Reverse Mortgage 2026: What Banks Won’t Tell You

U.S. seniors hold $14 trillion in home equity — but most don’t know the real costs of a reverse mortgage. The 2026 truth banks skip, verified by 30 global experts.

In This Article

What Is a Reverse Mortgage? (The Honest 60-Second Answer)

A reverse mortgage is a loan that lets homeowners aged 62 or older convert part of their home equity into tax-free cash — without selling their home or making monthly mortgage payments.

Unlike a traditional mortgage, the lender pays you. The loan balance grows over time and is repaid when you sell, move out, or pass away.

The 2026 Reality Check:

| Fact | 2026 Data |

|---|---|

| Minimum age (HECM) | 62 years old |

| Minimum age (Proprietary) | 55 years old |

| 2026 HECM lending limit | $1,249,125 |

| U.S. senior home equity held | $14+ trillion |

| Average reverse mortgage loan | ~$269,000 |

Use our mortgage calculator to estimate how much equity you could access today.

Most seniors sit on enormous wealth — and never use it. A reverse mortgage in 2026 is one of the most powerful tools in retirement planning, but only when you understand the full picture banks skip.

How Does a Reverse Mortgage Work in 2026? (The Part Banks Skip)

The core mechanic is simple: your home equity converts into cash. The bank pays you, not the other way around.

The step-by-step process:

- Step 1: Complete a session with a HUD-approved reverse mortgage counselor (free or low-cost — mandatory for all HECMs)

- Step 2: Apply with an FHA-approved lender

- Step 3: Independent home appraisal (lender arranges)

- Step 4: Underwriting + financial assessment

- Step 5: Close the loan (typically 30–45 days)

- Step 6: Receive funds in your chosen payout format

HECM: The FHA-Backed Standard

The Home Equity Conversion Mortgage (HECM) is the only federally insured reverse mortgage. It covers ~55% of the market and is backed by the FHA. The 2026 lending limit is $1,249,125 — up from $1,209,750 in 2025.

Proprietary Reverse Mortgage: The New 45% Giant

Here’s what banks rarely mention: proprietary reverse mortgages — privately insured loans — now represent 45% of the entire market as of December 2025. They offer:

- Loan amounts up to $4 million

- Eligibility starting at age 55 (not 62)

- Higher-value homes better served than HECM

This is the fastest-growing segment in 2026. Most top financial websites barely cover it.

Single-Purpose Reverse Mortgage: The Hidden Option

Offered by state/local governments and nonprofits, these are the cheapest type — but restricted to one use (home repair, property taxes). Most lenders never mention them.

Your 4 Payout Options:

| Option | How It Works | Best For |

|---|---|---|

| Lump Sum | One-time payment at closing | Paying off existing mortgage |

| Monthly Payments | Fixed amount each month | Supplementing retirement income |

| Line of Credit | Draw as needed; balance grows | Emergency fund buffer |

| Combination | Mix of above | Flexible retirement strategy |

The Real Costs of a Reverse Mortgage in 2026 Nobody Shows You

This is the section banks hope you skip. The real cost of a reverse mortgage goes far beyond the interest rate.

