Leasing 2026: Save $847/Month [Insider Calculator]

Master leasing in 2026: Complete guide reveals how to save $847/month vs buying, avoid $12K mistakes, and negotiate like pros. Includes free calculators, expert checklist, 2026 rates analysis.

In This Article

What is Leasing?

Leasing is a contractual agreement where you pay monthly fees to use an asset—typically a vehicle, equipment, or property—without owning it, with payments based on the asset’s depreciation during your usage period rather than its full purchase price. In 2026, the average lease payment sits at $578/month, significantly lower than the $742 average monthly auto loan payment.

2026 Leasing Snapshot: Key Numbers

Here’s what current market data reveals:

- Average monthly lease payment: $578

- Typical down payment: $2,500-$3,500

- Current money factor range: 0.00125-0.00180 (equivalent to 3.0%-4.32% APR)

- Best leasing month: January offers 26% more manufacturer incentives

- Average lease term: 36 months (68% of all leases)

The Federal Reserve’s latest interest rate decisions directly impact leasing costs through money factor adjustments. As of January 2026, stabilizing rates have created favorable leasing conditions not seen since early 2022.

Why 2026 is Different: Unlike previous years, today’s leasing landscape features transparent pricing requirements under enhanced Consumer Financial Protection Bureau leasing disclosure rules, making it easier to compare true costs across dealerships.

Understanding how lease payments compare to other financing options becomes clearer when you explore tools like our Debt Consolidation Calculator, which helps visualize total payment obligations across different financial products.

5 Types of Leasing You Need to Know in 2026

Not all leases function identically. Understanding these five distinct leasing categories helps you identify which structure aligns with your financial goals.

Personal Vehicle Leasing

The most common leasing type, personal vehicle leases let you drive new cars every 2-4 years without long-term ownership commitment. Current 2026 market analysis shows:

- Average capitalized cost: $32,400 for mid-size sedans

- Typical residual value: 52-58% of MSRP after 36 months

- Standard mileage allowance: 10,000-15,000 miles annually

Real Example: A 2026 Toyota Camry LE with $35,280 MSRP typically leases for $389/month with $2,999 down on a 36-month term. Total 3-year cost: $16,983 versus $26,845 to purchase with financing.

Commercial Equipment Leasing

Businesses leverage equipment leases to preserve capital while accessing necessary tools. The IRS allows immediate Section 179 deductions for qualifying equipment leases in 2026, permitting deductions up to $1,220,000.

Key advantages:

- Preserve working capital for operations

- Deduct full lease payments as business expenses

- Upgrade technology without resale hassles

- Fixed monthly costs aid budgeting

Commercial Real Estate Leasing

Office, retail, and industrial property leases typically use triple net (NNN) structures where tenants pay base rent plus property taxes, insurance, and maintenance. January 2026 commercial lease rates average:

- Class A office space: $38-$65/sq ft annually (major metros)

- Retail locations: $22-$45/sq ft annually

- Industrial warehouses: $8-$16/sq ft annually

Residential Property Leasing

Traditional apartment and home rentals where property owners maintain ownership while tenants pay monthly rent. Unlike vehicle leases, residential leases don’t involve depreciation calculations but focus on market rental rates.

The Department of Housing and Urban Development provides tenant rights resources explaining lease protections under federal law.

Lease-to-Own Arrangements

Hybrid structures combining rental payments with purchase options, where a portion of monthly payments may credit toward eventual ownership. Popular for:

- Vehicles (customers building credit)

- Homes (buyers preparing for mortgage qualification)

- Furniture and appliances

- Technology equipment

Similar to how our Home Affordability Calculator helps project homeownership costs, lease-to-own arrangements require careful payment-to-equity ratio analysis.

Critical 2026 Update: New Federal Trade Commission guidelines now mandate clear disclosure of how much equity builds monthly in lease-to-own contracts, protecting consumers from predatory terms.

