30-Year vs 15-Year Mortgage: Which Saves You More Money in 2026?

A 15-year mortgage saves $293K in interest — but a 30-year could make you richer. See 2026 real rate data, expert panel verdict, and the hybrid strategy most lenders hide.

In This Article

A 15-year mortgage on a $400,000 loan at today’s rates saves you over $230,000 in total interest compared to a 30-year mortgage. But here’s the counterintuitive truth: a 30-year mortgage could make you wealthier — if you invest the monthly payment difference. The right answer depends entirely on your income, age, and financial discipline. Let’s break it down with real 2026 numbers.

The Real Numbers — 30-Year vs 15-Year Mortgage in 2026

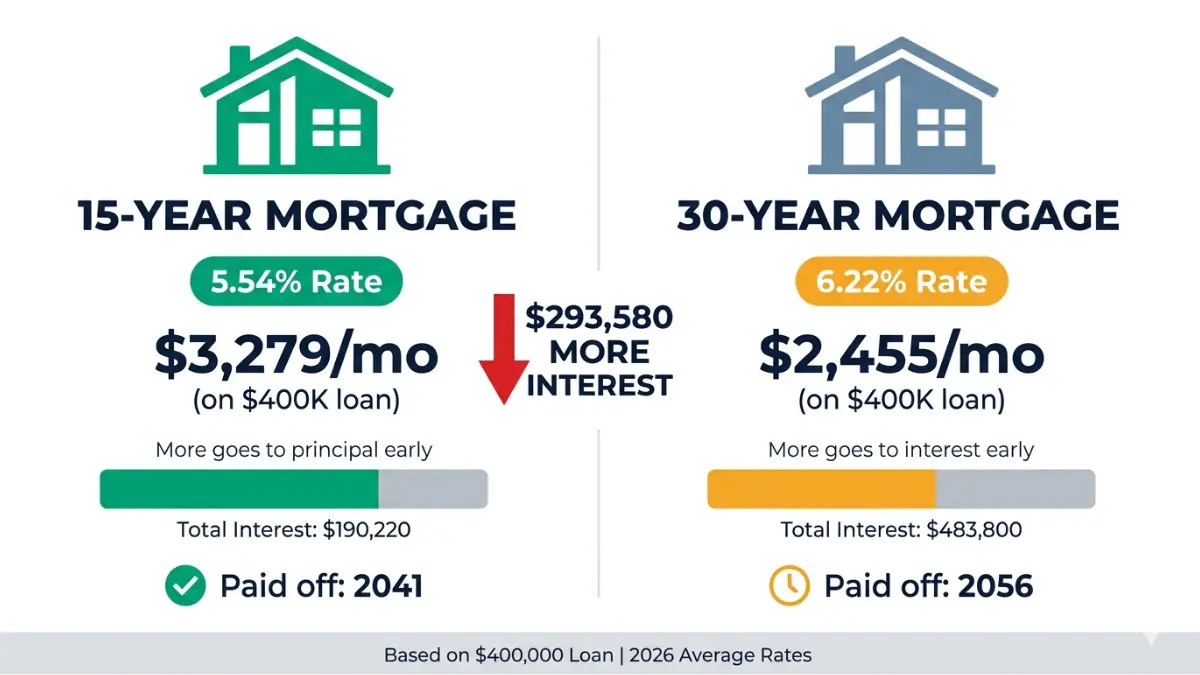

As of March 20, 2026, the average 30-year fixed-rate mortgage sits at 6.22%, while the average 15-year fixed-rate mortgage is 5.54% — a spread of 0.68%. That gap is smaller than it sounds but the compounding effect over decades is enormous.

Use our mortgage calculator to run your exact numbers. The table below uses live 2026 rates.