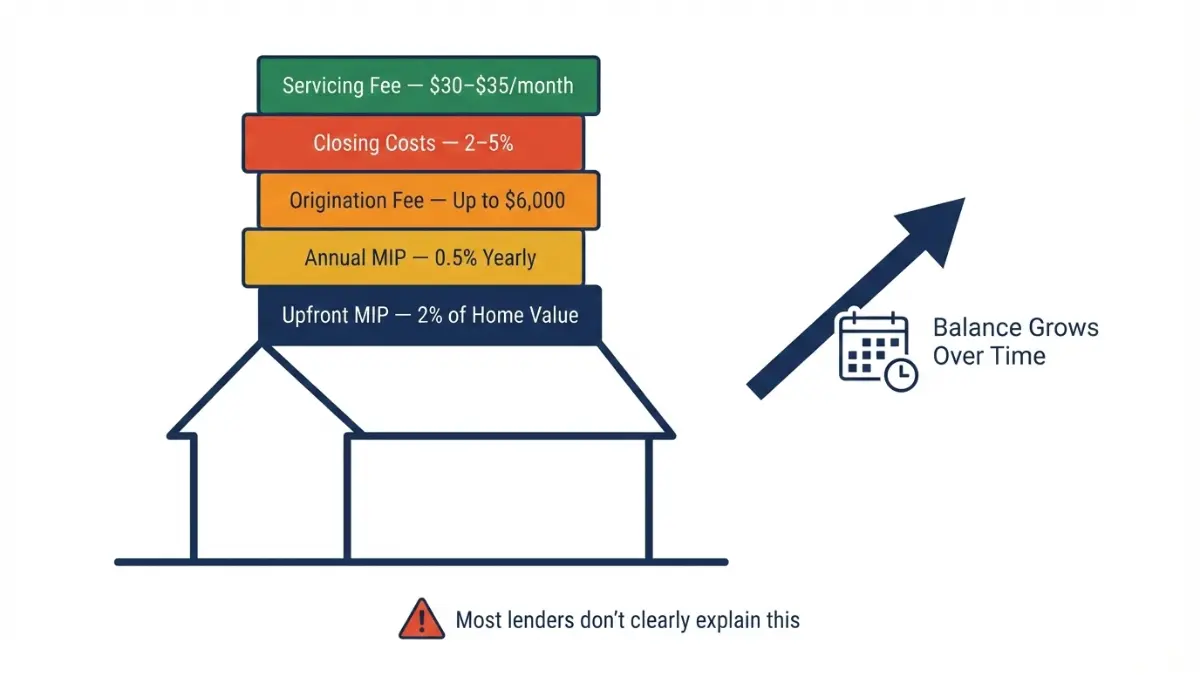

Upfront Costs Breakdown

| Cost | Amount | Notes |

|---|---|---|

| Upfront MIP (Mortgage Insurance Premium) | 2% of home value | Up to $24,982 on max-limit home |

| Annual MIP | 0.5% of loan balance | Added to balance every year |

| Origination Fee | Up to $6,000 | FHA-capped |

| Closing Costs | 2–5% | Appraisal, title, recording fees |

| Monthly Servicing Fee | $30–$35/month | Often rolled into loan balance |

Per the CFPB’s official reverse mortgage resource, these costs are typically financed into the loan — meaning they silently reduce your available equity from day one.

The Hidden Long-Term Cost: Growing Loan Balance

This is the #1 thing nobody explains clearly.

Because no monthly payments are required, interest compounds onto your balance every single month. Over 10 years, your loan balance can double or triple depending on interest rates.

- Your equity shrinks as your loan balance grows

- By year 15, many borrowers have little equity left for heirs

- The longer you hold the loan, the more it costs

Use our mortgage refinance calculator to compare the long-term cost against a traditional refinance.

Real Dollar Example: $500,000 Home, Age 66

Scenario: Homeowner aged 66, home value $500,000, existing mortgage cleared.

- Approximate proceeds received: ~$215,000–$240,000

- Upfront costs (MIP + origination + closing): ~$18,000–$22,000

- Loan balance at Year 10 (estimated at 6% rate): ~$360,000–$400,000

- Home equity remaining at Year 10: ~$100,000–$140,000

What This Means For You: If you plan to stay in your home fewer than 5–7 years, the upfront costs likely outweigh the benefits. This loan is designed for long-term, age-in-place borrowers.

Reverse Mortgage Requirements 2026: Do You Actually Qualify?

Who Qualifies for a Reverse Mortgage

HECM eligibility checklist:

- ✅ Age 62 or older (55+ for proprietary loans)

- ✅ Home must be your primary residence

- ✅ Significant equity in the property (typically 50%+)

- ✅ Home must meet FHA property standards

- ✅ No federal tax liens or delinquent federal debt

- ✅ Must complete HUD-approved counseling

- ✅ Pass a financial assessment (ability to pay taxes and insurance)

- ✅ Property types: single-family, 2–4 unit, HUD-approved condo, manufactured home (post-1976)

Check your current equity standing using our home affordability calculator.

