair or replace other people’s vehicles, fences, buildings, or any property you damage.

According to the Insurance Information Institute (III), it is strongly recommended that policyholders carry more than the state-required minimum liability insurance — enough to protect assets such as your home and savings.

What Liability Car Insurance Covers

- ✅ Medical bills, rehab costs, and lost wages for the other driver and passengers

- ✅ Repairs or replacement of the other driver’s vehicle

- ✅ Damage to fences, buildings, utility poles, or other property

- ✅ Legal defense costs and court judgments against you

- ✅ Pain and suffering settlements for injured parties

What Liability Car Insurance Does NOT Cover

- ❌ Your own medical bills after the accident

- ❌ Damage to your own vehicle

- ❌ Your passengers’ injuries

- ❌ Accidents that happen while driving for rideshare (Uber, Lyft) — special coverage is needed

- ❌ Any costs that exceed your policy limits — you pay those personally

Key Takeaway: Liability protects others from you. It does not protect you from yourself. For damage to your own car, you need comprehensive car insurance or collision coverage.

Understanding Liability Limits — The Numbers That Define Your Financial Risk

When you buy liability car insurance, you’ll see three numbers on your policy separated by slashes. This is your split limit — the most misunderstood part of any auto policy.

How to Read Your Liability Limits

A policy listed as 25/50/25 means:

| Number | What It Covers | Maximum Payout |

|---|---|---|

| First: 25 | Bodily injury per person | $25,000 |

| Second: 50 | Bodily injury per accident (total) | $50,000 |

| Third: 25 | Property damage per accident | $25,000 |

So if you cause an accident injuring 3 people and your policy is 25/50/25 — your insurer pays a maximum of $50,000 total for all injuries combined, capped at $25,000 per person. Everything above those caps is your personal responsibility.

Split Limits vs. Combined Single Limit

Some insurers offer a combined single limit (CSL) — one larger number that covers both bodily injury and property damage with no per-person cap.

| Coverage Type | Example | How It Works |

|---|---|---|

| Split Limit | 25/50/25 | Separate caps per person, per accident, per property |

| Combined Single Limit | $300,000 CSL | One flexible pool for all claims |

CSL policies offer more flexibility in serious multi-victim accidents but typically cost more. If you’re involved in a 4-car pileup with 6 injured people, a CSL policy distributes the full limit more fairly across all claims.