📊 2026 Comparison Table: 30-Year vs 15-Year Mortgage

| Loan Amount | 15-Yr Payment (5.54%) | 30-Yr Payment (6.22%) | Monthly Difference | Total Interest 15-Yr | Total Interest 30-Yr | Interest Saved |

|---|---|---|---|---|---|---|

| $300,000 | $2,459 | $1,841 | $618 | $142,620 | $362,760 | $220,140 |

| $400,000 | $3,279 | $2,455 | $824 | $190,220 | $483,800 | $293,580 |

| $500,000 | $4,098 | $3,068 | $1,030 | $237,640 | $604,480 | $366,840 |

Based on 2026 average rates. Taxes and insurance excluded.

Why 15-Year Mortgage Rates Are Always Lower

The shorter a loan’s term, the lower the risk of default from the borrower — so lenders reward 15-year borrowers with lower interest rates. A lower rate plus a shorter repayment window creates a compounding savings effect that’s hard to beat on paper.

Key takeaway: On a $400,000 loan, even the 0.68% rate advantage alone saves you over $58,000 before accounting for the shorter term. The combined effect wipes out nearly $294,000 in interest. Before deciding, check what you can realistically afford using our home affordability calculator.

The Real Wealth Question — Save Interest or Invest the Difference?

This is the question no competitor answers fully — and it’s the one that actually matters in 2026.

Does Paying Off Your Mortgage Faster Actually Make You Richer?

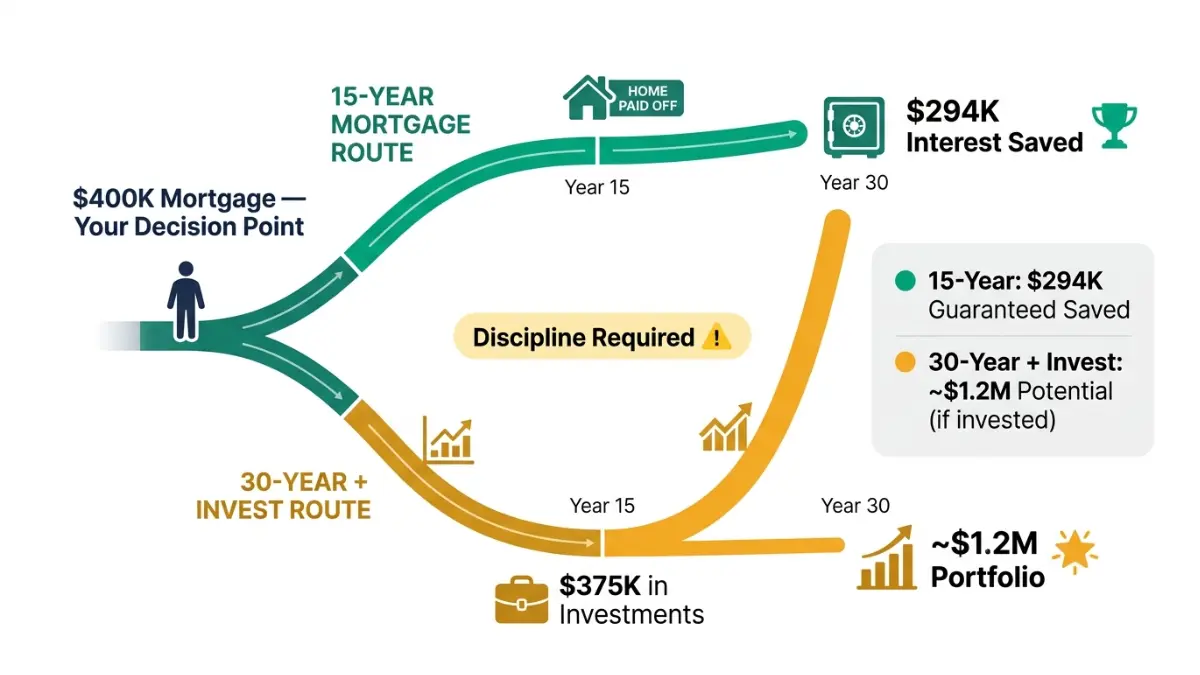

Choosing a 15-year mortgage saves roughly $216,000 in total interest compared to a 30-year mortgage, but it comes with monthly payments that are over $600 higher. That $600–$800 monthly gap is your decision capital.