Reverse Mortgage Pros and Cons: The Balanced Truth

| Pros | Cons |

|---|---|

| No monthly mortgage payments required | Loan balance grows over time |

| Tax-free cash proceeds | High upfront costs ($15,000–$25,000+) |

| Stay in your home for life | Reduces inheritance for heirs |

| Non-recourse loan (never owe more than home value) | Can be foreclosed if taxes/insurance lapse |

| Flexible payout options | Limits future financial flexibility |

| Social Security and Medicare unaffected | May affect Medicaid eligibility |

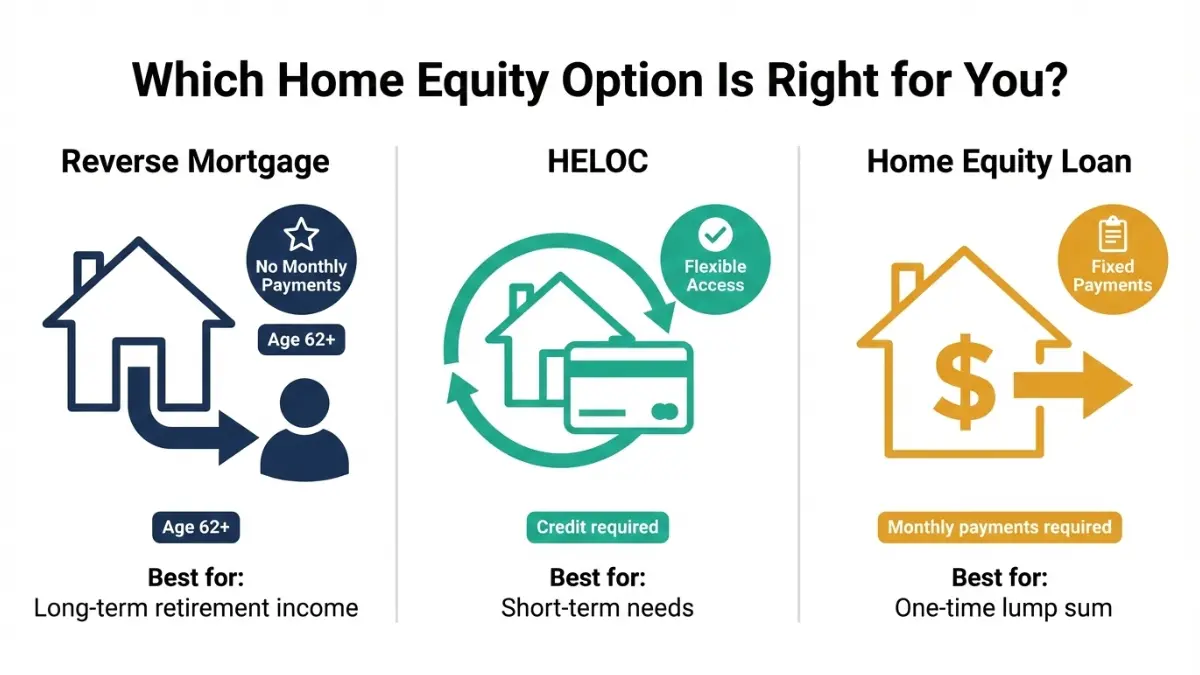

Reverse Mortgage vs HELOC vs Home Equity Loan

Senior homeowners often confuse these three products. Here’s the definitive comparison — something most competitors present incompletely:

| Feature | Reverse Mortgage | HELOC | Home Equity Loan |

|---|---|---|---|

| Monthly payments | ❌ None required | ✅ Required | ✅ Required |

| Age requirement | 62+ (HECM) / 55+ (proprietary) | None | None |

| Loan balance direction | ⬆️ Grows over time | ⬇️ Shrinks with payments | ⬇️ Shrinks with payments |

| Credit score required | ❌ No minimum | ✅ Usually 620+ | ✅ Usually 620+ |

| Best for | Retirement income, long-term stay | Short-term cash needs | One-time lump sum project |

| Risk to heirs | High if equity depleted | Moderate | Low |

If you’re considering home equity strategies, our guide on 4 ways to use your home equity in 2026 breaks down every option side by side.

