Commercial Truck Insurance: Real 2026 Costs Revealed

Commercial truck insurance costs $421–$1,800+/month in 2026. Discover real rates by truck type, state, and authority status — plus 7 proven ways to lower your premium today.

In This Article

Commercial truck insurance costs $421 per month on average in 2026 for $1 million in liability coverage. But owner-operators under their own authority typically pay $900–$1,800+ per month — and first-year carriers can pay even more. If you’ve been quoted double what you expected, here’s exactly why, and what you can do about it.

What this guide covers:

- Real 2026 cost data by truck type, state, and authority status

- Every coverage type explained in plain English

- FMCSA federal requirements (including the new 2026 Motus update)

- 7 proven strategies to lower your premium today

- 11 expert-answered FAQs

What Is Commercial Truck Insurance — and Who Actually Needs It?

Commercial truck insurance is a specialized business insurance policy that protects truck operators, their vehicles, cargo, and third parties from financial losses caused by accidents, theft, and liability claims. It is fundamentally different from personal auto insurance — and the gap matters enormously.

Commercial Truck Insurance vs. Personal Auto Insurance

| Feature | Commercial Truck Insurance | Personal Auto Insurance |

|---|---|---|

| Coverage for business use | ✅ Yes | ❌ No |

| Cargo protection | ✅ Optional add-on | ❌ Not available |

| FMCSA filing support | ✅ Included | ❌ Not applicable |

| Liability limits | Up to $5 million | Typically $300K–$500K max |

| Bobtail/non-trucking | ✅ Available | ❌ Not available |

If you haul freight for hire and carry only a personal auto policy, you have zero coverage the moment you’re on a commercial run. Insurers will deny the claim entirely.

Who Is Legally Required to Carry It?

Under 49 CFR Part 387, the Federal Motor Carrier Safety Administration (FMCSA) mandates that all for-hire motor carriers maintain minimum insurance before receiving operating authority. This applies to:

- Owner-operators running under their own USDOT authority

- Motor carriers operating fleets of commercial vehicles

- New authority carriers within their first 12 months of operation

- Leased-on drivers (though their carrier may cover primary liability)

Private carriers transporting their own goods interstate are also subject to FMCSA financial responsibility rules based on vehicle weight and cargo type.

What This Means For You: Even if you’re leased to a larger motor carrier, you likely still need bobtail insurance, non-trucking liability, and possibly physical damage coverage. Never assume your carrier’s policy covers everything.

Commercial Truck Insurance Costs in 2026 — What You’ll Actually Pay

This is where most truckers get blindsided. Advertised “average” rates rarely reflect what owner-operators under their own authority actually pay. Here is the full, unfiltered 2026 picture.

