Mortgage Amortization Explained: How Every Payment Breaks Down in 2026

Every mortgage payment is secretly split between interest and principal. Learn how mortgage amortization works and how to beat it with 5 expert money-saving strategies.

In This Article

On a $350,000 mortgage at 6.5% interest over 30 years, you will pay $442,257 in total — meaning $92,257 goes purely to interest. Understanding mortgage amortization is the single most powerful tool to cut that number dramatically. This guide breaks down exactly how every dollar of your payment works, month by month.

What Is Mortgage Amortization? The Simple Truth

Mortgage amortization is the structured process of paying off your home loan through fixed monthly payments over a set term. Each payment is split into two parts:

- Principal — the portion that reduces your actual loan balance

- Interest — the cost the lender charges you for borrowing

The critical detail most borrowers never realize: your lender front-loads interest. In the early years, the vast majority of each payment covers interest — almost nothing reduces your balance. This is by mathematical design, not by accident.

The Amortization Formula (Simplified)

Lenders calculate your fixed monthly payment using this formula:

M = P × [r(1+r)^n] / [(1+r)^n – 1]

Where:

- P = Loan principal

- r = Monthly interest rate (annual rate ÷ 12)

- n = Total number of payments

You don’t need to run this manually. Use our Mortgage Calculator to model your exact amortization in under 60 seconds.

Real Example: Month 1 Breakdown on a $350,000 Loan

| Loan Details | Value |

|---|---|

| Loan Amount | $350,000 |

| Interest Rate | 6.5% |

| Loan Term | 30 years |

| Monthly Payment (P&I) | $2,212.24 |

| Month 1 — Interest Paid | $1,895.83 |

| Month 1 — Principal Paid | $316.41 |

| Remaining Balance | $349,683.59 |

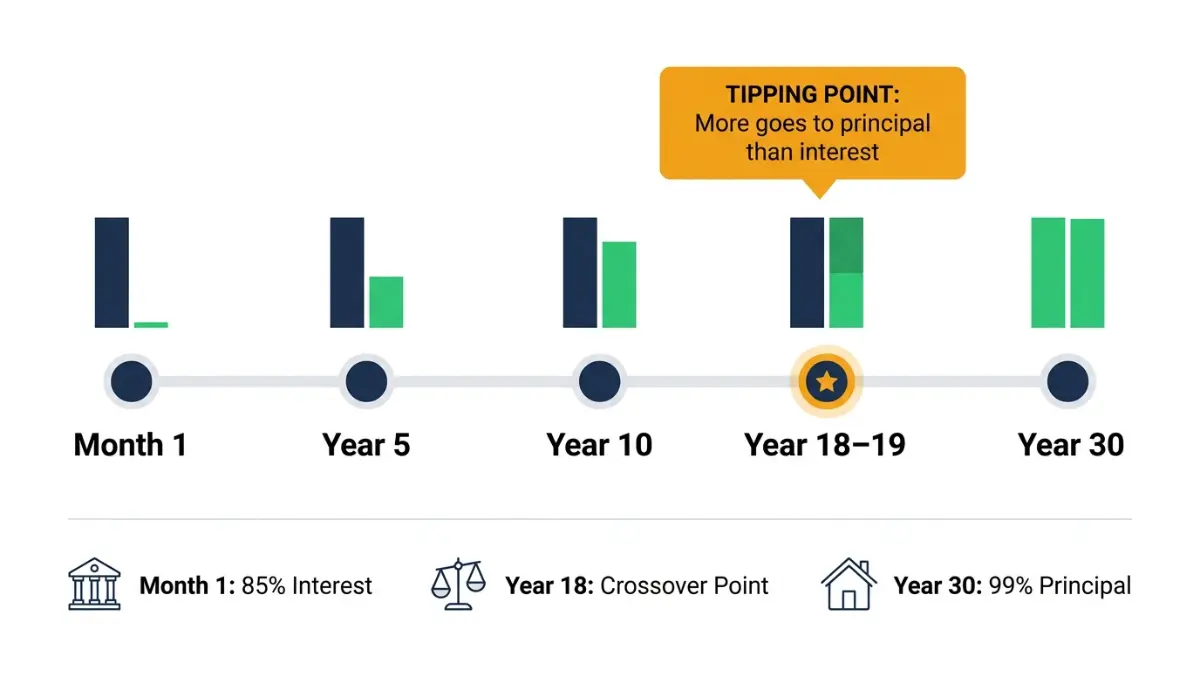

What This Means For You: After your very first mortgage payment of $2,212, only $316 actually reduced what you owe. The bank collected $1,895 in interest — 85.7% of your payment. This is mortgage amortization working exactly as designed. Knowing this is your first step to fighting back.

