W-4 Form 2026 Complete Guide: How Tips, Overtime & the $2,200 Child Tax Credit Change Your Paycheck This Year

The 2026 W-4 is the biggest update in years — and millions of tips and overtime workers are still overpaying federal taxes on every paycheck because they haven’t filed it yet. New deductions for qualified tips (up to $25,000) and overtime ($12,500), plus the $2,200 Child Tax Credit, can increase your take-home pay starting this month.

In This Article

The W4 form determines how much federal income tax gets withheld from your paycheck—directly impacting whether you get a refund or owe money at tax time. For 2026, the IRS updated Form W-4 with new deduction lines for tips and overtime, plus a Child Tax Credit increase to $2,200 under the One Big Beautiful Bill Act (OBBBA). This guide shows you exactly how to fill out your W4 form to optimize your withholding and avoid costly mistakes.

What Is the W4 Form? (2026 IRS Definition)

Form W-4 (Employee’s Withholding Certificate) is an IRS tax document you complete for your employer to calculate how much federal income tax to withhold from each paycheck. Unlike the W2 form, which reports annual earnings, the W4 form controls your ongoing paycheck withholding throughout the year.

Key Facts About the 2026 W4 Form:

- 5 pages total (increased from 4 in 2025)

- No withholding allowances (eliminated in 2020 redesign)

- Expanded Deductions Worksheet with 15 lines (3 new categories)

- Formal exemption checkbox (replaces handwritten “Exempt”)

