AGI 2026: Lower Line 11 & Save $3,800+ (Form 1040)

Your adjusted gross income on Form 1040 Line 11 determines tax credits worth thousands. Learn how to reduce your AGI in 2026 using IRA contributions, HSA limits, and above-the-line deductions.

In This Article

Your adjusted gross income determines whether you qualify for thousands of dollars in tax credits, retirement contributions, and deductions. Understanding how to calculate and reduce your AGI on Form 1040 Line 11 can unlock significant tax savings in 2026—potentially $3,800 or more through strategic planning.

What Is Adjusted Gross Income (AGI) on Your 2026 Tax Return?

Adjusted gross income (AGI) is your total income from all sources minus specific IRS-approved adjustments. It appears on Line 11 of Form 1040 and serves as the foundation for calculating your tax liability, determining eligibility for tax credits, and qualifying for retirement account contributions.

AGI differs from both gross income and taxable income. Your gross income includes every dollar you earn from wages, investments, business income, and other sources. After subtracting certain deductions—called “above-the-line” deductions—you arrive at your AGI. Then, after subtracting either the standard deduction ($16,100 for single filers in 2026) or itemized deductions, you reach your taxable income.

Here’s how these three income types relate:

| Income Type | Definition | Where It Appears |

|---|---|---|

| Gross Income | Total income from all sources | Form 1040 Line 9 |

| AGI | Gross income minus adjustments | Form 1040 Line 11 |

| Taxable Income | AGI minus standard/itemized deductions | Form 1040 Line 15 |

Your AGI matters because it determines eligibility for 18+ tax benefits. Lower your AGI, and you may qualify for larger tax credits, higher retirement contributions, and additional deductions. According to IRS data, taxpayers who strategically reduce their AGI save an average of $3,200 annually through expanded tax benefit eligibility.

For 2026, new provisions under recent tax legislation include a $6,000 bonus deduction for seniors with modified AGI below certain thresholds, plus exclusions for overtime and tip income under specific circumstances. These changes make AGI optimization more valuable than ever.

Step-by-Step: Calculating AGI on Form 1040 (2026 Tax Year)