According to the Consumer Financial Protection Bureau (CFPB), in the early years of a mortgage the majority of each monthly payment goes toward interest, not principal — and this ratio only shifts meaningfully over time.

Your Mortgage Amortization Schedule — Decoded

A mortgage amortization schedule is a complete table listing every single payment across your loan term. It shows, payment by payment:

- How much goes to interest

- How much reduces your principal balance

- Your remaining loan balance after each payment

Sample Amortization Schedule — $350,000 @ 6.5%, 30-Year Fixed

| Payment | Monthly Payment | Interest Paid | Principal Paid | Remaining Balance |

|---|---|---|---|---|

| Month 1 | $2,212.24 | $1,895.83 | $316.41 | $349,683.59 |

| Month 60 (Year 5) | $2,212.24 | $1,788.11 | $424.13 | $331,426.08 |

| Month 120 (Year 10) | $2,212.24 | $1,660.54 | $551.70 | $309,647.85 |

| Month 240 (Year 20) | $2,212.24 | $1,282.09 | $930.15 | $237,958.98 |

| Month 348 (Year 29) | $2,212.24 | $142.70 | $2,069.54 | $24,516.83 |

Key observation: After 10 full years of payments (120 months), your remaining balance is still $309,647 — you’ve only paid off $40,352 of principal despite paying $265,468 in total. That’s the reality of front-loaded amortization.

🔑 The Amortization Tipping Point (What Competitors Never Tell You)

On a standard 30-year fixed mortgage, the month where more of your payment goes to principal than interest doesn’t arrive until Year 18–19. That’s 216–228 payments before your money starts working harder for you than for your lender.

- Fixed-rate mortgages: The amortization schedule is locked from day one. Every payment is predictable.

- Adjustable-rate mortgages (ARMs): When the rate adjusts, the lender recalculates your entire amortization schedule based on your current balance, new rate, and remaining term. Your payment can shift significantly.

Explore how different loan terms affect your schedule using our Amortization Calculator — enter any loan amount, rate, and term to see your full breakdown instantly.

