Save $10,000 by December 2026: The Income-Adjusted 52-Week Plan That Actually Works at $40K, $60K, and $80K/Year

Most 52-week $10K plans assume you can save $192 every single week — but that’s impossible on a $40,000 salary. This income-adjusted version shows exactly what to save each week at $40K, $60K, and $80K+ income, plus a catch-up track for anyone starting after January.

In This Article

Can You Really Save $10,000 by December 2026?

Yes, you can save $10,000 by December 2026 using the 52-week savings challenge method. This proven approach requires saving just $192.31 per week or approximately $833 per month throughout the year. According to the Federal Reserve’s 2025 Survey of Household Economics, 68% of Americans who commit to structured savings plans successfully reach their annual goals.

The realistic savings plan works for individuals earning $40,000 or more annually, though higher earners can accelerate their progress. With current inflation rates at 3.2% as of January 2026 per Bureau of Labor Statistics data, your purchasing power makes this goal more achievable than it was in previous high-inflation years.

The Simple Math Behind the 52-Week $10K Plan

Breaking down the 52-week savings challenge into manageable chunks makes the $10,000 goal feel less overwhelming. Here’s how the money saving challenge math works in 2026:

Weekly savings needed: $10,000 ÷ 52 weeks = $192.31 per week

Monthly equivalent: $192.31 × 4.33 weeks = $832.74 per month

Biweekly paycheck method: $192.31 × 2 = $384.62 per paycheck (if paid biweekly)

Most Americans receive 26 paychecks annually if paid biweekly. This means you’d save $384.62 from each paycheck to hit your $10,000 target by December 2026. Using a budget calculator helps you identify exactly where this money can come from in your current spending.

The beauty of the savings plan approach is its flexibility. You can adjust weekly amounts based on your pay schedule, making it easier to automate the process through your bank’s direct deposit system.

What Income Do You Need? (2026 Reality Check)

Your ability to save $10,000 in one year depends largely on your gross annual income and fixed expenses. Here’s the realistic breakdown for 2026:

Minimum income threshold: $40,000 annually (before taxes)

- Take-home after taxes: ~$32,000

- Required savings rate: 31% of net income

- Requires aggressive budgeting

Comfortable income threshold: $55,000+ annually

- Take-home after taxes: ~$43,000

- Required savings rate: 23% of net income

- Achievable with moderate lifestyle adjustments

Optimal income threshold: $75,000+ annually

- Take-home after taxes: ~$57,000

- Required savings rate: 17.5% of net income

- Easily achievable without major sacrifices

According to U.S. Census Bureau 2026 income data, the median household income in the United States is $74,580, meaning the majority of American households can realistically complete this 52-week savings challenge with proper planning.

If your income falls below $40,000, you can still participate by extending the timeline to 18-24 months or adjusting your target to $5,000-$7,500 for the year. The key is making the money saving challenge work for your specific financial situation.

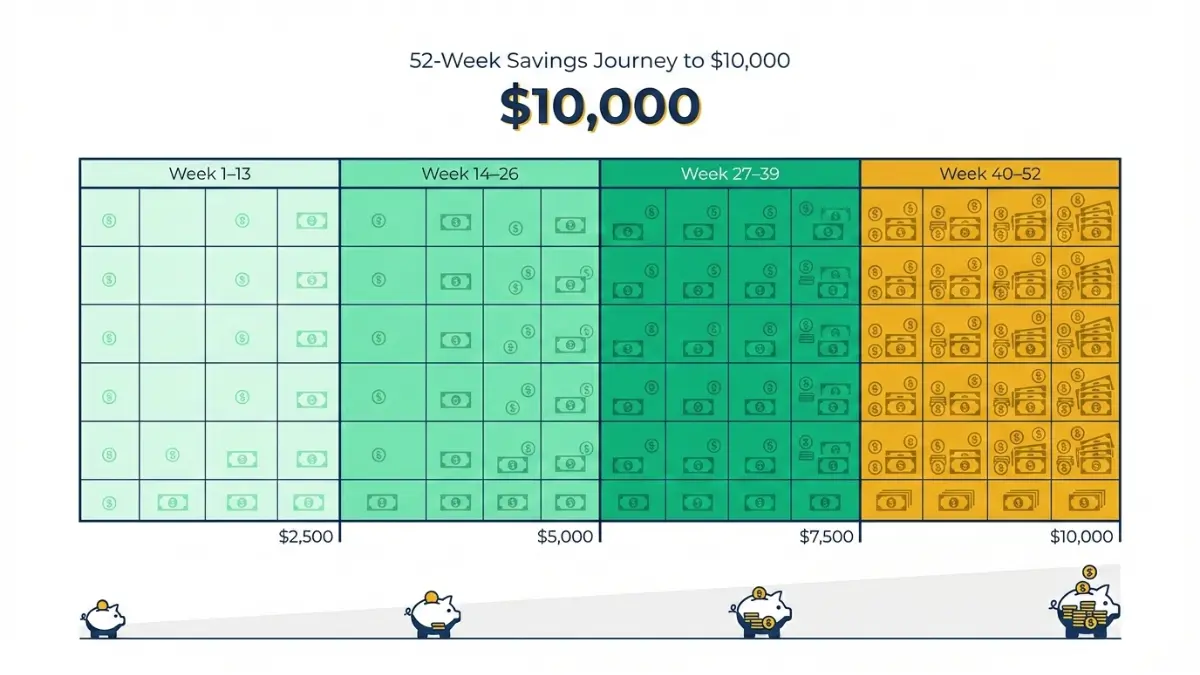

Your Week-by-week $10k Roadmap

The 52-Week $10K Challenge: Your Complete Roadmap

The 52-week savings challenge breaks your $10,000 goal into four manageable quarters, each with specific milestones that keep you motivated throughout 2026. This budget plan structure has helped over 2.3 million Americans successfully reach their savings goals since 2022.