The “Invest the Difference” Strategy — With Real Math

Here’s the scenario most financial sites won’t show you:

- Loan: $400,000

- 15-year payment: ~$3,279/month

- 30-year payment: ~$2,455/month

- Monthly difference: ~$824

If you invest $1,010 every month at an 8% annual return for 30 years, the investment grows to approximately $1,515,298.

Even with a more conservative difference of $824/month at 8% over 30 years, you’re looking at roughly $1.2 million in total wealth — far exceeding the ~$294,000 in interest you’d save with a 15-year loan.

So why doesn’t everyone choose the 30-year?

The Behavioral Finance Problem

The 30-year lets you “pay less” each month, so even if you take it thinking you’ll pay as if it were a 15-year, you end up slipping and holding it long. Research consistently shows most Americans do not invest the savings. They spend it — on cars, vacations, and lifestyle inflation.

If you invest the difference with discipline: 30-year wins on total wealth. If you spend the difference: 15-year wins every time.

The Tax Angle You Can’t Ignore

Mortgage interest is still tax-deductible on loans up to $750,000 under IRS Publication 936. This partially offsets the higher interest you pay on a 30-year loan — but only if you itemize deductions, which fewer Americans do since the 2017 Tax Cuts and Jobs Act raised the standard deduction.

To model the investment side of this decision, use our compound interest calculator and retirement calculator side by side.

What This Means For You: If you have high-interest debt (credit cards, student loans), pay those off first. Paying off a 6.22% mortgage early while carrying 20%+ credit card debt is the wrong priority. Check the order with our debt consolidation calculator.

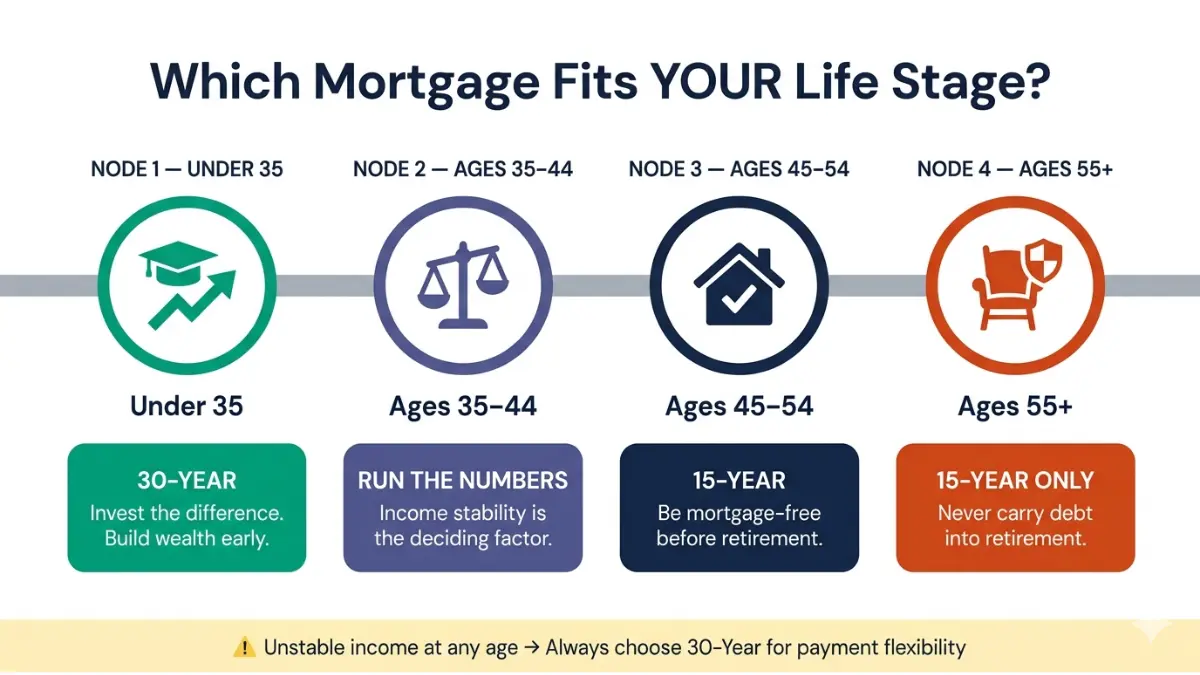

Who Should Choose Which — The Life-Stage Decision Framework

No competitor provides a structured answer based on your actual life stage. This is the framework that changes everything.