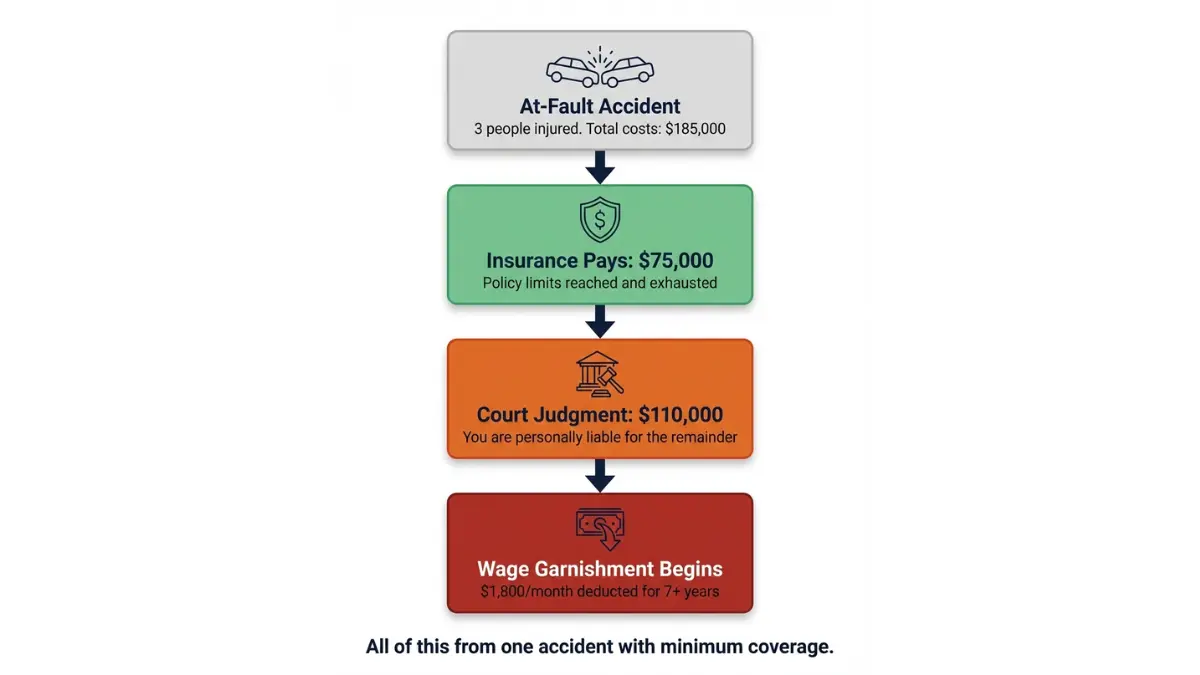

The Limit Exhaustion Trap: A Real-World Scenario

This is what no competitor tells you — and what every driver needs to read.

Real-World Scenario: A 38-year-old driver with a standard 25/50/25 policy runs a red light and strikes two vehicles. Three people are hospitalized. Total medical bills: $185,000. Vehicle damages: $45,000. The insurance company pays its maximum: $50,000 for injuries + $25,000 for property = $75,000. The remaining $155,000? The court orders a wage garnishment of $1,800/month from the at-fault driver’s paycheck — for over 7 years.

According to NHTSA’s economic crash cost data, motor vehicle crashes cost the U.S. economy $340 billion in direct economic costs in 2019 alone — a figure that has risen significantly with inflation. The average bodily injury liability claim now exceeds $24,000, and serious multi-person accidents easily reach $200,000–$500,000+.

State minimum liability limits — often $25,000–$50,000 — are nowhere near enough for a serious crash.

2026 State Minimum Liability Requirements — Is Your State’s Limit a Danger Zone?

Most state minimums were set decades ago and have never been adjusted for inflation or modern medical costs. Here’s the critical 2026 update most drivers haven’t seen.

🚨 Major 2026 State Limit Changes

Two states raised their minimum liability requirements in the last 12 months — and if you renewed before the change, you may already be under-covered:

- New Jersey: Raised minimums from 25/50/25 → 35/70/25 effective January 1, 2026

- North Carolina: Raised minimums from 30/60/25 → 50/100/50 effective July 1, 2025

If you live in either state and bought a 12-month policy before those dates, your coverage is still legal but now below the new recommended baseline.

State Minimum Liability Requirements: Top 10 States (2026)

| State | Bodily Injury Min | Property Damage Min | 2026 Update |

|---|---|---|---|

| California | 15/30/5 | $5,000 | ⚠️ Increase under legislative review |

| Texas | 30/60/25 | $25,000 | No change |

| Florida | ❌ No BI required | $10,000 PD only | No change |

| New York | 25/50/10 | $10,000 | No change |

| New Jersey | 35/70/25 | $25,000 | ✅ Raised Jan 2026 |

| North Carolina | 50/100/50 | $50,000 | ✅ Raised Jul 2025 |

| Illinois | 25/50/20 | $20,000 | No change |

| Ohio | 25/50/25 | $25,000 | No change |

| Georgia | 25/50/25 | $25,000 | No change |

| Pennsylvania | 15/30/5 | $5,000 | No change |

⚠️ California Warning: California’s property damage minimum is $5,000 — set in 1967. The average new vehicle repair after a moderate collision now exceeds $5,000. This limit is dangerously outdated.

⚠️ Florida Warning: Florida does not require bodily injury liability insurance. If you’re in a Florida at-fault accident, you may have zero coverage for the other driver’s medical bills unless you voluntarily purchased BIL.

You can verify your state’s current auto insurance requirements at your state DMV or the III’s state law resource.

How Much Liability Car Insurance Do You Actually Need in 2026?

State minimums are a legal floor, not a financial safety net. Here’s how to calculate the right coverage for your situation.