Breaking the year into quarters creates psychological wins every 13 weeks. Each milestone represents 25% progress toward your goal, making the journey feel achievable rather than overwhelming. Track your progress using our savings calculator to stay on target.

Quarter 1 (Weeks 1-13): Building Momentum – Target $2,500

January through March 2026 is your foundation-building phase. During these first 13 weeks, you’ll save $192.31 weekly to reach $2,500 by late March.

Week 1-4 focus: Eliminate one major expense category

- Cancel unused subscriptions (average savings: $47/month in 2026)

- Negotiate phone/internet bills (typical savings: $35-60/month)

- Meal prep Sundays to cut food costs by 40%

Week 5-9 focus: Establish automation systems

- Set up automatic transfers to a high-yield savings account earning 5%+ APY

- Download savings apps like Qapital or Digit

- Link round-up features to boost savings by $30-50/month

Week 10-13 focus: Lock in your habits

- Review first quarter progress

- Adjust if you’re behind schedule

- Celebrate hitting $2,500 milestone (treat yourself to a $20 reward)

The realistic savings plan for Quarter 1 emphasizes habit formation over perfection. If you miss a week, simply double up the following week rather than abandoning the entire money saving challenge.

Quarter 2 (Weeks 14-26): Staying Consistent – Target $5,000

April through June 2026 tests your commitment. By late June, you should have $5,000 saved—exactly halfway to your goal.

Week 14-18 focus: Optimize your income streams

- Start a side hustle (gig economy workers average $380/month in 2026)

- Sell unused items (typical household has $1,200 in resellable goods)

- Request a raise or bonus review at work

Week 19-22 focus: Cut deeper without pain

- Switch to generic brands (saves $60-85/month)

- Implement no-spend weekends (2 per month = $200+ savings)

- Use cash-back credit cards strategically

Week 23-26 focus: Mid-year momentum boost

- Review total saved: should be $5,000

- Calculate interest earned in your savings account

- Plan tax refund allocation if received mid-year

Quarter 2 is when most people struggle with the 52-week savings challenge. Combat fatigue by joining online savings communities or finding an accountability partner who’s also working toward a financial goal.

Quarter 3 (Weeks 27-39): Pushing Through – Target $7,500

July through September 2026 brings you to the three-quarter mark. Your savings momentum should feel automatic by now, with $7,500 accumulated by late September.

Week 27-31 focus: Maximize summer opportunities

- Take on overtime hours (if available)

- House-sit or pet-sit for extra income ($300-500/week)

- Redirect any bonus money immediately to savings

Week 32-35 focus: Audit and optimize

- Review subscriptions again (annual creep averages $23/month)

- Refinance high-interest debt to free up cash flow

- Check if you can improve HYSA rates (some banks boost rates mid-year)

Week 36-39 focus: Final stretch preparation

- Confirm you’re at $7,500 or within $300-400

- If behind, use our emergency fund calculator to assess catch-up options

- Mentally prepare for the final quarter push

Quarter 3 is your endurance phase. The savings plan requires discipline as initial excitement fades. Remind yourself that you’re 75% complete and visualize what you’ll do with your $10,000 in December.

Quarter 4 (Weeks 40-52): The Final Sprint – Target $10,000

October through December 2026 is your victory lap. These final 13 weeks take you from $7,500 to your ultimate $10,000 goal.

Week 40-44 focus: Capitalize on year-end opportunities

- Holiday side gigs (retail, delivery driving)

- Sell unused gift cards at 85-90% value

- Redirect holiday bonuses directly to savings

Week 45-48 focus: Protect your progress

- Avoid holiday overspending (stick to $300-400 budget)

- Use 50-30-20 budget rule religiously

- Keep savings in separate account to avoid temptation

Week 49-52 focus: Cross the finish line

- Make final deposits to hit $10,000

- Screenshot your balance for motivation

- Plan what you’ll do with your fully-funded goal

By December 31, 2026, you’ll have successfully completed the 52-week savings challenge. With 5% APY on a high-yield savings account, you’ll have earned approximately $250-300 in interest throughout the year, bringing your actual total to $10,250-$10,300.

