Debt Consolidation Calculator – Cut Debt Fast 2026

Debt Consolidation Calculator

Compare paying multiple debts separately vs replacing them with one consolidation loan (with optional fees and extra payments).

Inputs

Enter balance + APR + the payment you plan to make each month for each debt (minimum or more).

Note: This tool estimates your “current” payoff using the monthly payment you enter for each debt. Consolidation can simplify payments but may not always reduce total interest. [web:87]

Results

Current debts (combined)

—

Monthly payments: —

Current payoff estimate

— months

Total interest (estimate): —

Consolidation loan

—

Payment: —

Consolidation payoff

— months

Total interest: —

Fees + savings view

Fees: — (—) • Upfront fees: —

Monthly savings (current − consolidation): — • Break-even months (upfront fees): —

Interest difference (current − consolidation): —

Entered debts (payoff estimate per debt)

| Debt | Balance | APR | Monthly payment | Months to payoff | Interest (est.) |

|---|

Consolidation loan amortization schedule

| Month | Payment | Principal | Interest | Extra paid | Remaining balance |

|---|

Results appear after you click “Calculate.”

In This Article

What Is a Debt Consolidation Calculator — And Why You Need One Right Now

A debt consolidation calculator shows you in seconds whether combining your multiple debts into one single loan will save you money, reduce your monthly payments, or help you become debt-free faster.

The 2026 reality: U.S. credit card debt hit a record $1.28 trillion at the end of 2025, with the average American carrying multiple high-interest balances. As of February 2026, the average rate on a personal loan is 12.15% — compared to the average credit card APR of around 20%. That gap is your opportunity.

What This Means For You: If you’re paying 20%+ on credit cards and can qualify for a consolidation loan at 12–14%, our calculator above will show exactly how many thousands of dollars you could save.

Use our free debt consolidation calculator tool above to run your numbers. Already have a mortgage? Cross-reference your home equity potential with our Home Affordability Calculator before deciding on a HELOC route.

How to Use This Debt Consolidation Calculator (5 Simple Steps)

Our tool is built for both desktop and mobile. Here’s exactly how to get the most accurate results.

Step 1: Enter each of your current debts

- Input the debt name (e.g., “Chase Visa”), balance, APR %, and your current monthly payment

- Add as many debts as you have — click “Add another debt” for each one

- Our calculator supports USD, GBP, CAD, AUD, and 18 other currencies

Step 2: Set your start date

- This tells the calculator when your consolidation loan would begin

- It generates a month-by-month amortization schedule from that date

Step 3: Enter your consolidation loan offer

- Input the APR % you’ve been quoted (or estimate based on your credit score)

- Enter the loan term in months (e.g., 36, 48, or 60 months)

- Add any origination fees your lender charges

Step 4: Choose your fee option

- Roll fees into the loan (adds to your balance) OR pay them upfront

- Our calculator shows you the break-even point for both options

Step 5: Hit “Calculate” and read your results

| Result Shown | What It Tells You |

|---|---|

| Monthly savings | How much less you pay each month vs. now |

| Break-even months | How long until upfront fees are recovered |

| Interest difference | Total dollars saved (or lost) in interest |

| Payoff months | How many months until you’re debt-free |

Pro tip: Click “Toggle consolidation loan schedule” to see your full month-by-month payment breakdown, or download the CSV to save it.

Is Debt Consolidation Worth It in 2026? Here’s the Math

Direct answer: Yes — but only if your consolidation loan APR is meaningfully lower than your weighted average debt APR. If it isn’t, you’ll pay more, not less.