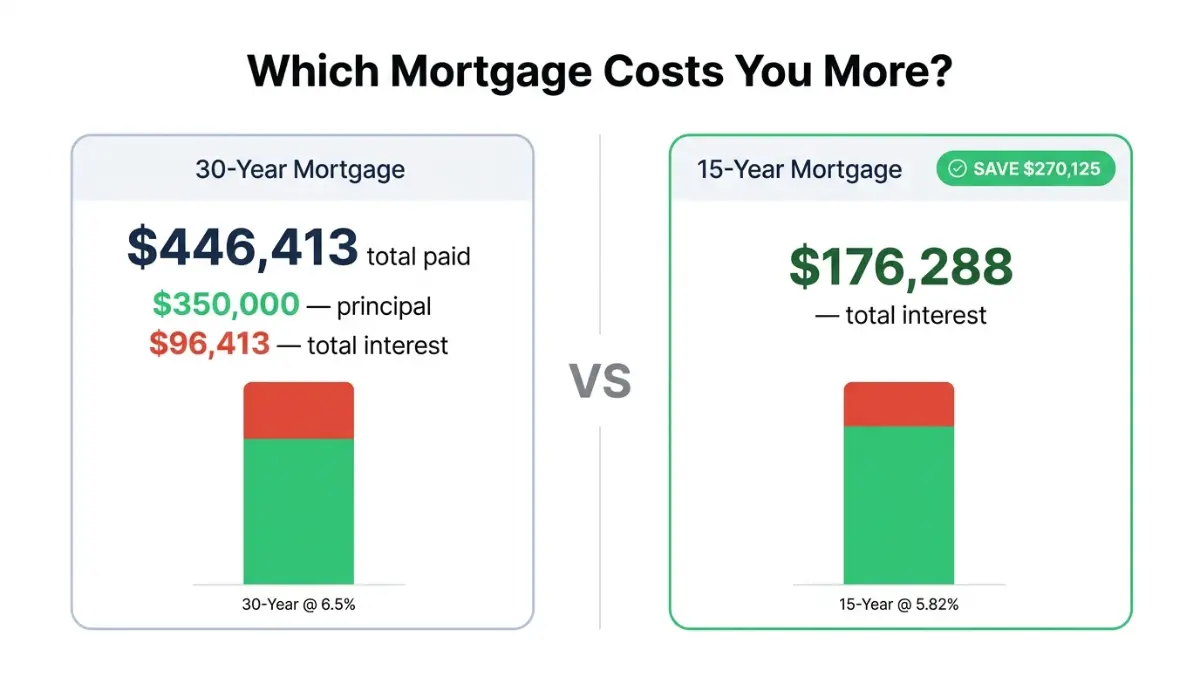

15-Year vs. 30-Year Mortgage — The Real Numbers (2026 Rates)

The loan term you choose is the single biggest lever controlling your mortgage amortization. Here’s the real-dollar comparison using current 2026 average rates.

Side-by-Side Comparison: $350,000 Mortgage

| 30-Year Fixed (6.5%) | 15-Year Fixed (5.82%) | |

|---|---|---|

| Monthly Payment (P&I) | $2,212 | $2,924 |

| Total Interest Paid | $446,413 | $176,288 |

| Interest Savings | — | $270,125 |

| Balance at Year 5 | $331,426 | $264,973 |

| Balance at Year 10 | $309,648 | $160,291 |

| Payoff Date | 2055 | 2040 |

The 15-year mortgage costs $712 more per month — but saves over $270,000 in total interest and builds equity dramatically faster. See our dedicated 15 vs 30 Year Mortgage Comparison article for a full analysis.

The Hybrid Strategy Most Buyers Miss

You don’t have to lock yourself into a 15-year payment. Take a 30-year loan, but voluntarily pay the 15-year payment amount when your budget allows. This gives you:

- Flexibility — you can drop back to the lower 30-year payment in tight months

- Savings — you shave years off your loan and save tens of thousands in interest

- No penalties — on most conventional loans, extra principal payments are free

Use our Mortgage Refinance Calculator to model whether refinancing to a shorter term makes sense for your situation right now.

What This Means For You: The difference between a 15-year and 30-year mortgage isn’t just about monthly cash flow. On a $350,000 loan, choosing the 15-year term is worth an extra $270,000 staying in your pocket. If that monthly difference is manageable, the 15-year amortization schedule wins by a landslide.

5 Expert Strategies to Beat Mortgage Amortization and Save Thousands

Understanding how your mortgage amortization schedule works gives you the power to manipulate it in your favor. Here are five proven strategies — with real numbers.