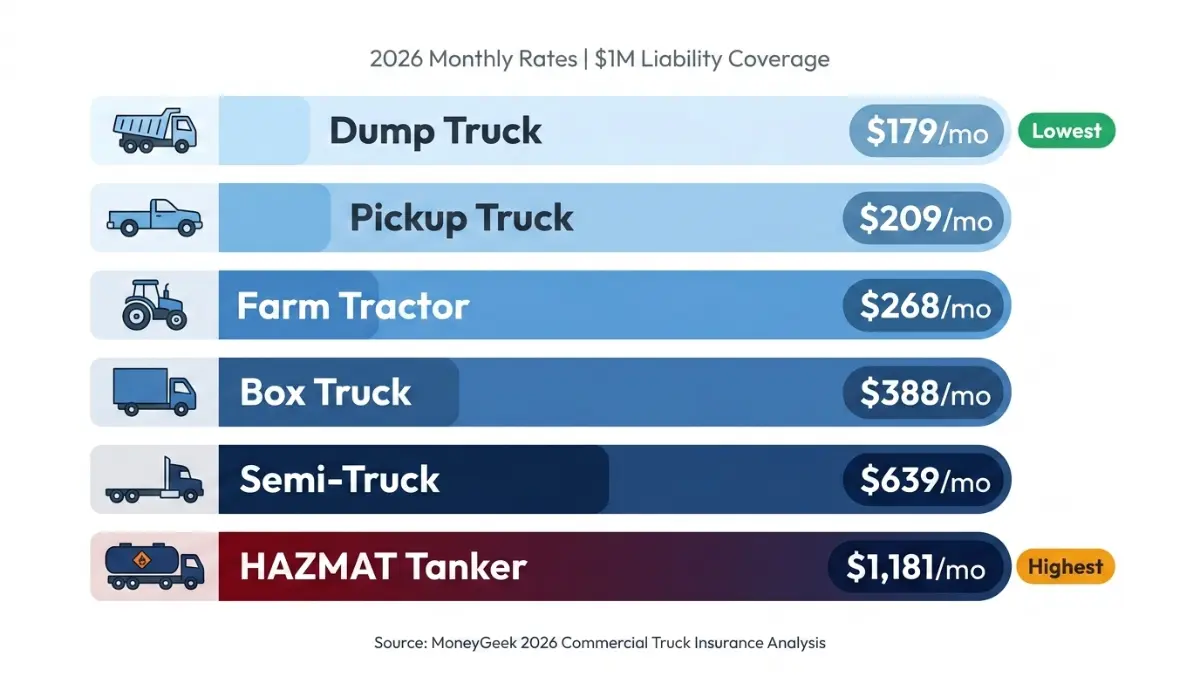

Average Monthly Cost by Truck Type

| Truck Type | Average Monthly Cost (2026) |

|---|---|

| Pickup Truck | $209 |

| Dump Truck | $179 |

| Farm Tractor | $268 |

| Forklift | $403 |

| Box Truck | $388 |

| Semi-Truck (standard freight) | $639 |

| HAZMAT Tanker | $1,181 |

Source: MoneyGeek 2026 commercial truck insurance analysis

Cost by Operating Authority Status

This is the breakdown almost no competitor publishes clearly:

| Operator Type | Monthly Cost Range |

|---|---|

| Leased-on driver (carrier covers primary) | $250–$500 |

| Owner-operator (own authority, established) | $900–$1,800+ |

| New authority (0–12 months) | $1,800–$2,500+ |

Leased-on drivers pay dramatically less because their motor carrier covers primary liability. They typically only need bobtail, non-trucking liability, and physical damage — which keeps costs manageable.

If you’re comparing quotes online and seeing numbers like “$421/month,” confirm whether those quotes include a full package (liability + physical damage + cargo) or just liability-only. The difference can exceed $800/month.

State-by-State Cost Variation

Where you operate can shift your premium by over 240%. States with dense litigation environments — Florida, New York, New Jersey — carry significantly higher premiums.

| State | Average Monthly Cost ($1M Liability) |

|---|---|

| Vermont | $284 |

| Maine | $275 (cheapest) |

| New Hampshire | $300 |

| Idaho | $309 |

| New York | $666 (most expensive) |

If your operating radius is regional rather than national, tightening your declared radius to match your actual routes can reduce your premium by 10–15% immediately.

The New Authority Tax — Why First-Year Carriers Pay 40–100% More

New authority carriers (0–12 months of operating history) are treated as the highest-risk segment by underwriters. You have no loss runs, no track record, and no safety data — so insurers price in maximum uncertainty.

The result: A new authority owner-operator hauling general freight can pay $1,800–$2,500+/month for the same coverage an established carrier pays $900/month for. This “new authority tax” typically drops significantly after 24–36 months of clean operation.

To reduce it faster: install dash cams immediately, document maintenance logs, maintain a clean MVR, and submit organized quote packages to underwriters rather than applying haphazardly.

Why Are 2026 Premiums Still Rising? The Nuclear Verdict Effect

This is the factor almost every competitor article misses entirely.

According to the American Transportation Research Institute (ATRI), nuclear verdicts — jury awards exceeding $10 million — surged 52% in 2024. These massive lawsuit payouts directly force insurers to raise premiums industry-wide, regardless of your individual safety record.