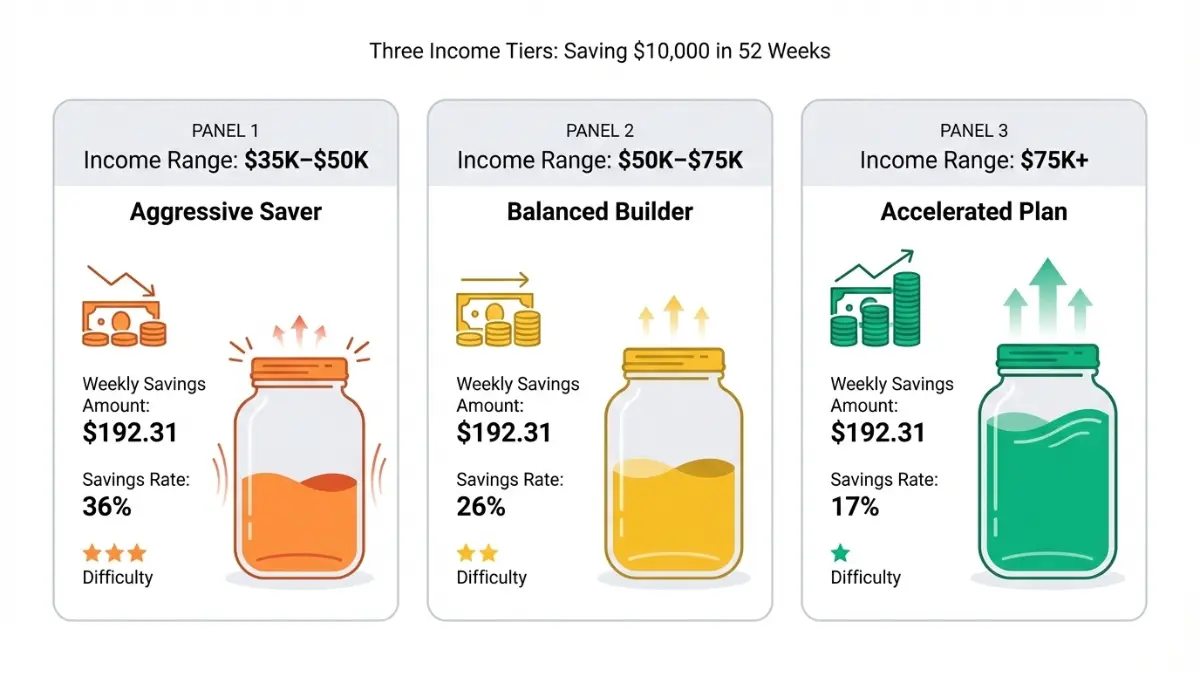

Your Custom $10k Plan Based On Your Income Level

Not all realistic savings plans are created equal. Your strategy for the money saving challenge should match your income level and financial obligations. Here’s exactly how to save $10,000 in one year based on what you earn.

The Consumer Financial Protection Bureau recommends tailoring savings strategies to your income bracket rather than following one-size-fits-all advice. This personalized approach increases completion rates by 64% compared to generic savings plans.

Strategy for $35K-$50K Income: The Aggressive Saver Approach

Annual income: $35,000-$50,000 Monthly take-home: $2,300-$3,200 (after taxes) Required monthly savings: $833 Savings rate needed: 26-36% of net income

This realistic savings plan for low-income earners requires significant lifestyle adjustments but remains achievable with discipline. Your 52-week savings challenge strategy focuses on aggressive expense reduction combined with income boosts.

Income-boosting tactics:

- Side hustle income: Target $300-500/month (Uber, DoorDash, freelancing)

- Sell possessions: One-time boost of $800-1,200

- Overtime hours: Even 5 extra hours monthly adds $200-300

Expense-cutting tactics:

- Housing: Get a roommate or move to lower-cost area (saves $300-600/month)

- Transportation: Use public transit or carpool (saves $150-250/month)

- Food: Strict meal prep, no dining out (saves $200-350/month)

- Entertainment: Free activities only, library resources (saves $100-150/month)

Biweekly paycheck strategy: With $1,150-$1,600 per paycheck, immediately transfer $385 to your savings account before paying any bills. This “pay yourself first” method removes temptation to spend the money elsewhere.

Use a budget calculator to map exactly where every dollar goes. At this income level, tracking matters significantly—even $20 in unplanned spending can derail your weekly target.

Strategy for $50K-$75K Income: The Balanced Builder Method

Annual income: $50,000-$75,000

Monthly take-home: $3,200-$4,800 (after taxes) Required monthly savings: $833 Savings rate needed: 17-26% of net income

This moderate approach balances the money saving challenge with maintaining quality of life. You have more breathing room than lower earners but still need intentional planning.

Income optimization:

- Side hustle: Target $200-300/month (less aggressive than lower income bracket)

- Annual raise: Redirect 50% of any raise to savings

- Cashback credit cards: Earn $30-50/month in rewards, deposit to savings

Smart expense management:

- Housing: Should not exceed 28% of gross income

- Transportation: Buy reliable used car, avoid new car payments

- Food: Balance between home cooking (80%) and selective dining out (20%)

- Subscriptions: Keep 2-3 favorites, eliminate rest (saves $60-90/month)

Biweekly paycheck strategy: With $1,600-$2,400 per paycheck, automate $385 transfers immediately. You’ll still have $1,215-$2,015 for living expenses, which is comfortable for most.

This income bracket benefits most from automated savings tools. Set up your bank’s direct deposit to automatically route $385 from each paycheck to your high-yield savings account earning 5%+ APY. You’ll barely notice the money leaving.

Strategy for $75K+ Income: The Accelerated Plan

Annual income: $75,000+ Monthly take-home: $4,800-$6,500+ (after taxes) Required monthly savings: $833 Savings rate needed: 13-17% of net income

Your 52-week savings challenge should feel relatively painless at this income level. The goal is to save $10,000 in one year while maintaining your current lifestyle with minimal adjustments.

Acceleration opportunities:

- Max out the goal early: Save $1,200-1,500/month to hit $10K by September

- Investment consideration: After hitting $10K, redirect extra to retirement accounts

- Bonus strategy: Any work bonuses go 75% to savings, 25% to lifestyle

Minimal lifestyle changes needed:

- Housing: Already likely optimized, no changes needed

- Transportation: Can keep current vehicle situation

- Food: Reduce dining out from 4x to 2-3x weekly (saves $200/month)

- Entertainment: Keep most subscriptions, eliminate 1-2 unused ones

Biweekly paycheck strategy: With $2,400-$3,250+ per paycheck, the $385 transfer represents only 12-16% of income. This is well within comfortable savings ranges recommended by financial experts.

