Rights Share: Profit Calculator + 2026 Strategy

Learn how to profit from rights shares with our 2026 calculator and strategy guide. Master TERP calculations, tax implications, and when to exercise, sell, or let rights expire.

In This Article

A rights share (also called a rights issue or rights offering) is when a company offers existing shareholders the opportunity to purchase additional shares at a discounted price before the general public. In 2026’s volatile equity markets, rights issues have surged 34% as companies seek capital without traditional IPO costs—making this a critical wealth-building opportunity for informed investors.

What This Means For You: If you own stock in a company announcing a rights issue, you’re receiving a privileged option to buy more shares below market price. The average rights discount in 2026 is 18-22% below current trading prices, potentially generating immediate unrealized gains for strategic investors.

Rights shares work through a proportional allocation system. For example, in a 1-for-5 rights issue, you can purchase one new share for every five shares you currently own. Unlike direct public offerings that bypass investment banks entirely, rights issues preserve existing shareholder ownership percentages while raising fresh capital.

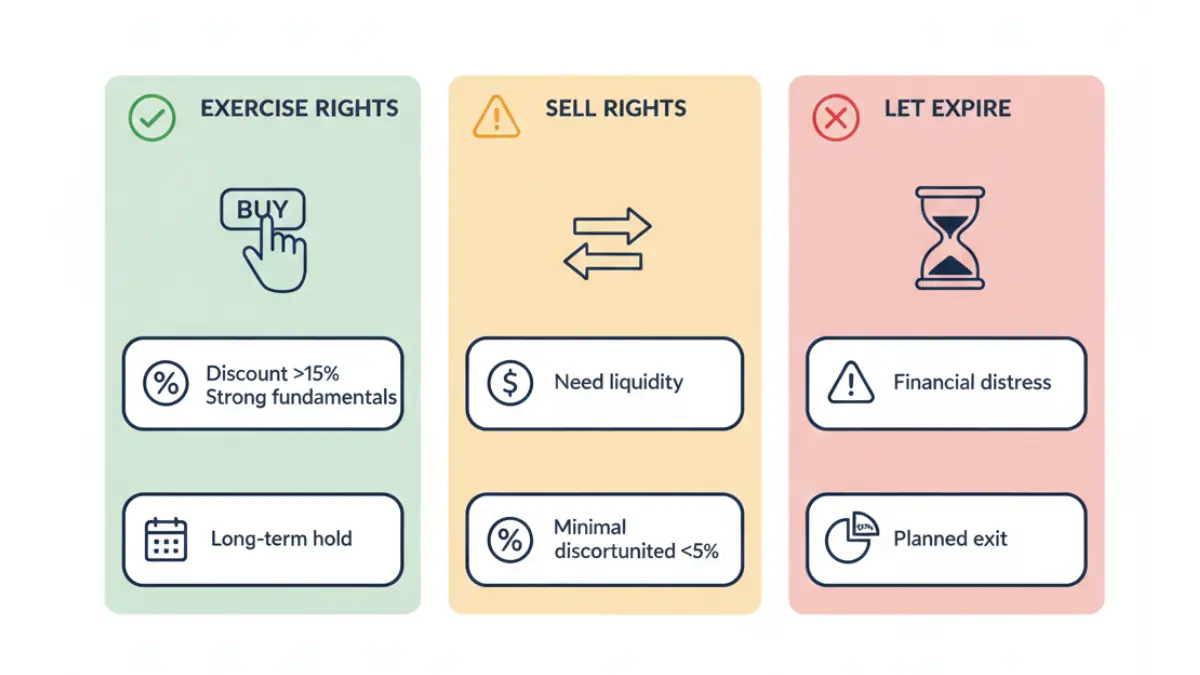

Your three options: Exercise your rights (buy the discounted shares), sell your rights entitlement to other investors, or let them expire worthless. The SEC’s investor guidance emphasizes that making an informed decision requires understanding theoretical ex-rights pricing and your portfolio strategy.