Insurance costs hit a record $0.102 per mile in 2024, making up roughly 10% of total operating costs for most owner-operators. This is not a temporary spike. Underwriters have baked in higher litigation risk as a permanent pricing floor for 2026.

Cost-Per-Mile Framework: Divide your monthly premium by your monthly miles to find your true insurance CPM. Example: $1,200/month ÷ 10,000 miles = $0.12/mile. This makes comparison shopping and budgeting far more precise than looking at monthly totals alone.

For owner-operators also managing vehicle financing, see our guide on liability insurance to understand how liability coverage layers with your other business obligations.

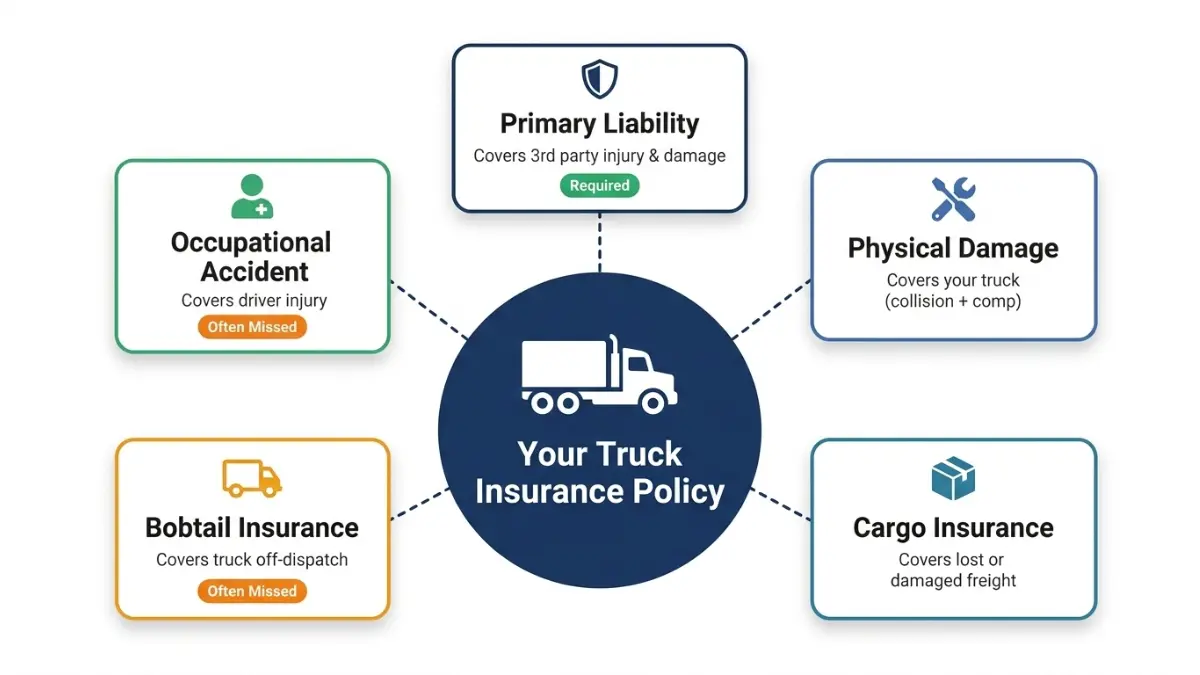

Types of Commercial Truck Insurance Coverage Explained

Not all trucking insurance is the same. Understanding exactly what each coverage type does — and doesn’t — protect is the difference between a manageable claim and a business-ending loss.

Primary Liability — The Non-Negotiable

Primary liability covers bodily injury and property damage you cause to third parties in an accident. This is federally mandated by FMCSA and is the foundation of every commercial truck insurance policy.

Without an active primary liability filing on record with FMCSA, your operating authority is subject to revocation.

Physical Damage (Collision + Comprehensive)

Physical damage covers your own truck — not required by FMCSA, but often required by lenders and leasing companies. It typically costs 3%–6% of your truck’s stated value per year. On a $120,000 tractor, that’s roughly $300–$600/month.

