What Credit Score Do You Need toBuy a House in 2026?

Want to buy a house in 2026? Here’s the exact credit score you need by loan type — plus the 2026 FHFA rule change that unlocks 5 million new buyers.

In This Article

The short answer: You need a minimum credit score of 500 for an FHA loan (with 10% down), 580 for FHA with 3.5% down, and 620 for most conventional loans. VA and USDA loans have no official minimum. But in 2026, the rules just changed — and millions of buyers who were previously rejected may now qualify. Here’s everything you need to know.

The 2026 Credit Score Bombshell Most Buyers Don’t Know About

The mortgage world just shifted — and most homebuyers haven’t heard about it.

In July 2025, the Federal Housing Finance Agency (FHFA) officially approved VantageScore 4.0 for use on all Fannie Mae and Freddie Mac loans. These two agencies back over 56% of all U.S. home loans. For decades, only the Classic FICO score was accepted. That monopoly is now over.

What this means for you:

- Up to 5 million new buyers could now qualify for a mortgage who previously couldn’t

- Lenders can now choose between Classic FICO or VantageScore 4.0

- Rent, utility, and phone payment history now counts toward your credit profile

- “Credit invisible” borrowers — young buyers, immigrants, veterans with thin files — now have a real path to homeownership

This is the biggest shift in mortgage credit scoring since these models were invented. If you’ve been told your score isn’t good enough, check again.

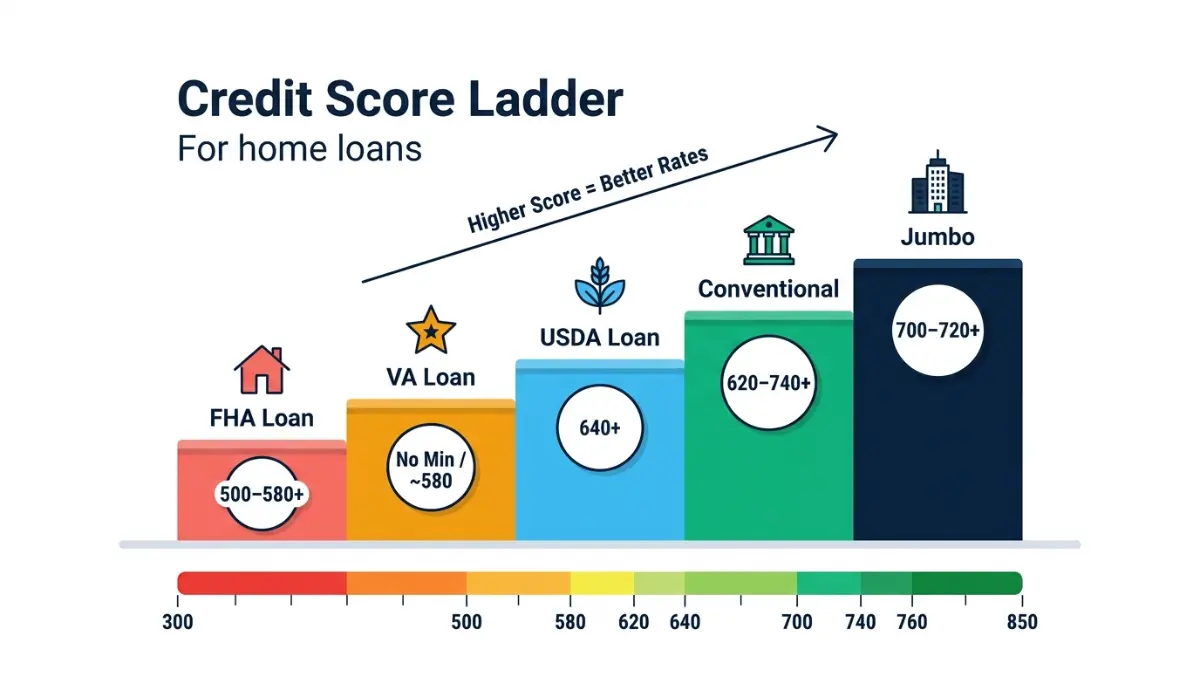

Quick Reference: Minimum Credit Score by Loan Type (2026)