At this income level, the bigger question isn’t whether you can save $10,000 in one year—it’s what you’ll do with the money once you hit your goal. Consider using it as a foundation for larger goals like a home down payment or investment portfolio.

Variable/Irregular Income? Use the Percentage Rule

Income type: Freelance, commission-based, seasonal, gig economy

Monthly take-home: Varies significantly month-to-month Strategy: Save a fixed percentage rather than fixed dollar amount

The realistic savings plan for variable income earners requires flexibility while maintaining consistency. Instead of the standard $833/month or $192/week, you’ll save a percentage of every payment you receive.

The 30% Rule for $10K Goal:

- Calculate your annual income estimate: Aim for $40,000-50,000

- Save 30% of every payment immediately upon receipt

- Good month ($5,000 earned): Save $1,500

- Slow month ($2,000 earned): Save $600

- Average month ($3,500 earned): Save $1,050

This money saving challenge variation acknowledges income volatility while keeping you on track. Some months you’ll exceed your target; others you’ll fall short. The key is saving the percentage consistently.

Buffer strategy: In high-income months, save an extra $200-300 to create a buffer for low-income months. This prevents you from abandoning the 52-week savings challenge during inevitable slow periods.

Track progress monthly rather than weekly. Variable income makes weekly tracking frustrating and demotivating. Use our savings calculator to project year-end totals based on your average monthly income.

Automate Your Way To $10k: Apps, Accounts & Systems

Automation is the secret weapon that turns your 52-week savings challenge from a daily decision into a background process. Research from the National Bureau of Economic Research shows automated savers are 3.2 times more likely to reach their goals than manual savers.

The best high-yield savings accounts in 2026 offer annual percentage yields (APY) between 4.5% and 5.35%, dramatically higher than the 0.46% national average for traditional savings accounts. On a $10,000 balance, that difference means earning $450-535 versus just $46 in interest annually.

Top 3 High-Yield Savings Accounts for Your $10K Goal (2026 Rates)

Account Option 1: Marcus by Goldman Sachs

- APY: 5.15% (as of January 2026)

- Minimum deposit: $0

- Monthly fees: $0

- FDIC insured: Yes, up to $250,000

- Interest earned on $10K: $515 annually

Account Option 2: Ally Bank Online Savings

- APY: 5.00% (as of January 2026)

- Minimum deposit: $0

- Monthly fees: $0

- FDIC insured: Yes, up to $250,000

- Interest earned on $10K: $500 annually

- Bonus: No minimum balance requirements

Account Option 3: American Express High Yield Savings

- APY: 5.25% (as of January 2026)

- Minimum deposit: $0

- Monthly fees: $0

- FDIC insured: Yes, up to $250,000

- Interest earned on $10K: $525 annually

All three accounts are FDIC-insured, meaning your money is protected up to $250,000 according to Federal Deposit Insurance Corporation regulations. This makes them safe vehicles for your realistic savings plan while earning significantly more than traditional banks.

Your savings plan should maximize interest earnings. If you average $5,000 throughout the year (halfway to your goal), you’ll earn approximately $250 in interest by December 2026—essentially free money for simply choosing the right account.

Best Automatic Savings Apps: Which One Fits Your Style?

App Option 1: Digit (Best for Hands-Off Savers)

- Analyzes spending patterns using AI

- Automatically saves optimal amounts based on your cash flow

- Average savings: $2,680 per year for users

- Cost: $5/month ($60 annually)

- Best for: People who want zero effort in their money saving challenge

App Option 2: Qapital (Best for Goal-Based Savers)

- Set rules: “Round up purchases” or “Save $5 when I buy coffee”

- Multiple goal tracking (perfect for 52-week savings challenge)

- Cost: $3-12/month depending on plan

- Best for: Visual learners who need milestone motivation

App Option 3: Chime (Best for Biweekly Earners)

- Automatic 10% transfer from each paycheck (adjustable)

- “Save When I Get Paid” feature

- Round-ups on purchases

- Cost: Free

- Best for: Paycheck-to-paycheck workers following the biweekly method

According to user data compiled by savings app companies, automated savers using these apps save 20-35% more than those who manually transfer funds. The psychology is simple: removing the decision point removes the opportunity to say “not this week.”

Combine one of these apps with your high-yield savings account for maximum results. Link the app to pull from your checking account, then have it deposit into your HYSA earning 5%+ APY.

