Is 700 a Good Credit Score in 2026? Here’s What Lenders Actually See

Most people with a 700 score think they’re in good shape. Lenders disagree — and it costs them $340/month on a mortgage. Discover the 7 FICO tiers, exact approval thresholds by loan type, and the 60-day plan to cross the 740 line.

In This Article

What Is A Good Credit Score In 2026?

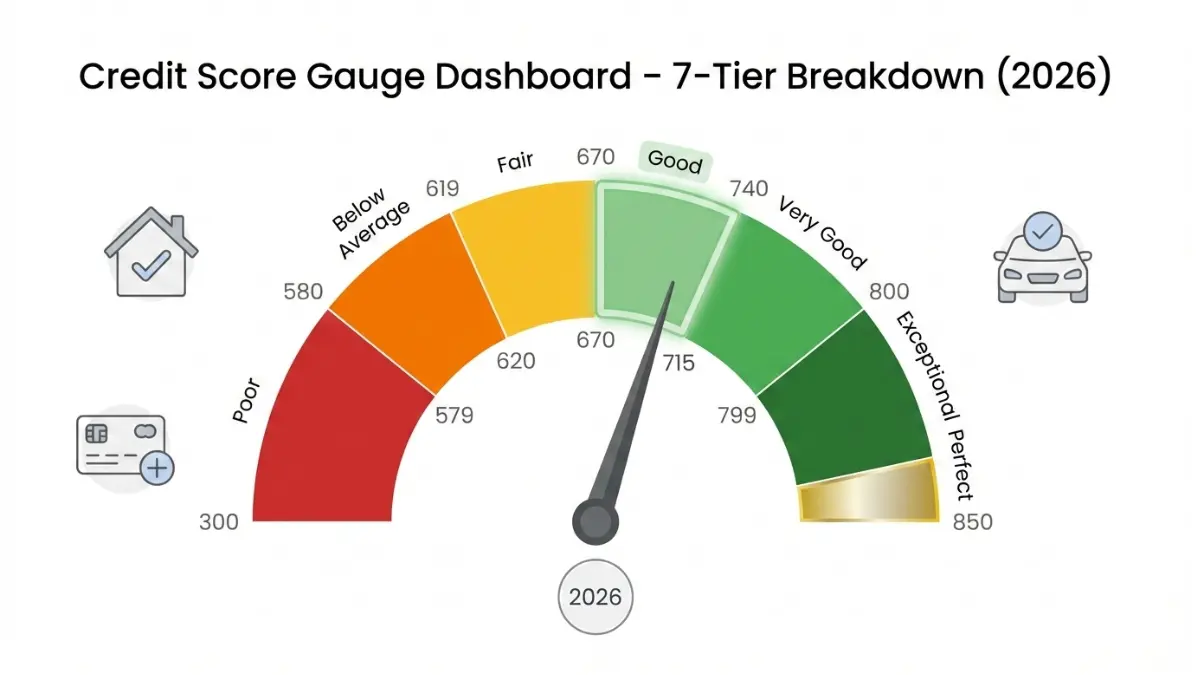

A good credit score in 2026 ranges from 670 to 739 on the FICO scoring model, which most lenders use to evaluate creditworthiness. If you’re wondering whether your score qualifies as “good,” you’re likely comparing yourself against national benchmarks—and you should know that the average American credit score now sits at 715, according to recent consumer credit data from the CFPB.

Here’s the reality: credit score tiers determine everything from mortgage approval to the interest rates you’ll pay over decades. The difference between a “good” and “excellent” credit score can translate to tens of thousands of dollars in savings on major purchases.

The 7 Credit Score Tiers (2026 FICO Model):

| Score Range | Credit Tier | What It Means |

|---|---|---|

| 300-579 | Poor | High-risk; limited approval odds |

| 580-619 | Below Average | Subprime rates; requires large deposits |

| 620-669 | Fair | Conditional approval; higher rates |

| 670-739 | Good | Prime rates; solid approval odds |

| 740-799 | Very Good | Excellent rates; premium card access |

| 800-849 | Exceptional | Best available rates; top-tier rewards |

| 850 | Perfect | Maximum financial leverage |

Most lenders draw the line at 670 when determining whether you qualify for prime interest rates. Below that threshold, you’re typically categorized as a higher-risk borrower, which means steeper costs and stricter terms. Above 670, you enter the realm of competitive rates and broader approval options.

But here’s what most articles won’t tell you: the score you “need” depends entirely on your financial goal. A 620 might get you an FHA mortgage, but you’ll need closer to 740 for premium credit cards or the best auto loan rates. The Federal Trade Commission emphasizes understanding these thresholds before applying for credit to avoid unnecessary hard inquiries.