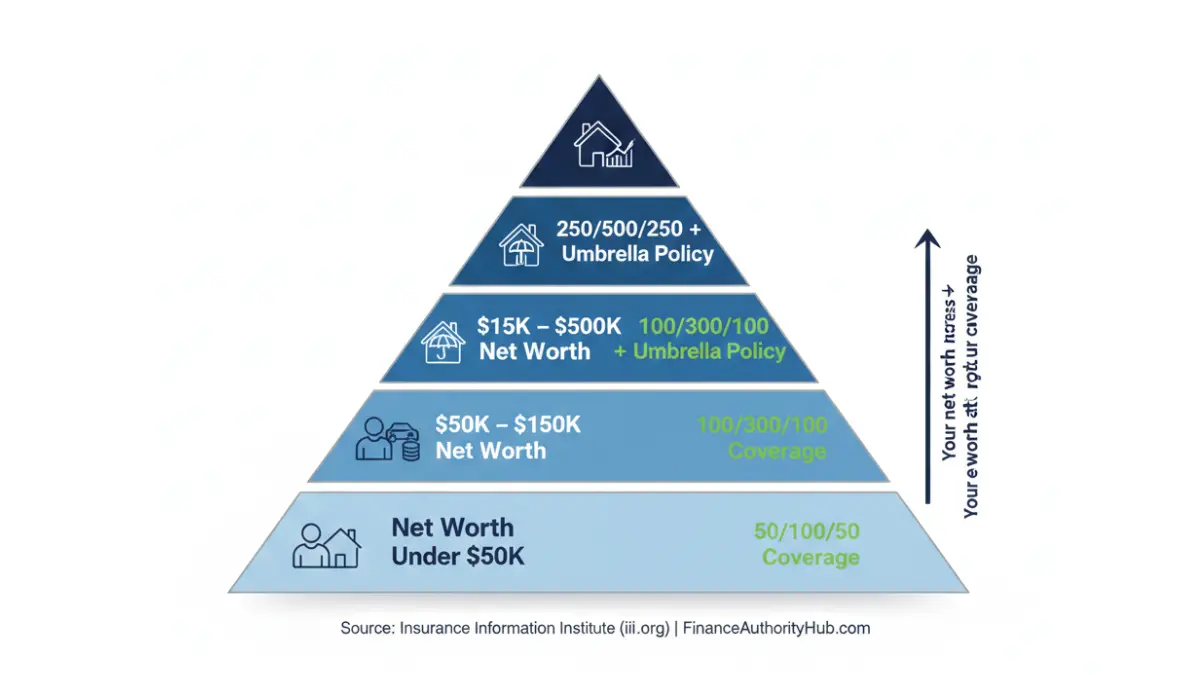

The Net Worth Rule (The Only Formula That Matters)

Your liability limits should equal or exceed your total net worth. This includes your savings, home equity, retirement accounts, and investments. If a court judgment exceeds your policy, plaintiffs come after your assets next.

| Your Net Worth | Minimum Recommended Liability | Why |

|---|---|---|

| Under $50,000 | 50/100/50 | Protects wages and basic savings |

| $50,000–$150,000 | 100/300/100 | Covers most serious accident scenarios |

| $150,000–$500,000 | 100/300/100 + umbrella policy | Home equity is at risk without it |

| $500,000+ | 250/500/250 + umbrella policy | Multiple assets need layered protection |

The Insurance Information Institute states directly: “If you’re found legally responsible for bills that are more than your insurance covers, you will have to pay the difference out of your own pocket. These costs could wipe you out.”

What Experts Actually Recommend

Insurance professionals universally recommend 100/300/100 as the practical minimum for most American drivers — that’s 4x what most state minimums require.

Here’s the real cost difference:

- State minimum coverage (25/50/25): ~$807/year nationally

- 100/300/100 coverage: ~$1,100–$1,300/year nationally

- Extra protection: just $25–$40/month more for 4x the financial safety net

That’s less than a streaming subscription to protect your home, savings, and wages.

High-Risk Situations That Demand Higher Limits

If any of these apply to you, increase your liability limits immediately:

- You own a home — equity can be seized to satisfy court judgments

- You have retirement savings — in some states, 401(k)s and IRAs are not fully protected

- You drive in a metro area — higher traffic = higher accident probability

- You have a teen driver on your policy — accident risk is 3x higher for drivers under 25

- You drive for rideshare — personal liability coverage may be suspended during active rides

What This Means For You: If you’re also managing a mortgage or planning a home purchase, unexpected liability costs can derail your financial plan entirely. Use our home affordability calculator to factor insurance costs into your monthly housing budget.

Should You Add an Umbrella Policy?

An umbrella policy kicks in when your auto liability limits are exhausted. It typically provides $1–$5 million in additional coverage for roughly $150–$300/year — often the most cost-effective financial protection available.