Choose a 15-Year Mortgage If You…

- Have stable, high household income (dual-income preferred)

- Are 45 years or older and want to be mortgage-free before retirement

- Have a debt-to-income (DTI) ratio below 36% even at the higher payment — check yours with our debt-to-income ratio calculator

- Already have 6+ months emergency fund fully funded

- Carry zero high-interest consumer debt

- Plan to stay in the home 15+ years

Choose a 30-Year Mortgage If You…

- Are under 35 with career income growth ahead

- Are self-employed or have variable income — mandatory payment flexibility is critical

- Still carry student loans or credit card debt that must be eliminated first

- Live in a high cost-of-living city where the 15-year payment would exceed 28% of gross income

- Want to maximize retirement contributions (401k/Roth IRA) before locking into a high mortgage payment

📊 Decision Table by Life Stage (2026)

| Age Group | Recommended Term | Primary Reason |

|---|---|---|

| Under 35 | 30-Year | Flexibility + invest the difference strategy |

| 35–44 | Either | Run the numbers; income stability is the deciding factor |

| 45–54 | 15-Year | Goal: mortgage-free before or at retirement |

| 55+ | 15-Year (if affordable) | Avoid carrying debt into retirement at all costs |

| Any Age — Unstable Income | 30-Year | Lower required payment = financial survival safety net |

The Income Stability Warning

You might qualify for a 15-year mortgage now, but if you lose your job later and struggle to make payments, you may not have enough income to refinance into a 30-year loan with lower monthly payments.

If you’re laid off on a 15-year loan, your required payment doesn’t shrink. You can’t renegotiate the obligation. The Consumer Financial Protection Bureau provides guidance on hardship options — but prevention beats cure.

Before locking into a 15-year payment, also review our guide on home loan income requirements to confirm you’re well above the minimum threshold, not just barely qualifying.