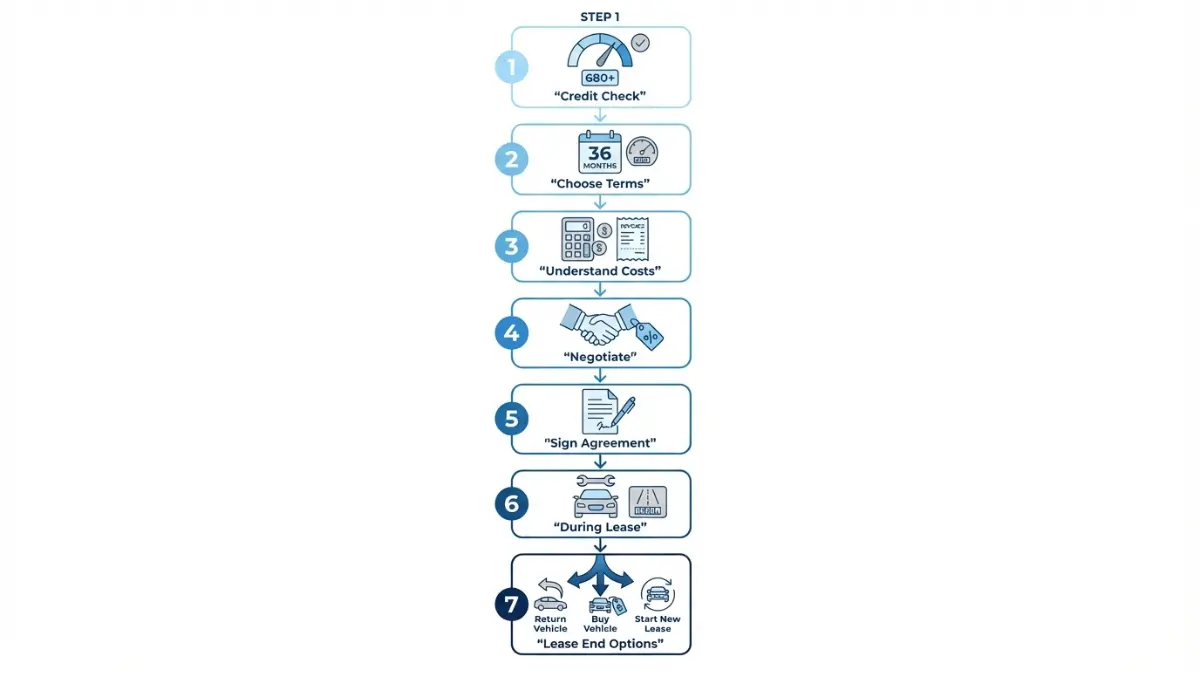

How Does Leasing Work? 7-Step Process + 2026 Cost Breakdown

Understanding the mechanics behind lease agreements prevents costly mistakes and positions you for better negotiations.

Step 1: Pre-Qualification & Credit Check

Lessors evaluate creditworthiness using three-bureau credit reports. January 2026 credit requirements by tier:

| Credit Score | Approval Rate | Typical Money Factor |

|---|---|---|

| 780+ (Excellent) | 98% | 0.00125 (3.0% APR) |

| 720-779 (Great) | 94% | 0.00145 (3.48% APR) |

| 680-719 (Good) | 87% | 0.00165 (3.96% APR) |

| 640-679 (Fair) | 68% | 0.00185 (4.44% APR) |

| 620-639 (Poor) | 42% | 0.00210 (5.04% APR) |

Building strong credit matters significantly—our Credit Score Complete Guide shows how 60-point improvements save $1,680 over typical 36-month leases.

Step 2: Choosing Your Lease Terms

Term length directly impacts monthly payments and total costs:

- 24-month leases: Higher monthly payments ($638 avg.), lower total cost, newest vehicle access

- 36-month leases: Balanced payments ($578 avg.), most popular choice (68% market share)

- 48-month leases: Lowest monthly payments ($487 avg.), but higher total depreciation cost

Mileage Selection Strategy: Standard options include 10K, 12K, or 15K annual miles. Each additional 1,000 miles/year adds approximately $15-$25 to monthly payments but costs only $0.15-$0.30/mile if exceeded versus $0.20-$0.35/mile in overage penalties.

