Home Equity: 4 Ways to Use It + 2026 Rate Cuts

Home equity rates dropped to 7.92%—the lowest in 3 years. With Fed rate cuts coming in 2026, homeowners can leverage $200K+ equity for renovations, debt consolidation, or investments.

In This Article

Home equity is the difference between your home’s current market value and what you owe on your mortgage—and with rates expected to drop throughout 2026, now’s the time to understand how to leverage this powerful financial tool. With the average U.S. homeowner sitting on over $200,000 in equity and the Federal Reserve signaling three potential rate cuts this year, understanding your options could save you thousands.

What Is Home Equity and Why It Matters in 2026

Home equity represents the portion of your property you actually own. If your home is worth $400,000 and you owe $250,000 on your mortgage, you have $150,000 in home equity—that’s 37.5% ownership.

Here’s the simple calculation:

Home Equity = Current Home Value – Outstanding Mortgage Balance

This equity isn’t just a number on paper. It’s accessible capital you can use for major financial goals, and 2026’s rate environment makes it more affordable than it’s been in years.

2026 Market Context You Need to Know

The National Association of REALTORS® predicts home values will increase 4% in 2026, automatically building your equity without any action on your part. Meanwhile, mortgage rates are forecast to drop to 6%, creating a rare opportunity window.

According to Bankrate’s senior industry analyst Ted Rossman, home equity loan rates are averaging 7.92% as of January 2026—the lowest since 2023. Home equity lines of credit (HELOCs) sit even lower at 7.44%.

| Scenario | Home Value | Mortgage Balance | Your Equity | Equity % |

|---|---|---|---|---|

| New Homeowner | $350,000 | $315,000 | $35,000 | 10% |

| Mid-Journey | $450,000 | $270,000 | $180,000 | 40% |

| Nearly Paid Off | $500,000 | $100,000 | $400,000 | 80% |

Key takeaway: Most lenders require you to maintain at least 15-20% equity in your home, meaning you can typically access up to 80-85% of your home’s value through borrowing.

