How Much Income Do You Need to Qualify for a Home Loan in 2026?

There’s no minimum salary to qualify for a home loan. Your debt-to-income ratio is what lenders actually check. Here’s the exact income needed by home price in 2026.

In This Article

There is no minimum income required to qualify for a home loan. What lenders actually measure is whether your income is stable, verifiable, and large enough relative to your debts. The single number that determines your approval — and the loan amount you receive — is your debt-to-income (DTI) ratio, not your salary.

This 2026 guide breaks down the exact income you need by home price, every DTI limit by loan type, which income sources count, and five proven steps to qualify even if your finances feel borderline right now. Use our Home Affordability Calculator to run your personalized numbers before you speak to a single lender.

Why “How Much Income?” Is the Wrong Question

Most borrowers walk into the home loan process asking for a salary number. Lenders don’t think that way.

What lenders actually evaluate:

- Debt-to-Income (DTI) Ratio — your total monthly debt payments divided by your gross monthly income

- Income stability — at least 2 years of consistent, verifiable earnings

- Loan program eligibility — FHA, VA, USDA, and conventional all have different thresholds

- Credit score — directly impacts your rate, which changes how much income you need

Here’s the critical insight competitors miss: two borrowers earning the same salary can have completely different home loan outcomes based on their existing debts alone. A $75,000/year earner with no car loan or student debt may qualify for significantly more than an $85,000/year earner carrying $800/month in existing obligations.

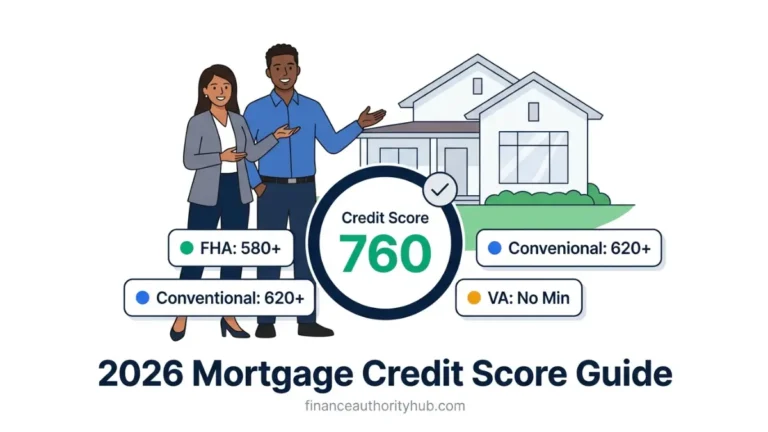

Before diving into numbers, check your Credit Score — it directly affects which loan programs you qualify for and what rate you’ll receive, which changes your required income threshold.

Income Required by Home Price in 2026 — Real Numbers

This is the master reference table competitors don’t provide. These figures use a ~6.8% 30-year fixed rate, 5% down payment, standard PMI, 1.2% property tax, and 0.35% homeowner’s insurance, with ≤$600/month in existing other debts.

Income Required by Home Price (2026)

| Home Price | Down Payment | Loan Amount | Est. Monthly PITI | Min. Annual Income (36% DTI) | Min. Annual Income (43% DTI) |

|---|---|---|---|---|---|

| $200,000 | 5% ($10K) | $190,000 | ~$1,630 | ~$54,333 | ~$45,500 |

| $300,000 | 5% ($15K) | $285,000 | ~$2,445 | ~$81,500 | ~$68,200 |

| $400,000 | 10% ($40K) | $360,000 | ~$3,100 | ~$103,000 | ~$86,500 |

| $500,000 | 10% ($50K) | $450,000 | ~$3,850 | ~$128,000 | ~$107,000 |

| $700,000 | 20% ($140K) | $560,000 | ~$4,750 | ~$158,000 | ~$132,000 |

Estimates are illustrative. Actual figures vary by lender, credit score, location, and loan program.

Key Insight: For a $300,000 home, the realistic income requirement falls between $74,000 and $95,000 annually, depending on your other debts and the specific loan program chosen.