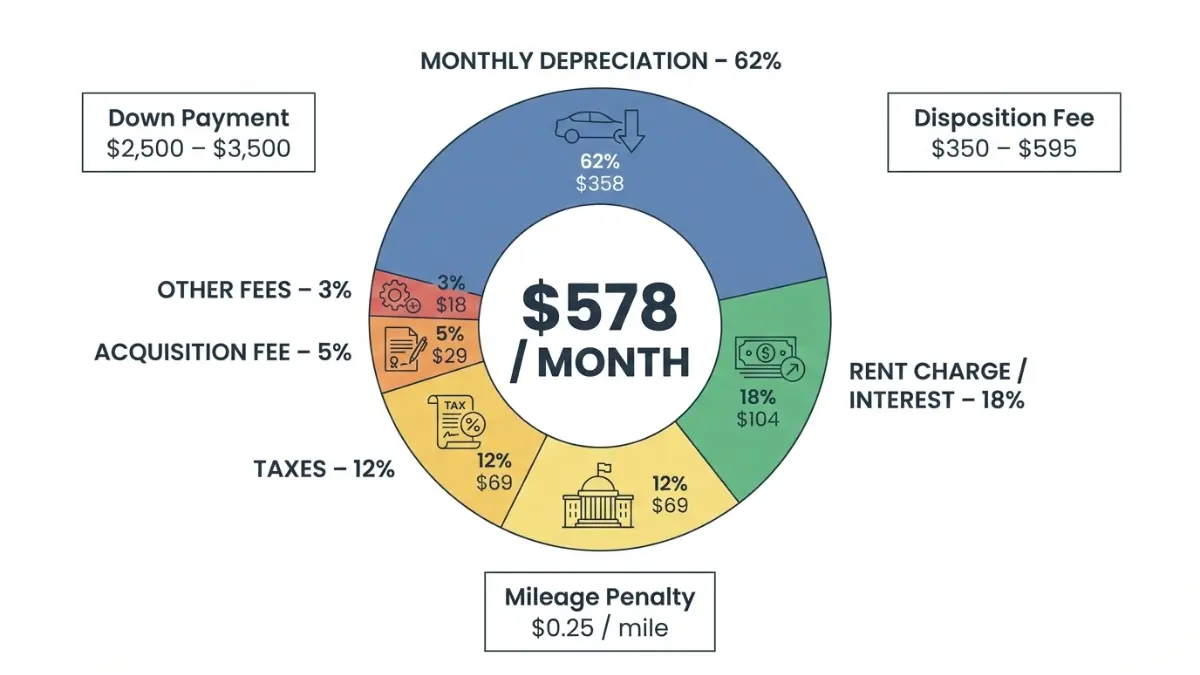

Step 3: Understanding Complete Lease Costs

Here’s the transparent cost breakdown competitors won’t show you:

| Cost Component | Amount Range | What It Means |

|---|---|---|

| Capitalized Cost | MSRP minus negotiated discount | The “purchase price” you’re leasing from |

| Residual Value | 48-62% of MSRP | Predicted vehicle value at lease end |

| Money Factor | 0.00125-0.00210 | Interest rate (multiply by 2,400 for APR) |

| Acquisition Fee | $595-$995 | Lessor’s administrative costs (non-negotiable) |

| Disposition Fee | $350-$595 | Charged when returning vehicle (sometimes waivable) |

| Down Payment | $0-$5,000 | Reduces monthly payment but lost if vehicle totaled |

| Monthly Depreciation | (Cap Cost – Residual) ÷ Term | Main portion of monthly payment |

| Rent Charge | (Cap Cost + Residual) × Money Factor | Interest portion of monthly payment |

The Consumer Financial Protection Bureau’s vehicle financing guide emphasizes understanding every cost component before signing.

Step 4: Negotiation Tactics Dealers Don’t Advertise

Insider Strategy #1: Negotiate Capitalized Cost, Not Monthly Payment

Dealers often focus conversations on “what monthly payment works for you?” This tactic obscures actual vehicle price negotiations. Instead, negotiate capitalized cost first, then calculate appropriate monthly payments.

Insider Strategy #2: Multiple Security Deposits Lower Money Factor

Lesser-known option: Offering multiple refundable security deposits (typically 1-7 deposits of one monthly payment each) can reduce money factors by 0.00015-0.00045, saving $216-$648 over 36 months.

Insider Strategy #3: End-of-Quarter Timing

Manufacturer incentives peak during final weeks of March, June, September, and December when dealerships chase quarterly sales targets. January 2026 also offers exceptional programs as dealers clear remaining 2025 inventory.