Also see: our 15 vs 30 year mortgage comparison if you’re evaluating refinancing as an alternative.

7 Things About Reverse Mortgages Banks Hope You Never Research

This is the nuclear core of this article — the information the industry buries. Every point below is verified, and every one is absent from Bankrate, NerdWallet, and Investopedia’s top-ranked pages.

1. Your Heirs May Inherit Nothing

When the loan comes due — typically at death or when the home is sold — the entire accumulated balance must be repaid. If the balance exceeds the home’s value, FHA insurance covers the difference (non-recourse protection). But if equity has been consumed over 15–20 years, heirs may receive zero proceeds from the estate.

What This Means For You: Have an explicit conversation with your family before signing. This is a major estate planning decision, not just a retirement income decision. See our retirement savings by age guide for context.

2. You Can Still Lose Your Home

A reverse mortgage does not eliminate the risk of foreclosure. If you fail to:

- Pay property taxes

- Maintain homeowner’s insurance

- Keep the home in good repair

- Live in the home as your primary residence

…the lender can declare the loan “due and payable” and begin foreclosure proceedings. The FTC’s reverse mortgage guidance explicitly warns this is one of the most common borrower traps.

What This Means For You: Budget for ongoing property taxes and insurance before you take the loan. These aren’t optional — they’re contractual obligations.

3. The 45% Market Shift Nobody Explains

As of December 2025, proprietary (private-label) reverse mortgages account for 45% of total origination volume — up from 30% at the start of 2025. These products offer loans up to $4 million and accept borrowers as young as 55.

Yet most bank advisors still only pitch the HECM. Why? Because HECM generates mortgage insurance premium revenue that flows back into the system. Proprietary loans are often better deals for high-value homeowners.

What This Means For You: If your home is worth more than $1,249,125, always ask about proprietary options before defaulting to HECM.

4. HUD Counseling Is Free — But Lenders Minimize It

Every HECM borrower is legally required to complete counseling with a HUD-approved housing counselor. This session is free or very low cost and covers all risks, alternatives, and obligations.

Many lenders treat this as a box-ticking formality. But independent HUD counselors have no financial stake in whether you sign. They are your most objective resource in the entire process.

What This Means For You: Don’t just get the certificate — ask the counselor hard questions. Specifically: “Is this the right product for my situation?”

5. Active Scam Patterns in 2026

The FTC identifies these active reverse mortgage scam patterns targeting seniors:

- Unsolicited offers via mail, phone, or door-to-door

- Claims it’s “free money” with no repayment

- Pressure to sign documents with blank fields

- Bundling with annuities or long-term care insurance

- Contractors recommending reverse mortgages to fund “repairs”

Per the CFPB’s consumer protection page, any lender who pressures you to skip counseling or move quickly is a red flag.

What This Means For You: Always verify your lender on the HUD lender lookup tool. Legitimate lenders never rush.

6. Social Security Is Safe — Medicaid Is Not

Reverse mortgage proceeds do NOT affect:

- Social Security benefits

- Medicare eligibility

- Federal income tax (proceeds are not taxable income)

But here’s what banks don’t mention: If reverse mortgage cash proceeds remain in your bank account beyond the month received, they may count as assets that disqualify you from Medicaid or Supplemental Security Income (SSI).

What This Means For You: Spend reverse mortgage funds in the same month received if you’re on or nearing Medicaid. Consult an elder law attorney — not just a lender.