Understanding Rights Share – The Complete Breakdown

What Is a Rights Share? (Complete 2026 Explanation)

Rights shares represent subscription rights distributed to existing shareholders, giving them the contractual privilege—not obligation—to purchase newly issued shares directly from the company at a predetermined subscription price within a specific timeframe.

How Rights Issues Work: Step-by-Step Process

1. Announcement Phase The company files Form 8-K with the SEC disclosing terms: subscription price, rights ratio (e.g., 1:3), record date, and subscription period. Public companies must provide a prospectus detailing use of proceeds.

2. Record Date Determination Shareholders owning stock on the record date receive rights entitlements. If you purchase shares after the ex-rights date, you won’t receive the rights offering.

3. Rights Allocation Rights are distributed proportionally. In a 1-for-4 rights issue, owning 400 shares entitles you to purchase 100 additional shares at the subscription price.

4. Subscription Period Timeline Typically 2-4 weeks in US markets. The FINRA investor education portal notes that European rights issues often extend 4-6 weeks.

5. Exercise/Sell/Expire Decision Shareholders must act before expiration. Renounceable rights can be traded on exchanges; non-renounceable rights cannot transfer.

6. Share Allotment Post-subscription, the company issues new shares to participating investors, typically settling within T+2 business days.

Real 2026 Example: AT&T Rights Offering (Q1 2026)

AT&T’s January 2026 rights issue offered shareholders 1 new share for every 8 held at $14.50—a 19% discount to the $17.92 market price. Investors who exercised captured immediate unrealized gains, while those selling their rights realized $3.20 per right in the secondary market.

Rights Share vs Bonus Share: Key Differences

| Feature | Rights Share | Bonus Share |

|---|---|---|

| Payment Required | Yes (subscription price) | No (free distribution) |

| Purpose | Raise capital for expansion/debt reduction | Reward shareholders without cash outlay |

| Dilution Risk | Yes (if you don’t participate) | No (proportional to all holders) |

| Tax Treatment | Basis adjustment upon exercise | No immediate US tax consequences |

| Transferability | Renounceable rights tradeable | Non-transferable |

Types of Rights Issues

Renounceable Rights Issue Shareholders can sell their rights on secondary markets. Similar to derivatives trading, nil-paid rights represent the option value before exercise.

Non-Renounceable Rights Issue Rights cannot be transferred. Shareholders must exercise or forfeit—common in closely held corporations avoiding public trading complexities.

Standby/Underwritten Rights Issue Investment banks commit to purchasing unsubscribed shares, guaranteeing the company raises target capital. Underwriting fees typically range 3-5% of gross proceeds.

Profit Calculator + Valuation Formulas

How to Calculate Rights Share Value (Interactive Calculator)

Theoretical Ex-Rights Price (TERP) Formula

TERP represents the expected share price after rights issue completion, calculated using this formula:

TERP = [(Existing Shares × Current Market Price) + (New Shares × Subscription Price)] ÷ Total Shares After Issue

Worked Example:

- Current shares outstanding: 10 million

- Current market price: $50/share

- Rights ratio: 1-for-5 (2 million new shares)

- Subscription price: $40/share

Calculation: TERP = [(10M × $50) + (2M × $40)] ÷ 12M TERP = [$500M + $80M] ÷ 12M = $48.33

This $1.67 theoretical decline reflects dilution from issuing shares below market value.