- ✅ Covers judgments above your auto policy limits

- ✅ Also extends to your homeowner’s liability coverage

- ✅ Covers legal defense costs in excess liability lawsuits

- ✅ Best for anyone with a net worth over $150,000

Liability Car Insurance Cost in 2026 — What You’ll Actually Pay

2026 National Average Rates (Real Data)

Per Insurify’s February 2026 rate analysis:

- National average liability-only: $100/month ($1,200/year)

- GEICO cheapest minimum coverage: ~$43/month

- Travelers: ~$50/month for minimum liability

- Full coverage national average: $178/month ($2,136/year)

Good news for 2026: after three years of sharp rate increases (premiums rose over 50% from 2020–2025), rates held steady in January–February 2026.

Liability Car Insurance Cost by Driver Profile

| Driver Profile | Avg. Monthly Liability Cost | Key Factor |

|---|---|---|

| Clean record, age 35 | ~$67/month | Baseline |

| Teen driver (added to family policy) | ~$101/month | High accident risk |

| Senior driver (age 65+) | ~$87/month | Rising medical costs |

| At-fault accident on record | ~$103/month | Risk surcharge |

| DUI conviction | $150–$300/month | High-risk designation |

| Poor credit score | +40–72% above baseline | Varies by state |

Note: California, Hawaii, and Massachusetts prohibit using credit scores to set auto insurance rates.

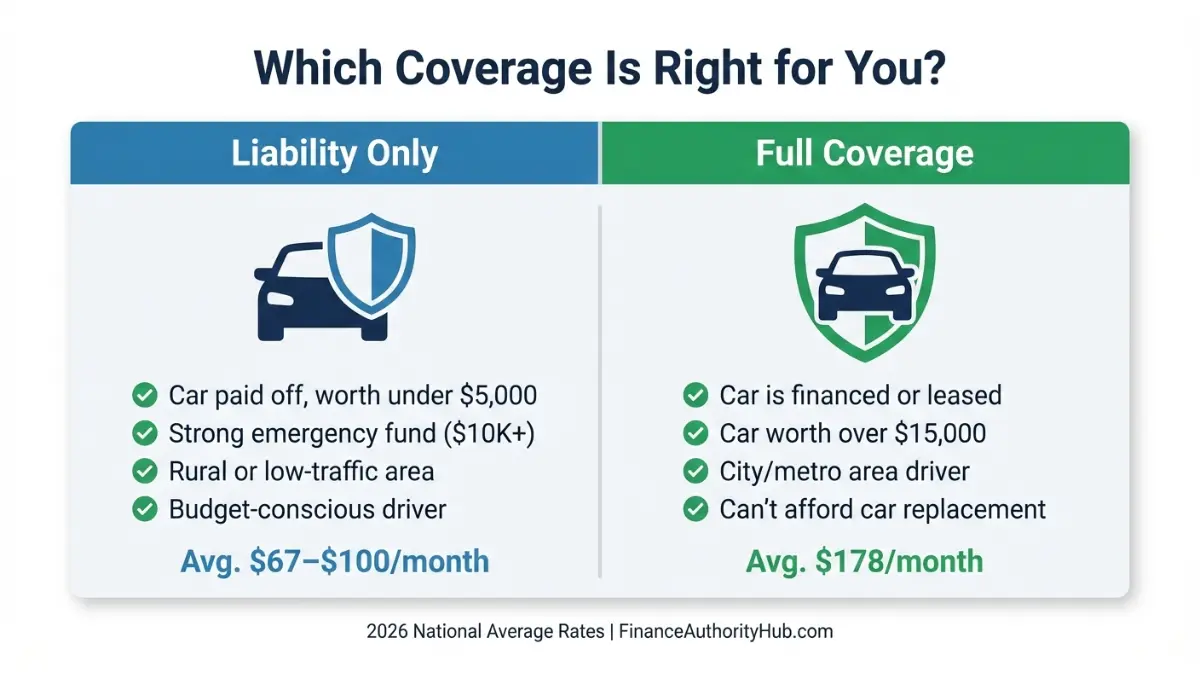

Liability vs. Full Coverage: Quick Decision Guide

| Choose Liability-Only If | Choose Full Coverage If |

|---|---|

| Car is paid off and worth under $5,000 | Car is financed or leased (lender requires it) |

| You have $10,000+ emergency fund | Car is worth more than $15,000 |

| Low-traffic, rural area | High-traffic metro area |

| You can afford to replace your vehicle | Replacing it would cause financial hardship |

If you’re comparing your comprehensive car insurance options alongside liability coverage, understanding what each covers is essential before you choose.