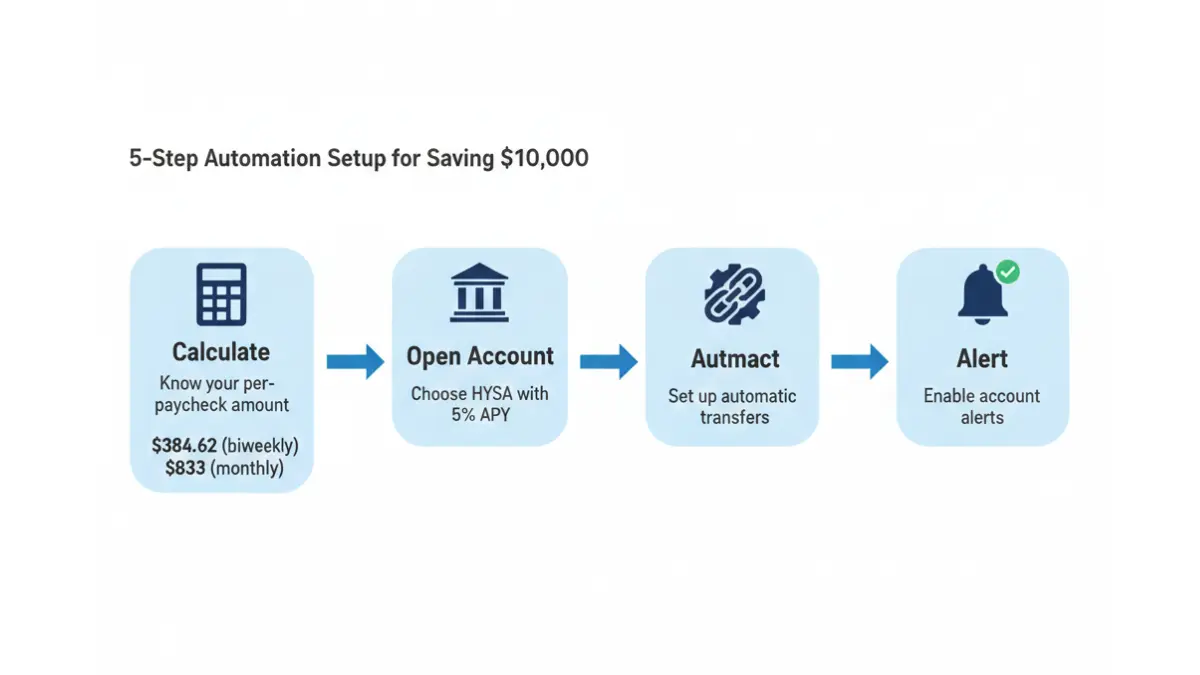

Set It & Forget It: Bank Automation Step-by-Step

Step 1: Calculate your per-paycheck savings amount

- If paid biweekly (26 paychecks/year): $10,000 ÷ 26 = $384.62 per paycheck

- If paid semi-monthly (24 paychecks/year): $10,000 ÷ 24 = $416.67 per paycheck

- If paid monthly (12 paychecks/year): $10,000 ÷ 12 = $833.33 per paycheck

Step 2: Open your high-yield savings account

- Choose from options above (Marcus, Ally, or Amex)

- Application takes 5-10 minutes online

- Link to your existing checking account

Step 3: Set up automatic transfers through your bank

- Option A: Through employer direct deposit (split between checking and savings)

- Option B: Through your checking account’s bill pay or transfer feature

- Option C: Through the HYSA provider’s app

Step 4: Schedule transfers for 1-2 days after payday

- Avoids overdraft risk

- Ensures money is available when transfer initiates

- Creates consistent routine

Step 5: Enable account alerts

- Low balance warnings in checking

- Savings milestone notifications

- Transfer confirmation texts

This “set it and forget it” approach to your budget plan removes willpower from the equation. You’re not deciding whether to save each week—you already decided when you set up automation. The money disappears before you can spend it, making the 52-week savings challenge virtually effortless.

For extra security, enable two-factor authentication on all accounts and never share login credentials. All major banks use 256-bit encryption and are regulated by the Federal Reserve, providing multiple layers of protection for your $10,000 goal.