| Loan Type | Minimum Score | Down Payment | Best For |

|---|---|---|---|

| FHA Loan | 500 (10% down) / 580 (3.5% down) | 3.5%–10% | First-time buyers, lower scores |

| Conventional Loan | 620 (practical minimum) | 3%–20% | Good credit, stable income |

| VA Loan | No official minimum (~580 lender typical) | 0% | Veterans, active military |

| USDA Loan | 640 typical | 0% | Rural/suburban buyers |

| Jumbo Loan | 700–720+ | 10%–20% | Loans above $806,500 |

Use our home affordability calculator to see what price range you can realistically target based on your current credit score and income.

Minimum Credit Score by Mortgage Type — Full 2026 Breakdown

Your credit score to buy a house depends entirely on the loan program. Here’s a surgical breakdown of each option.

FHA Loans — Best for Scores 500–619

FHA loans are government-backed and designed for buyers with lower credit scores.

- 580 or above → 3.5% down payment required

- 500–579 → 10% down payment required

- Below 500 → Most lenders will not approve, even with FHA backing

- You’ll also pay mortgage insurance premium (MIP): 1.75% upfront + 0.40%–0.85% annually

Key 2026 update: The Consumer Financial Protection Bureau (CFPB) notes that FHA loans remain the most accessible path for borrowers with fair credit scores, especially as lenders begin incorporating alternative credit data like rent history.

Conventional Loans — Best for Scores 620+

Conventional loans are the most common type, backed by Fannie Mae and Freddie Mac.

- 620 → Practical minimum for most lenders

- 740+ → Best rates and lowest PMI costs

- Fannie Mae/Freddie Mac update: Starting in 2026, lenders can now use VantageScore 4.0 — meaning your rent and utility history may now boost your conventional loan eligibility

No PMI is required with a 20% down payment. Scores below 740 may trigger PMI costs of 0.5%–1.5% annually on the loan balance.

VA Loans — Best for Veterans

VA loans are guaranteed by the U.S. Department of Veterans Affairs and are among the best home loan products available.

- No official minimum credit score set by the VA

- Most lenders set an internal minimum of 580–620

- Some lenders accept 500+ with strong compensating factors and clean payment history in the prior 12 months

- Zero down payment required — a major advantage

- No private mortgage insurance (PMI) ever

If you’re a veteran, review our types of home loans guide to compare VA loans side by side with other programs.

USDA Loans — Best for Rural/Suburban Buyers

USDA loans are backed by the U.S. Department of Agriculture for buyers in eligible rural and suburban areas.

- 640 is the typical minimum for automated underwriting approval

- Manual underwriting may allow lower scores with compensating factors

- Zero down payment required

- Household income limits apply — varies by county

Jumbo Loans — For High-Value Purchases

Jumbo loans exceed the 2026 conforming loan limit of $806,500 for most counties.