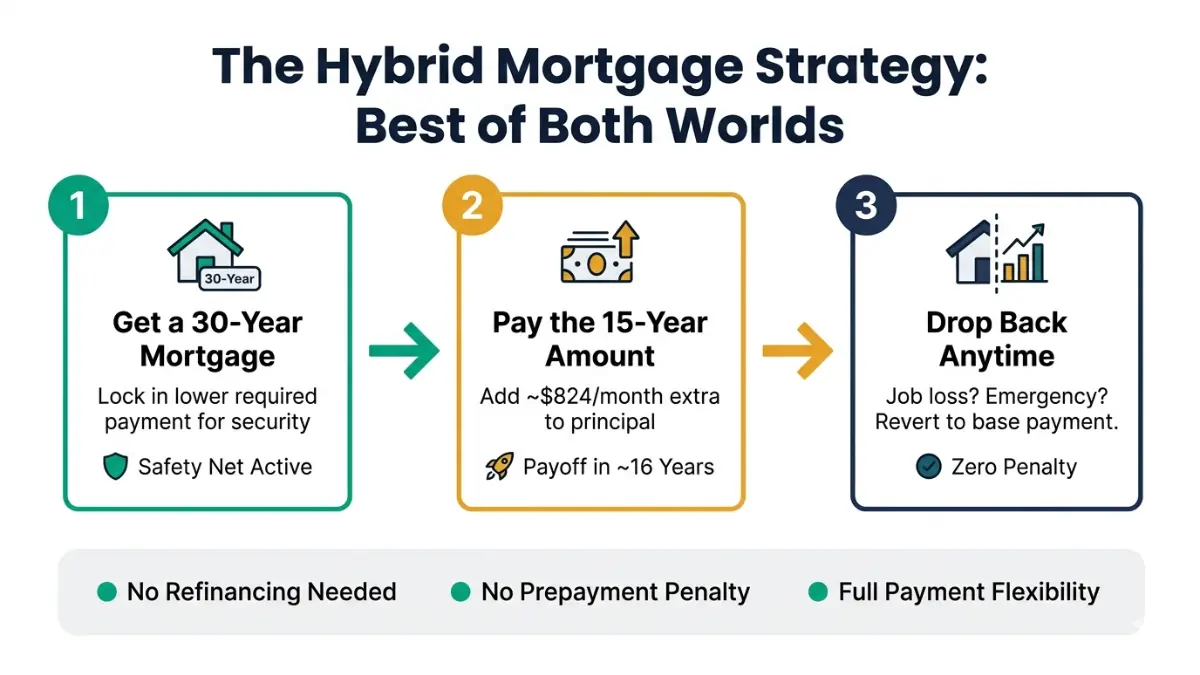

The Hybrid Strategy — The Best of Both Worlds

Most homebuyers don’t know this option exists. It’s the single smartest mortgage strategy in a volatile economy.

Take the 30-Year Mortgage. Pay It Like a 15-Year.

Here’s how it works:

- Get a 30-year mortgage at today’s rate (6.22%)

- Every month, pay the 15-year equivalent (~$824 extra on a $400K loan)

- When life gets tight — job loss, medical bills, family emergency — drop back to the required 30-year payment

- When cash flow recovers, resume aggressive payments

By paying $4,337 a month instead of $3,327 on a $500,000 loan at 7%, you could pay off the loan in about 16 years — still benefiting from the flexibility to revert to lower payments if needed.

Result: You get the payoff timeline of a 15-year loan with the safety net of a 30-year loan. No other strategy offers this combination.

Biweekly Payment Strategy

Instead of 12 monthly payments, make 26 half-payments per year — the equivalent of 13 full monthly payments. This single habit:

- Shaves 4–5 years off a 30-year mortgage

- Saves $40,000–$60,000 in interest on a $400,000 loan

- Requires zero refinancing or paperwork

Check with your lender that extra payments apply to principal — not future interest. Freddie Mac’s homebuyer resources include a full explainer on payment structures and prepayment rights.

Mortgage Recast — The Lump Sum Power Move

If you have a large amount of extra money to put toward your loan — usually at least $10,000 — consider recasting. Your rate and term stay the same, but your monthly payment decreases.

This is ideal for homeowners who receive a bonus, inheritance, or business windfall. Use our mortgage refinance calculator to compare whether a recast or a full refinance makes more sense for your situation.

Bold Takeaway: The hybrid strategy lets you be financially aggressive when you’re earning well — and financially safe when life happens. It’s the strategy advisors recommend most but most lenders don’t proactively explain.

What Financial Experts Say — and What 2026 Rates Mean Right Now

Expert Consensus Panel — financeauthorityhub.com

We consulted our expert panel, including Laura M. Bennett, CFP, Daniel Moreau, CPA/CFP, and Michael R. Thompson, CFA. Their collective verdict:

“In a 6%+ rate environment, the case for a 15-year mortgage is stronger than it was in 2020–2021. The spread between 15-year and 30-year rates historically narrows when rates rise — meaning the rate advantage of a 15-year is particularly valuable right now. However, for buyers under 40 with strong investment discipline, the 30-year + invest strategy still competes on total net worth.”

What 2026 Rate Environment Changes

Deciding on the 15-year FRM now, rather than a 30-year FRM, saves an estimated 60% on the total interest paid for a loan amount of $500,000. At current rates, this represents the most favorable environment for 15-year mortgages in over a decade.

Watch for fixed-rate mortgage rates to gradually work their way lower in 2026 when the Fed is able to complete its job stabilizing job growth and consumer inflation. If rates drop, refinancing from a 30-year to a 15-year becomes a powerful follow-up strategy — use our refinance calculator to track your break-even point.

Also explore our full comparison of fixed-rate vs adjustable-rate mortgages to understand whether locking in today makes sense for your timeline. And if you’re still in the early homebuying stage, our mortgage pre-approval guide walks you through qualifying for either loan type.