FICO vs. VantageScore: Quick Comparison

You actually have multiple credit scores. FICO scores (used by 90% of lenders) and VantageScore (used by Credit Karma and similar platforms) use similar ranges but different calculation methods. Your VantageScore might be 20-30 points different from your FICO score, so always check which model a lender uses before applying.

The bottom line? A good credit score opens doors—but knowing which doors require which scores gives you the strategic advantage most consumers lack.

The 7 Credit Score Tiers Explained (2026 Breakdown)

Understanding credit score tiers is like having a roadmap to financial opportunity. Each tier unlocks different products, rates, and approval probabilities—and knowing where you stand helps you target the right next step.

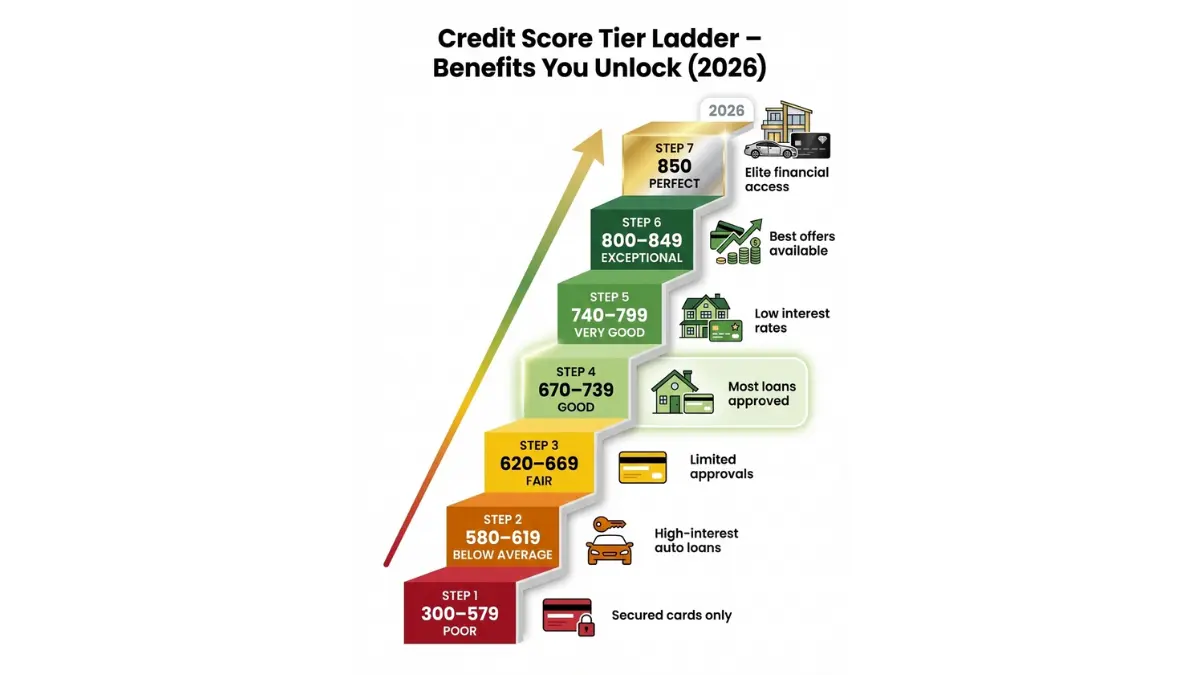

Tier 1 – Poor Credit (300-579)

This range signals severe credit challenges: recent bankruptcies, charge-offs, or collections. Only 16% of Americans fall into this category, and approval odds for traditional loans hover around 8-12%.

You’ll face security deposits for utilities, prepaid cards instead of traditional credit, and sky-high interest rates if approved at all. The focus here isn’t borrowing—it’s rebuilding through secured credit cards and becoming an authorized user on someone else’s established account.

Tier 2 – Below Average Credit (580-619)

This “subprime” zone includes roughly 12% of consumers. You can access FHA mortgages starting at 580, but expect interest rates 1.5-2.5 percentage points higher than prime borrowers pay.

A $250,000 mortgage at 580 might carry a 7.8% rate versus 5.3% for a 740 score—that’s $127,000 more in interest over 30 years. Auto lenders will approve you, but often with 18-24% APRs and larger down payment requirements.

Tier 3 – Good Credit (670-739)

Welcome to the sweet spot where 21% of Americans reside. This is where our comprehensive credit score guide becomes essential reading—you’re positioned to access prime rates but still have room for significant savings by climbing higher.

At 700, you’ll get approved for most conventional mortgages, mid-tier rewards credit cards, and auto loans around 6-8% APR. The gap you’re missing? $40,000-60,000 in lifetime interest savings compared to the next tier up. You’re good, but not optimized.