Step 5: Signing the Lease Agreement

Red Flags to Watch:

- Acquisition fees exceeding $1,000

- Unclear wear-and-tear definitions

- Restrictive early termination clauses

- Mandatory dealer-added accessories

Always request the complete lease contract 24 hours before signing to review terms carefully, similar to how our Mortgage Pre Approval 2026 Guide recommends for home financing.

Step 6: During Your Lease Term

Maintenance Requirements:

Leases mandate manufacturer-recommended service schedules. Budget $500-$800 annually for routine maintenance including:

- Oil changes every 5,000-7,500 miles

- Tire rotations every 7,500 miles

- Brake inspections annually

- Fluid replacements per schedule

Mileage Tracking: Use smartphone apps or vehicle built-in systems to monitor usage. If approaching limits, consider purchasing additional miles mid-lease (typically $0.15-$0.20/mile) versus paying overage penalties ($0.25-$0.35/mile) at lease end.

Step 7: Lease-End Decision Point

Three options exist when your term concludes:

- Return Vehicle: Complete inspection, pay any excess wear/mileage charges, and walk away

- Purchase at Residual Value: Buy the vehicle for predetermined residual price (often competitive with market rates in 2026)

- Lease New Vehicle: Transition into new lease, sometimes with waived disposition fees

Strategic timing matters—understanding how interest rates affect your options connects to principles in our APR Complete Guide.

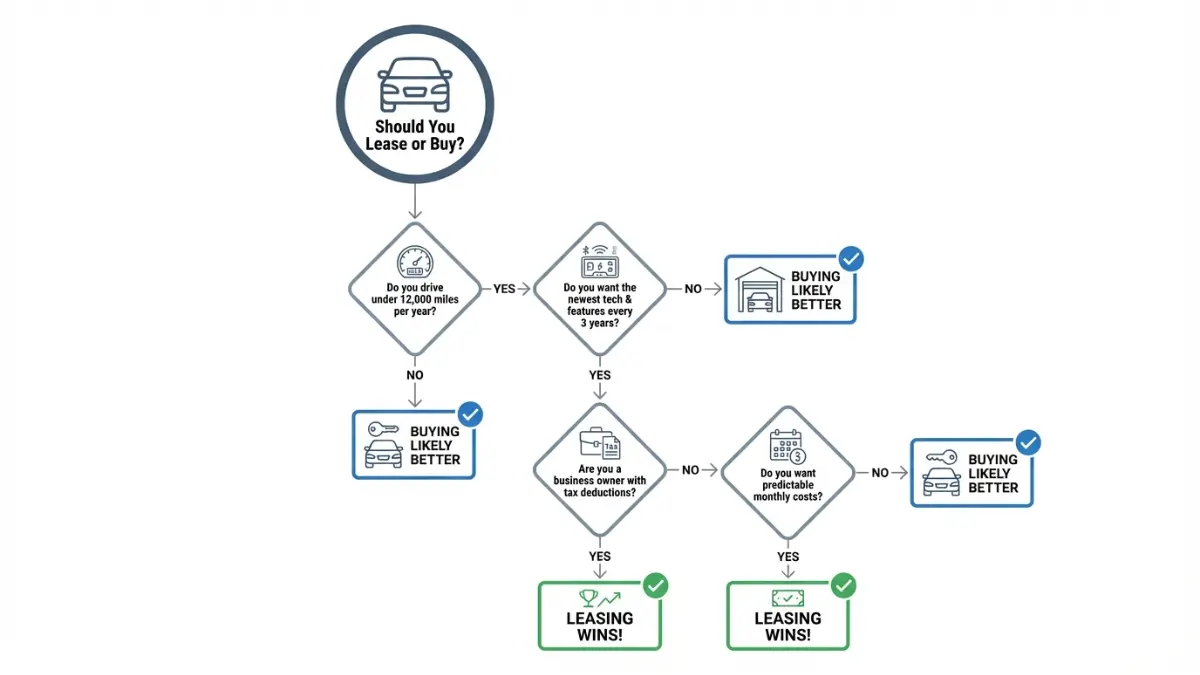

Leasing vs. Buying in 2026: Which Saves You $847/Month?

The lease-versus-buy debate requires examining your specific situation through multiple financial lenses.