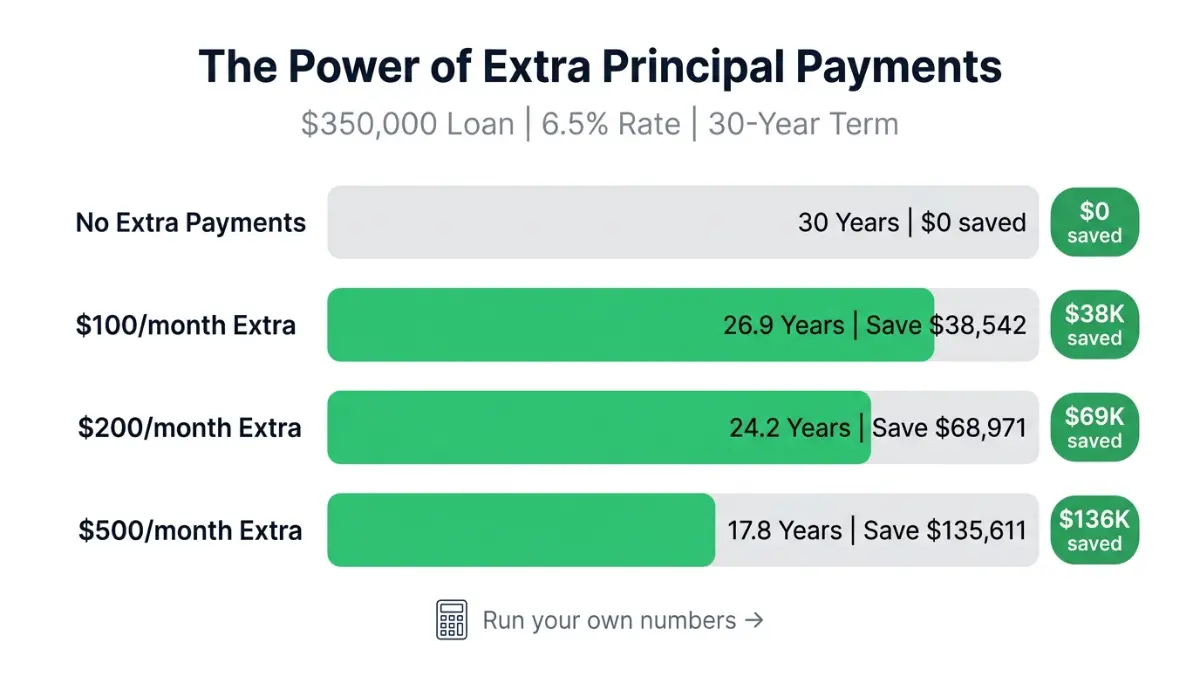

1. Make Extra Principal Payments

Every dollar you pay above your minimum goes 100% to principal, which directly reduces future interest charges. The compounding effect is dramatic.

Real Savings on a $350,000 Loan @ 6.5%, 30-Year:

| Extra Monthly Payment | Years Saved | Total Interest Saved |

|---|---|---|

| $100/month extra | 3.1 years | $38,542 |

| $200/month extra | 5.8 years | $68,971 |

| $300/month extra | 8.1 years | $93,204 |

| $500/month extra | 12.2 years | $135,611 |

Important: Extra payments reduce your balance and future interest — but they do not lower your required monthly minimum. As the CFPB confirms, paying down your principal directly reduces how much interest accrues each subsequent month.

2. Switch to Biweekly Mortgage Payments

Instead of 12 monthly payments per year, make a half-payment every two weeks. This produces 26 half-payments = 13 full payments annually — one free extra payment per year, automatically.

- On a $350,000 loan at 6.5%, this saves approximately 4–5 years off a 30-year term

- Estimated total interest savings: $58,000–$65,000

- Ask your servicer to set up a biweekly payment plan — many offer this free of charge

3. Refinance Strategically (Avoid the Clock Reset Trap)

Refinancing into a lower rate can save money — but it also resets your amortization schedule to year one, meaning your early payments are once again heavily weighted toward interest.

Refinancing makes sense when:

- Your new rate is at least 0.75%–1% lower than your current rate

- You plan to stay in the home long enough to recoup closing costs (typically 2–4 years)

- You refinance into the same or shorter remaining term, not a fresh 30-year

Check current rates and model your break-even timeline with our Mortgage Refinance Calculator before making any decision. For deeper insight, read our full guide on APR vs Interest Rate to understand the true cost of any refinance offer.

4. Request a Mortgage Recast

A mortgage recast (also called re-amortization) lets you make a large lump-sum principal payment, then have your lender recalculate your monthly payment based on the reduced balance — at your same interest rate and remaining term.

Why this beats most refinances:

- No credit check required

- No income verification

- Closing cost: just $150–$300 (vs. $3,000–$6,000 for a refinance)

- Your rate stays the same

Best use case: You sold a previous home, received an inheritance, or earned a large bonus, and you want to permanently lower your monthly payment.

Note: Not all loan types qualify. FHA and VA loans typically do not allow recasting. Confirm eligibility with your servicer first.

5. Choose Your Loan Term Wisely From Day One

The most powerful amortization decision happens before you even close. Choosing a 20-year term instead of 30 on a $350,000 loan at 6.5% saves approximately $155,000 in interest with a payment that’s only about $400/month higher.

Use our Home Affordability Calculator to find the loan amount and term that fits your budget before you start shopping.