Tier 4 – Very Good Credit (740-799)

This tier houses 25% of consumers and unlocks premium financial products. Chase Sapphire Reserve, American Express Platinum, and 0% APR promotional financing become accessible. Mortgage rates drop another 0.5-0.75%, and auto lenders compete aggressively for your business.

You’ll receive pre-approved offers regularly, qualify for higher credit limits, and access mortgage refinance opportunities that borrowers below 740 simply don’t see. The difference between 700 and 760? Roughly $380/month on a $400,000 mortgage.

Tier 5 – Excellent Credit (800-850)

Only 23% of Americans reach this elite tier, where you command the absolute best rates and terms available. Banks view you as minimal risk, offering top-tier rewards cards, the lowest mortgage rates (often 0.25-0.5% below market), and instant approvals for virtually any consumer credit product.

According to research from the Federal Reserve, consumers with 800+ scores pay an average of $250,000 less in interest over their lifetime compared to those maintaining scores in the 650-680 range. That’s not a typo—a quarter million dollars in savings from disciplined credit management.

The path from good credit score territory to excellent isn’t luck—it’s strategy. Each tier represents specific financial opportunities and costs, making your position on this spectrum one of the most important numbers in your financial life.

What You’ll Get Approved For (By Credit Score)

Your credit score isn’t just a number—it’s the key that unlocks specific financial products at specific prices. Here’s exactly what you can expect at each threshold in 2026.

Mortgage Approval & Rates (2026 Thresholds)