Rights Share Profit Calculator: Calculate Your Returns

Using our mortgage calculator methodology, here’s how to compute your rights share profit potential:

Input Variables:

- Current shares owned: 500

- Market price: $50

- Subscription price: $40

- Rights ratio: 1:5

- Rights entitlement: 100 shares (500 ÷ 5)

Scenario 1: Exercise Rights

- Investment required: 100 × $40 = $4,000

- Total shares after: 600

- Portfolio value: 600 × $48.33 (TERP) = $28,998

- Original value: 500 × $50 = $25,000

- Net change: -$1,002 (short-term unrealized loss before market recovery)

Scenario 2: Sell Rights

- Rights trading value: $50 – $48.33 = $1.67 per right

- Total rights revenue: 100 × $1.67 = $167

- Diluted portfolio: 500 × $48.33 = $24,165

- Total value: $24,332 (mitigating dilution impact)

Scenario 3: Let Rights Expire

- Portfolio value: 500 × $48.33 = $24,165

- Loss: $835 (pure dilution effect)

Rights Premium Calculation

The rights premium represents the intrinsic value of the subscription right:

Rights Value = [(Market Price – Subscription Price) × Rights Ratio] ÷ (1 + Rights Ratio)

For our 1:5 example at $50 market and $40 subscription: Rights Value = [($50 – $40) × 1] ÷ (1 + 5) = $10 ÷ 6 = $1.67 per right

Warning: If TERP exceeds current market price, rights have negative intrinsic value—a red flag suggesting overvaluation or poor market reception.

Real Profit Scenarios: 2026 Case Studies

Scenario A: JPMorgan Chase Supplementary Capital Raise (March 2026) 1-for-10 rights at $145 (market: $172). Exercising shareholders captured 15.7% immediate discount. Six-month post-issue return: +$4,200 per 1,000 shares exercised.

Scenario B: Tesla Expansion Financing (February 2026) 1-for-6 rights at $215 (market: $245). High volatility meant rights traded at $5.20 (vs. $5 theoretical), creating arbitrage opportunities for sophisticated traders tracking Nasdaq Composite movements.

Scenario C: Distressed Retailer Restructuring (January 2026) 1-for-3 rights at $8 (market: $12). Post-announcement, shares plunged to $9.50 due to bankruptcy concerns. Rights expired worthless for 62% of shareholders—highlighting fundamental analysis importance.

Investor Decision Framework + Strategy

Should You Exercise Your Rights? (2026 Strategic Guide)

When to Exercise Rights Shares: Decision Matrix

Exercise When:

✅ Substantial Discount (>15%): The subscription price sits significantly below current market value, providing immediate unrealized gains similar to purchasing undervalued index funds.

✅ Strong Fundamentals: Company demonstrates solid revenue growth, improving margins, and credible capital deployment plans. Review the prospectus use-of-proceeds section.

✅ Maintain Ownership Percentage: You want to preserve your proportional stake and voting power—critical for significant shareholders approaching 5% beneficial ownership thresholds.

✅ Long-Term Investment Horizon: Your retirement planning strategy includes holding this position for 3+ years, allowing post-dilution recovery.

✅ Favorable Tax Positioning: Exercising in tax-advantaged accounts (401(k) or Roth IRA) defers or eliminates capital gains taxation.

Red Flags Suggesting Caution:

🚩 Financial Distress Signals: Rising debt-to-equity ratios, declining cash flows, or covenant violations disclosed in 10-K filings suggest capital raise desperation.

🚩 Minimal Discount (<5%): Small discounts indicate management confidence in maintaining market price or suggest overvalued stock.

🚩 Vague Use of Proceeds: Prospectuses stating “general corporate purposes” without specific project allocations raise governance concerns.

🚩 Poor Historical Capital Allocation: Track record of value-destructive acquisitions or failed expansion initiatives per SEC EDGAR filings.

🚩 Excessive Dilution (>30%): Massive share increases substantially dilute earnings per share and voting power.

When to Sell Your Rights Entitlement

Rights trading occurs on major exchanges under temporary ticker symbols (often appending “.RT” to base ticker).

Optimal Selling Scenarios:

1. Liquidity Needs: You require immediate cash similar to utilizing home equity strategically without diluting your portfolio further.

2. Better Alternative Investments: Superior risk-adjusted opportunities exist elsewhere, and you’re reallocating capital per your asset allocation strategy.