2026 Live Rate Comparison Table

| Debt Type | Avg APR (2026) | Typical Consolidation Rate | Verdict |

|---|---|---|---|

| Credit Cards | ~20% | 12–14% | ✅ Usually worth it |

| Payday Loans | 300–400% | 12–25% | ✅ Almost always worth it |

| Personal Loans | ~12.26% | 10–14% | ⚠️ Marginal — check fees |

| Medical Bills | 0–6% | 12.15% | ❌ Do NOT consolidate |

| Auto Loans | 6–9% | 12.15% | ❌ Do NOT consolidate |

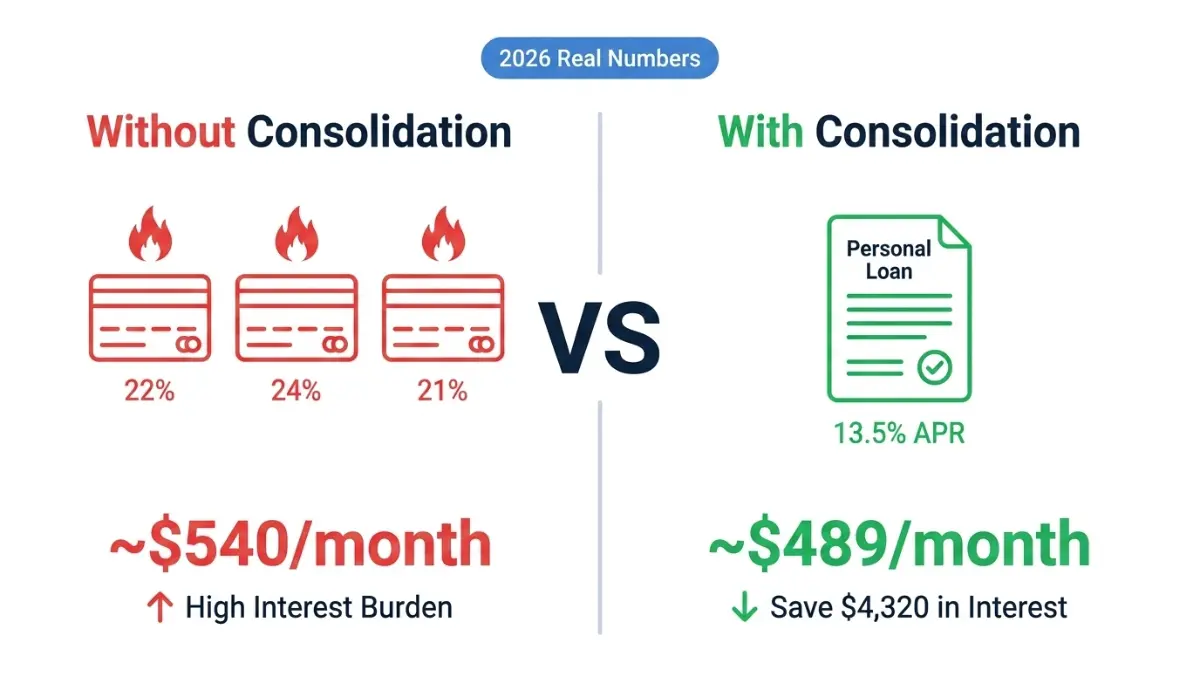

Real Case Study: $18,000 Across 3 Credit Cards

Sarah, 34, from Texas had:

- Chase Visa: $7,000 at 22.99% APR

- Citi Card: $6,500 at 21.74% APR

- Discover Card: $4,500 at 24.99% APR

- Combined monthly minimum payments: $540

After consolidating into a single personal loan at 13.5% APR over 48 months:

- New monthly payment: $489 (saves $51/month)

- Total interest saved: $4,320

- Debt-free 6 months earlier

Run your own version of Sarah’s numbers in our debt consolidation calculator above.

The Break-Even Formula (Simplified)

If your lender charges an origination fee, use this:

Break-even months = Upfront fees ÷ Monthly savings

Example: $400 fee ÷ $51/month savings = 7.8 months to break even

If you plan to keep the loan longer than your break-even point, the fee is worth paying.