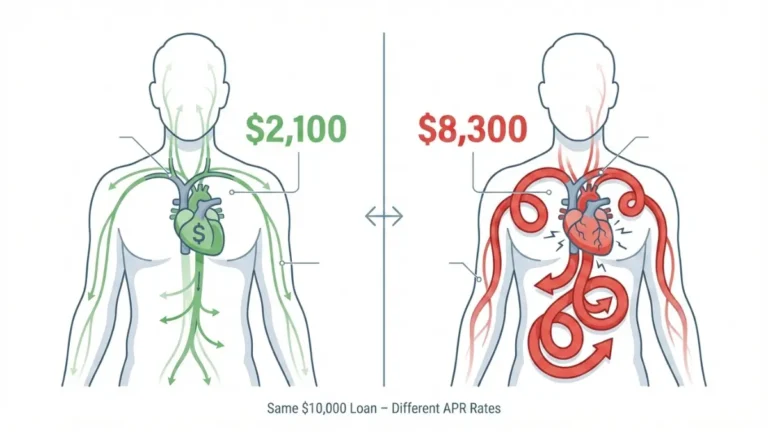

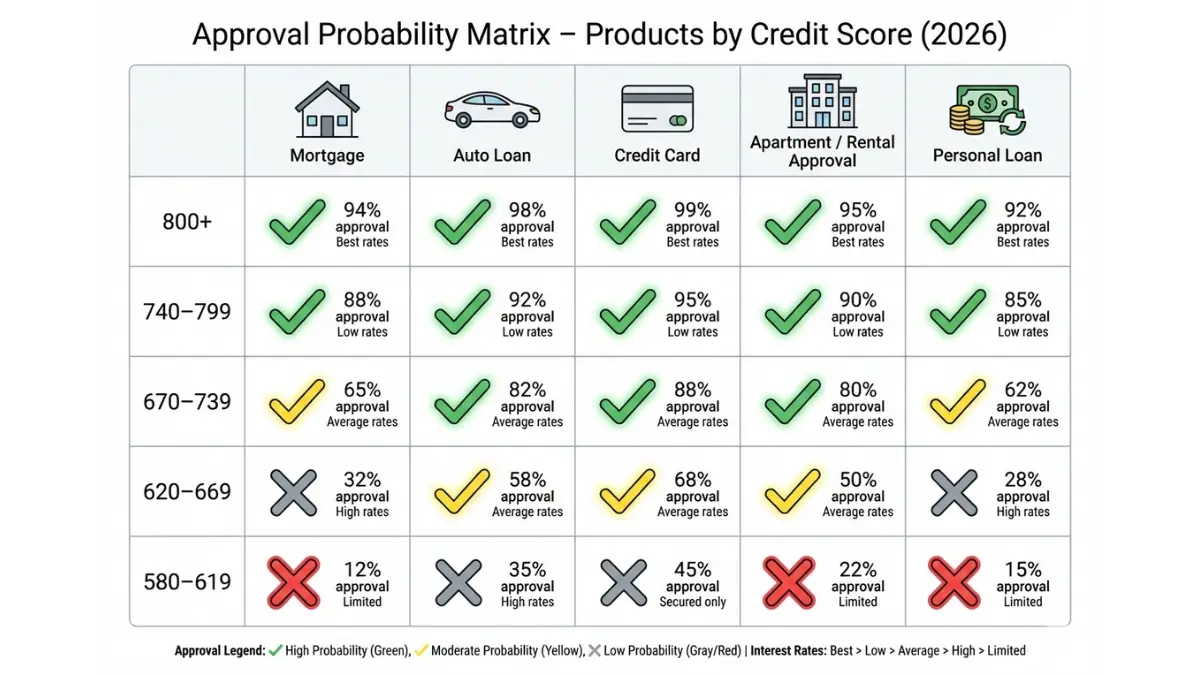

FHA Loans: 580 minimum with 3.5% down, but rates run 6.8-7.5%. At 620, conventional loans open up with 5% down and rates around 6.5-7.2%. The real savings start at 740+, where you’ll see rates of 5.8-6.3%—which translates to $340/month savings on a $350,000 loan compared to a 620 score.

Using our home affordability calculator shows that a 100-point score improvement can increase your buying power by $45,000-65,000 without changing your monthly payment. That’s the difference between a 3-bedroom and 4-bedroom home in most markets.

The Consumer Financial Protection Bureau reports that borrowers with 760+ scores receive the best available rates from 93% of lenders, while those between 620-679 face rate premiums averaging 1.2 percentage points higher.

Auto Loan Approval Odds

Subprime (580-619): 62% approval rate with average APRs of 18-24% and required down payments of 15-20%. Prime (670-739): 88% approval rate with APRs around 7-11% and negotiable down payments. Super-prime (740+): 96% approval rate with promotional rates as low as 2.9-4.9% and zero-down options.

A $35,000 car loan over 60 months at 680 versus 760 represents $4,200 in interest savings. That’s substantial money that could fund your emergency fund or retirement contributions instead.

Credit Card Approval by Score

670-699: Approved for standard rewards cards like Chase Freedom Unlimited, Discover it, and Capital One Quicksilver. Credit limits typically $3,000-8,000. Annual fees usually waived, but premium cards remain out of reach.

700-739: Access to mid-tier travel cards like Chase Sapphire Preferred, Capital One Venture, and American Express Gold. Limits jump to $8,000-15,000, and you’ll qualify for sign-up bonuses worth $500-750.

740+: Premium cards like Chase Sapphire Reserve, American Express Platinum, and high-limit business cards become available. Initial limits often $15,000-25,000+, and you’ll receive 0% APR promotional offers lasting 15-21 months. Our credit card payoff calculator can help you strategically use these promotional periods to eliminate existing balances.

Apartment Rental Requirements

Major metro markets have gotten stricter. NYC landlords typically require 700+ for competitive apartments. San Francisco and Los Angeles: 680+ is standard. Smaller markets may accept 620-650, but expect larger security deposits (2-3 months’ rent vs. 1 month at 700+).

Property management companies increasingly use automated screening that auto-rejects applications below certain thresholds. Missing the cutoff by even 10 points can mean losing your ideal apartment to another applicant.

Personal Loan Rates

640-679: APRs of 16-24% on personal loans of $5,000-15,000. Origination fees of 3-6%. 680-719: APRs drop to 11-18% with lower fees (1-3%). Loan amounts up to $25,000. 720+: APRs of 6-12% with minimal fees and loan amounts reaching $50,000+.

The spread matters enormously. Borrowing $20,000 over 5 years at 680 versus 740 costs you $6,800 more in interest—enough to fully fund a Roth IRA for more than a year.

Understanding these thresholds helps you target the right score for your immediate needs. Whether you’re three months from buying a home or planning for next year’s car purchase, knowing the approval landscape lets you optimize your credit strategy with precision.

How Does Your Credit Score Compare? [by Age Group]

Context matters. A 680 credit score means something different at age 25 versus 55, and understanding how you stack up against your age cohort provides valuable perspective on your credit journey.