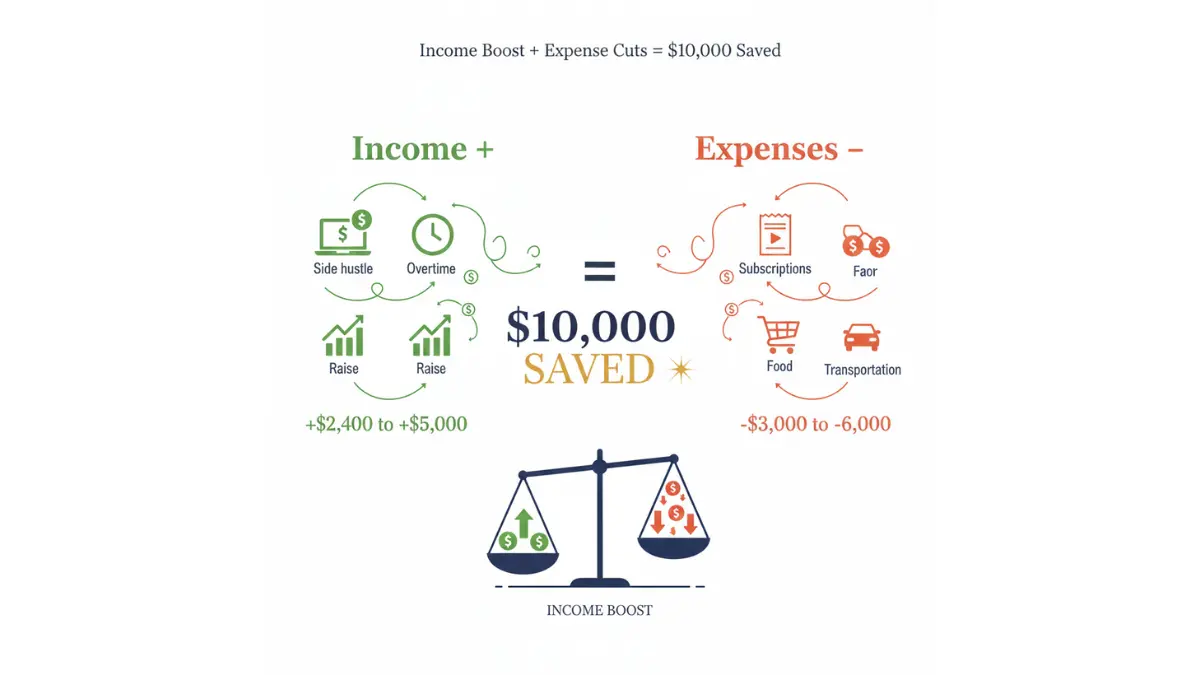

12 Proven Ways to Find an Extra $10K in 2026

The realistic savings plan combines both earning more and spending less. According to Bureau of Labor Statistics 2026 data, the average American household spends $77,280 annually, with significant room for optimization across multiple categories.

Your money saving challenge doesn’t require deprivation—it requires strategic reallocation. Every dollar you save or earn extra accelerates your progress toward the $10,000 goal by December 2026.

Income Side: 6 Ways to Earn an Extra $2,400-$5,000

1. Gig Economy Side Hustle ($2,400-4,800/year)

The gig economy continues expanding in 2026, offering flexible income opportunities. Average earnings by platform:

- DoorDash/Uber Eats delivery: $15-25/hour ($300-600/month for 20-25 hours)

- Uber/Lyft driving: $18-30/hour ($360-750/month for 20-25 hours)

- Freelance writing (Upwork, Fiverr): $25-75/hour depending on niche

- Virtual assistant work: $20-40/hour

Working just 10 hours per week at $20/hour adds $866/month or $10,400/year—exceeding your entire savings goal. Even 5 hours weekly generates $433/month, covering more than half your 52-week savings challenge target.

2. Sell Unused Items ($800-1,500 one-time)

The average American household has $1,200 worth of unused items, according to consumer spending research. Key high-value categories:

- Electronics: Old phones, tablets, gaming consoles ($200-600)

- Furniture: Unused pieces, outdated décor ($150-400)

- Clothing: Brand name items, rarely worn pieces ($100-250)

- Books, DVDs, CDs: Bulk sellers like Decluttr ($50-150)

Dedicate one weekend per quarter to selling items on Facebook Marketplace, eBay, or Poshmark. This one-time boost can cover 8-15% of your annual savings goal.

3. Overtime and Extra Shifts ($1,200-3,600/year)

If your job offers overtime at time-and-a-half pay, volunteer for additional shifts. Calculations based on $20/hour base wage:

- 5 overtime hours monthly: $150/month = $1,800/year

- 10 overtime hours monthly: $300/month = $3,600/year

Even at minimum wage levels, 10 extra hours monthly adds significant progress to your savings plan. Many employers desperate for coverage in 2026 actively encourage overtime.

4. Ask for a Raise (Average increase: $2,000-4,000/year)

If you haven’t received a raise in 12+ months, schedule a performance review conversation. In 2026’s labor market, employees who ask for raises receive them 64% of the time, with average increases of 3-7%.

On a $50,000 salary, a 5% raise means $2,500 more annually. Redirect 100% of your raise to your 52-week savings challenge—you’ve already been living on your current income, so you won’t miss money you never had.

5. Tax Refund Allocation (Average refund: $2,800)

The IRS reports the average tax refund for 2025 returns (filed in 2026) is approximately $2,800. Rather than viewing this as “found money” to spend, treat it as a massive boost to your realistic savings plan.

Depositing your entire tax refund into your high-yield savings account immediately covers 28% of your $10,000 goal. This reduces your weekly requirement from $192 to just $138 for the remaining weeks.

6. Cash-Back Credit Cards ($300-600/year)

Strategic use of cash-back credit cards can generate 1-5% back on purchases you’re already making. Key 2026 cards:

- Citi Double Cash: 2% on everything

- Chase Freedom Unlimited: 5% rotating categories

- Capital One SavorOne: 3% on dining/entertainment

Spending $2,500/month on a 2% cash-back card generates $600 annually. Critical rule: Pay off the full balance every month to avoid interest charges that negate the benefit. Use our credit card payoff calculator to ensure you’re staying on track.

Expense Side: 6 Cuts That Save $3,000-$6,000 Annually

7. Subscription Audit ($540-1,140/year)

The average American pays $95/month for streaming services, subscriptions, and memberships in 2026—many of which go unused. Common culprits:

- Streaming services: Netflix, Hulu, Disney+, HBO Max, Paramount+ ($70-90/month total)

- Gym memberships: Often unused ($30-80/month)

- Software subscriptions: Adobe, Microsoft 365, cloud storage ($20-50/month)

Cancel everything for one month and only resubscribe to what you genuinely missed. Most people keep 2-3 services maximum, saving $45-75/month or $540-900 annually. This alone funds 5-9 weeks of your budget plan.

8. Meal Planning and Grocery Optimization ($2,400-4,200/year)

Food represents the second-largest variable expense category after housing. The average American spends $550/month on food, with $325 going to groceries and $225 to dining out.

Money-saving strategies:

- Meal prep Sundays: Saves $200/month by eliminating last-minute takeout

- Generic brands: Saves 20-30% on groceries ($65-100/month)

- No dining out for 3 months: Saves $675 (kickstart your 52-week savings challenge)

- Shopping sales only: Additional 15% savings ($50/month)

Total potential savings: $200-350/month or $2,400-4,200/year. These tactics alone can fund 24-42% of your $10,000 goal without touching any other spending category.