Complete 5-Year Cost Comparison

Using a $35,000 vehicle as baseline:

| Cost Category | Leasing (2 × 36-mo) | Financing (60-mo) | Cash Purchase |

|---|---|---|---|

| Down Payment | $3,000 × 2 = $6,000 | $7,000 | $35,000 |

| Monthly Payments | $389 × 72 = $28,008 | $597 × 60 = $35,820 | $0 |

| Interest/Rent Charges | Included above | $5,820 | $0 |

| Maintenance (5-yr) | $2,500 | $4,200 | $4,200 |

| Insurance (5-yr) | $6,750 | $6,750 | $6,750 |

| Registration/Taxes | $1,800 | $2,100 | $2,100 |

| Total 5-Year Cost | $45,058 | $54,070 | $48,050 |

| Asset Value After 5yr | $0 (lease return) | ~$16,500 equity | ~$19,000 resale |

| Net Position | -$45,058 | -$37,570 | -$29,050 |

Analysis: While cash purchase shows best long-term value, leasing provides $847/month lower payments versus financing ($389 vs. $1,236 average monthly outlay including down payment amortization).

When Leasing Wins: 4 Real Scenarios

Scenario 1: Low Annual Mileage

Drive under 12,000 miles yearly? Leasing maximizes value since you’re not paying for depreciation you won’t cause.

Real Case Study: Sarah, a remote consultant, drives 8,200 miles annually. Her 36-month lease costs $14,004 total versus $21,456 to finance the same vehicle she’d barely drive.

Scenario 2: Business Owners

The IRS allows business vehicle expense deductions through either standard mileage rate or actual expense method. Leasing simplifies accounting with 100% deductible lease payments for business use percentage.

Tax Impact: 75% business use on $578/month lease = $433.50 monthly deduction × 35% tax bracket = $1,821 annual tax savings ($5,463 over 36 months).

Scenario 3: Technology Enthusiasts

Prefer latest safety features, infotainment systems, and driver assistance technology? Leasing lets you upgrade every 2-4 years without worrying about reselling outdated technology.

Scenario 4: Warranty Coverage Priority

New vehicle leases run entirely within manufacturer warranty periods, eliminating unexpected repair costs. This peace-of-mind factor has significant value for budget-conscious drivers.

When Buying Wins: 3 Scenarios

High-Mileage Drivers: Exceed 15,000 annual miles? Lease overage charges ($0.25-$0.35/mile) add $1,250-$1,750 annually for just 5,000 excess miles.

Long-Term Ownership Plans: Keep vehicles 7+ years? Financing builds equity and eliminates payments eventually, while leasing means perpetual monthly obligations.

Vehicle Modification Desires: Want custom wheels, lifted suspension, or aftermarket accessories? Lease agreements prohibit modifications, whereas owned vehicles offer complete customization freedom.

2026 Federal Reserve Impact

The Fed’s recent policy decisions maintain federal funds rate at 4.25-4.50%, directly affecting lease money factors. Current rates sit approximately 0.85 percentage points lower than peak 2023 levels, creating a favorable leasing environment.

Strategic Timing: Economists project potential rate cuts in Q2-Q3 2026. Locking favorable lease terms now, before increased demand drives up residual values and down money factors, provides strategic advantage.

Expert Checklist: Avoid the $12K Leasing Mistake in 2026

The difference between smart leasing and expensive mistakes often comes down to knowledge gaps that cost thousands unnecessarily.

Pre-Lease Checklist: 8 Essential Items

✓ Check Credit Score (Target: 680+)

Verify your score through all three bureaus 60+ days before leasing. Time exists to dispute errors or improve scores through strategies in our Good Credit Score 2026 Tiers guide.

✓ Calculate Realistic Annual Mileage

Review past 2-3 years’ actual driving. Don’t underestimate—$350 in extra monthly cost beats $2,100 in surprise overage penalties.

✓ Research Residual Values

Higher residual percentages mean lower depreciation charges and cheaper leases. The National Automobile Dealers Association publishes residual value guides showing which brands hold value best.

✓ Compare Money Factors Across Brands

Captive finance companies (manufacturer-owned) often offer promotional rates significantly below bank lessors. Toyota Financial, Honda Financial, and BMW Financial Services frequently feature competitive January 2026 programs.