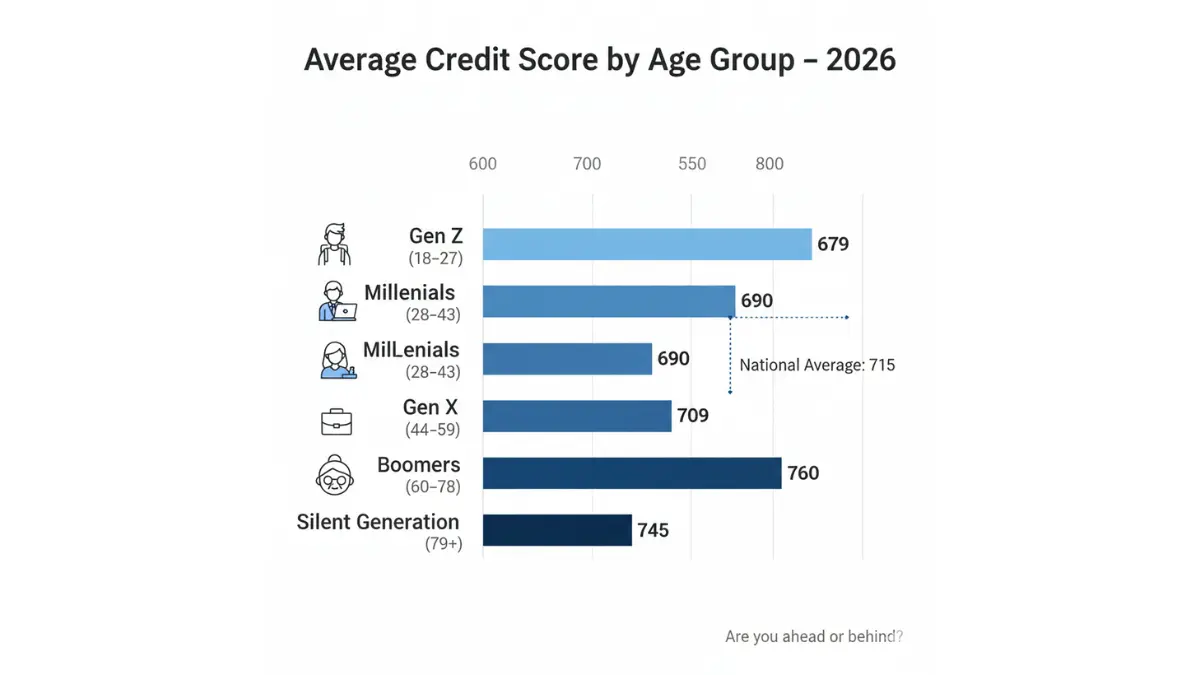

2026 Average Credit Scores by Generation:

| Age Group | Generation | Average Score | Median Score |

|---|---|---|---|

| 18-27 | Gen Z | 679 | 672 |

| 28-43 | Millennials | 690 | 687 |

| 44-59 | Gen X | 709 | 706 |

| 60-78 | Boomers | 745 | 742 |

| 79+ | Silent Gen | 760 | 758 |

These benchmarks come from Federal Reserve consumer credit data analyzing 220 million credit files. The pattern is clear: age correlates strongly with credit scores because older consumers have longer payment histories, lower utilization rates, and more diverse credit mixes.

Why Gen Z Averages Lower (But It’s Normal)

At 23, having a 660 score isn’t a failure—it’s expected. You likely have just 2-4 years of credit history, maybe one or two credit cards, and possibly a student loan. Your age cohort hasn’t had time to build the 10+ year payment history that boosts scores into the 740+ range.

The opportunity? If you’re above your age group average, you’re ahead of schedule. A 25-year-old with a 720 score is positioned for massive long-term savings because they’ll access premium rates decades earlier than peers. Understanding strategies from our guide on how to pay off debt fast accelerates this advantage.

The Millennial Middle Ground

Millennials averaging 690 sit in an interesting position—right at the edge of prime rates but not quite optimized. This generation carries higher student loan balances than predecessors, which can suppress scores through utilization and inquiry impacts.

The gap to close? Just 20-30 points to reach 720 unlocks significantly better mortgage rates. For a generation entering peak home-buying years, this matters tremendously.

Gen X: Peak Earning, Peak Scores

Gen X enjoys both higher incomes and better credit profiles. Average scores of 709 reflect established credit histories, paid-off student loans, and strategic credit management. This demographic has the financial literacy that comes from experience—they’ve weathered rate changes, recessions, and understand how credit impacts major purchases.

Boomers & Silent Generation: Credit Mastery

Scores averaging 745-760 aren’t accidental. These generations benefit from 30-50 years of payment history, minimal hard inquiries (they’re not frequently applying for new credit), low utilization (high limits, lower balances), and diverse credit mixes including fully paid mortgages.

The lesson? Time is your ally. Consistent positive behavior compounds just like investment returns. A 28-year-old managing credit wisely today is setting up their 58-year-old self for maximum financial flexibility.

Are you ahead or behind for your age? If you’re below your cohort average, focus on the fundamentals: on-time payments, utilization below 30%, and avoiding new inquiries. If you’re above average, you’re already winning—maintain those habits and watch your score naturally climb as your history lengthens.