The debt multiplier rule to remember:

- Every $100/month of existing debt (car payment, student loan, credit card minimum) reduces your home-buying power by roughly $15,000–$18,000

- Paying off a $300/month car loan before applying could increase your qualifying purchase price by ~$50,000

Use our Mortgage Calculator to stress-test different home prices, down payments, and interest rate scenarios before pre-approval.

Down payment matters more than most buyers realize. On a $300,000 home:

- 3% down → $291,000 loan → higher monthly payment → more income required

- 20% down → $240,000 loan → no PMI → lower monthly payment → less income required

That difference can equal roughly $17,000 in annual income needed to qualify. Check our Down Payment Calculator to model how your down payment changes the income equation.

The DTI Ratio — The Real Gatekeeper for Home Loan Approval

Your debt-to-income (DTI) ratio is all your monthly debt payments divided by your gross monthly income — and it is one of the primary ways lenders measure your ability to manage repayments.

Understanding this one number is more valuable than any salary benchmark.

Two Types of DTI You Must Know

Front-End DTI (Housing Ratio): Only your housing costs (mortgage principal + interest + property tax + insurance + HOA) divided by gross monthly income. Standard guideline: ≤28%.

Back-End DTI (Total DTI): All monthly debt obligations — housing + car loans + student loans + credit cards + personal loans — divided by gross monthly income. This is the number lenders weight most heavily.

DTI Limits by Loan Type — 2026 Master Table

| Loan Type | Front-End Max | Back-End Max | Notes |

|---|---|---|---|

| Conventional | 28% | 36–45% | Up to 50% with strong credit/assets |

| FHA | 31% | 43% standard | Up to 56.9% with compensating factors via AUS approval |

| VA | No strict limit | ~41–60% | Residual income test used instead of DTI cap |

| USDA | 29% | 41–46% | Rural properties; income limits apply |

| Jumbo | 28% | 36–43% | Stricter; often requires 20%+ down payment |

Maximum DTI ratios in 2026: Conventional loans allow up to 45–50% with strong compensating factors, FHA up to 57%, VA up to 60% in some cases, and USDA generally maxes at 41–46%.

The CFPB standard to know: To receive a standard Qualified Mortgage, your monthly debt-to-income ratio generally must be at or below 43 percent — meaning no more than 43% of your gross monthly income goes toward fixed debt payments including your mortgage.

Real DTI Calculation Example

Borrower: $6,500/month gross income Existing debts: $350 car loan + $200 student loan + $100 credit card minimum = $650/month Proposed mortgage (PITI): $1,800/month Total monthly debt: $650 + $1,800 = $2,450 Back-End DTI: $2,450 ÷ $6,500 = 37.7% → ✅ Comfortably qualifies for conventional loan

Check your exact ratio instantly with our Debt-to-Income Ratio Calculator. If your DTI is above 43%, see Section 5’s action plan — there are real paths forward.