The AGI Calculation Formula

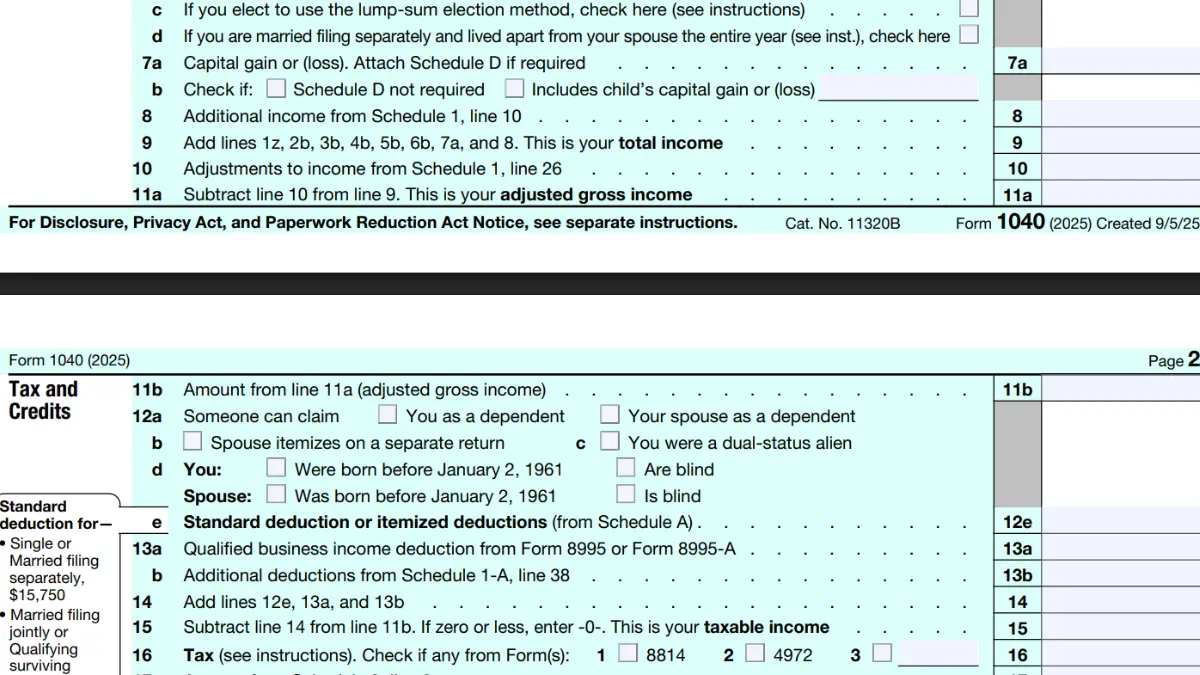

Calculating your AGI follows a straightforward three-step process on Form 1040. The formula is simple: Total Income (Line 9) – Adjustments to Income (Line 10) = Adjusted Gross Income (Line 11).

Start by adding all taxable income sources. Include wages from your W-2, freelance income from 1099 forms, business profits, rental income, investment gains, retirement distributions, and taxable Social Security benefits. Everything flows to Line 9.

Next, subtract eligible adjustments from Schedule 1. These “above-the-line” deductions reduce your AGI without requiring you to itemize. The result on Line 11 is your AGI—the number that unlocks tax-saving opportunities.

Form 1040 Line-by-Line Breakdown

Line 9: Total Income includes:

- W-2 wages and salaries

- Interest and dividends from investments

- Business income (Schedule C)

- Capital gains and losses

- Retirement account distributions

- Rental and royalty income (Schedule E)

- Unemployment compensation

- Taxable Social Security benefits

Line 10: Adjustments come from Schedule 1, Part II and include:

- IRA contributions ($7,500 limit for 2026)

- Student loan interest ($2,500 maximum)

- Health Savings Account contributions

- Self-employment tax deduction (50%)

- Self-employed health insurance premiums

- Educator expenses ($300 per eligible teacher)