How To Build Your Credit Score To 740+ [step-by-step]

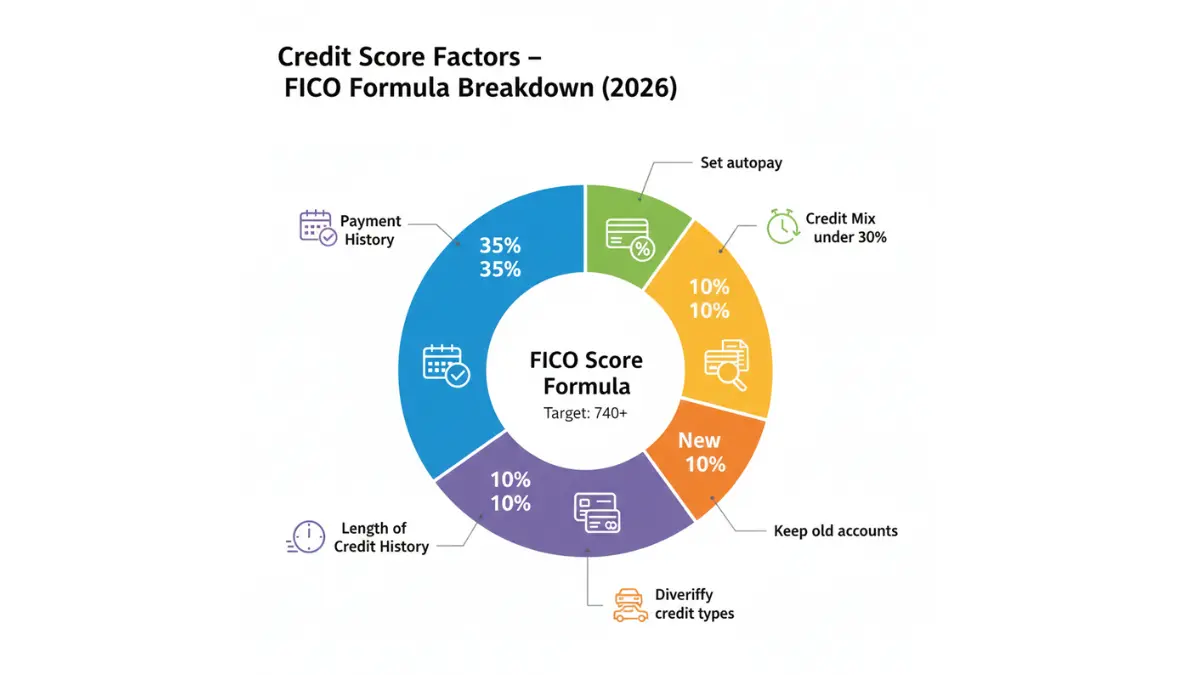

Building excellent credit isn’t mysterious—it’s mechanical. Understanding the five factors that create your credit score lets you systematically engineer improvements over 12-18 months.

Payment History (35% of Your Score)

This single factor carries more weight than everything else combined. One 30-day late payment can drop your score 60-110 points and remain on your report for seven years.

The fix is automation. Set up autopay for at least minimum payments on every account. Even if you pay more manually later in the month, that automated minimum ensures you never miss a due date because of travel, illness, or simple forgetfulness.

Recovery timeline: If you have late payments, the damage fades as they age. A late payment from 24 months ago hurts less than one from 6 months ago. There’s no shortcut—you need consistent on-time payments moving forward.

Credit Utilization (30% of Your Score)

This ratio—your balances divided by your total credit limits—should stay below 30% overall and ideally under 10% per card. A $3,000 balance on a $10,000 limit is 30% utilization. A $300 balance on that same limit is 3%—and the difference in score impact is substantial.

Strategic utilization moves:

- Request credit limit increases every 6-12 months (doesn’t require hard inquiry at many issuers)

- Pay down balances before statement closing dates (the balance reported to bureaus is usually your statement balance, not your current balance)

- Split large purchases across multiple cards to avoid high utilization on any single account

- Use our debt consolidation calculator to evaluate whether consolidating multiple high-balance cards into a personal loan improves your overall utilization

Real example: A client reduced utilization from 68% to 18% by requesting limit increases on three cards and paying an extra $200/month toward balances. Score jumped 47 points in 90 days.

The Federal Trade Commission’s credit guidance confirms that utilization is the fastest-moving component of your score—improve it and you’ll see results within 30-60 days.

Credit History Length (15% of Your Score)

Average age of accounts matters. Opening five new credit cards in one month tanks this metric. Closing your oldest card shortens your history. The strategy? Keep old accounts active with small recurring charges (Netflix subscription, phone bill) set to autopay.

You can’t speed up time, but you can avoid resetting the clock. If you have a 7-year-old credit card, keep it. Even if you rarely use it, that seasoned account boosts your average age.