- 700–720 minimum score is standard

- Some lenders require 740+ for LTV ratios above 80%

- Higher reserves and income documentation required

- No government backing — lenders assume full risk

How Your Credit Score Affects Your Mortgage Rate and Total Cost

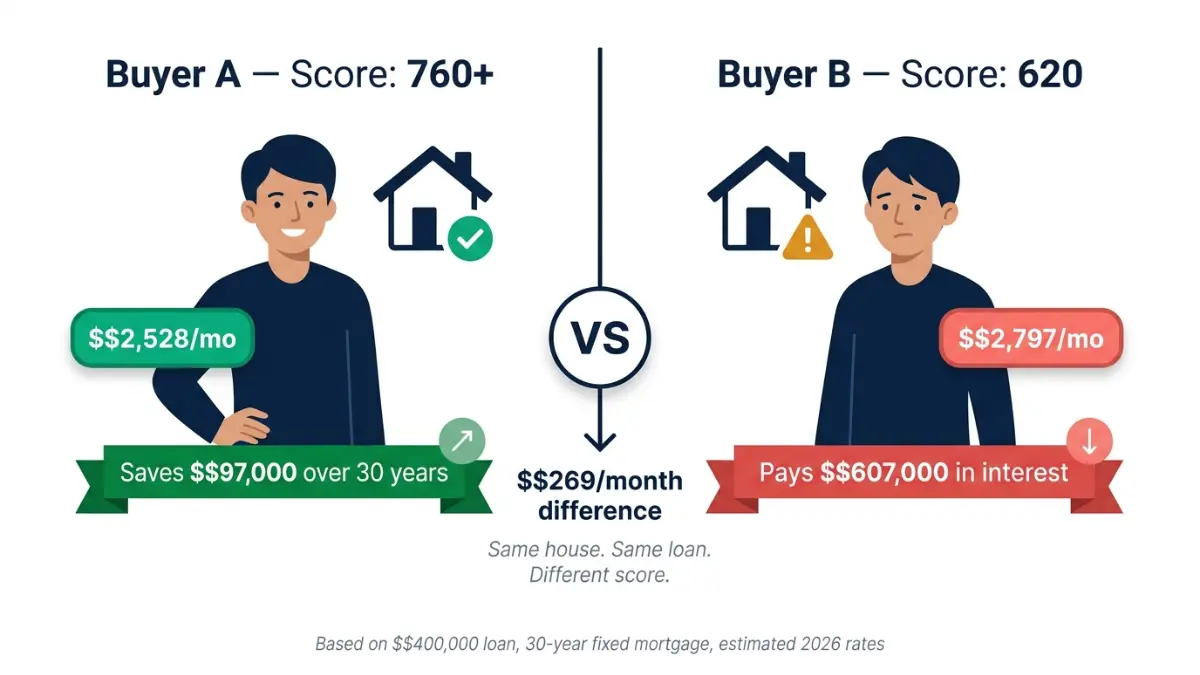

A credit score isn’t just a number. It’s a dollar amount — and the difference can be staggering.

According to the CFPB’s mortgage rate explorer, even a modest improvement in your credit score can translate into tens of thousands of dollars in savings over a 30-year loan.

Real Cost Comparison: $400,000 Home, 30-Year Fixed Loan (2026)

| Credit Score | Est. Rate | Monthly Payment | Total Interest Paid | Total Loan Cost |

|---|---|---|---|---|

| 760–850 | ~6.50% | ~$2,528 | ~$510,000 | ~$910,000 |

| 700–759 | ~6.75% | ~$2,594 | ~$534,000 | ~$934,000 |

| 660–699 | ~7.10% | ~$2,690 | ~$568,000 | ~$968,000 |

| 620–659 | ~7.50% | ~$2,797 | ~$607,000 | ~$1,007,000 |

What This Means For You: A buyer with a 760 score vs. a 620 score saves approximately $269/month and nearly $97,000 in total interest on the same $400,000 loan. That’s enough to fully fund a retirement account or pay for a child’s college education.

Run your exact numbers with our mortgage calculator to see what your monthly payment looks like at your current credit score.

How Credit Score Affects PMI

Private mortgage insurance (PMI) is required on conventional loans with less than 20% down. Your credit score directly affects PMI costs:

- 760+ → PMI approximately 0.2%–0.5% annually

- 700–759 → PMI approximately 0.5%–0.8% annually

- 620–699 → PMI approximately 0.9%–1.5% annually

On a $400,000 loan with 5% down, the difference between a 760 score and a 620 score in PMI alone can be $200–$400 per month — even before accounting for the higher interest rate.