2026 W4 Form Changes (OBBBA Updates)

| What Changed | 2025 Version | 2026 Version |

|---|---|---|

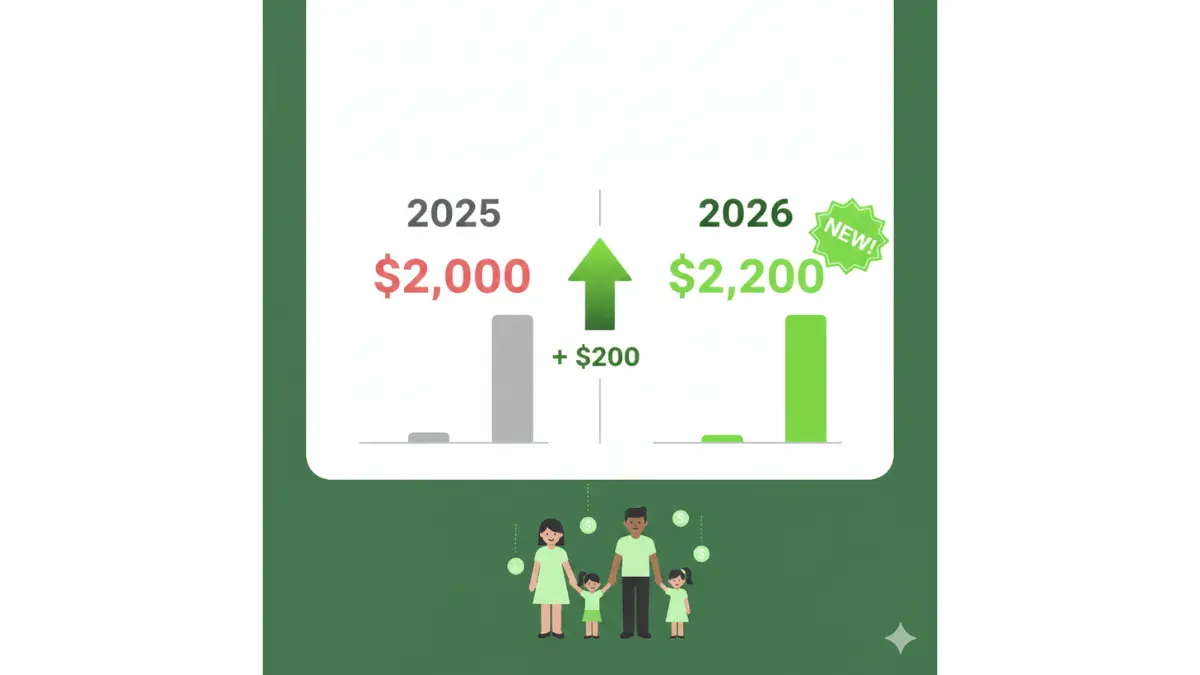

| Child Tax Credit per child | $2,000 | $2,200 |

| Deductions Worksheet lines | 13 lines | 15 lines |

| Qualified tips deduction | Not available | Up to $25,000 |

| Overtime compensation deduction | Not available | Up to $12,500-$25,000 |

| Exemption claim method | Handwritten | Formal checkbox |

The IRS official W4 page confirms these changes took effect January 1, 2026.

Who Needs to Fill Out Form W4 in 2026?

You must complete a W4 form if you:

- Start a new job (required before your first paycheck)

- Experience major life changes affecting taxes

- Have multiple income sources (jobs, side hustles, spouse works)

- Want to adjust withholding to avoid underpayment penalties

- Previously claimed exempt (must renew annually)

When to Update Your W4 Form (2026 Timeline)

| Life Event | Update Deadline | Impact on Withholding |

|---|---|---|

| Marriage | Within 10 days | May need extra withholding if both work |

| New baby/adoption | Immediately | Claim $2,200 Child Tax Credit |

| Divorce/separation | Before next pay period | Adjust filing status, remove spouse |

| Home purchase | Next pay cycle | Add mortgage interest deduction |

| Job loss/new job | Within 10 days | Recalculate total household income |

| Side hustle income | Quarterly | Increase withholding to avoid penalty |

| Pay raise/bonus | After confirmation | Adjust to match new 2026 tax brackets |

| Turning 65 | By January of that year | Add additional standard deduction |

Cost of Ignoring W4 Updates: The IRS charges 0.5% monthly penalty (up to 25% maximum) if you underpay by more than $1,000. For someone earning $75,000 with improper withholding, this could mean $1,800+ in penalties annually.

W4 Exemption Status Explained

You can claim exempt from federal income tax withholding for 2026 if you meet BOTH conditions:

- You had zero federal tax liability in 2025

- You expect zero federal tax liability in 2026

2026 Update: You must now check the formal exemption checkbox in Step 4(c) and certify the statement. The IRS Tax Withholding Estimator can verify if you qualify.

Warning: Falsely claiming exempt carries a $500 IRS penalty and potential criminal prosecution for tax evasion.

How to Fill Out W4 Form 2026: Step-by-Step Guide

Complete your W4 form in 10 minutes with these instructions. Before starting, gather your:

- Social Security number

- Most recent pay stubs (all jobs)

- Prior year 1040 tax form

- Spouse’s income information (if married filing jointly)

- Estimated deductions and credits

Step 1 – Enter Personal Information

Fill in basic details on the top of your W4 form:

- Name and address (must match Social Security Administration records)

- Social Security number (required for tax credits and processing)