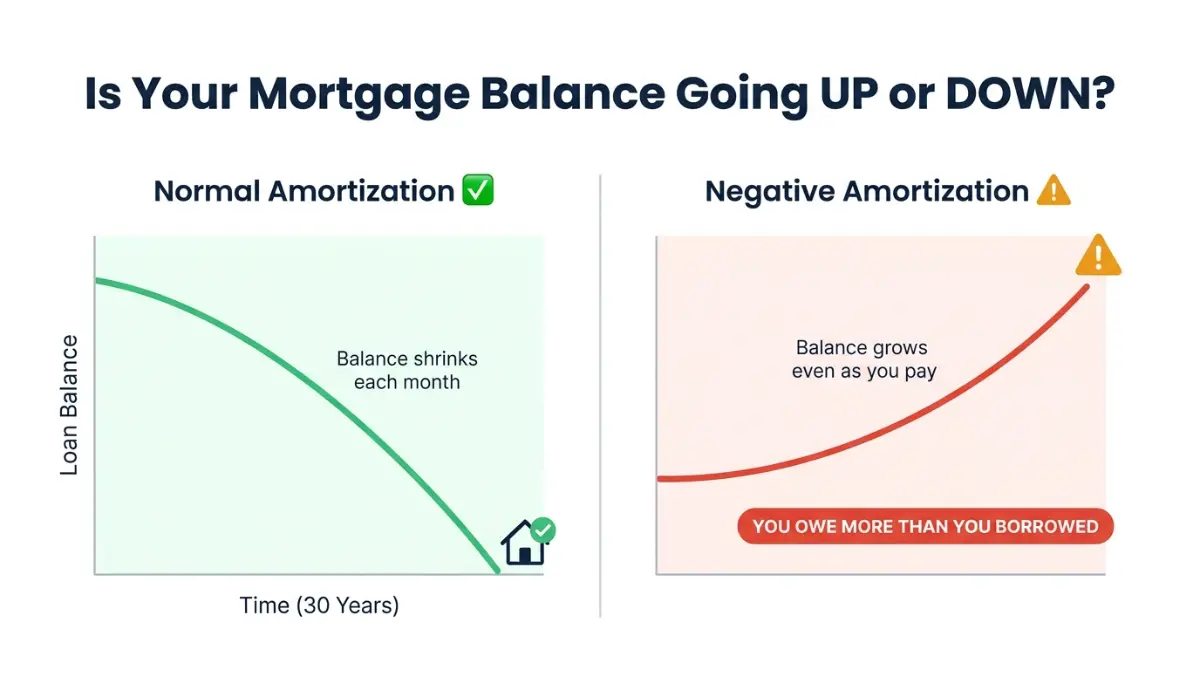

Negative Amortization, ARMs, and What Your Lender Won’t Volunteer

⚠️ Negative Amortization — The Danger Zone

Negative amortization occurs when your monthly payment is less than the interest due that month. Instead of your balance going down, it goes up.

- Your unpaid interest is added to your principal

- Next month’s interest is calculated on a now-larger balance

- Over time, you can owe significantly more than you originally borrowed

This most commonly occurs with:

- Option ARMs that allow minimum payments below the interest threshold

- Interest-only loans in their early phase

- Certain deferred payment programs

As the Consumer Financial Protection Bureau explicitly warns, negative amortization means that even when you pay, the amount you owe can still go up. In 2026’s rate environment, borrowers with older payment-option ARMs face particular risk.

Adjustable-Rate Mortgages and Your Amortization Schedule

With an ARM, your initial amortization schedule is only valid during the fixed-rate period. Once the rate adjusts:

- Your lender recalculates the full schedule using the new rate, remaining balance, and remaining term

- A rate increase can cause significant payment shock

- Your amortization tipping point can shift dramatically

Example: A 5/1 ARM at 5.5% fixed for 5 years may adjust to 7.5% at Year 6. On $310,000 remaining balance, your payment could jump by $350–$400/month overnight, and your amortization schedule resets toward interest again.

If you have an ARM and rates have shifted, model your new payment with our Mortgage Rate Calculator immediately.

Interest-Only Loans — A False Economy

Interest-only mortgages appear to save money short-term because your payment is lower. The reality: you are not amortizing at all during the interest-only period. Your balance stays exactly where it started. Once the principal repayment phase begins, your monthly payment can increase sharply since the same principal must now be paid over a shorter remaining term.