Motor Truck Cargo Insurance

Cargo insurance covers loss or damage to freight in transit. Most freight brokers require minimum $100,000 cargo limits before dispatching loads. Without it, one damaged shipment can erase months of revenue.

Bobtail and Non-Trucking Liability

This is the most misunderstood coverage in trucking. Bobtail insurance covers your truck when you’re driving without a trailer. Non-trucking liability (NTL) covers personal use of your truck outside of dispatch.

If you’re leased to a carrier, their insurance only covers you while under dispatch. The moment you drop a trailer and drive to a rest stop, you’re uninsured without bobtail coverage. Monthly cost: approximately $50–$100.

Occupational Accident Insurance

Owner-operators are typically classified as independent contractors — which means no workers’ compensation coverage. Occupational accident insurance fills this gap, covering medical costs and lost income if you’re injured on the job.

This coverage is skipped by the majority of new owner-operators and almost never mentioned by competitor articles. Monthly cost: approximately $100–$200.

| Coverage Type | What It Covers | Federally Required | Monthly Add-on |

|---|---|---|---|

| Primary Liability | 3rd party injury/property damage | ✅ Yes | Base policy |

| Physical Damage | Your truck (collision + comp) | ❌ No | $300–$600 |

| Cargo Insurance | Lost/damaged freight | ❌ No (brokers require) | Varies |

| Bobtail Insurance | Truck off-dispatch, no trailer | ❌ No | $50–$100 |

| Occupational Accident | Driver injury (no workers’ comp) | ❌ No | $100–$200 |

For a broader view of how commercial coverage fits alongside personal protection, our workers’ compensation guide explains the gap that occupational accident insurance is designed to fill.

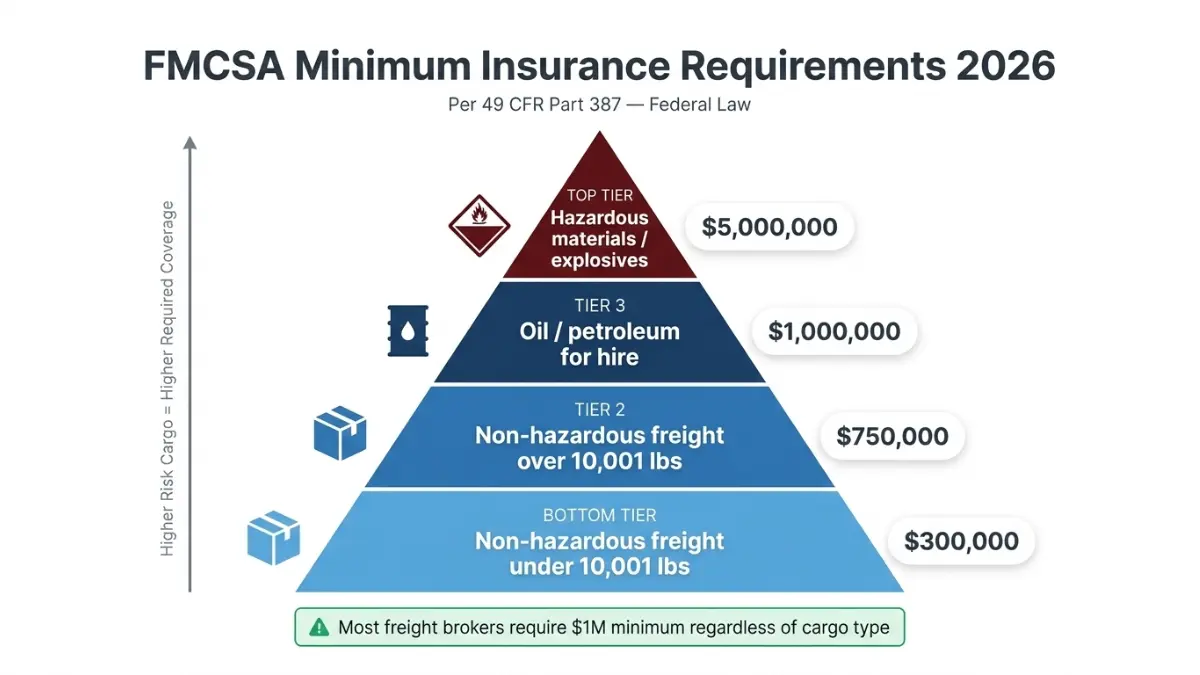

FMCSA Commercial Truck Insurance Requirements (Updated 2026)

Federal minimums are not optional — and they changed more than most carriers realize heading into 2026.