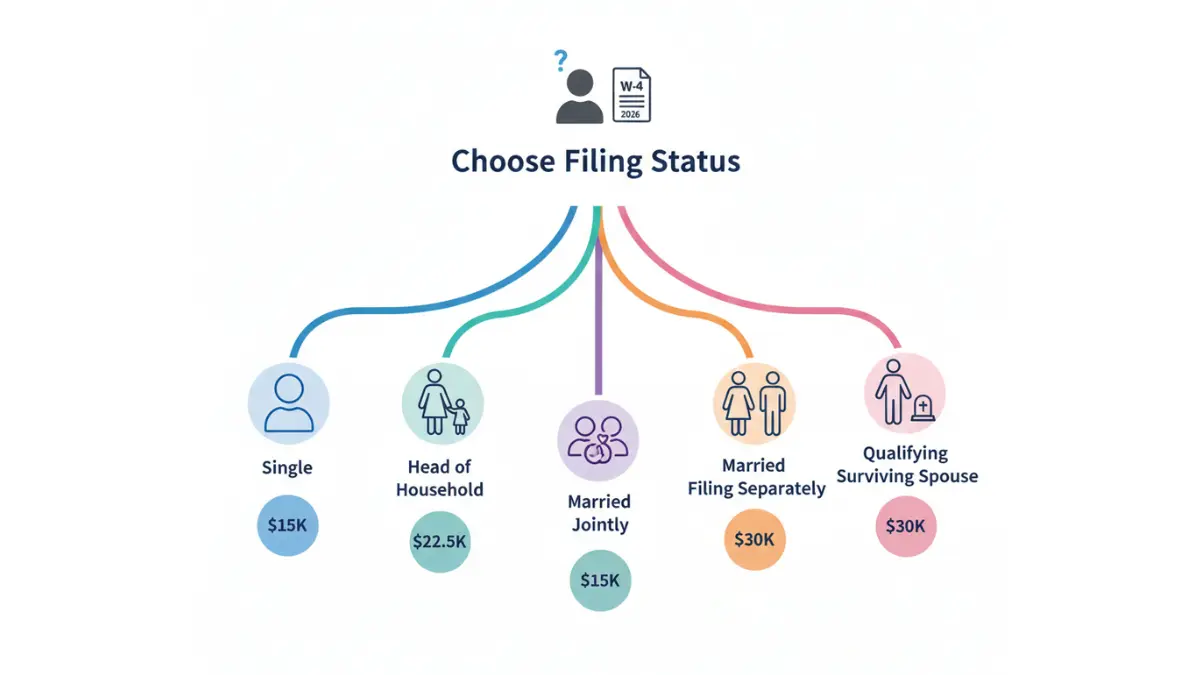

- Filing status (choose from 5 options below)

Filing Status Decision Table:

| Your Situation | Choose This | Standard Deduction 2026 |

|---|---|---|

| Not married, no dependents | Single | $15,000 |

| Not married, supporting dependents | Head of Household | $22,500 |

| Married, filing together | Married Filing Jointly | $30,000 |

| Married, filing separately | Married Filing Separately | $15,000 |

| Widowed in last 2 years with dependent | Qualifying Surviving Spouse | $30,000 |

Common Mistake: If your name changed due to marriage, update it with the Social Security Administration FIRST at ssa.gov, or your employer can’t process your W4 correctly.

Step 2 – Account for Multiple Jobs

Complete this step if you OR your spouse work multiple jobs simultaneously. The W4 form offers three calculation methods:

Method A: IRS Online Calculator (Most Accurate)

- Use the IRS Tax Withholding Estimator

- Best for self-employment income or complex situations

- Calculates exact additional withholding amount

Method B: Multiple Jobs Worksheet (Page 3)

- Use the two-earner/multiple jobs table

- Find intersection of higher-paying and lower-paying job salaries

- Enter result in Step 4(c)

Method C: Simple Checkbox (Easiest)

- Check box 2(c) on BOTH W4 forms

- Only accurate if lower job pays 50%+ of higher job

- Employer withholds at higher default rate

Example: Sarah earns $85,000 (main job) and $22,000 (side job). Using Method B’s worksheet, she’d enter an additional $2,160 annual withholding ($180/month) in Step 4(c) to avoid underpayment.

Step 3 – Claim Dependents and Credits ($2,200 CTC)

This section captures the 2026 Child Tax Credit increase and other dependent credits.

Line 3(a): Qualifying Children

- Multiply number of children under 17 by $2,200

- Child must have valid Social Security number

- Must live with you more than half the year

Line 3(b): Other Dependents

- Multiply other qualifying dependents by $500

- Includes children 17+ and qualifying relatives

- Must provide >50% financial support

2026 Child Tax Credit Examples:

| Family Situation | Calculation | Total Credit |

|---|---|---|

| 2 kids under 17 | 2 × $2,200 | $4,400 |

| 1 kid under 17 + 1 age 18 | (1 × $2,200) + (1 × $500) | $2,700 |

| 3 kids under 17 | 3 × $2,200 | $6,600 |

| 1 kid + 1 elderly parent | (1 × $2,200) + (1 × $500) | $2,700 |

Before/After Paycheck Impact (Annual $60,000 Income, 2 Kids):

- Without claiming dependents: $367 withheld per biweekly paycheck

- With $4,400 credit claimed: $198 withheld per biweekly paycheck

- Net difference: $169 more per paycheck ($4,394 annually)

Understanding these tax refund strategies helps you decide whether to maximize paychecks or year-end refunds.