5 Proven Ways to Lower Your Liability Premium

- Bundle auto + home insurance with the same insurer: save 5–10%

- Complete an approved defensive driving course: save up to 10% in most states

- Maintain a clean driving record for 3+ years: unlocks good-driver discounts

- Compare quotes from at least 3 insurers annually: rates for the same coverage can vary 40%+

- Raise deductibles on collision/comprehensive: frees budget for higher liability limits (note: liability coverage itself has no deductible)

For more strategies on cutting auto insurance costs, see our deep-dive guide on how to cut car insurance costs 34% in 2026.

You may also want to explore affordable car insurance options to find the best rates in your state without sacrificing protection.

Frequently Asked Questions about Liability Car Insurance

1: What does liability car insurance cover?

Liability car insurance covers bodily injuries and property damage you cause to others in an at-fault accident. It pays for the other driver’s medical bills, lost wages, vehicle repairs, and your legal defense if you’re sued. It does not cover your own injuries or vehicle damage.

2: Is liability car insurance required in every state?

Every U.S. state except New Hampshire requires minimum liability car insurance to drive legally. New Hampshire allows drivers to instead prove financial responsibility. As of 2026, New Jersey and North Carolina have both raised their minimum liability limits.

3: What does 25/50/25 liability insurance mean?

It means your policy covers $25,000 per injured person, $50,000 total per accident for bodily injury, and $25,000 for property damage. This is one of the most common state minimums — and dangerously low for any accident involving multiple people or serious injuries.

4: What happens if accident costs exceed my liability limits?

Once your liability limits are exhausted, you become personally responsible for all remaining costs. Courts can garnish wages, freeze bank accounts, or place liens on your home or property to satisfy a judgment. This can last years and severely damage your financial stability.

5: What is the difference between liability and full coverage car insurance?

Liability-only insurance covers damage and injuries you cause to others. Full coverage adds collision insurance (repairs your own car after a crash) and comprehensive insurance (theft, weather, vandalism). For a full breakdown, see our guide on comprehensive car insurance.

6: How much does liability car insurance cost per month in 2026?

The national average is $100/month as of February 2026, per Insurify data. GEICO offers the cheapest minimum liability at roughly $43/month. Your rate depends on your state, age, driving history, credit score (in most states), and coverage limits selected.

7: What is bodily injury liability coverage?

Bodily injury liability (BIL) pays for the medical expenses, lost wages, and pain and suffering of people you injure in an at-fault accident. It also covers your legal defense costs if you are sued for damages caused in the crash.

8: Can I be sued personally even if I have liability insurance?

Yes. If the accident costs exceed your policy limits, the injured party can sue you personally for the difference. Courts may order wage garnishment, bank account levies, or property liens. Higher liability limits and an umbrella policy protect against this outcome.

9: Should I carry more than the state minimum liability coverage?

Strongly yes. The Insurance Information Institute warns that state minimums are often exhausted quickly in serious accidents. Insurance professionals recommend at least 100/300/100 for most drivers — the extra cost is typically $25–$40/month.

10: What is an umbrella policy and do I need one?

An umbrella policy provides $1–$5 million in additional liability coverage beyond your auto and home insurance limits. It typically costs $150–$300/year. If your net worth exceeds $150,000 — including home equity, savings, or retirement accounts — an umbrella policy is strongly worth considering.

11: Does my liability car insurance cover me in a rental car?

Your personal liability car insurance generally extends to rental vehicles in the same way it applies to your own car — protecting others you injure or property you damage. However, it does not cover damage to the rental vehicle itself. For that, you need collision coverage or the rental company’s own damage waiver.

Disclaimer

This article is intended for educational and informational purposes only and does not constitute financial, legal, or insurance advice. Coverage requirements, premium rates, and state minimum requirements vary and change frequently. Always consult a licensed insurance professional or your state’s Department of Insurance before making any coverage decisions. Rate data referenced reflects national averages as reported by Insurify as of February 2026 and individual rates will vary based on personal circumstances, driving history, location, and insurer.

Related reading: Affordable Car Insurance | Comprehensive Car Insurance Guide | Car Insurance: Cut Costs 34% | Liability Insurance Explained | Temporary Car Insurance Options

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.