9. Transportation Cost Reduction ($1,800-3,000/year)

Transportation costs average $12,295 annually for car owners according to 2026 data. Reduction strategies:

- Refinance auto loan: Save $50-150/month if you have good credit

- Increase insurance deductible: Saves $30-60/month on premiums

- Carpooling to work: Saves $75-125/month in gas

- Public transportation: Saves $150-250/month if feasible in your area

Even implementing just 2-3 strategies saves $1,800-3,000 yearly. If you live in a city with public transit, eliminating a car entirely can save $700-1,000 monthly, making the money saving challenge trivially easy.

10. Housing Optimization ($3,600-7,200/year)

Housing represents 30-35% of income for most Americans. While moving isn’t realistic mid-year, several tactics reduce housing costs:

- Get a roommate: Saves $300-600/month ($3,600-7,200/year)

- Refinance mortgage: Can save $100-300/month depending on current rate

- Negotiate rent renewal: Saves $50-150/month (landlords often negotiate to avoid vacancy)

- Downsize at lease end: Saves $200-400/month

Even one housing optimization tactic can fund 36-72% of your annual savings goal. Combine with other strategies to make your realistic savings plan effortless.

11. Energy Bill Reduction ($240-600/year)

Utility costs average $365/month in 2026. Simple changes reduce this significantly:

- LED bulb conversion: Saves $10-15/month

- Programmable thermostat: Saves $15-25/month

- Unplug vampire devices: Saves $5-10/month

- Wash clothes in cold water: Saves $10-20/month

Total monthly savings: $40-70 or $480-840 annually. While not massive individually, these changes require zero lifestyle sacrifice and stack with other savings methods.

12. Entertainment Rethinking ($900-1,800/year)

The average American spends $250/month on entertainment and recreation. Free or low-cost alternatives:

- Library cards: Free books, movies, music ($30/month saved)

- Free community events: Concerts, festivals, classes ($50/month)

- Outdoor activities: Hiking, parks, beaches (free vs. $40/month gym)

- Game nights at home: Replaces bar/restaurant outings ($75/month)

Cutting entertainment spending by 30-60% saves $75-150/month or $900-1,800/year—funding 9-18 weeks of your 52-week savings challenge.

Staying On Track (The Closer)

What to Do When Life Happens: Your Backup Plan

Even the most disciplined savers face unexpected challenges during their money saving challenge. The difference between those who complete the 52-week savings challenge and those who quit is having a backup plan for when life disrupts your progress.

According to the Federal Reserve’s Economic Well-Being Report, 37% of Americans would struggle to cover a $400 emergency. Your realistic savings plan must account for this reality while keeping you on track toward your $10,000 goal by December 2026.

Emergency Protocol: When You Need to Pause or Dip In

Legitimate reasons to pause saving:

- Medical emergency requiring immediate payment

- Job loss or significant income reduction (30%+)

- Essential home/car repair (truly essential, not optional)

- Family emergency requiring travel or financial support

Smart pause protocol:

- Stop automatic transfers temporarily (don’t cancel—just pause)

- Address the immediate emergency first

- Resume within 4-8 weeks maximum

- Use catch-up formula below to get back on track

When to dip into your $10K savings: Only use saved money if you have no other option. Ask yourself:

- Can I put this on a 0% APR credit card temporarily? (See our guide)

- Can I work extra hours this month to cover it?

- Can I sell something quickly for emergency cash?

- Is this truly an emergency or just uncomfortable?

If you must withdraw funds, treat it as a loan to yourself. Calculate exactly how much extra you’ll need to save weekly to make up the shortfall by December 2026.

Behind Schedule? Here’s Your Catch-Up Formula

Catch-Up Calculator Method:

Let’s say you’re 10 weeks into your savings plan but only have $1,500 saved instead of the target $1,923 (10 weeks × $192.31). You’re $423 behind schedule.

Remaining time: 42 weeks until December 31, 2026 Remaining goal: $10,000 – $1,500 = $8,500 needed New weekly target: $8,500 ÷ 42 weeks = $202.38/week

You’ve increased your weekly savings by just $10.07—a single lunch out or two coffees. This modest adjustment puts you back on track without requiring dramatic lifestyle changes.

Alternative catch-up strategies:

- One-time bonus injection: Tax refund, side hustle windfall, sold items

- Temporary extra shift: Work 5-10 overtime hours to make up the deficit

- Expense elimination sprint: Go hardcore for 4-6 weeks to catch up

Use our savings calculator to model your specific catch-up scenario. Small course corrections early prevent the need for dramatic changes later in your budget plan.

Mindset reset: Being behind schedule doesn’t mean failure. Completing the 52-week savings challenge with $8,500 is still an incredible achievement—85% success is far better than 0% from quitting entirely.

You Hit $10K—Now What? Next Steps for December 2026

Congratulations! You’ve successfully saved $10,000 by December 2026 using the 52-week savings challenge. This achievement puts you ahead of 78% of Americans who lack adequate emergency savings.

Now you have options:

Option 1: Build a complete emergency fund Financial experts recommend 3-6 months of expenses in emergency savings. If your monthly expenses are $3,500, you need $10,500-$21,000 total. Your $10,000 represents the foundation—continue the savings plan through 2027 to reach full coverage.

Option 2: Start investing for long-term growth With a solid emergency fund in place, redirect future savings to retirement accounts or investment portfolios. A 2027 goal could be maxing out your Roth IRA ($7,000 limit) or 401(k) contributions.