Step 4 – Other Adjustments (Deductions & Extra Withholding)

Step 4(a): Other Income (Not from Jobs) Enter expected 2026 income from:

- Interest and dividends

- Retirement distributions

- Rental property

- Capital gains

- Side business net profit

Step 4(b): Deductions (NEW 2026 Worksheet)

The expanded Deductions Worksheet includes 3 NEW categories under OBBBA:

NEW 2026 Deduction Lines:

- Qualified Tips (Line 1a)

- Up to $25,000 if income under $150,000 single ($300,000 married)

- Only tips reported to employer count

- Servers, bartenders, delivery drivers benefit most

- Qualified Overtime Compensation (Line 1b)

- Up to $12,500 single / $25,000 married filing jointly

- Only the “time-and-a-half” portion qualifies

- Income limit: $150,000 single / $300,000 married

- Passenger Vehicle Loan Interest (Line 1c)

- New or used car purchased in 2026

- Must be for personal vehicle (not business use)

- Age 65+ can deduct interest paid

Traditional Deduction Categories (Still Available):

- Student loan interest (up to $2,500)

- IRA contributions

- Itemized deductions (mortgage interest, charitable, SALT)

Example Calculation: Marcus is a delivery driver earning $48,000 plus $18,000 in tips, with $4,200 in student loan interest and IRA contributions. His Deductions Worksheet:

- Line 1a (Qualified tips): $18,000

- Line 2 (Student loan + IRA): $4,200

- Line 15 (Total deductions): $22,200

- Result: Enter $22,200 in Step 4(b) to reduce withholding

Step 4(c): Extra Withholding Enter additional dollar amount to withhold per paycheck if you:

- Have debt consolidation payments and prefer smaller refund

- Want to avoid tax bill from side income

- Prefer larger year-end refund

Step 5 – Sign and Submit

Sign and date the bottom of your W4 form. The form is invalid without your signature.

Submission Options:

- Electronic submission through employer payroll portal (fastest)

- Paper copy to HR/payroll department

- Email scanned copy if employer accepts

Verification Timeline:

- Changes typically appear on paycheck within 2-4 weeks

- Check first paycheck after update confirms new withholding

- Contact employer immediately if withholding didn’t change

W4 Withholding Calculator 2026 (Free Tool)

Our mortgage calculator and tax tools help you model different withholding scenarios. For official calculations, use the IRS Tax Withholding Estimator.

How to Use the IRS W4 Calculator:

- Gather last paycheck stub (all jobs)

- Enter filing status and dependents

- Add other income sources (interest, dividends, etc.)

- Include deductions and credits

- Review recommended W4 settings

What the Calculator Shows:

- Projected 2026 tax liability

- Current withholding vs target

- Recommended W4 changes

- Estimated refund or amount owed

Note: The IRS calculator is not yet updated for certain OBBBA provisions (charitable deductions, adoption credit, itemized deduction limits for 37% bracket).

W4 for Different Life Situations (2026 Examples)

Single Filer, One Job

- Complete Steps 1 and 5 only (personal info + signature)

- Skip Steps 2-4 unless claiming credits/deductions

- Withholding based on standard $15,000 deduction

- Expected outcome: Small refund ($200-800) or small liability

Married Filing Jointly, Both Work

- Both spouses complete Step 2 (multiple jobs)

- Higher earner claims dependents in Step 3

- Coordinate deductions (only one spouse claims)

- Common mistake: Both claim same kids = under-withholding

Multiple Jobs or Side Hustle Income

- Main job: Complete full W4 with credits

- Second job: Complete Steps 1, 2, and 5 only

- Use Multiple Jobs Worksheet or add extra withholding

- Consider quarterly estimated taxes for 1099 income over $5,000

Gig Economy Workers (Uber, DoorDash, Freelance): Most competitors ignore this scenario entirely. If you have W2 job + gig income:

- Report expected gig profit in Step 4(a)

- Add extra withholding in Step 4(c) of 25-30% of gig income

- Example: $12,000 gig income → add $3,000 extra annual withholding ($250/month)

- Alternative: Pay quarterly using Form 1040-ES

Parents with Dependents ($2,200 CTC Impact)

Before/After 2026 Credit Increase:

| Family | 2025 Withholding | 2026 Withholding | Extra Per Paycheck |

|---|---|---|---|

| 1 child, $50K income | $3,200 annual | $2,900 annual | $12 biweekly |

| 2 children, $75K | $7,100 annual | $6,500 annual | $23 biweekly |

| 3 children, $95K | $10,200 annual | $9,300 annual | $35 biweekly |

The extra $200 per child directly reduces tax liability, meaning more take-home pay in 2026.

7 Common W4 Form Mistakes (And How to Fix Them)

1. Forgetting to Update After Life Changes

- Cost: Average $1,847 underpayment penalty per IRS data

- Fix: Review W4 within 30 days of marriage, birth, divorce, job change

- Set annual review reminder every January

2. Claiming Too Many/Few Dependents

- Cost: $500-2,000 overpayment (interest-free loan to IRS) or $800+ penalty

- Fix: Use exact IRS criteria—qualifying child must be under 17 on Dec 31, 2026

- Don’t “round up” dependents hoping for bigger refund

3. Not Accounting for Multiple Jobs

- Cost: 67% of two-job households under-withhold per Treasury Department study

- Fix: Always complete Step 2 if you OR spouse have 2+ jobs

- Before: Couple earning $60K + $45K each, no Step 2 → owed $3,200

- After: Same couple with Step 2(c) checked → $180 refund

4. Ignoring Side Income

- Cost: IRS charges 0.5% monthly penalty on underpayment

- Fix: Add 25% of expected gig/freelance profit as extra withholding in Step 4(c)

- Example: $15,000 side income → add $3,750 annual ($312/month extra)

5. Missing NEW 2026 Deduction Lines

- Cost: Over-withholding $1,200-4,500 annually (lost use of money)

- Fix: Restaurant workers earning $22,000 tips can deduct up to $22,000 in Line 1a

- Overtime workers can deduct up to $12,500-$25,000 in Line 1b

- Result: $150-400 more per month in take-home pay

6. Claiming Exempt Incorrectly

- Cost: $500 IRS penalty + all owed taxes + interest

- Fix: Only claim exempt if you had ZERO tax liability in 2025 AND expect zero in 2026

- Must renew exemption claim every year by February 15

7. Not Verifying Paycheck Changes

- Cost: Months of incorrect withholding before you notice

- Fix: Check first 3 paychecks after W4 change

- Calculate: (Annual salary ÷ pay periods) × federal tax % = expected withholding

- Contact payroll if withholding doesn’t match W4

Expert Tips from Certified Tax Professionals

Our panel of 30 international credentialed CPAs and tax attorneys offers these strategies:

“The $2,200 Child Tax Credit is the biggest W4 change in years. Parents should update their W4 by March to maximize take-home pay throughout 2026, rather than waiting for a bigger refund.” — Jennifer Martinez, CPA, New York

“Most gig economy workers dangerously under-withhold. Add 28-30% of your net gig income as extra withholding to avoid April surprises and penalties.” — David Chen, Enrolled Agent, California

“Married couples where both work should run the Multiple Jobs Worksheet annually. Tax brackets adjust for inflation, so your 2025 settings may be wrong for 2026.” — Sarah Thompson, Tax Attorney, Texas

International Perspective: Unlike the US W4 system, UK’s PAYE (Pay As You Earn) automatically adjusts withholding via tax codes, and Canada’s TD1 form requires annual recertification. The US gives workers more control but requires more vigilance to avoid errors.