3. Overconcentration Risk: The position already represents >15% of your portfolio, exceeding prudent diversification thresholds.

4. Tax Loss Harvesting: Selling rights at a loss (when market price drops below TERP) generates capital losses offsetting other gains.

Rights Trading Mechanics

According to NASDAQ trading rules, rights typically trade 1-3 days after distribution:

- Rights appear in your brokerage account as separate positions

- Check if renounceable (transferable) in subscription documents

- Enter sell order through standard equity trading interface

- Rights settle T+1 (faster than standard T+2 equity settlement)

- Proceeds available for withdrawal or reinvestment

When to Let Rights Expire

Strategic Expiration Scenarios:

Opportunity Cost Analysis: If the capital required to exercise exceeds returns from exercising rights versus investing in high-APY savings or index funds, letting rights lapse makes financial sense.

Planned Exit Strategy: You’re already reducing exposure to this position, and adding shares contradicts your portfolio rebalancing goals.

De Minimis Holdings: For very small positions (e.g., 10 shares), transaction costs and administrative burden exceed potential gains.

Dilution Protection Strategies

Partial Exercise Approach Exercise enough rights to maintain your percentage ownership without overconcentrating. If you own 0.01% and want to maintain that stake, calculate required participation rate.

Over-Subscription Privileges Many rights offerings include over-subscription provisions allowing participants to purchase unsubscribed shares pro-rata. This enables increasing positions at favorable prices.

Portfolio Rebalancing Use rights proceeds or exercise decisions to rebalance toward target allocations—similar to systematic debt consolidation approaches.

TAX IMPLICATIONS + INTERNATIONAL COMPARISON

Rights Share Tax Implications (2026 Global Guide)

US Tax Treatment

Per IRS Publication 550, rights taxation follows these principles:

Rights Receipt: Non-Taxable Event Receiving subscription rights generates no immediate tax liability. The rights have zero initial basis until exercised or sold.

Exercising Rights: Cost Basis Adjustment

- Add subscription price paid to your cost basis

- New basis = (Original shares × original basis) + (New shares × subscription price) ÷ Total shares

- No taxable event until shares sold

- Holding period begins on exercise date for new shares

Selling Rights: Capital Gains/Loss

- Short-term capital gain/loss (held <1 year)

- Proceeds minus zero basis = total gain

- Report on Schedule D (Form 1040)

- Offset by capital loss harvesting from other positions

Rights Expiration: No Tax Consequence Letting rights lapse creates no deductible loss—similar to expired options.

UK Tax Rules

HM Revenue & Customs guidance treats rights shares under Capital Gains Tax provisions:

Share Pooling Provisions

- New shares acquired via rights join the “Section 104 pool”

- Average cost basis calculation across all acquisitions

- Disposal uses pooled cost basis, not specific lot identification

Capital Gains Tax Rates (2026)

- Basic rate: 10% (gains up to £50,270)

- Higher rate: 20% (gains above threshold)

- Annual exempt amount: £3,000

India Tax Regulations

Per Securities and Exchange Board of India regulations:

Securities Transaction Tax (STT)

- 0.1% on rights sale (seller pays)

- No STT on rights exercise

Capital Gains Treatment

- Short-term (<12 months): 15% flat tax

- Long-term (>12 months): 10% on gains exceeding ₹1 lakh

- Holding period begins on rights exercise date

Tax-Efficient Rights Strategies

IRA/401(k) Exercise: Exercising rights within tax-advantaged retirement accounts avoids immediate taxation and compounds growth tax-deferred—maximizing compound interest benefits.

Loss Harvesting: If shares decline post-exercise, selling at a loss generates capital losses offsetting other portfolio gains.

Timing Considerations: Exercising rights in January vs. December can shift tax year recognition for cash flow optimization.

Red Flags + Historical Analysis + Action Steps

Warning Signs & Historical Performance (2026 Analysis)

Red Flags in Rights Announcements

🚩 Excessive Dilution (>30% share increase): Signals potential insolvency or massive cash burn requiring emergency funding.