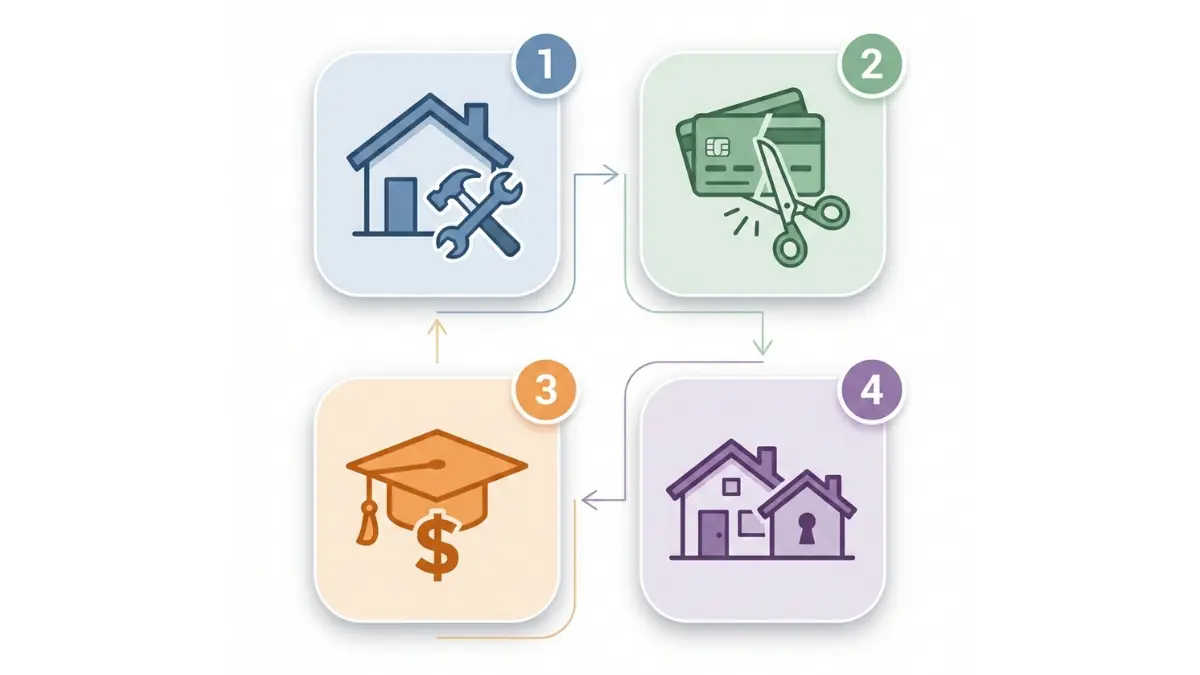

4 Smart Ways to Use Your Home Equity in 2026

1. Home Renovations That Add Value

Using home equity for strategic renovations is one of the most financially sound decisions you can make—especially when those improvements increase your property value.

According to Zonda’s 2025 Cost vs. Value Report, certain renovations deliver exceptional returns:

- Garage door replacement: 268% ROI

- Minor kitchen remodel: 113% ROI

- Wood deck addition: 95% ROI

Let’s break down a real-world example. Say you borrow $50,000 through a home equity loan at current 7.92% rates for a kitchen renovation. Over a 10-year term, your monthly payment would be approximately $603. But if that renovation increases your home’s value by $56,500 (113% ROI), you’ve netted $6,500 in equity while enjoying an updated kitchen.

Important tax benefit: Under current IRS rules, interest paid on home equity loans used for substantial home improvements may be tax-deductible, up to debt limits of $750,000. Always consult a tax professional to verify eligibility.

Before starting renovations, use our Home Affordability Calculator to ensure the project fits your overall financial picture.

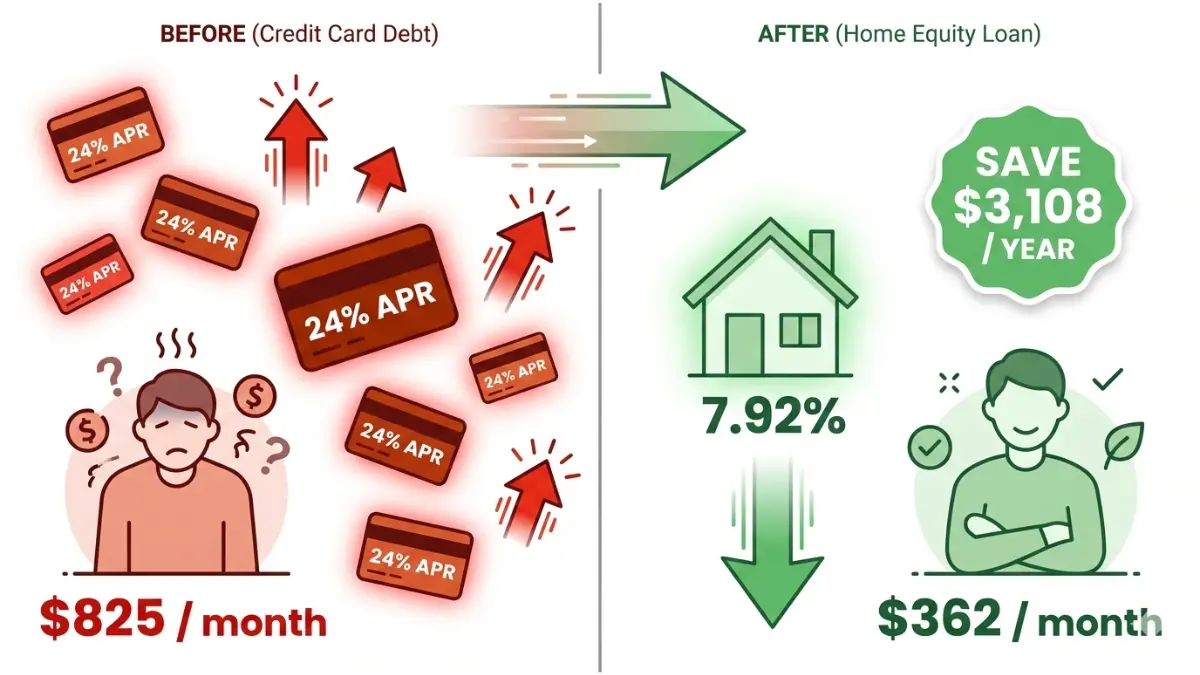

2. High-Interest Debt Consolidation

This strategy can save you hundreds of dollars monthly by replacing expensive debt with cheaper home equity financing.