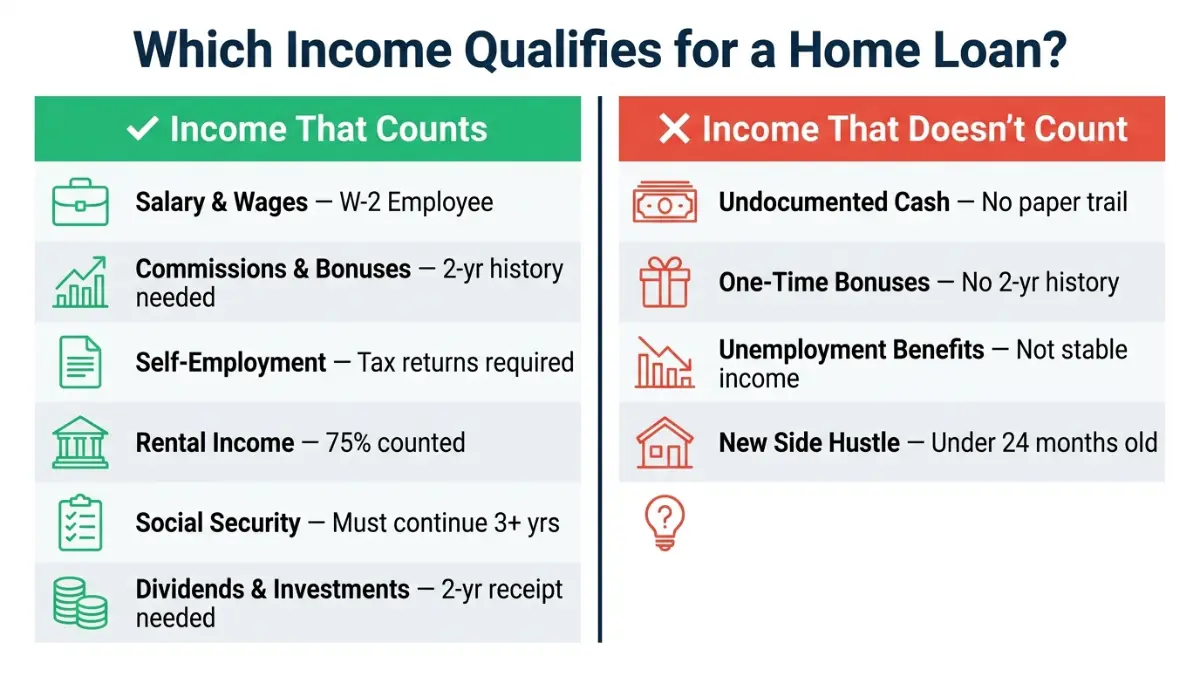

What Income Sources Count Toward a Home Loan?

This is where most guides fail borrowers. Lenders count far more than your W-2 salary — but every income type has documentation requirements.

Income Sources Lenders Accept in 2026

Standard Employment Income (Easiest to Document)

- Salary and hourly wages — requires 30 days of recent pay stubs + 2 years of W-2s

- Variable income like commissions, overtime, or bonuses requires proof of 2–3 years of consistent receipt to be used in qualification

- Part-time income — accepted with 2-year history of consistent receipt

Self-Employed, Freelance, and Gig Workers

- 2 years of personal and business tax returns required

- Lenders average net income over the 2-year period — large deductions reduce qualifying income

- Bank statement loans available: qualify based on 12–24 months of deposits instead of tax returns (ideal if deductions significantly lower reported income)

- Required documents: P&L statement, business bank statements, and a CPA confirmation letter is recommended

Retirement and Investment Income

- Retirement and Social Security income must be expected to continue for at least 3 years post-closing to qualify

- Dividend and investment income: 2-year receipt history required; must be expected to continue

- Rental income: typically 75% of documented rental income is counted

Alimony and Child Support

- Must have received regular payments for at least 6–12 months prior to application

- Support payments must be documented to continue for 3+ more years

Income That Does NOT Count

- Undocumented cash income without a paper trail

- One-time year-end bonuses without multi-year history

- Unemployment benefits (not ongoing/stable income)

- Side income received for fewer than 24 months without supporting tax returns

Pro Tip for Self-Employed Borrowers: Large business deductions reduce your taxable income — which also reduces your qualifying home loan income. A bank statement loan can solve this. Review your Home Loan Requirements guide to understand full documentation standards before applying.

For self-employed borrowers, the IRS provides guidance on income documentation at irs.gov/businesses/self-employed.