Line 11: Your AGI = Line 9 minus Line 10

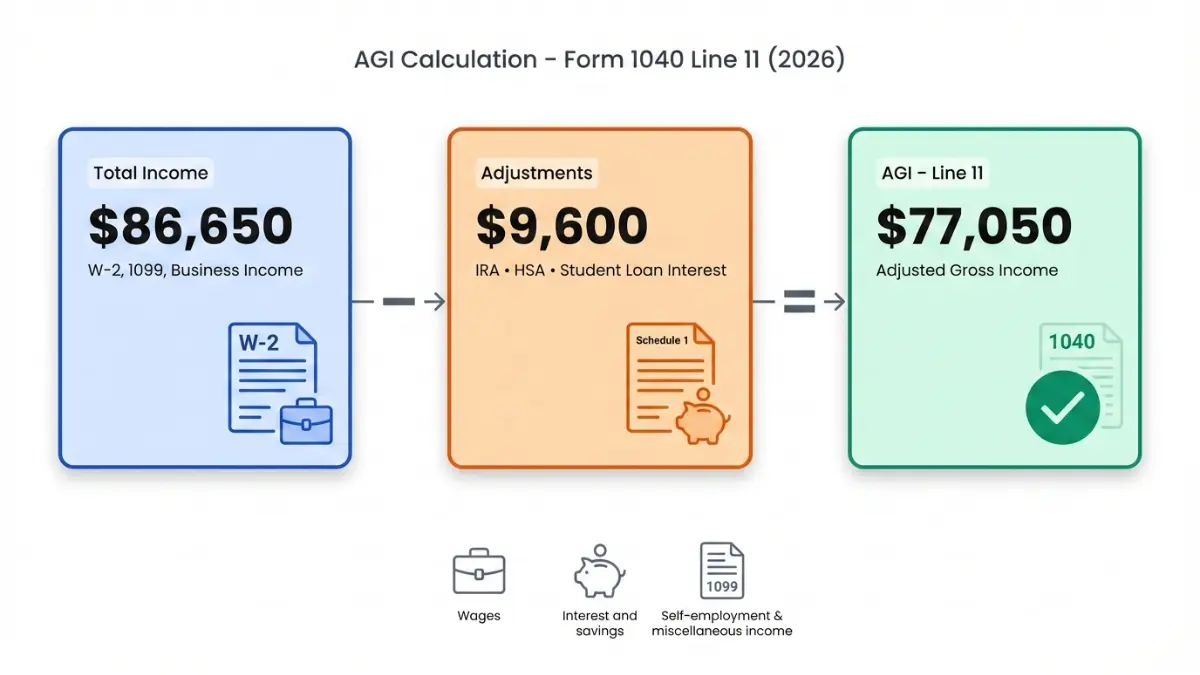

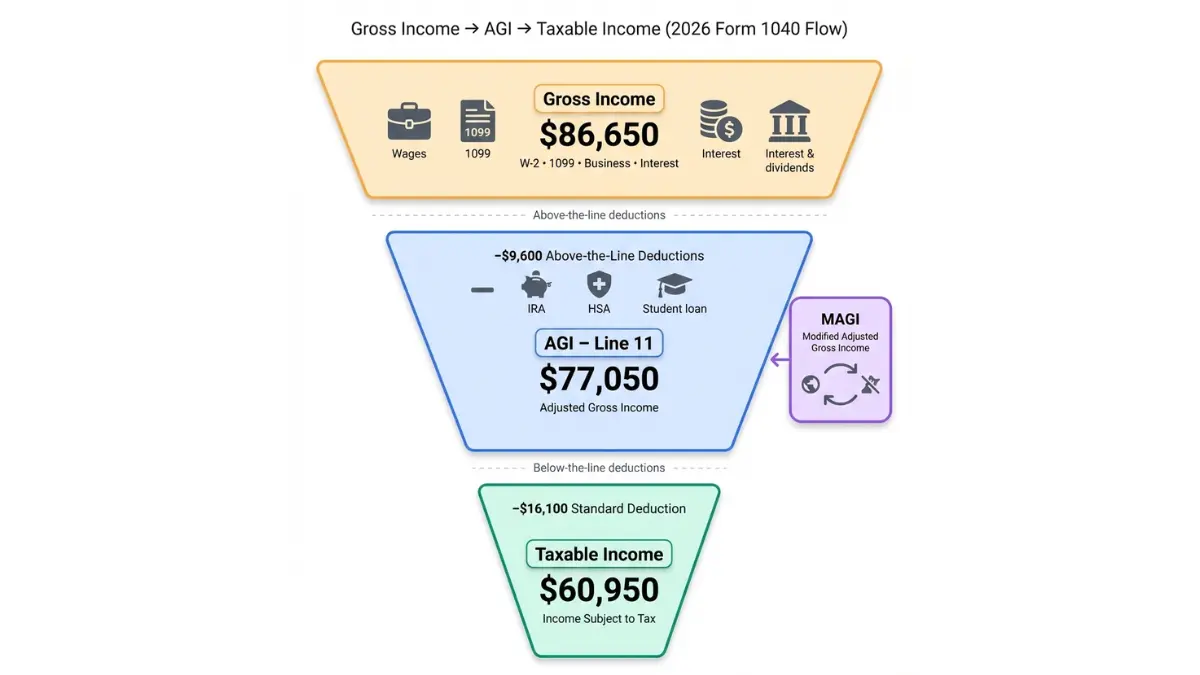

Real Example: $85,000 Salary Earner

Sarah, a single teacher in California, earned $85,000 in 2026. Here’s how she calculated her AGI:

Total Income (Line 9):

- Salary: $85,000

- Bank interest: $450

- Stock dividends: $1,200

- Total: $86,650

Adjustments (Line 10) via Schedule 1:

- Traditional IRA contribution: $7,500

- Educator expenses: $300

- Student loan interest: $1,800

- Total adjustments: $9,600

AGI (Line 11): $86,650 – $9,600 = $77,050

By maximizing her above-the-line deductions, Sarah reduced her AGI by $9,600. This lower AGI helped her qualify for a larger retirement contribution deduction and positioned her below several tax credit phase-out thresholds.