The math is compelling:

Credit card debt currently averages 24.84% APR. Personal loans sit around 12%. Meanwhile, home equity loans average under 8%. If you’re carrying $30,000 in credit card debt at 24.84%, you’re paying approximately $621 monthly in interest alone.

Consolidate that into a home equity loan at 7.92% for 10 years, and your total monthly payment drops to approximately $362 (principal + interest)—a savings of $259 per month, or $3,108 annually.

| Debt Type | Balance | APR | Monthly Payment | Total Interest (10 yrs) |

|---|---|---|---|---|

| Credit Cards | $30,000 | 24.84% | $825+ | $69,000+ |

| Personal Loan | $30,000 | 12.00% | $430 | $21,600 |

| Home Equity Loan | $30,000 | 7.92% | $362 | $13,440 |

Use our Debt Consolidation Calculator to see your exact savings potential.

Critical warning: You’re converting unsecured debt into secured debt. If you default, you could lose your home. Only consolidate if you’re committed to not accumulating new credit card balances. For comprehensive debt elimination strategies, read our guide on how to pay off debt fast.

3. Education Funding Without Student Loans

Home equity can bridge education funding gaps when federal student aid falls short, typically offering lower rates than private student loans (currently 8-14% for undergraduates).

A $40,000 home equity loan at 7.92% over 10 years costs $483 monthly. Compare that to a private student loan at 10% APR: $528 monthly. You’d save $5,400 over the loan term.

Strategic approach: Maximize federal student aid first (currently 5.50% for undergraduate Direct Loans), then use home equity for remaining costs. Federal loans offer income-driven repayment and forgiveness options that home equity loans don’t provide.

Before borrowing for education, understand all your funding options by visiting the Federal Student Aid website for comprehensive federal loan information.

4. Investment Property Down Payment

Real estate investors frequently tap home equity to fund down payments on rental properties, creating a wealth-building loop.

Here’s how it works: You need $50,000 for a 20% down payment on a $250,000 rental property. You borrow it via HELOC at 7.44% variable rate. Your interest-only payment during the draw period is approximately $310 monthly.

Meanwhile, if the rental property generates $2,200 monthly rent with a $1,600 mortgage payment, you net $600 monthly (before other expenses). That $600 covers the HELOC payment and provides cash flow.

Tax consideration: Rental property mortgage interest is generally fully deductible as a business expense. Consult IRS Publication 527 – Residential Rental Property for detailed tax guidance.

Many investors use this strategy repeatedly, building portfolios by leveraging equity in one property to purchase the next. Learn more about strategic home buying in our Buy First Home 2026 Guide.

How to Access Home Equity: 5 Options Compared

Home Equity Loan (Fixed-Rate Second Mortgage)

A home equity loan provides a lump sum at a fixed interest rate, repaid over 5-30 years with predictable monthly payments.

Current rates: 7.92% for 5-year terms, 8.10% for 10-year terms, 8.09% for 15-year terms (Bankrate, January 2026).

Best for: Large one-time expenses like major renovations, debt consolidation, or property purchases where you know the exact amount needed.

Pros:

- Fixed rate protects against future rate increases

- Predictable monthly payments aid budgeting

- Lower rates than most unsecured debt

Cons:

- Fixed rate won’t benefit from future rate drops

- Closing costs typically 2-5% of loan amount

- Your home serves as collateral

HELOC (Variable-Rate Line of Credit)

A HELOC works like a credit card secured by your home, offering a revolving credit line you can draw from during a 5-10 year period, then repay over 10-20 years.

Current rates: 7.44% variable (Bankrate, January 2026).

Best for: Ongoing expenses with uncertain costs, like extended renovations, college tuition paid over multiple years, or keeping emergency funds accessible.

The Consumer Financial Protection Bureau’s HELOC guide explains the draw period and repayment mechanics in detail.

Pros:

- Borrow only what you need, when you need it

- Interest charged only on amount borrowed

- Variable rates drop automatically when Fed cuts rates

Cons:

- Variable rates can increase if Fed reverses course

- Payment fluctuations complicate budgeting

- Risk of overspending with easy access

Calculate your potential HELOC payments using our Mortgage Refinance Calculator.