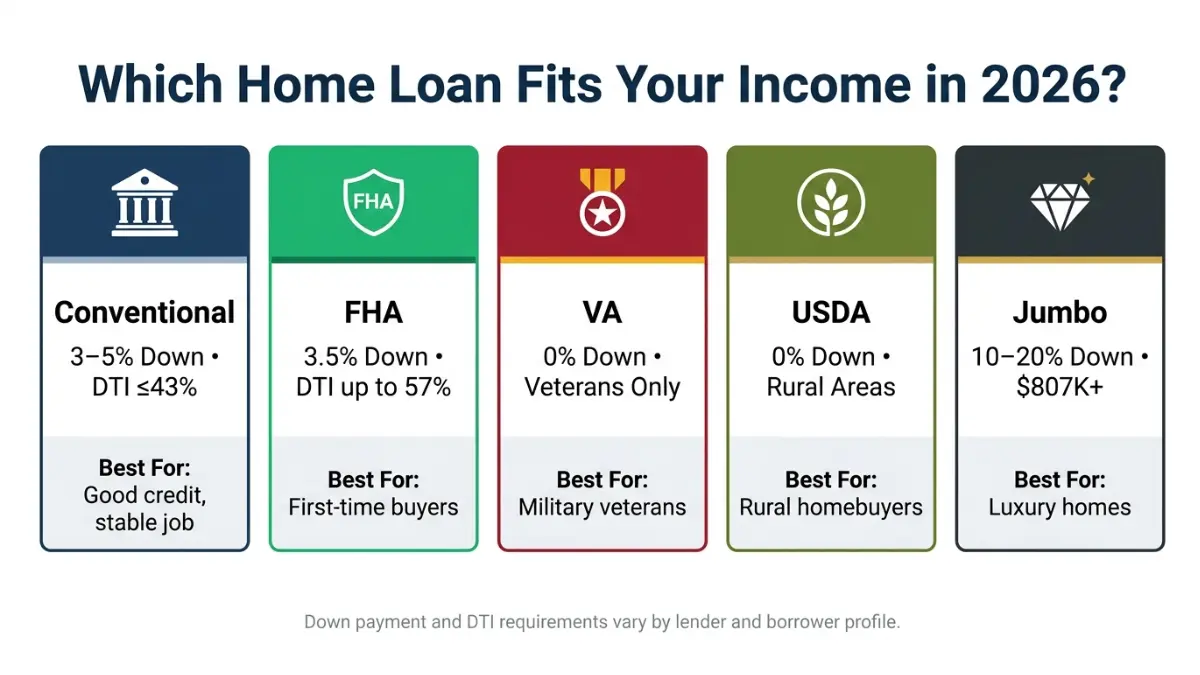

Which Home Loan Program Fits Your Income? FHA, VA, USDA, or Conventional

Choosing the wrong loan program is one of the most expensive mistakes first-time buyers make. A borrower who fails a conventional application may easily qualify with FHA — at the same income level.

Quick Match Guide: Loan by Borrower Profile (2026)

| Your Situation | Best Loan Type | Min. Down Payment | Key Income Rule |

|---|---|---|---|

| Good credit (700+), stable job | Conventional | 3–5% | DTI ≤43% preferred |

| First-time buyer, credit 580–699 | FHA | 3.5% | No minimum income; DTI is the primary qualifier |

| Military veteran/active duty | VA | 0% | Residual income test; very flexible DTI |

| Rural property, moderate income | USDA | 0% | Household income caps apply by county |

| Lower-to-moderate income buyer | HomeReady / Home Possible | 3% | Income must not exceed 80% of area median income (AMI) to meet HomeReady eligibility |

| Luxury / high-value home ($807K+) | Jumbo | 10–20% | Stricter DTI; higher cash reserves required |

2026 Loan Limit Updates — What Changed

- FHA loan limits increased to $541,287 for most U.S. counties in 2026, giving more borrowers access to FHA financing

- Conforming loan limit (conventional) rose by over $26,000 vs. prior year

- Jumbo loans now apply above $806,500 in most markets

- VA loans have no loan limit for eligible veterans with full entitlement

Low-Income Buyer Programs Worth Knowing in 2026

- Fannie Mae HomeReady and Freddie Mac Home Possible: 3% minimum down, income caps at 80% of AMI, reduced PMI rates

- HFA Loans: State housing finance agency programs often include down payment assistance and below-market interest rates

- FHA 203(k) Rehab Loans: For buyers purchasing fixer-uppers — renovation costs rolled into the mortgage

If you’re unsure which program fits your income profile, a HUD-approved housing counselor provides free, unbiased guidance. Find one at hud.gov/findacounselor.

Also review our Types of Home Loans guide for a complete breakdown of every major loan program, or compare Fixed Rate vs Adjustable Rate Mortgages to understand how rate type affects your required qualifying income.

Considering refinancing later? Our Mortgage Refinance Calculator shows exactly when refinancing makes financial sense.

5 Proven Steps to Qualify for a Home Loan on Your Current Income + FAQs

You don’t always need a raise to qualify. These five moves — applied strategically before you apply — can move you from “denied” to “approved.”

Your 2026 Home Loan Qualification Action Plan

Step 1: Calculate Your DTI Before Talking to Any Lender Know your number first. Use our Debt-to-Income Ratio Calculator to see exactly where you stand. If your DTI is above 43%, proceed to Steps 2 and 3 immediately.