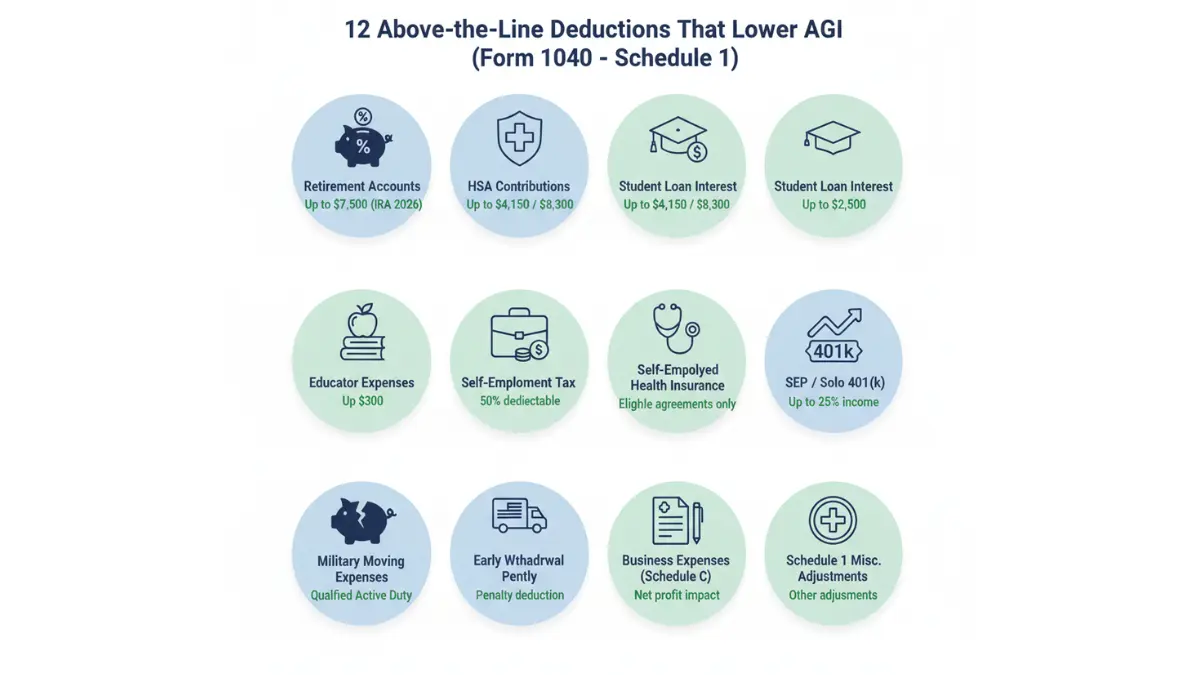

How to Lower Your AGI: Above-the-Line Deductions for 2026

Reducing your AGI requires strategic use of above-the-line deductions—adjustments you can claim regardless of whether you itemize. These deductions appear on Schedule 1 and directly reduce Line 11 of your Form 1040.

Retirement Contributions (IRA, 401k, SEP)

Traditional IRA contributions offer one of the most powerful AGI reduction strategies. For 2026, you can contribute up to $7,500 ($8,600 if age 50 or older) and deduct the full amount if you meet income requirements.

Deduction eligibility depends on whether you’re covered by a workplace retirement plan. If you have no workplace plan, you can deduct the full contribution regardless of income. With workplace coverage, the deduction phases out based on modified AGI:

- Single filers: Full deduction if MAGI is $79,000 or less; phased out between $79,001-$89,000

- Married filing jointly: Full deduction if MAGI is $126,000 or less; phased out between $126,001-$146,000

For self-employed individuals, SEP-IRA contributions can reach $69,000 in 2026 (or 25% of compensation), providing substantial AGI reduction for high earners.

Health Savings Account (HSA) Contributions

HSA contributions deliver a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. For 2026, contribution limits increased to:

- Individual coverage: $4,400 (up from $4,300 in 2025)

- Family coverage: $8,750 (up from $8,550 in 2025)

- Age 55+ catch-up: Additional $1,000

To qualify, you must have a high-deductible health plan (HDHP) with minimum deductibles of $1,650 for individuals or $3,300 for families. HSA contributions reduce your AGI dollar-for-dollar and provide long-term health insurance planning benefits.