Federal Minimum Coverage Limits by Cargo Type

Per 49 CFR Part 387, all for-hire interstate motor carriers must maintain the following minimum liability limits:

| Cargo Type | Minimum Federal Coverage |

|---|---|

| Non-hazardous freight, under 10,001 lbs | $300,000 |

| Non-hazardous freight, over 10,001 lbs | $750,000 |

| Oil / petroleum products (for-hire) | $1,000,000 |

| Hazardous materials / explosives | $5,000,000 |

Most freight brokers and shippers require $1 million regardless of your FMCSA minimum — so budget for $1M liability from day one.

The New FMCSA Motus System — What Changed in January 2026

This is a critical update that virtually no competitor has covered.

FMCSA launched its new Motus registration system in January 2026, replacing the legacy Licensing and Insurance (L&I) portal. All existing insurance filings must be migrated to Motus. New applicants for operating authority now begin their registration through Motus directly.

What you need to do:

- If you already have an L&I account, log in and “claim” your existing account in Motus to preserve your active filings

- All MCS-90 endorsements and BMC-91 filings continue through your insurer — confirm your insurer is registered as a Motus filer

- Do not allow any gap in your active insurance filing — revocation proceedings begin automatically if filings lapse

For full official Motus instructions, visit FMCSA’s insurance filing requirements page directly.

Staying compliant with FMCSA requirements also connects to your broader business financial health. If you’re managing startup costs alongside insurance, our guide on personal loan rates and traps can help you evaluate financing options without overpaying.