Step 2: Pay Down Revolving Debt Strategically Every $100 reduction in monthly debt payments improves your DTI by roughly 1.5–2 percentage points on a $6,000/month income. Paying off a $200/month credit card before applying can add $30,000+ to your qualifying purchase price. Use our Credit Card Payoff Calculator to build a targeted payoff timeline.

Step 3: Avoid New Debt for 6–12 Months Before Applying New car loans, personal loans, or credit card accounts directly increase your monthly debt obligations — and destroy your DTI. This is the most underestimated mistake in home buying.

Step 4: Build Your Income Paper Trail Side income, rental income, bonuses, and freelance work all count — but only with a 2-year documented history. Start documenting now if you plan to apply within the next 12–24 months.

Step 5: Choose the Right Loan Program for Your Profile A 42% DTI borrower may fail a conventional loan application but qualify easily with FHA. Matching your financial profile to the right program is often the difference between approval and denial. Review How Does a Home Loan Work for a full picture of the approval process.

The CFPB’s mortgage resource center at consumerfinance.gov provides further detail on how lenders assess your DTI during underwriting.

Frequently Asked Questions About Home Loan Income Requirements

Q1: Is there a minimum income required to qualify for a home loan?

No. There is no set minimum income requirement — lenders evaluate whether your income is stable, verifiable, and sufficient for the loan amount you’re seeking.

Q2: What DTI ratio do I need to qualify for a home loan?

Most lenders prefer a back-end DTI of 43% or below. In 2026, conventional loans allow up to 50% with strong compensating factors, FHA up to 57%, and VA up to 60% in some cases.

Q3: How much income do I need for a $300,000 home loan?

You’ll want to earn at least $6,750/month (~$81,000/year) based on a 6.877% rate, 5% down payment, and standard 30-year fixed conventional terms. This assumes ≤$600/month in other debts.

Q4: Can self-employed borrowers qualify for a home loan?

Yes. Two years of personal and business tax returns are required. Bank statement loans are also available if your tax deductions reduce your documented qualifying income significantly.

Q5: Does bonus or overtime income count toward home loan qualification?

Yes — if you can demonstrate 2–3 years of consistent receipt through pay stubs, W-2s, and tax returns.

Q6: What is the 28/36 rule for home loans?

A guideline stating that housing costs should not exceed 28% of gross monthly income, and total debt should not exceed 36%. FHA and VA programs allow higher ratios, making this a baseline rather than a hard rule.

Q7: Can I qualify for a home loan with a high DTI?

Yes — particularly through FHA (up to ~57%) or VA (flexible with residual income). Compensating factors like high credit scores, large down payments, and substantial cash reserves can also offset a high DTI on conventional loans.

Q8: Does Social Security income count toward home loan qualification?

Yes, provided the income is expected to continue for at least 3 years after the loan closes.

Q9: What documents do I need to prove income for a home loan?

– Last 30 days of pay stubs

– 2 years of W-2s or 1099s

– 2 years of federal tax returns

– 2–3 months of bank statements

– Documentation for all supplemental income sources

Q10: Does a larger down payment reduce my income requirement?

Yes — significantly. A 20% down payment eliminates PMI, reduces the loan amount, and lowers monthly payments. On a $300,000 home, this difference can reduce the minimum qualifying income by approximately $15,000–$17,000 annually.

Q11: What is the maximum home loan I can qualify for on $60,000 per year?

At $5,000/month gross income, a 36% DTI allows $1,800/month for all debts combined. With $400/month in existing obligations, your maximum mortgage payment is approximately $1,400/month — qualifying for roughly $195,000–$215,000 at current 2026 rates. Use our Home Affordability Calculator for a personalized figure.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, mortgage, or legal advice. Home loan qualification requirements vary by lender, loan program, state, and individual financial circumstances. Income figures and DTI thresholds are estimates based on 2026 market conditions and are subject to change. Always consult a licensed mortgage professional or HUD-approved housing counselor before making any home financing decisions. External links are included for reference only and do not constitute an endorsement by Finance Authority Hub.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.