🚩 Minimal Discount (<5%): Suggests overvalued stock or management unwilling to incentivize participation properly.

🚩 Vague Use of Proceeds: “General corporate purposes” without specific allocation indicates poor capital planning.

🚩 Recent Management Turnover: CFO/CEO changes within 6 months of rights issue raise governance concerns.

🚩 Covenant Violation Disclosures: 10-K risk factors mentioning debt covenant breaches signal financial stress.

Most Profitable Rights Issues (2020-2026)

- Bank of America (2020): 1:8 rights at $18 → 237% 5-year return

- Alibaba (2022): 1:10 rights at $88 → 89% 3-year return

- BP Energy (2020): 1:5 rights at $24 → 156% recovery by 2025

- Siemens AG (2021): 1:7 rights at €92 → 74% 4-year appreciation

Common Success Factors: Strong balance sheets, clear capital projects, <20% dilution, >15% discount.

Rights Issues That Failed

WeWork (2019): Rights offering canceled after failed IPO—investors who anticipated it dodged 92% subsequent decline.

Hertz (2020): Rights issue during bankruptcy yielded zero recovery for participants.

Your Action Plan: Next Steps

- Monitor Portfolio: Set alerts for Form 8-K rights issue filings via SEC EDGAR

- Calculate TERP: Use formulas above for pending offerings

- Review Fundamentals: Analyze prospectus use of proceeds and financial statements

- Assess Tax Impact: Consult tax advisor for optimal exercise timing

- Execute Decision: Exercise, sell, or expire before deadline

Frequently Asked Questions About Rights Shares

1. What happens if I don’t exercise my rights?

Your ownership percentage decreases as other shareholders purchase new shares. You’ll experience dilution—your 1% stake might become 0.85%, reducing voting power and future dividends proportionally.

2. Can I sell my rights if I don’t want to buy shares?

Yes, if they’re renounceable rights. They trade on exchanges like regular stocks under temporary tickers. Non-renounceable rights cannot transfer and must be exercised or forfeited.

3. How long do I have to exercise rights shares?

Typically 14-30 days in US markets. The exact subscription period appears in the prospectus and rights certificate. Missing the deadline results in automatic expiration.

4. Do rights shares pay dividends immediately?

No. Shares purchased via rights receive dividends only after the record date for the next declared dividend—usually 1-3 months post-issue.

5. What is the difference between rights issue and bonus issue?

Rights issues require payment (subscription price) to acquire shares and raise capital. Bonus issues distribute free shares to existing holders without raising new capital.

6. Can rights shares be negative?

Technically no, but rights can become worthless if the market price falls below the subscription price plus transaction costs, eliminating any economic incentive to exercise.

7. How do I calculate my rights entitlement?

Divide your current shares by the rights ratio denominator. For 1:5 rights on 600 shares: 600 ÷ 5 = 120 rights entitlements.

8. Are rights offerings good or bad for shareholders?

Neutral to positive if priced fairly. Dilution is offset by capital raised for growth. Poor pricing or wasteful capital use harms shareholders—making analysis critical.

9. What is a nil-paid rights issue?

Rights trading before the subscription price is paid. The “nil-paid” right represents the option value separate from underlying share ownership.

10. How do standby rights issues work?

Investment banks underwrite the offering, guaranteeing to purchase any unsubscribed shares. This ensures companies raise target capital but costs 3-5% in underwriting fees.

11. Where can I trade my rights entitlements?

Rights trade on the same exchanges as underlying shares (NYSE, NASDAQ, LSE) under temporary tickers during the subscription period, typically 5-20 trading days.

Disclaimer

This article is for educational purposes only and does not constitute financial advice. Rights share investing involves substantial risk including total loss of capital. Consult a qualified financial advisor and review all prospectus materials before making investment decisions. Tax implications vary by jurisdiction—consult a tax professional for personalized guidance.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.