⚠️ The Trap No One Mentions

Personal loan originations hit a record 7.2 million in Q3 2025, with 51% of borrowers using them for debt consolidation or credit card payoff. But the most common way consolidation fails? You pay off the cards — then run them back up. Suddenly you have a personal loan AND new credit card balances.

The fix: Freeze or close the paid-off cards immediately after consolidation. Consolidation should be the last step in changing your spending pattern, not a bridge to more debt.

For a deeper look at debt types and risks, see our guide on debt in 2026: types, risks, and how to break free.

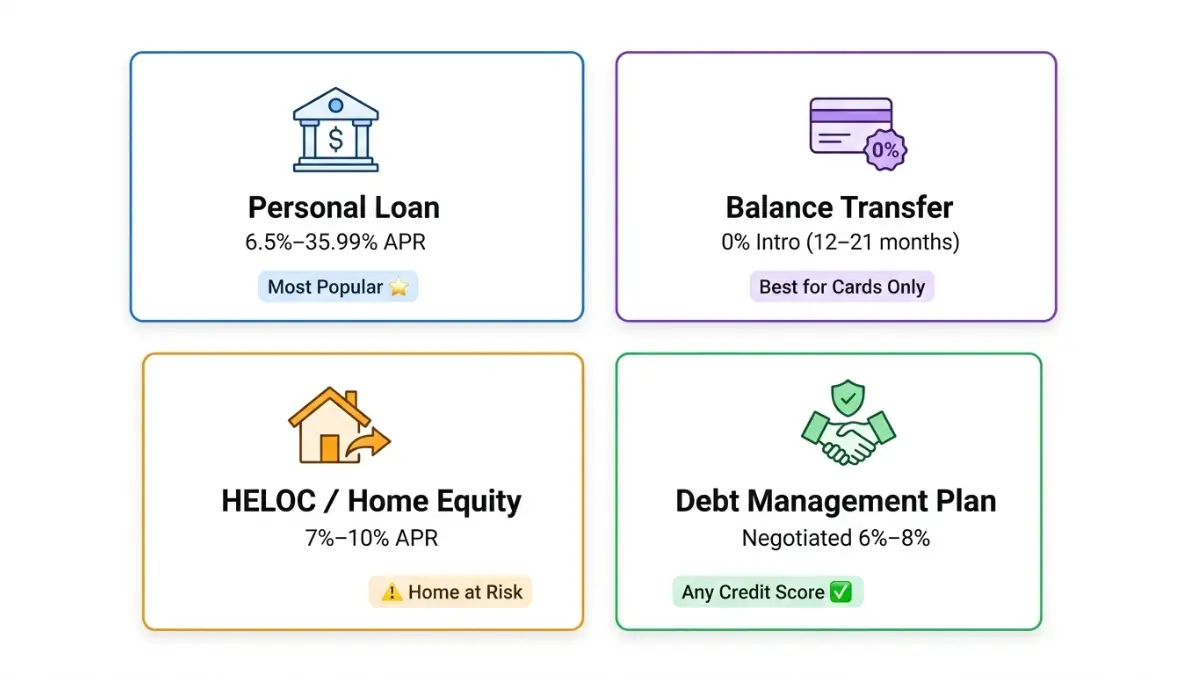

4 Debt Consolidation Methods Compared (2026 Guide)

Not all consolidation paths are equal. Here’s what to know before choosing.

| Method | Best For | APR Range (2026) | Risk Level | Min. Credit Score |

|---|---|---|---|---|

| Personal Loan | Multiple debts, fixed payoff | 6.5%–35.99% | Low | 670+ |

| Balance Transfer Card | Credit card debt only | 0% intro (12–21 mo) | Medium | 690+ |

| Home Equity Loan / HELOC | Large debt, homeowners | 7%–10% | HIGH | 620+ |

| Debt Management Plan | Poor credit, financial hardship | Negotiated 6–8% | Low | Any |

Personal Loan — Most Popular in 2026

A personal loan is the most straightforward path. You borrow a fixed amount, get a fixed rate, and make equal monthly payments. The average personal loan debt per borrower in the U.S. in September 2025 was $11,724.