For building history faster: Become an authorized user on a parent’s or spouse’s long-standing, well-managed account. You inherit the age and payment history of that card, potentially adding years to your profile instantly.

Credit Mix (10% of Your Score)

Lenders like seeing that you can manage different credit types: revolving (credit cards), installment (auto loans, personal loans, mortgages), and open (charge cards that must be paid in full monthly).

You don’t need to take out a loan just for credit mix, but if you’re choosing between financing a car or paying cash, financing strategically can help—especially if you’re young with a thin credit file. A $15,000 auto loan at 5% over 60 months adds installment diversity while building payment history.

Exploring our snowball vs avalanche debt payoff strategies helps you manage multiple account types optimally while improving your credit mix organically.

New Credit Inquiries (10% of Your Score)

Each hard inquiry typically drops your score 3-5 points temporarily. The impact fades after 6 months and disappears completely after 12 months.

Rate shopping exception: Multiple mortgage or auto loan inquiries within 14-45 days count as one inquiry. This lets you shop for the best rate without penalty. Credit card applications don’t get this benefit—each is a separate inquiry.

Strategy: Limit applications to 2-3 per year maximum unless you’re rate shopping for a major purchase. Space them at least 3-4 months apart when possible.

The 12-18 Month Reality Check

Building from 650 to 740 typically requires 12-18 months of consistent positive behavior. From 680 to 760? Usually 14-20 months. There are no legal shortcuts, and anyone promising instant fixes is selling credit repair scams.

Real case: A 32-year-old client started at 662 with $12,000 in credit card debt. Using our credit card debt escape strategies, she paid down to $3,500 (75% utilization to 22%), became an authorized user on her mother’s 15-year-old account, and made 18 consecutive on-time payments. Final score after 18 months: 743—enough to qualify for a mortgage rate 0.6% lower than her starting profile, saving $52,000 over 30 years.

That’s the power of systematic credit building. It takes patience, but the financial rewards compound for decades.

Credit Score Myths & Facts (2026 Edition)

Misinformation about credit scores costs consumers thousands in missed opportunities and poor decisions. Let’s destroy the most persistent myths with data-backed facts.

❌ Myth 1: “Checking Your Credit Score Hurts It”

✅ Fact: Checking your own score is a soft inquiry that has zero impact. Only hard inquiries from lenders reviewing your application for new credit affect your score. You should check your score monthly—it’s free through most credit card issuers now, and vigilance helps you catch errors or fraud early.

The Consumer Financial Protection Bureau encourages consumers to review their reports regularly from all three bureaus (Equifax, Experian, TransUnion) at AnnualCreditReport.com.

❌ Myth 2: “Carrying a Credit Card Balance Improves Your Score”

✅ Fact: This costs people millions in unnecessary interest annually. Paying your full statement balance every month is optimal. You don’t need to carry a balance or pay interest to build credit—you just need the card to report a balance above $0 before you pay it off.

Strategy: Let a small charge post ($5-20), let it appear on your statement, then pay in full before the due date. You build credit without paying a cent in interest.

❌ Myth 3: “Closing Old Credit Cards Helps Your Score”

✅ Fact: Closing cards typically hurts your score in two ways. First, it reduces your total available credit, increasing your utilization ratio. Second, eventually those closed accounts age off your report, reducing your average account age.

Keep old cards active with small recurring charges set to autopay. Even a card you haven’t used in years contributes to your available credit and history length.

❌ Myth 4: “You Need to Be in Debt to Have Good Credit”

✅ Fact: You need to use credit, not carry debt. Big difference. Charging $500/month and paying it off in full every month builds the same payment history as carrying a $5,000 balance and making minimum payments—except you save hundreds in interest and maintain lower utilization.

Debt and credit usage aren’t synonymous. Smart credit users leverage the system without paying the debt tax.

❌ Myth 5: “Income Affects Your Credit Score”

✅ Fact: FICO and VantageScore don’t factor income at all. A person making $40,000 and someone making $400,000 can have identical 780 scores if they manage credit identically. Income matters for loan approval (debt-to-income ratio), but it’s invisible to scoring models.

This is why understanding credit fundamentals matters more than your paycheck size. A modest earner with excellent credit habits often qualifies for better rates than a high earner with poor credit management.

These myths persist because credit scoring feels opaque. But the truth is refreshingly simple: pay on time, keep utilization low, maintain old accounts, diversify your credit types, and limit new applications. Master these five factors and your score takes care of itself.

Frequently Asked Questions About Credit Scores

1. Is 700 a good credit score in 2026?

Yes, 700 is solidly in the “good” credit score range (670-739). You’ll qualify for most conventional mortgages, decent auto loan rates around 6-8%, and mid-tier rewards credit cards. However, you’re leaving money on the table—increasing to 740+ typically saves $30,000-50,000 over a 30-year mortgage through lower interest rates.