Expert Verdict — Is Your Amortization Schedule Working Hard Enough?

Understanding your mortgage amortization schedule is not a one-time exercise. It’s an active financial monitoring tool.

3-Point Expert Amortization Audit (Run This Right Now)

✅ Check 1: Where Are You on the Tipping Point Timeline? Pull your latest mortgage statement. If you’re before Year 18 on a 30-year loan, more than half of every payment still goes to interest. Any extra principal payment you make today is disproportionately powerful.

✅ Check 2: Have You Modeled Biweekly Payments? If your servicer allows biweekly payments, enabling this takes five minutes and could save you 4–5 years of payments worth tens of thousands of dollars. This is one of the highest-ROI financial moves available to any homeowner.

✅ Check 3: Is Your Interest Rate Above Today’s Market? If your current mortgage rate is 1% or more above prevailing 2026 rates, run a refinance calculation immediately. Check current home loan interest rates on our site and model your break-even with the Refinance Calculator.

What This Means For You (Final Verdict)

The mortgage amortization schedule is not your enemy — but it is your lender’s best friend if you ignore it. Every month you pay without understanding your breakdown is a month you’re likely leaving money on the table.

Run your full mortgage amortization schedule right now using our Mortgage Calculator — it takes 60 seconds and shows you exactly where every dollar goes for the life of your loan.

Reviewed by Laura M. Bennett, CFP® | financeauthorityhub.com Expert Finance Panel

Frequently Asked Questions About Mortgage Amortization

Q1: What is mortgage amortization in simple terms?

Mortgage amortization is the process of paying off your home loan through fixed monthly payments over time. Each payment covers both interest and principal, with the interest share gradually shrinking as your balance decreases.

Q2: How is an amortization schedule calculated?

Lenders use the formula M = P × [r(1+r)^n] / [(1+r)^n – 1]. Your loan amount, interest rate, and term determine your fixed monthly payment, and the principal/interest split is recalculated each month based on your remaining balance.

Q3: What is the mortgage amortization tipping point?

On a standard 30-year fixed mortgage, the tipping point — when more of your payment goes to principal than interest — typically arrives around Year 18 or 19, roughly payment 216–228.

Q4: Does paying extra principal change my amortization schedule?

Extra principal payments reduce your remaining balance, which lowers future interest charges and shortens your loan term. However, your required monthly payment does not automatically decrease unless you formally recast the loan.

Q5: What’s the difference between a 15-year and 30-year amortization?

A 15-year mortgage builds equity twice as fast and pays roughly 60% less total interest. On a $350,000 loan, the 30-year option costs over $270,000 more in interest than the 15-year option at current rates.

Q6: What is negative amortization?

Negative amortization occurs when your monthly payment is less than the interest owed, causing your loan balance to grow instead of shrink. It most commonly occurs with option ARMs and interest-only loans.

Q7: Can I get my amortization schedule from my lender?

Yes. Your lender is required to provide an amortization schedule at closing. You can also request an updated one at any time, or generate it yourself using any mortgage amortization calculator.

Q8: Does refinancing reset my amortization schedule?

Yes. Refinancing creates a brand-new loan with a fresh amortization schedule starting at payment one. This means your early payments will again be heavily weighted toward interest, even on a lower rate.

Q9: What is a mortgage recast and how does it affect amortization?

A mortgage recast is when you make a large lump-sum principal payment and request your lender to recalculate your monthly payment on the reduced balance. Unlike refinancing, a recast keeps your same rate and term but lowers your monthly payment — typically for a fee of just $150–$300.

Q10: How do biweekly payments affect amortization?

Biweekly payments result in 13 full payments per year instead of 12. This extra annual payment accelerates principal paydown, can shorten a 30-year mortgage by 4–5 years, and saves tens of thousands in interest over the life of the loan.

Q11: Can I pay off my mortgage early without penalties?

Most conventional mortgages have no prepayment penalty. You can make extra principal payments at any time. Always confirm with your servicer that extra payments are being applied to principal, not held for future monthly payments.

⚠️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, mortgage, or legal advice. Mortgage amortization calculations shown are estimates based on fixed-rate assumptions. Individual loan terms vary. Please consult a licensed mortgage professional or certified financial advisor before making any borrowing or refinancing decisions.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.