Best for: People with a credit score above 670 who want predictable, fixed payments and a clear debt-free date. Compare rates across at least three lenders — banks, credit unions, and online lenders — before committing. For more on rates and pitfalls, read our in-depth guide to personal loan rates and traps in 2026.

Balance Transfer Card — Best for Credit Card Debt Only

A 0% APR balance transfer card gives you an interest-free window (typically 12–21 months) to pay down debt. You’ll pay a balance transfer fee of 3–5%, but the math often works out if you can pay off the balance before the promotional period ends.

Critical risk: If you can’t clear the balance before the 0% period expires, the rate often jumps to 20%+. Our 0% APR credit cards guide covers the best current options.

Home Equity Loan / HELOC — Lowest Rate, Highest Risk

Home equity loans offer the lowest interest rates because your home is the collateral. However, as the Consumer Financial Protection Bureau warns, if you fail to repay the loan, you could lose your home to foreclosure. Only use this option if you have a stable income and strong financial discipline.

Debt Management Plan — When Your Credit Score Is Low

A nonprofit credit counseling agency can negotiate reduced interest rates with your creditors and set up a single monthly payment on your behalf. There’s no minimum credit score requirement. Fees are typically low or waived for hardship cases. The Federal Trade Commission’s guide on how to get out of debt is an excellent free resource for anyone evaluating this path.

Debt Consolidation vs. Debt Settlement: Critical Difference

Debt consolidation = You repay 100% of what you owe, but under better terms (lower rate, one payment).

Debt settlement = A company negotiates to pay creditors less than you owe. This severely damages your credit score and the forgiven amount may be taxed as income.

Never confuse the two. If a company promises to “eliminate” your debt for a fee upfront, that’s likely a scam or a settlement scheme — not consolidation.

Will Debt Consolidation Hurt My Credit Score?

Short answer: Temporarily, yes. Long-term, it usually helps.

- Applying triggers a hard inquiry, which can drop your score by 5–10 points

- Closing old credit card accounts can reduce your available credit and raise your utilization ratio

- However: Making consistent on-time payments on your new loan rebuilds your score fast. Using a loan to pay off $1,000 in credit card debt can boost your credit score by 29 points after just one month.

For your full credit score roadmap, see our credit score complete guide.

How to Get the Best Consolidation Loan Rate in 2026 (Action Plan)

The rate you get determines whether consolidation saves money or costs more. Here’s how to maximize your chances of a low APR.

Step 1: Check your credit score for free Visit AnnualCreditReport.com — the only federally authorized site — to get your free reports from all three bureaus (Equifax, Experian, TransUnion). Dispute any errors before applying.

Step 2: Calculate your debt-to-income ratio (DTI)

DTI = Total monthly debt payments ÷ Gross monthly income × 100

Lenders prefer DTI below 36%. Above 43% significantly limits your options.

Step 3: Compare at least 3 lenders Banks, credit unions, and online lenders each have different criteria. Credit unions typically offer lower rates than banks. Online lenders often have the most flexible requirements.

Step 4: Pre-qualify using soft inquiries only Most lenders offer pre-qualification that does NOT affect your credit score. Get 3–5 pre-qualification offers and compare APR (not just the interest rate). Understanding the difference between APR and interest rate is critical — our APR vs. interest rate guide explains exactly what to look for.

Step 5: Watch origination fees carefully Some lenders charge 1–8% of the loan amount upfront. On a $20,000 loan, an 8% fee = $1,600 added cost. Always use our calculator’s fee field to factor this into your true cost.

Step 6: Don’t extend your term unnecessarily A 60-month term has lower monthly payments than a 36-month term, but you’ll pay significantly more total interest. Use the calculator to compare both scenarios before deciding.