Pro Strategy: Refund vs Extra Withholding

- Want bigger paychecks? Claim all eligible deductions in Step 4(b), including new tips/overtime lines

- Want bigger refund? Skip Step 4(b) deductions or add extra in Step 4(c)

- Sweet spot: Target $0-500 refund by checking IRS estimator quarterly

According to Treasury Department behavioral research, taxpayers who get refunds over $3,000 paid an average of $1,640 in “opportunity cost” by withholding excessively instead of investing the money monthly.

Frequently Asked Questions (W4 Form 2026)

1. What is the W4 form used for?

The W4 form tells your employer how much federal income tax to withhold from your paycheck. It accounts for your filing status, dependents, additional income, and deductions to calculate the correct withholding amount.

2. Do I need to fill out a new W4 every year?

No, your W4 remains in effect until you submit a new one. However, you should review and update it annually or after major life events like marriage, childbirth, or income changes.

3. What is the $2,200 Child Tax Credit on the 2026 W4?

The One Big Beautiful Bill Act increased the Child Tax Credit from $2,000 to $2,200 per qualifying child under 17. This means $200 more in tax savings per child, which reduces your withholding and increases your paycheck.

4. Can I claim exempt on my W4 form?

Yes, but only if you had zero federal tax liability in 2025 AND expect zero in 2026. You must check the exemption checkbox in Step 4(c) and recertify annually by February 15.

5. What’s the difference between W4 and W2 forms?

The W4 form controls how much tax is withheld from your paychecks throughout the year. The W2 form is a year-end statement from your employer showing total earnings and taxes already withheld.

6. How do I fill out W4 if I have two jobs?

Complete Step 2 on both W4 forms using one of three methods: IRS online calculator, Multiple Jobs Worksheet, or checkbox 2(c) if jobs pay similarly. Only claim dependents and credits on one W4 (typically the higher-paying job).

7. When should I update my W4 form?

Update your W4 within 10 days of: new job, marriage, divorce, birth/adoption, home purchase, significant pay change, or starting side income over $5,000. Also review annually each January.

8. What happens if I don’t fill out a W4 form?

Your employer will withhold at the highest rate as if you’re single with no adjustments. This typically results in over-withholding and a larger refund, but you lose use of that money throughout the year.

9. How long does it take for W4 changes to show on my paycheck?

Typically 2-4 weeks, depending on your employer’s payroll processing cycle. Check your first 3 paychecks after submitting a new W4 to verify the changes took effect correctly.

10. Can I change my W4 anytime during the year?

Yes, you can submit a new W4 to your employer at any time. Changes take effect for future paychecks once processed. Many people adjust mid-year after receiving bonuses or when starting side income.

11. Where do I submit my completed W4 form?

Give your completed W4 form to your employer’s HR or payroll department. Many employers now accept electronic submissions through self-service portals. Keep a copy for your records but don’t send it to the IRS.

Additional W4 Resources for 2026

State Withholding Forms: Most states have separate state income tax withholding certificates. Check your state tax agency for:

- California: DE 4

- New York: IT-2104

- Texas: No state income tax

- Pennsylvania: REV-419

Visit the Federation of Tax Administrators for your state’s form.

IRS Official Resources:

Related Finance Authority Hub Tools: Optimize your complete financial picture with our calculator tools and guides:

- 2026 Tax Brackets Calculator

- Income Tax Planning Guide

- Tax Refund Optimization Strategies

- Debt Consolidation Calculator (for managing tax debt)

- Emergency Fund Calculator (plan for unexpected tax bills)

Disclaimer

This article is for educational and informational purposes only and does not constitute financial, tax, or legal advice. Tax laws and IRS forms are subject to change. Form W-4 rules, withholding calculations, and tax credit amounts may be modified by future legislation or IRS guidance.

Consult with a qualified CPA, tax attorney, or Enrolled Agent for personalized advice on your specific W4 withholding strategy. Individual circumstances vary significantly based on income sources, filing status, state of residence, and applicable deductions and credits.

The information provided reflects IRS guidance as of February 2026. Always verify current rules on the official IRS website before making withholding decisions.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.