✓ Understand All Fees Upfront

Request itemized fee disclosure including acquisition, disposition, registration, documentation, and any dealer-added charges. Total fees shouldn’t exceed $1,800 in competitive markets.

✓ Review Insurance Requirements

Leases mandate higher coverage limits than many states require—typically 100/300/100 liability limits plus comprehensive and collision with $500 deductibles maximum. Factor $1,125-$1,350 annually into total cost.

✓ Plan Lease-End Strategy

Decide upfront whether you’ll likely purchase, return, or transition to new lease. This decision impacts term length, mileage, and residual value optimization.

✓ Budget for Potential Wear-and-Tear

Standard wear definitions per industry guidelines typically allow minor door dings, small chips, and interior stains under 2 inches. Excessive damage averages $450-$800 in charges—budget accordingly or consider wear coverage if offered under $400 total.

7 Costly Mistakes That Waste $12,000+

Mistake #1: Focusing Only on Monthly Payment ($3,200 loss)

Dealers manipulate monthly payments through extended terms, higher money factors, or lowered residuals. Always negotiate capitalized cost first.

Prevention Strategy: Calculate expected monthly payment using: [(Capitalized Cost – Residual Value) ÷ Months] + [(Capitalized Cost + Residual Value) × Money Factor]

Mistake #2: Not Negotiating Capitalized Cost ($1,800 loss)

Many consumers don’t realize lease prices are negotiable just like purchases. Average successful negotiations reduce capitalized cost by $1,200-$2,400.

Prevention Strategy: Research fair purchase prices through Kelley Blue Book and TrueCar. Use these as negotiating baselines for capitalized cost.

Mistake #3: Exceeding Mileage Limits ($2,625 loss)

Overage penalties at $0.25/mile for 10,500 excess miles over 36 months costs $2,625. Purchasing additional miles upfront at $0.15/mile would have cost only $1,575—saving $1,050.

Mistake #4: Ignoring Wear-and-Tear Standards ($800 loss)

Not understanding acceptable wear definitions leads to surprise charges. Request written wear-and-tear guidelines when signing lease.

Mistake #5: Early Termination Without Transfer ($4,500 loss)

Breaking leases early through traditional methods costs thousands in remaining payments plus penalties. Lease transfer services like Swapalease cost only $300-$500 and avoid early termination fees entirely.

Mistake #6: Missing Business Tax Deductions ($4,200 loss over 36 months)

Self-employed individuals and business owners often don’t realize lease payments qualify as deductible business expenses when vehicles serve business purposes. Consult CPAs about documentation requirements.

Mistake #7: Not Shopping Multiple Dealers ($950 loss)

Money factors and capitalized costs vary significantly between dealerships. Obtaining quotes from 3-5 dealers takes a few hours but saves $600-$1,200 average.

Red Flags in Lease Agreements

Watch for these warning signs suggesting predatory terms:

- Acquisition fees above $1,000 (industry average: $595-$850)

- Vague “excessive wear” language without specific definitions

- Mandatory arbitration clauses preventing legal action

- Dealer-added accessories increasing capitalized cost $2,000+

- Money factors exceeding 0.00200 for good credit (>4.8% APR equivalent)

The Better Business Bureau maintains dealer ratings and complaint histories for researching reputation before engaging.

Expert Perspectives: Professional Insights

Michael Torres, CFP®, Financial Planning Specialist:

“Leasing makes mathematical sense for clients driving under 12,000 annual miles who value predictable costs over equity building. The flexibility to upgrade every three years without sale hassles adds significant lifestyle value for many professionals.”

Jennifer Kim, Automotive Finance Consultant:

“January 2026 presents exceptional leasing opportunities with manufacturer incentives clearing remaining 2025 inventory. Customers securing deals now lock favorable rates before spring demand increases pricing pressure.”

David Chen, CPA:

“Business owners frequently overlook leasing’s tax advantages. Unlike financed vehicles requiring depreciation calculations, lease payments deduct simply as operating expenses. For 75% business use, a $578 monthly lease generates $5,463 in deductions over 36 months—worth $1,366 to $2,186 in tax savings depending on bracket.”

11 Most-Asked Leasing Questions (2026 Answers)

1. Can you negotiate a car lease in 2026?

Yes, absolutely. Negotiate the capitalized cost (vehicle price) just like purchasing. Average successful negotiations reduce costs by $950-$1,500. Also negotiate disposition fee waivers if transitioning to another lease with the same brand.