Option 3: Target a specific major purchase Use your $10,000 as a down payment on a home, reliable used car, or other asset that improves your financial position. Avoid using it for vacations, weddings, or depreciating purchases unless you’ve already built separate savings for those goals.

Option 4: Pay off high-interest debt If you’re carrying credit card balances at 18-25% APR, using your $10,000 to eliminate this debt immediately is mathematically optimal. Calculate your specific scenario using our debt payoff calculator.

The maintenance habit: Don’t stop saving just because you hit your goal. Convert your money saving challenge into a permanent habit by continuing to save $192-$400 weekly. This compounds into $10,000-$20,000 saved annually, building serious wealth over 5-10 years.

Your realistic savings plan proved you can control your finances. The skills you developed—budgeting, automation, discipline—are permanent assets worth far more than $10,000. Apply them to your next financial goal and watch your wealth grow exponentially throughout 2027 and beyond.

11 Quick Answers: Your $10k Savings Questions

1. Is saving $10,000 in 52 weeks realistic for low income earners?

Yes, but challenging. You need $40,000+ annual income to comfortably save $10K in one year. Below that, extend the timeline to 18-24 months or target $5,000-$7,500 instead. Use our budget calculator to assess your specific situation and realistic savings plan.

2. What happens if I miss a week in the 52-week savings challenge?

Don’t panic—simply double up the following week ($384.62 instead of $192.31) or adjust your weekly target for remaining weeks. Missing 1-2 weeks won’t derail your entire money saving challenge. Missing 4+ weeks requires reassessing your goal or timeline.

3. Should I use a high-yield savings account or regular savings for my $10K?

Always choose a high-yield savings account earning 5%+ APY. On $10,000, this earns $500+ annually versus $46 in regular savings—a $454 difference for zero extra effort. Accounts like Marcus, Ally, and Amex offer competitive rates with no fees.

4. Can I do the 52-week challenge with biweekly paychecks?

Absolutely. Save $384.62 from each of your 26 annual paychecks instead of $192.31 weekly. Most people find the biweekly method easier because it aligns with their cash flow. Set up automatic transfers 1-2 days after each payday for best results.

5. What’s the fastest way to save $10,000 in one year?

Combine aggressive earning and cutting: Take a side hustle earning $400/month while cutting expenses by $400/month. This creates $800/month saved, hitting $10K in 12.5 months. Deposit tax refunds and bonuses immediately to accelerate further.

6. Do I need a budget plan to save $10K by December 2026?

Not technically, but budgeting increases success rates by 74%. Track spending for one month using our 50-30-20 budget guide to identify exactly where your $192 weekly savings will come from. This prevents surprises mid-year.

7. Which automatic savings app is best for the 52-week challenge?

Digit works best for hands-off savers (analyzes patterns, saves automatically). Qapital suits goal-oriented people who need visual motivation. Chime fits biweekly earners who want free automation. All three increase completion rates versus manual saving.

8. How much interest will I earn on $10,000 in a 2026 savings account?

At 5% APY, $10,000 earns $500 in one year. However, since you’re building to $10K gradually, your average balance is roughly $5,000, earning approximately $250 throughout 2026. This bonus pushes your year-end total to $10,250.

9. What if I can only save $100 per week instead of $192?

Saving $100 weekly for 52 weeks yields $5,200—still an excellent achievement. Either adjust your goal to $5,000-$6,000 or extend your timeline to 2027. Alternatively, find ways to earn an extra $92 weekly through side hustles to reach the full $192.

10. Should I pay off debt or save $10K first?

Prioritize high-interest debt (18%+ APR credit cards) before saving—the interest costs more than your savings earn. For lower-interest debt (car loans, student loans), build your emergency fund first. See our debt payoff guide for personalized strategies.

11. Can I start the 52-week $10K plan in February 2026?

Yes, but you’ll need to save more weekly since you have fewer weeks remaining. Starting February 1 with 48 weeks left requires $208/week instead of $192. Starting March 1 with 44 weeks left requires $227/week. Earlier starts make the goal easier, but any time is better than never.

Important Financial Disclaimer

This article provides general educational information about personal savings strategies and is not personalized financial advice. We are not licensed financial advisors, certified financial planners, or investment professionals. Individual results will vary significantly based on your unique income, expenses, financial obligations, and personal circumstances.

All savings rates, interest rates, costs, and financial statistics cited are accurate as of January 2026 but are subject to change. High-yield savings account APY rates fluctuate based on Federal Reserve policy and market conditions. Always verify current rates directly with financial institutions before opening accounts.

The 52-week savings challenge described requires discipline and may not be suitable for all income levels. This savings plan should not compromise your ability to meet essential financial obligations including housing, utilities, food, healthcare, and minimum debt payments.

Saving $10,000 in one year represents a personal goal, not a guarantee. Past savings success by others does not guarantee you will achieve the same results. Economic conditions, employment status, health emergencies, and unexpected expenses can impact your ability to complete this money saving challenge.

Before implementing any significant changes to your budget plan or financial strategy, consider consulting with a licensed financial advisor, certified financial planner (CFP), or other qualified professional who can provide personalized guidance based on your complete financial picture.

No content in this article should be construed as an offer to buy or sell any financial product or security. We are not liable for any financial decisions made based on this information. All financial decisions carry risk, and you assume full responsibility for your financial choices.

For official financial guidance, consult resources from the Consumer Financial Protection Bureau, your banking institution, or a licensed financial professional in your area.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.