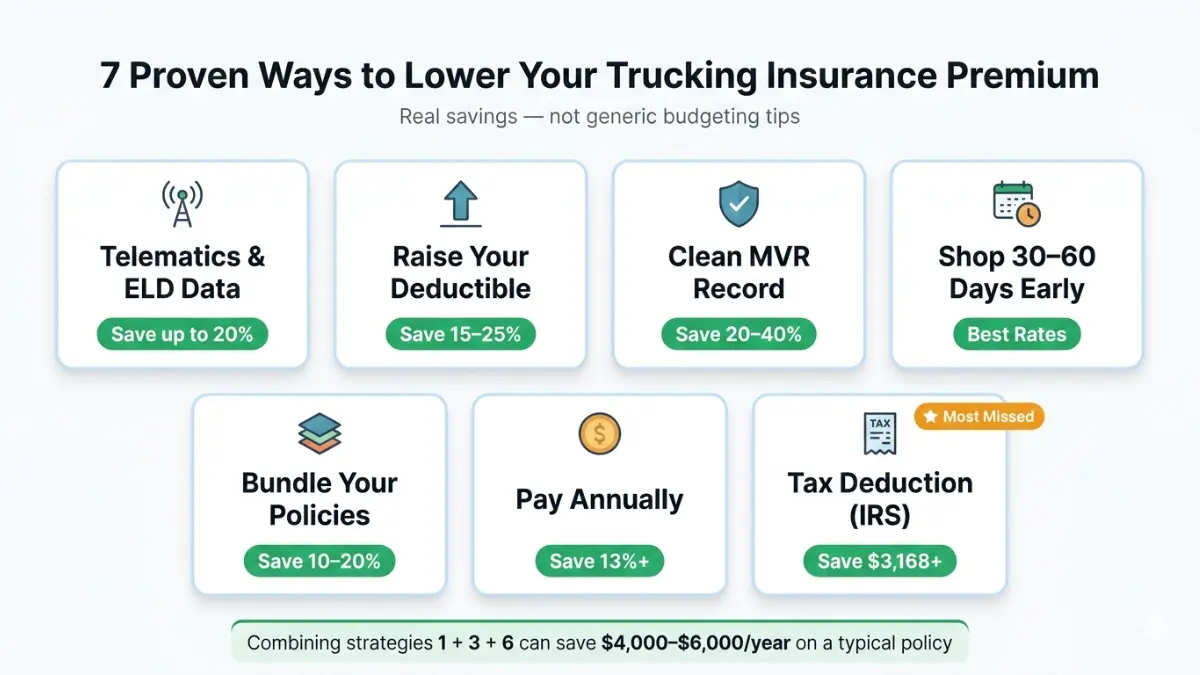

7 Proven Ways to Lower Your Commercial Truck Insurance in 2026

The strategies below are drawn from real underwriting practices — not generic budgeting advice. Each has a documented, quantifiable impact on your annual premium.

1. Use Telematics and ELD Data to Unlock Discounts

Progressive’s Smart Haul® program allows new commercial truck customers to share Electronic Logging Device (ELD) data in exchange for an average saving of $1,261/year. Telematics programs across the industry typically reduce premiums by 5–20% for verified safe drivers.

Install a qualifying dash cam and ELD before your next renewal. Document the data. Present it proactively to underwriters — this signals risk control, not just compliance.

2. Raise Your Deductible Strategically

Increasing your collision deductible from $1,000 to $2,500 typically reduces your physical damage premium by 15–25%. On a $6,000/year physical damage policy, that’s $900–$1,500 in annual savings.

Only raise your deductible to an amount you can actually fund from reserves. A deductible you can’t pay is worse than a higher premium.

3. Maintain a Clean MVR and PSP Record

A spotless Motor Vehicle Record (MVR) and Pre-Employment Screening Program (PSP) history saves 20–40% on your premium. A single serious violation — speeding 15+ mph over the limit, hours-of-service violation, or DUI — can add $3,000–$8,000 annually to your policy cost.

Pull your own PSP report before applying for insurance. Know what underwriters see before they price your risk.

4. Shop 30–60 Days Before Renewal

Last-minute renewal shopping forces you into expensive, limited markets. Starting 30–60 days early gives you leverage to get 3+ competing quotes and negotiate from a position of choice, not desperation.

Rates for identical coverage can vary 30–50% between insurers for the same operator profile.

5. Bundle Policies with One Insurer

Adding cargo coverage, general liability, or occupational accident to your core trucking policy with the same carrier typically saves 10–20% compared to buying separate policies from multiple insurers.

6. Pay Annually Instead of Monthly

Most insurers offer a 13%+ discount for paying your annual premium upfront. On a $10,000 annual policy, that’s a guaranteed $1,300 saving — equivalent to one month of premium, free.

7. Are Your Premiums Tax-Deductible? (Yes — Here’s How)

This is the savings angle almost every competitor article ignores completely.

Commercial truck insurance premiums are fully deductible as ordinary and necessary business expenses under IRS Publication 535. This includes primary liability, physical damage, cargo insurance, bobtail, and occupational accident premiums.

For a driver paying $14,400/year in premiums in the 22% tax bracket, the deduction is worth approximately $3,168 in real tax savings. Work with a tax professional to ensure proper documentation.

| Strategy | Potential Annual Saving |

|---|---|

| Telematics/ELD program | $1,261 avg (Progressive data) |

| Clean MVR/PSP record | 20–40% premium reduction |

| Raise deductible ($1K → $2.5K) | 15–25% on physical damage |

| Annual vs. monthly payment | 13%+ (~$1,300 on $10K policy) |

| Policy bundling | 10–20% |

| Tighten operating radius | 10–15% |

| Premium tax deduction (22% bracket) | ~$3,168 real dollar value |

To get the most out of your business finances alongside insurance savings, explore our income tax 2026 guide for updated bracket information that affects how much your deductions are worth.