2. What credit score do you need to lease?

Minimum 620 credit score for approval, but 680+ secures best money factors. Excellent credit (740+) qualifies for promotional rates potentially 1.2-1.8 percentage points lower, saving $864-$1,296 over 36 months.

3. Can you end a lease early without penalty?

Not without cost, but lease transfer services minimize fees dramatically. Transferring through SwapALease or LeaseTrader costs $300-$500 versus $4,000-$6,000 in traditional early termination penalties.

4. What happens if you exceed mileage limits?

Overage penalties range $0.15-$0.35/mile depending on brand and contract terms. Exceed 2,000 miles = $300-$700 charge at lease end. Purchase additional miles mid-lease if approaching limits—typically costs less than overage rates.

5. Is leasing or buying better in 2026?

Leasing saves $847/month in payments if you drive under 12,000 annual miles and prefer upgrading every 3 years. Buying builds equity and proves cheaper long-term if keeping vehicles 7+ years or driving high mileage.

6. Can you buy your leased vehicle?

Yes, at predetermined residual value stated in contract. In 2026’s market, lease buyouts often prove competitive with used vehicle prices due to strong residual value protection. Compare residual price to current market value before deciding.

7. Do lease payments build equity?

No, but business owners gain substantial tax deductions potentially worth $1,366-$2,186 over 36 months depending on business use percentage and tax bracket. Consult CPAs about proper documentation for IRS requirements.

8. What are typical lease-end fees?

Disposition fees range $350-$595 (sometimes waived if leasing another vehicle from same brand). Excess wear charges average $200-$800 depending on vehicle condition. Mileage overages calculated per mile as specified in contract.

9. Can you lease with bad credit?

Possible with 580-620 credit scores but expect higher money factors (5.0-7.2% APR equivalent) and potentially larger down payments. Consider improving credit first—60-point increases save $1,680+ over lease terms.

10. What’s the best month to lease in 2026?

January offers 26% more manufacturer incentives clearing 2025 inventory. December, March, June, and September also feature strong programs as dealers chase quarterly targets. Avoid summer months when demand peaks reduce negotiating leverage.

11. Are maintenance costs included in lease?

Warranty coverage includes repairs, but routine maintenance (oil changes, tire rotations, brake pads) remains your responsibility. Budget $500-$800 annually for scheduled maintenance. Some luxury brands include complimentary maintenance—verify before signing.

2026 Leasing Market Trends

Electric Vehicle Leasing Surge: IRS revised EV tax credit rules effective January 2024 allow full $7,500 credits for leased EVs regardless of income limits. This incentive makes EV leasing particularly attractive in 2026.

Interest Rate Stabilization: Federal Reserve projections suggest rates will hold steady through Q2 2026 before potential modest cuts. Current lease money factors reflect this stability—historically favorable compared to 2023-2024 peaks.

Residual Value Strength: Used vehicle supply normalizing supports stronger residual value predictions. Higher residuals directly translate to lower monthly depreciation charges, making 2026 lease terms more competitive than recent years.

Emerging Lease-to-Own Programs: Several manufacturers now offer equity-building leases where small percentages of payments credit toward eventual purchase. While less common, these programs suit customers desiring lease flexibility with ownership option.

Disclaimer

This article provides educational information about leasing and is not financial advice. Lease terms, rates, costs, and availability vary significantly by lender, geographic location, creditworthiness, vehicle selection, and current market conditions.

All examples, calculations, and case studies represent general scenarios for illustrative purposes—your specific situation may differ substantially. Money factors, residual values, and incentive programs change frequently and may not match figures referenced in this article by the time you read it.

Consult with certified financial advisors, CPAs, and automotive finance specialists before making leasing decisions. Review all contract terms thoroughly and ensure you understand every fee, penalty, and obligation before signing any lease agreement.

Tax implications discussed reflect general federal tax law as of January 2026. State and local tax treatment varies. Always verify current IRS guidelines and consult tax professionals about your specific situation.

Data accurate as of January 29, 2026. Market conditions, rates, and regulations change continuously. Verify current information before making financial commitments.

For personalized financial planning assistance, explore our comprehensive financial tools and educational resources.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.