Student Loan Interest Deduction

You can deduct up to $2,500 in student loan interest paid during 2026, even if you take the standard deduction. This deduction reduces your AGI and doesn’t require itemization.

Income limits apply. The deduction phases out for single filers with MAGI between $80,000-$95,000 and married couples filing jointly with MAGI between $165,000-$195,000. Track interest payments on Form 1098-E from your loan servicer.

Educator Expenses

K-12 teachers, instructors, counselors, and principals who work at least 900 hours during the school year can deduct up to $300 in unreimbursed classroom expenses. Married educators filing jointly can deduct up to $600 total (maximum $300 each).

Qualifying expenses include books, supplies, equipment, software, and professional development courses. Keep receipts and documentation for purchases like classroom technology, supplementary materials, and COVID-19 protective items.

Self-Employment Deductions

Self-employed individuals access several powerful AGI reducers:

Self-employment tax deduction: Deduct 50% of your self-employment tax (Social Security and Medicare). If you paid $8,000 in self-employment tax, you can deduct $4,000 from your AGI.

Self-employed health insurance: Deduct 100% of health insurance premiums paid for yourself, spouse, and dependents. This includes medical, dental, and qualified long-term care insurance.

Retirement plan contributions: Self-employed workers can establish SEP-IRAs, SIMPLE IRAs, or solo 401(k) plans with higher contribution limits than traditional IRAs.

Other AGI-Reducing Strategies

Additional above-the-line deductions for 2026 include:

- Alimony payments (for divorce agreements finalized before 2019)

- Moving expenses (active-duty military only)

- Early withdrawal penalties from certificates of deposit

- Jury duty pay given to your employer

- Certain business expenses for reservists, performing artists, and fee-basis government officials

The key to maximizing AGI reduction is stacking multiple deductions strategically. Understanding your income tax brackets helps you target the optimal AGI range.

AGI vs MAGI vs Taxable Income: Critical Differences

Understanding the distinction between AGI, modified adjusted gross income (MAGI), and taxable income prevents costly mistakes when claiming tax benefits.

Modified Adjusted Gross Income (MAGI) Explained

MAGI is your AGI with certain deductions added back. The specific add-backs vary depending on which tax benefit you’re calculating. Common MAGI add-backs include:

- Student loan interest deduction

- IRA contributions

- Foreign earned income exclusion

- Tax-exempt interest from municipal bonds

- Excluded income from U.S. territories

For most taxpayers, MAGI equals AGI. You only need separate MAGI calculations when determining eligibility for specific credits or contributions—like Roth IRA eligibility or premium tax credits for health insurance.

How Taxable Income Differs from AGI

Taxable income is what remains after subtracting either the standard deduction or itemized deductions from your AGI. This is the final number used to calculate your actual tax bill using the 2026 tax brackets.

Here’s the calculation flow:

- Gross Income (all income sources)

- Subtract above-the-line deductions

- = AGI (Line 11 on Form 1040)

- Subtract standard deduction ($16,100 single) or itemized deductions

- = Taxable Income (Line 15 on Form 1040)

- Apply tax brackets to calculate tax owed

When Each Number Matters

Different tax benefits use different income measures:

| Tax Benefit | Uses AGI | Uses MAGI | Uses Taxable Income |

|---|---|---|---|

| IRA contribution limits | ✓ | ||

| Roth IRA eligibility | ✓ | ||

| Premium tax credits | ✓ | ||

| Child Tax Credit | ✓ | ||

| Student loan interest | ✓ | ||

| Medical expense deduction | ✓ | ||

| Tax bracket calculation | ✓ | ||

| Standard deduction | ✓ |

For 2026, the new senior deduction ($6,000 single / $12,000 married) phases out based on MAGI, not AGI. Single filers with MAGI above $75,000 see reduced benefits, with complete phase-out at $175,000.

Understanding these differences helps you optimize tax refund outcomes and avoid leaving money on the table.

Why Your AGI Determines These 18 Critical Tax Benefits

Your AGI serves as the gatekeeper for numerous tax credits, deductions, and contribution opportunities. Lower AGI opens doors to benefits that can save thousands annually.