Commercial Truck Insurance — 11 Expert FAQs

1. How much does commercial truck insurance cost per month in 2026?

The national average is $421/month for $1 million in liability. Owner-operators under their own authority typically pay $900–$1,800/month for a full package. New authority carriers often pay $1,800–$2,500+/month. Leased-on drivers pay considerably less — typically $250–$500/month — because their carrier covers primary liability.

2. What is the minimum commercial truck insurance required by FMCSA?

FMCSA requires a minimum of $750,000 for most for-hire interstate carriers hauling non-hazardous freight over 10,001 lbs. Hazmat carriers must carry up to $5 million. Most freight brokers require $1 million regardless of the federal minimum. See the full FMCSA requirements for your specific cargo category.

3. How much does commercial truck insurance cost for new authority?

New authority carriers (0–12 months) typically pay 40–100% more than established carriers — often $1,800–$2,500+/month. Rates drop meaningfully after 24–36 months of clean operation and verifiable loss runs.

4. Is commercial truck insurance tax-deductible?

Yes. All commercial truck insurance premiums — including liability, physical damage, cargo, and bobtail — are deductible as ordinary business expenses per IRS Publication 535. Consult a tax professional to document and maximize this deduction.

5. What does commercial truck insurance cover?

A standard policy covers third-party liability (bodily injury and property damage), with optional add-ons for physical damage to your truck, motor truck cargo, bobtail, and occupational accident. The exact coverage depends on your policy structure and the endorsements you select.

6. Why is my commercial truck insurance so expensive?

Three primary drivers: nuclear verdict litigation surging 52% in 2024 (per ATRI), your new authority status if you’re under 24 months of operation, and high-risk cargo or urban operating territory. Your MVR history, truck value, and operating radius are additional major factors.

7. What is bobtail insurance and do I need it?

Bobtail insurance covers your truck when you’re driving without a trailer and off dispatch. If you’re leased to a carrier, their policy only covers you while under dispatch. Any personal or off-dispatch driving without bobtail coverage leaves you completely uninsured. Cost: approximately $50–$100/month — a critical but overlooked protection.

8. How can I get cheaper commercial truck insurance?

The most impactful strategies: maintain a clean MVR/PSP record (saves 20–40%), install telematics (saves 5–20%), pay your premium annually (saves 13%+), shop 30–60 days before renewal, and tighten your declared operating radius. Our cheap insurance guide covers cross-policy savings strategies that also apply to business insurance.

9. What is the difference between owner-operator and fleet truck insurance?

Owner-operators carry their own policy covering one or a small number of trucks. Fleet policies cover multiple vehicles under a single commercial policy, often with volume discounts and streamlined claims management. Fleets typically qualify for lower per-unit rates after reaching 5+ vehicles, depending on the insurer.

10. Does my driving record affect commercial truck insurance rates?

Significantly. A clean MVR saves 20–40% on your premium. Serious violations — DUI, excessive speeding, hours-of-service violations — can add $3,000–$8,000+ annually. Underwriters also check your PSP report (Pre-Employment Screening Program), which shows your full 5-year DOT inspection and violation history. Review yours before applying for coverage.

11. How do I file a commercial truck insurance claim?

Step-by-step:

– Stop and secure the scene — prioritize safety first

– Document everything — photos, police report number, witness contacts

– Notify your insurer immediately — most require same-day or next-day notification

– File the claim — online, by phone, or through your agent

– Cooperate with the adjuster — provide ELD data, dash cam footage, and maintenance records

– Track your claim timeline — commercial truck claims typically resolve in 30–90 days depending on complexity

Delayed reporting is one of the most common reasons claims are reduced or denied. Call your insurer the same day, even if you’re unsure whether to file.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or insurance advice. Commercial truck insurance costs and regulatory requirements vary by state, carrier, cargo type, and individual operator profile. Rate data reflects 2026 market analysis and is subject to change. Always consult a licensed insurance professional and refer to fmcsa.dot.gov for official federal requirements before making coverage decisions.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.