2. What is considered an excellent credit score?

Excellent credit starts at 800 on the FICO scale. Only 23% of Americans reach this tier, where you command the absolute best rates and terms. The difference between 740 and 800 is marginal in practical terms—both receive top-tier pricing from most lenders.

3. How long does it take to build a good credit score from scratch?

Building to 670-700 from zero typically takes 6-12 months with a secured credit card or credit-builder loan and responsible usage. Reaching 740+ usually requires 18-24 months because you need sufficient payment history length. There are no legal shortcuts to accelerate FICO’s time-based factors.

4. Can I get a mortgage with a 650 credit score?

Yes, but it’s expensive. FHA loans accept 580+, and conventional loans start at 620. At 650, expect interest rates 1.0-1.5% higher than borrowers with 740+ scores. On a $300,000 loan, that’s roughly $85,000 more in total interest over 30 years.

5. What’s the fastest way to raise my credit score 100 points?

Pay down credit card balances to under 10% utilization, dispute any errors on your credit reports, and become an authorized user on someone’s well-established account. Real timeline: 4-8 months for a 100-point jump from actions within your control, assuming you’re starting from a damaged profile with fixable issues.

6. Do I have different credit scores from different bureaus?

Yes. You have three credit reports (Equifax, Experian, TransUnion), and not all creditors report to all three bureaus. Your scores can vary by 10-30 points between bureaus. Mortgage lenders typically pull all three and use the middle score for qualification decisions.

7. What credit score do you start with?

You don’t start with any score. You become “scoreable” after about 6 months of credit activity on at least one account. Your initial score depends on how you’ve managed that first account—typically landing in the 620-680 range if handled responsibly.

8. How often should I check my credit score?

Monthly monitoring is ideal and free through most credit card issuers. This helps you catch fraud quickly and track progress if you’re actively building credit. Check your full credit reports from all three bureaus at least annually at AnnualCreditReport.com to review for errors.

9. Can paying off collections improve my credit score?

Sometimes. Newer scoring models (FICO 9, VantageScore 3.0+) ignore paid collections, so settling them could boost scores. Older models still count them. The collection stays on your report for 7 years regardless, but showing “$0 balance” is better than showing an outstanding amount when lenders manually review your report.

10. What’s the difference between FICO and VantageScore?

FICO is used by 90% of lenders for lending decisions and weighs payment history at 35%. VantageScore (used by Credit Karma, free monitoring apps) is primarily a consumer tool, weighing payment history at 40%. Scores can differ by 20-40 points between models due to different calculation methods.

11. Does closing a credit card hurt my score?

Usually yes, in two ways: it reduces your total available credit (increasing utilization), and eventually the closed account ages off your report (reducing average account age). Keep old cards active with small recurring charges instead of closing them, unless there’s an unavoidable annual fee issue.

Important Disclaimer

Educational Information Only: The information provided in this article is for educational and informational purposes only and should not be construed as financial advice. Finance Authority Hub is not a licensed financial advisor, credit counselor, or investment professional.

Consult Qualified Professionals: Before making any financial decisions, including actions related to credit management, loan applications, or debt repayment strategies, you should consult with a licensed financial advisor, certified credit counselor, or other qualified professional who can assess your individual circumstances.

Data Accuracy and Timeliness: While we strive to provide accurate and up-to-date information as of January 2026, credit scoring models, lender requirements, interest rates, and financial regulations change frequently. The data presented here is sourced from publicly available government resources and financial institutions, but individual results may vary significantly.

No Guaranteed Results: Credit score improvement timelines, approval odds, and financial outcomes described in this article are based on typical scenarios and historical data. Your individual results may differ based on your unique credit history, financial situation, geographic location, and lender-specific criteria. Past performance or typical results do not guarantee future outcomes.

Variable Lender Requirements: Credit score thresholds, interest rates, approval criteria, and product offerings vary by lender and change regularly. The specific numbers and ranges provided are representative averages and should not be interpreted as guarantees of approval or specific rate offerings.

Independent Verification Required: Always verify current rates, terms, requirements, and product details directly with lenders before making application decisions. Do not rely solely on the general information provided here for time-sensitive financial decisions.

No Liability: Finance Authority Hub, its authors, and contributors assume no liability for financial decisions made based on information in this article. You are solely responsible for evaluating your financial circumstances and making informed decisions appropriate to your situation.

Credit Inquiries and Applications: Applying for credit products results in hard inquiries that may temporarily impact your credit score. Consider the implications before submitting applications based on information in this article.

For personalized guidance, visit ConsumerFinance.gov or contact a certified financial professional in your area.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.