Tax Credits Limited by AGI/MAGI

Earned Income Tax Credit (EITC): Working families with moderate incomes can claim this refundable credit. For 2026, maximum credits reach $8,046 for families with three or more qualifying children. MAGI limits apply based on filing status and number of children.

Child Tax Credit: Worth $2,000 per qualifying child under age 17, this credit begins phasing out at $200,000 MAGI for single filers and $400,000 for married couples. The refundable portion (Additional Child Tax Credit) can return up to $1,700 per child.

Premium Tax Credit: If you purchase health insurance through the ACA marketplace, lower MAGI qualifies you for larger subsidies. Premium tax credits can reduce monthly insurance costs by hundreds of dollars.

American Opportunity Credit: This education credit provides up to $2,500 per eligible student for the first four years of higher education. The credit phases out for single filers with MAGI between $80,000-$90,000 and joint filers between $160,000-$180,000.

Lifetime Learning Credit: Worth up to $2,000 per return for qualified education expenses, this credit phases out at the same MAGI thresholds as the American Opportunity Credit.

Deduction Eligibility Based on AGI

Medical and dental expense deduction: You can only deduct medical expenses exceeding 7.5% of your AGI. If your AGI is $80,000, you must have more than $6,000 in medical expenses to claim any deduction. Lower AGI means you can deduct more medical costs.

IRA contribution deductibility: If you’re covered by a workplace retirement plan, your ability to deduct traditional IRA contributions depends on MAGI. For 2026, single filers can fully deduct contributions with MAGI up to $79,000. The deduction phases out between $79,001-$89,000.

Student loan interest deduction: This $2,500 deduction phases out based on MAGI. Single filers lose eligibility between $80,000-$95,000 MAGI; married couples between $165,000-$195,000.

Contribution Limits Tied to AGI

Roth IRA contributions: High earners face MAGI limits. For 2026, single filers can make full contributions with MAGI below $150,000. Contributions phase out between $150,000-$165,000. Married couples filing jointly face phase-outs between $236,000-$246,000.

Adoption credit: This credit can reach $17,670 in 2026 but phases out for taxpayers with MAGI above certain thresholds.

Retirement Savings Contributions Credit (Saver’s Credit): Low-to-moderate income taxpayers can claim 10%, 20%, or 50% of retirement contributions as a credit, depending on AGI. For 2026, the credit is available to single filers with AGI up to $39,500 and joint filers up to $79,000.

Additional AGI-Dependent Factors

Beyond federal tax benefits, your AGI affects:

- State income taxes: Most states use federal AGI as the starting point for state tax calculations

- Medicare premiums: High earners pay Income-Related Monthly Adjustment Amounts (IRMAA) based on AGI from two years prior

- Net Investment Income Tax: A 3.8% surtax applies to investment income when MAGI exceeds $200,000 (single) or $250,000 (married)

- College financial aid: The FAFSA uses AGI to determine aid eligibility

- Social Security taxation: MAGI determines how much of your Social Security benefits are taxable

Strategic AGI management through tools like debt consolidation and retirement planning can position you for maximum tax benefits. Even small AGI reductions can trigger substantial savings across multiple programs.

7 Strategic Ways to Lower Your AGI & Save $3,800+ in 2026

Maximizing AGI reduction requires combining multiple strategies simultaneously. Here’s how to achieve $3,800+ in tax savings through strategic AGI optimization.

Max Out Retirement Contributions

Start by contributing the maximum to tax-advantaged retirement accounts. For 2026, you can contribute:

- Traditional IRA: $7,500 ($8,600 if age 50+)

- 401(k), 403(b), 457: $24,500 employee deferral ($33,500 with catch-up for age 50+)

- SEP-IRA (self-employed): Up to $69,000 or 25% of compensation

- SIMPLE IRA: $16,500 ($20,000 with catch-up)

Each pre-tax dollar contributed reduces your AGI by one dollar. A $7,500 IRA contribution directly cuts your AGI by $7,500, potentially saving $1,800+ in federal taxes alone (at the 24% bracket).