Cash-Out Refinance

This replaces your existing mortgage with a larger loan, providing the difference in cash. You’ll have just one mortgage payment.

Current rates: 6.5-7% for qualified borrowers (January 2026).

Best for: Homeowners whose current mortgage rate exceeds today’s rates, or those needing large sums who want to consolidate into a single payment.

2026 consideration: Many homeowners locked in 3-4% rates in 2020-2021. Refinancing at 6.5% means significantly higher payments. Run the numbers carefully before proceeding.

Our Mortgage Calculator can help you compare your current payment to a potential cash-out refinance.

Pros:

- Single monthly payment simplifies finances

- May secure lower rate than current mortgage (if purchased in high-rate period)

- Potentially tax-deductible interest

Cons:

- Extends repayment timeline if refinancing into new 30-year term

- Closing costs similar to original mortgage (3-6%)

- Giving up a low existing rate costs money long-term

For detailed rate comparisons, check our Lowest Mortgage Rates by State analysis.

Equity Sharing Agreement (NEW 2026 Option)

Also called Home Equity Investments (HEIs), these agreements provide upfront cash without monthly payments. Instead, you share a percentage of your home’s future appreciation (or depreciation) with the provider.

How it works: You receive $50,000 now. In 10 years (or when you sell), you repay $50,000 plus 25% of any appreciation. If your home value increased from $400,000 to $500,000, you’d owe $50,000 + $25,000 (25% of the $100,000 gain) = $75,000.

Best for: Homeowners prioritizing cash-flow relief who can’t afford monthly payments but need immediate funds.

Important warning: The Consumer Financial Protection Bureau recently issued an advisory warning about home equity contracts, noting they often cost more than traditional financing and contain complex terms. Some contracts effectively charge 19.5-22% annually—far higher than home equity loans.

Pros:

- No monthly payments

- Flexible credit requirements (some accept 500+ scores)

- Access funds without taking on traditional debt

Cons:

- Extremely expensive long-term if home appreciates significantly

- Complex contracts with hidden costs

- May complicate future refinancing

- Could force home sale if you can’t pay settlement amount

Reverse Mortgage (Age 62+)

Available only to homeowners 62 and older, reverse mortgages allow you to convert equity into cash without monthly payments. The loan is repaid when you sell, move permanently, or pass away.

Best for: Retirees with substantial equity needing income supplementation who plan to stay in their home long-term.

For comprehensive information, visit the HUD Reverse Mortgage page to understand eligibility, requirements, and counseling.

Pros:

- No monthly payments required

- Stay in your home

- Funds typically not counted as taxable income

Cons:

- Reduces inheritance for heirs

- Ongoing costs (insurance, property taxes, maintenance)

- Loan balance grows over time with interest

Comprehensive Comparison Table

| Access Method | Current Rate | Best For | Monthly Payment | Risk Level | Typical Term |

|---|---|---|---|---|---|

| Home Equity Loan | 7.92% | Large one-time expenses | Fixed | Medium | 5-30 years |

| HELOC | 7.44% variable | Ongoing/uncertain needs | Variable | Medium-High | 10-year draw + 10-20 year repay |

| Cash-Out Refinance | 6.5-7% | Lowering existing rate | Fixed | Medium | 15-30 years |

| Equity Sharing | Effective 19-22% | Cash-flow relief | None | Very High | 10-30 years |

| Reverse Mortgage | N/A | Age 62+ income | None (deferred) | Medium | Until sale/death |

How 2026 Rate Cuts Impact Your Home Equity Strategy

Fed Rate Cut Predictions

The Federal Reserve is widely expected to implement three quarter-point rate cuts throughout 2026, according to economic forecasters and Bankrate’s analysis. This would reduce the Fed funds rate by 0.75 percentage points total.

Projected impact:

- Home equity loan rates: Expected to average 7.75% by year-end

- HELOC rates: Expected to average 7.3% by year-end

Ted Rossman, Bankrate’s senior industry analyst, states: “We could see lower home equity rates than we’ve seen for most of the past few years, but nowhere near as low as you could have gotten in 2021 or 2022.”