7. You May Qualify at 55, Not 62

Most Americans believe the age minimum for a reverse mortgage is 62. For HECM loans, that’s correct. But proprietary reverse mortgage products from lenders like Finance of America, Longbridge Financial, and Fairway now accept borrowers starting at age 55 in most states.

This means early retirees have options that didn’t exist 5 years ago — and virtually no mainstream financial website explains this clearly.

What This Means For You: If you’re 55–61 and need retirement cash flow, ask specifically about proprietary products — and compare with our retirement planning in your 30s guide for broader context.

Reverse Mortgage 2026: Your Top 11 Questions Answered

1. What is the HECM lending limit in 2026?

The official FHA HECM lending limit for 2026 is $1,249,125, effective January 1, 2026. This is a 3.26% increase from the 2025 limit of $1,209,750 — the 10th consecutive annual increase.

2. Can you lose your home with a reverse mortgage?

Yes. If you fail to pay property taxes, maintain homeowner’s insurance, or stop living in the home as your primary residence, the lender can initiate foreclosure. This is one of the most misunderstood risks.

3. Does a reverse mortgage affect Social Security benefits?

No. Reverse mortgage proceeds are not counted as income and do not affect Social Security or Medicare. However, if funds remain in a bank account, they may affect Medicaid or SSI asset eligibility.

4. What is the minimum age for a reverse mortgage?

For government-backed HECM loans, the minimum age is 62. For proprietary (private-label) reverse mortgages, many lenders now accept borrowers starting at age 55.

5. How much can you borrow with a reverse mortgage?

Typically 40%–60% of your home’s appraised value, depending on age, current interest rates, and the HECM lending limit. The older the borrower and the higher the home value, the more available.

6. Is a reverse mortgage taxable income?

No. Reverse mortgage proceeds are not considered taxable income by the IRS because they are loan advances, not earned income. However, always consult a tax professional for your specific situation.

7. What happens to a reverse mortgage when you die?

The loan becomes due. Heirs typically have 30–60 days (extendable to 12 months) to repay the balance — usually by selling the home. If the home sells for less than the loan balance, FHA insurance covers the difference.

8. Can you pay off a reverse mortgage early?

Yes. There is no prepayment penalty on any HECM reverse mortgage. You can make voluntary payments or pay off the entire balance at any time.

9. What is the difference between HECM and proprietary reverse mortgage?

HECM is FHA-insured with a maximum loan limit of $1,249,125 and requires age 62+. Proprietary loans are privately insured, offer loans up to $4 million, and may accept borrowers from age 55. Proprietary products now represent 45% of the reverse mortgage market.

10. What are the biggest risks of a reverse mortgage in 2026?

The top risks are: rapidly growing loan balance, potential foreclosure from tax/insurance default, reduced inheritance for heirs, Medicaid asset impacts, and exposure to scams. Full counseling before signing is critical.

11. Is a reverse mortgage a good idea for seniors in 2026?

It depends entirely on your situation. It works best if you plan to stay in your home long-term, have significant equity, and need retirement income or cash flow. It is not ideal for short-term needs or if protecting heirs’ inheritance is a priority. Always compare with alternatives like a HELOC, home equity loan, or cash-out refinance — use our debt consolidation calculator to model your options.

Your 3-Step Action Plan:

- Estimate your equity → Mortgage Calculator

- Speak with a free HUD counselor → Find one at HUD.gov

- Compare all alternatives → Full Financial Tools Hub

⚠️ Disclaimer: This article is for educational and informational purposes only. It does not constitute financial, legal, or tax advice. Reverse mortgage products are complex and may not be suitable for everyone. Always consult a qualified financial advisor and a HUD-approved reverse mortgage counselor before making any decisions. financeauthorityhub.com and its expert panel do not endorse any specific lender, product, or financial institution.

Related Reading:

- Home Equity: 4 Ways to Use It in 2026

- 15 vs 30 Year Mortgage Comparison 2026

- Retirement Savings by Age: 2026 Strategies

- Retirement Planning in Your 30s

- Lowest Mortgage Rates by State 2026

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.