2026 Credit Score → Consolidation Rate Guide

| FICO Score Range | Estimated APR (Personal Loan) | Strategy |

|---|---|---|

| 720–850 (Excellent) | 6.5%–12% | Apply confidently, negotiate |

| 690–719 (Good) | 12%–17% | Shop credit unions first |

| 630–689 (Fair) | 17%–25% | Pre-qualify multiple lenders |

| 580–629 (Poor) | 25%–36%+ | Consider DMP first, improve score |

| Below 580 | May not qualify | Work on score for 6 months |

What This Means For You: Even improving your score by 30–40 points before applying could move you into a lower rate tier — potentially saving you thousands over the loan term. See our credit card debt escape strategies for proven ways to improve your score quickly.

Frequently Asked Questions about Debt Consolidation Calculator

1. What is a debt consolidation calculator?

A debt consolidation calculator is a free online tool that compares your current multiple debt payments against a single consolidation loan. It calculates your new monthly payment, total interest paid, monthly savings, and how long until you’re debt-free — all in seconds.

2. How accurate is a debt consolidation calculator?

Very accurate for estimation purposes, provided you enter correct balances, APRs, and monthly payments. Results are projections — your actual loan terms will depend on your lender’s offer and your credit profile.

3. What is the average interest rate for a debt consolidation loan in 2026?

The current average personal loan interest rate is 12.15%, based on Bankrate Monitor data for February 18, 2026, for a customer with a 700 FICO score. Rates range from as low as 6.49% for excellent credit to 35.99% for poor credit.

4. Does debt consolidation hurt your credit score?

It causes a small, temporary dip (5–10 points) from the hard inquiry. Long-term, it typically improves your score by reducing credit utilization and establishing a positive payment history.

5. How many debts can I consolidate at once?

There is no legal limit. Our calculator supports as many debts as you need to enter. Most personal loans allow you to consolidate all your unsecured debts — credit cards, medical bills, personal loans — in one transaction.

6. What is the minimum credit score for a debt consolidation loan?

Most traditional lenders require a minimum FICO score of 580–600. For competitive rates below 15%, you generally need 670+. If your score is below 580, a nonprofit debt management plan is usually the better starting point.

7. Is debt consolidation the same as debt settlement?

No. Consolidation means you repay everything you owe under new, better terms. Settlement means you negotiate to pay less than the full balance, which damages your credit for 7 years and may create a tax liability on the forgiven amount.

8. How long does it take to pay off a consolidated loan?

Typical terms range from 24 to 84 months. Most borrowers choose 36–60 months. Our calculator’s amortization schedule shows your exact payoff date based on your chosen term.

9. Can I consolidate student loans and credit cards together?

Generally, no — you shouldn’t mix federal student loans with other debt in a personal loan. Doing so eliminates federal protections like income-driven repayment and forgiveness programs. Use our Student Loan Calculator to manage student debt separately.

10. What happens if I miss a payment on a consolidation loan?

A missed payment triggers a late fee, a hard negative mark on your credit report, and potentially a penalty APR increase. If you foresee trouble, contact your lender immediately — many offer hardship deferment options.

11. Is it better to consolidate debt or pay it off separately?

Use the calculator to find out. If your consolidation rate is at least 3–5% lower than your average current rate, consolidation almost always wins. If the rates are similar, the debt avalanche or snowball methods may be more effective. Compare both strategies in our snowball vs. avalanche debt payoff guide.

Related Finance Tools

- Auto Loan Calculator — calculate your car loan payments

- Mortgage Calculator — plan your home purchase payments

- Mortgage Refinance Calculator — see if refinancing saves you money

- All Finance Tools — full tools library

📋 Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or tax advice. Debt consolidation decisions depend on your individual financial situation, credit profile, and the specific loan terms available to you. Always consult a licensed financial advisor or nonprofit credit counselor before making major debt decisions. Rate data sourced from Bankrate Monitor, Federal Reserve, and TransUnion as of February 2026.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.