Should You Wait or Act Now?

This is the critical question facing homeowners in early 2026. Here’s a decision framework:

Act Now If:

- You need funds immediately for time-sensitive opportunities

- You’re consolidating high-interest debt (credit cards 20%+)

- You’re choosing a HELOC (rates drop automatically)

- Current rates already save you money vs. alternatives

Wait for Lower Rates If:

- Your project timeline is 6+ months out

- You’re considering a fixed-rate loan and rates may drop further

- You’re financially stable and not paying high-interest debt

- You’re not in urgent need of funds

Use caution if:

- You have a sub-4% existing mortgage rate (cash-out refinance likely not worth it)

- You’re uncertain about repayment ability

- Your local housing market shows weakness

How Variable vs. Fixed Rates Respond to Fed Cuts

HELOCs benefit automatically: Variable rates are tied to the prime rate, which moves with the Fed funds rate. When the Fed cuts by 0.25%, your HELOC rate typically drops by 0.25% within 30-45 days.

Real savings example: A $50,000 HELOC at 10.16% (the 2024 peak) cost $423 monthly in interest. At today’s 7.44% rate, that drops to $310 monthly—saving $113 monthly or $1,356 annually. If rates hit the projected 7.3%, savings increase to $1,430 annually.

Fixed-rate loans require action: Home equity loans with fixed rates don’t automatically benefit from Fed cuts. You’d need to refinance—paying closing costs again—to capture lower rates. Before taking a fixed loan in early 2026, compare the cost of potential refinancing versus starting with a HELOC.

For strategic comparison of fixed versus variable rate products, our 15 vs 30 Year Mortgage Comparison offers parallel insights on rate strategy.

Home Equity Risks Every Homeowner Should Know

Foreclosure Risk (Your Home as Collateral)

This is non-negotiable: When you borrow against home equity, your property serves as collateral. Missing payments can trigger foreclosure proceedings, resulting in loss of your home.

Protection strategies:

- Build a 6-month emergency fund before borrowing (see our Emergency Fund Guide)

- Borrow conservatively—don’t max out available equity

- Set up automatic payments to avoid missed deadlines

- Maintain adequate homeowners insurance

- Keep emergency reserves separate from borrowed funds

Overborrowing Dangers

The 2026 market presents a specific risk: If you tap all available equity and home values decline, you could end up underwater—owing more than your home is worth.

Conservative borrowing guidelines:

- Maintain at least 20% equity cushion after borrowing

- Account for potential 10-15% market corrections

- Never borrow the maximum available

Market volatility warning: While the National Association of REALTORS® predicts 4% appreciation in 2026, local markets vary significantly. Some regions may experience declines, especially if economic conditions weaken or if specific local industries struggle.

What NOT to Use Home Equity For

Your home equity should fund value-adding or financially strategic purposes only—never depreciating assets or discretionary spending.

❌ Never use home equity for:

- Vacations or luxury travel

- Vehicles (cars, boats, RVs—all depreciate rapidly)

- Day-to-day living expenses or routine bills

- Speculative investments or cryptocurrency

- Consumable goods or entertainment

- Bailing out others financially

✅ Only use home equity for:

- Value-adding home improvements

- High-return education expenses

- Income-producing investments (rental property)

- Eliminating high-interest debt (when committed to financial discipline)

- Unavoidable emergency expenses (medical, critical repairs)

Tax Deductibility Rules (2026 Update)

Not all home equity interest is tax-deductible. Under current tax law:

Deductible scenarios:

- Funds used for substantial home improvements on the property securing the loan

- Total mortgage debt (primary + home equity) under $750,000 ($375,000 if married filing separately)

- You itemize deductions (standard deduction is $14,600 single, $29,200 married filing jointly for 2026)

Non-deductible scenarios:

- Funds used for debt consolidation, education, or other non-home purposes

- Total mortgage debt exceeds $750,000

Consult IRS Topic No. 505 – Interest Expense for complete tax guidance, and always work with a qualified tax professional to determine your specific deductibility.

Understanding the tax implications is crucial for maximizing your financial strategy, similar to understanding APR calculations when comparing loan products.