Strategic HSA/FSA Planning

Maximize health savings account contributions to achieve triple tax savings. For 2026:

- HSA individual: $4,400 contribution limit

- HSA family: $8,750 contribution limit

- FSA: $3,400 maximum (with $680 carryover allowed)

Unlike FSAs, HSA funds roll over indefinitely and can be invested for growth. After age 65, you can withdraw HSA funds for any purpose (taxed as ordinary income), making HSAs a powerful retirement planning tool.

Timing Income and Deductions

Strategic timing can significantly impact your AGI:

Defer income: If possible, delay year-end bonuses, freelance payments, or business income to the following tax year. This lowers current-year AGI while you’re in a higher bracket.

Accelerate deductions: Make January’s IRA contribution in December. Pay fourth-quarter estimated state taxes before December 31. Prepay January health insurance premiums in December.

Bunching strategy: For those near itemization thresholds, alternate between taking the standard deduction one year and itemizing the next. Concentrate charitable contributions and medical procedures in alternating years.

Gig Economy and Crypto Considerations

Modern income sources require special AGI attention:

1099 income optimization: Gig workers can deduct business expenses on Schedule C, reducing net business income before it hits AGI. Common deductions include home office expenses, mileage (67 cents per mile for 2026), equipment, and software subscriptions.

Crypto tax planning: Ordinary crypto income (staking rewards, mining, payment for services) increases AGI. Capital gains from selling crypto don’t hit AGI but affect other tax calculations. Consider tax-loss harvesting—selling crypto at a loss to offset gains and reduce AGI by up to $3,000 annually.

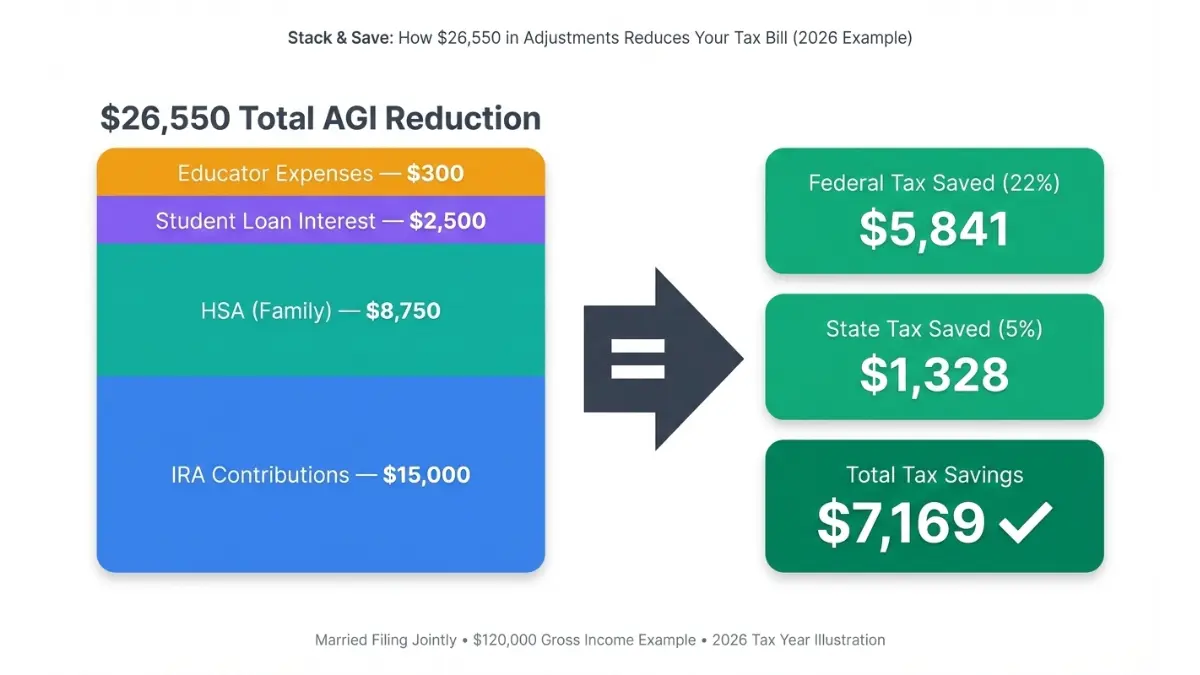

Advanced Optimization: The $3,800+ Savings Calculation

Combining strategies creates exponential benefits:

Example: A married couple earning $120,000 optimizes as follows:

- IRA contributions (both spouses): $15,000

- HSA contribution (family): $8,750

- Student loan interest: $2,500

- Educator expenses (one teacher spouse): $300

Total AGI reduction: $26,550

At a 22% marginal tax rate, this saves $5,841 in federal taxes. Add state tax savings of approximately 5%, and total savings exceed $7,000 annually.

Even conservative optimization saves substantial amounts. A single filer maximizing just IRA ($7,500) and HSA ($4,400) contributions reduces AGI by $11,900, saving $2,856 in federal taxes at the 24% bracket.

2026-Specific Opportunities

New for 2026, qualified tip and overtime income exclusions may reduce AGI for eligible workers. Seniors with MAGI below $75,000 (single) can claim an additional $6,000 deduction—effectively a $1,200-$1,800 tax savings.

The combination of traditional strategies with new 2026 provisions creates unprecedented AGI optimization potential. Strategic planning through professional tools and resources, including tax calculators and expert guidance, ensures you capture every available benefit.

Frequently Asked Questions About AGI

1. What is AGI on my tax return?

AGI (adjusted gross income) is your total income minus specific deductions allowed by the IRS. It appears on Line 11 of Form 1040 and determines eligibility for tax credits and deductions.

2. Where do I find my AGI from last year?

Look at Line 11 on your 2025 Form 1040, 1040-SR, or 1040-NR. You can also retrieve it from your IRS online account or last year’s tax return transcript.

3. Can my AGI be zero or negative?

Yes, if your adjustments equal or exceed your gross income. Negative AGI can occur with substantial business losses or above-the-line deductions exceeding income.

4. What’s the difference between AGI and gross income?

Gross income is all your income before any deductions. AGI is gross income minus specific “above-the-line” deductions like IRA contributions, HSA deposits, and student loan interest.

5. How does lowering my AGI help my taxes?

Lower AGI increases eligibility for tax credits, allows larger retirement contributions, reduces medical expense thresholds, and can lower your overall tax bracket. Each $1,000 AGI reduction can save $200-$370 in taxes depending on your bracket.

6. What are above-the-line deductions?

These are deductions you can take regardless of whether you itemize. They’re called “above-the-line” because they’re subtracted before arriving at AGI on Line 11, whereas itemized deductions come below that line.

7. Do I calculate AGI before or after standard deduction?

AGI is calculated before the standard deduction. The sequence is: gross income → subtract adjustments → AGI → subtract standard/itemized deduction → taxable income.

8. Can I change my AGI after filing?

You can file an amended return using Form 1040-X if you discover errors or missed deductions. However, you generally have three years from the original filing deadline to amend.

9. Does AGI include Social Security benefits?

Only the taxable portion of Social Security benefits is included in AGI. Depending on your total income, 0%, 50%, or 85% of benefits may be taxable.

10. What is MAGI and how is it different from AGI?

Modified AGI (MAGI) is AGI with certain deductions added back. The specific add-backs vary by tax benefit. MAGI determines eligibility for Roth IRAs, premium tax credits, and other benefits.

11. How do I reduce my AGI for 2026?

Maximize retirement contributions (IRA, 401k), contribute to an HSA, pay student loan interest, claim educator expenses if eligible, and consider self-employment deductions if applicable. Strategic timing of income and deductions also helps.

Disclaimer

This article is for educational purposes only and does not constitute financial, tax, or legal advice. Tax laws change frequently, and individual circumstances vary significantly. The information provided reflects tax year 2026 regulations as of February 2026 but may not account for subsequent legislative changes or IRS guidance updates.

Consult a licensed CPA, enrolled agent, or qualified tax professional for personalized guidance regarding your adjusted gross income, tax situation, and optimal filing strategies. The IRS provides official guidance at IRS.gov, and taxpayers should verify current regulations before making tax decisions.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.