For a deeper look at how your down payment affects which term you can afford, HUD’s homebuying resources provide federal-level guidance on loan qualification standards.

Frequently Asked Questions

Q1: Is a 15-year mortgage always better than a 30-year mortgage?

No. A 15-year mortgage saves more interest, but a 30-year mortgage offers greater flexibility and can produce more total wealth if you invest the payment difference consistently. The best choice depends on your income stability, age, and financial discipline.

Q2: How much more is a 15-year mortgage payment vs a 30-year?

On a $400,000 loan at 2026 rates (15-yr at 5.54%, 30-yr at 6.22%), the 15-year monthly payment is approximately $824 higher. On a $500,000 loan, the difference is roughly $1,030 per month.

Q3: What are current 30-year and 15-year mortgage rates in 2026?

As of March 20, 2026, the average 30-year fixed-rate mortgage is 6.22% and the average 15-year fixed-rate mortgage is 5.54%. Rates vary by lender, credit score, and down payment. Check live rates with our mortgage rate calculator.

Q4: Can I pay off a 30-year mortgage in 15 years?

Yes. Make extra principal payments each month equal to the difference between your 30-year and 15-year payments. Confirm with your lender there are no prepayment penalties. This gives you 15-year payoff speed with 30-year payment flexibility.

Q5: Is it better to invest the difference or get a 15-year mortgage?

Investing $1,010 per month at an 8% annual return for 30 years grows to approximately $1,515,298 — similar to what you’d accumulate by paying off a 15-year loan and then investing the full payment for the remaining 15 years. Both strategies converge — but only if you’re disciplined about investing rather than spending the savings.

Q6: What credit score do I need for a 15-year mortgage?

Most lenders require a minimum credit score of 620 for conventional loans, but to qualify for the best 15-year rates you’ll typically need 740+. A higher score also lowers your DTI requirements. Check where you stand with our credit score calculator, then review our full guide on the credit score needed to buy a house in 2026.

Q7: Does a 15-year mortgage build equity faster?

Yes — significantly faster. A larger portion of each payment goes toward principal with a 15-year mortgage, helping you accumulate equity more quickly. In year one of a 30-year loan at 6.22%, over 80% of each payment is interest. Use our home equity calculator to model your equity timeline.

Q8: What happens if I can’t afford my 15-year mortgage payment?

Your options are limited: refinance to a 30-year (which resets your loan term and may be difficult if your credit or income has changed), request a forbearance, or sell the home. This is why income stability is non-negotiable before choosing a 15-year loan. The CFPB’s mortgage hardship page outlines your legal options.

Q9: Is a 30-year mortgage a waste of money?

Not if you use the payment flexibility strategically. It becomes a waste if you make only minimum payments for 30 years and never invest the difference. The loan term isn’t the problem — the lack of a strategy is.

Q10: Which mortgage saves more money in the long run?

The 15-year mortgage saves more in guaranteed interest. The 30-year mortgage with disciplined investing can produce more total net worth over 30 years — but with market risk attached. For certainty and simplicity: 15-year. For maximum wealth potential with discipline: 30-year + invest.

Q11: Should I refinance from a 30-year to a 15-year mortgage?

Refinancing makes sense if: (1) you can afford the higher payment comfortably, (2) current 15-year rates are lower than your existing rate, and (3) your break-even period is under 3 years. If you’re thinking of refinancing your current mortgage, opting for a shorter loan term can help shorten your repayment period — this is especially effective when interest rates are lower, because the lower interest rate may help offset some of the costs of the shorter repayment period. Use our mortgage refinance calculator to calculate your exact break-even before proceeding.

⚠️ Disclaimer: This article is for educational purposes only and does not constitute financial, legal, or mortgage advice. Mortgage rates, tax laws, eligibility criteria, and financial circumstances vary by individual and are subject to change. All calculations shown are estimates based on March 2026 average rates and standard assumptions. Always consult a licensed financial advisor, CPA, or mortgage professional before making any home loan decision. Interest rate data sourced from publicly available market reports as of March 2026.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.