Ready to Use Your Home Equity? Your Next Steps

Follow this action plan to leverage your equity strategically:

- Calculate your current equity: Use our Mortgage Calculator to determine your exact mortgage balance, then subtract from your home’s current market value (get a recent appraisal or use tools like Zillow/Redfin for estimates).

- Define your specific need: Clarify exactly how much you need and for what purpose. This determines which access method makes sense.

- Compare access methods: Use the comparison table in this article to match your need with the appropriate product type.

- Get quotes from 3+ lenders: Rates and terms vary significantly. Credit unions often offer competitive rates. Compare closing costs carefully—they range from 2-6% of the loan amount.

- Review all fees and costs: Beyond interest rates, examine origination fees, annual fees, early closure penalties, appraisal costs, and prepayment penalties.

- Consult a tax advisor: Determine whether your intended use qualifies for interest deductibility to understand your true borrowing cost.

- Set up automatic payments: Once approved, automate payments to protect your home and credit score.

Additional resources: For homeowners pursuing homeownership for the first time or refinancing, our Mortgage Pre-Approval 2026 Guide provides comprehensive preparation strategies.

Frequently Asked Questions About Home Equity

1. How much home equity can I borrow?

Most lenders allow up to 80-85% combined loan-to-value ratio, meaning you keep 15-20% equity cushion. On a $400,000 home with $200,000 owed, you’d maintain $60,000-$80,000 equity and could borrow $120,000-$140,000.

2. Is home equity interest tax deductible in 2026?

Yes, if used for substantial home improvements and total mortgage debt stays under $750,000. Consult IRS Topic 505 and a tax professional for your specific situation.

3. What’s the difference between a home equity loan and HELOC?

Loans provide a lump sum with fixed rates and payments. HELOCs offer revolving credit with variable rates during a 5-10 year draw period, then convert to repayment.

4. How long does approval take?

Typically 2-6 weeks depending on lender efficiency, appraisal scheduling, and documentation completeness. Some lenders offer expedited processing for additional fees.

5. Can I qualify with bad credit?

Possible but challenging. Most lenders require 620+ credit scores. Equity sharing agreements may accept 500+. Low scores mean higher rates and stricter terms. Focus on building your credit score first for better options.

6. What if my home value drops after borrowing?

You could owe more than your home’s worth (underwater). This doesn’t trigger immediate payment but complicates refinancing and creates loss if selling. Maintain equity cushions to protect against this risk.

7. Are closing costs required?

Yes, typically 2-5% of loan amount, covering appraisal ($400-$600), origination fees (0.5-1%), title search ($200-$400), and recording fees ($50-$200). Some lenders offer no-closing-cost options with slightly higher rates.

8. Can I pay off early without penalty?

Usually yes, but verify before signing. Some lenders charge prepayment penalties of 2-5% if paid within first 3-5 years.

9. How does borrowing affect my credit score?

Initially, new debt and credit inquiry may lower score 5-10 points temporarily. Consistent on-time payments improve score long-term. High utilization (using most of credit line) can hurt scores.

10. What’s the minimum equity needed?

Generally 15-20% required. Some lenders offer 90% LTV programs requiring only 10% equity for borrowers with excellent credit (740+) and strong income.

11. Should I choose fixed or variable rate in 2026?

Fixed for payment certainty and protection if rates rise. Variable (HELOC) to automatically benefit from expected Fed rate cuts throughout 2026—potentially saving thousands in interest.

Disclaimer

This article provides educational information about home equity and related financial products. It is not financial, legal, tax, or investment advice tailored to your individual circumstances. Home equity products involve using your home as collateral, which carries foreclosure risk if payments aren’t made as agreed. Interest rates, loan terms, closing costs, and tax deductibility vary significantly by lender, individual financial situation, property location, and current tax law.

Always consult qualified financial advisors, certified public accountants, tax professionals, and licensed mortgage specialists before making borrowing decisions. Rate data and market projections current as of January 2026 and subject to change based on Federal Reserve policy, economic conditions, and market dynamics. Verify all current rates, terms, and tax implications with appropriate professionals before proceeding.

For comprehensive financial planning beyond home equity, explore our guides on retirement planning, debt management, and investment strategies to build a complete wealth-building framework.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.