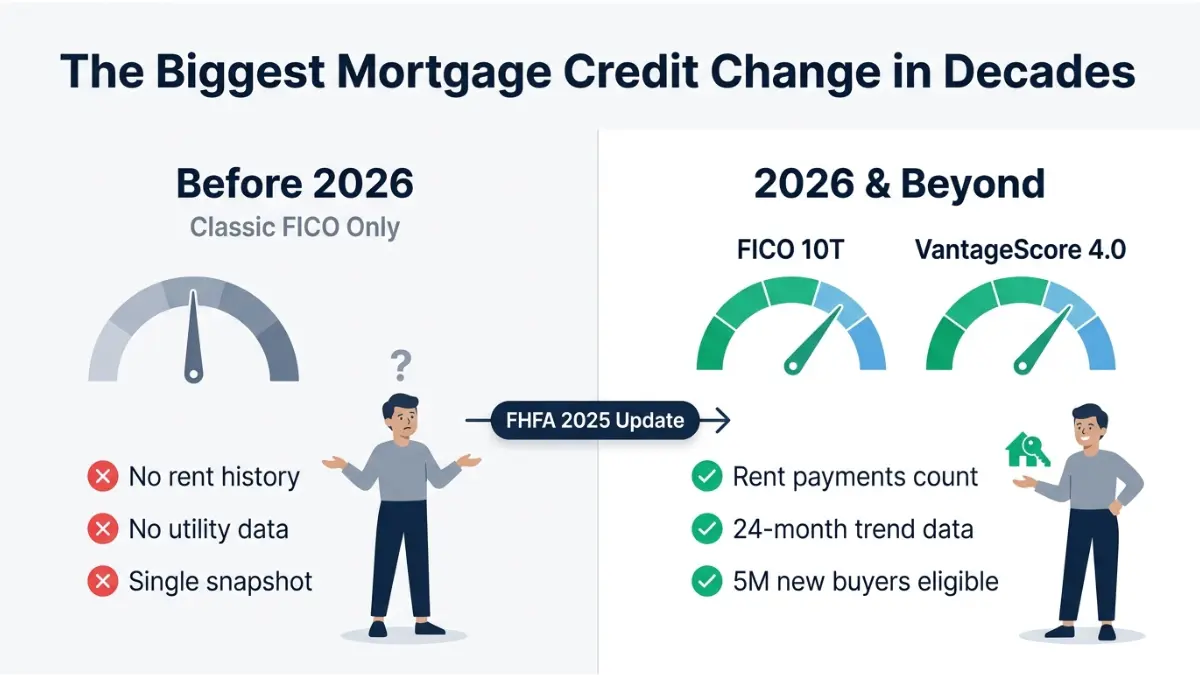

The 2026 Credit Scoring Revolution — VantageScore 4.0, FICO 10T, and What Changed

This is the section your competitors don’t cover. And it may be the most important financial news for homebuyers in a decade.

Old System vs. New System (2026)

| Classic FICO (Old) | VantageScore 4.0 / FICO 10T (New — 2026) |

|---|---|

| Single-day snapshot of your credit | 24-month trended credit behavior |

| No rent or utility payment history | Rent, utilities, phone payments count |

| Millions of “credit invisible” buyers excluded | 33 million more Americans now scoreable |

| Single model mandatory for all lenders | Lender choice: Classic FICO or VantageScore 4.0 |

| Static utilization ratio | Rewards consistent debt paydown over time |

Why Trended Data Is a Game-Changer

Under the old FICO model, if your credit card balance was $5,000 last month and $5,000 this month, you looked the same to a lender. Under VantageScore 4.0 and FICO 10T, if your balance was $9,000 six months ago and is now $5,000, you look like a responsible borrower trending in the right direction. That difference in perception can translate directly into a better rate.

Who benefits most from 2026’s new scoring models:

- First-time buyers with limited credit history

- Immigrants and newcomers with thin credit files

- Veterans transitioning out of service

- Young adults who pay rent on time but have minimal credit accounts

- Anyone who has been consistently paying down debt

The FHFA has confirmed that lenders now have immediate authorization to use VantageScore 4.0 for loans sold to Fannie Mae and Freddie Mac. FICO 10T implementation is progressing and expected to follow.

To understand how your credit score compares right now, try our credit score calculator for a clearer picture of your profile.

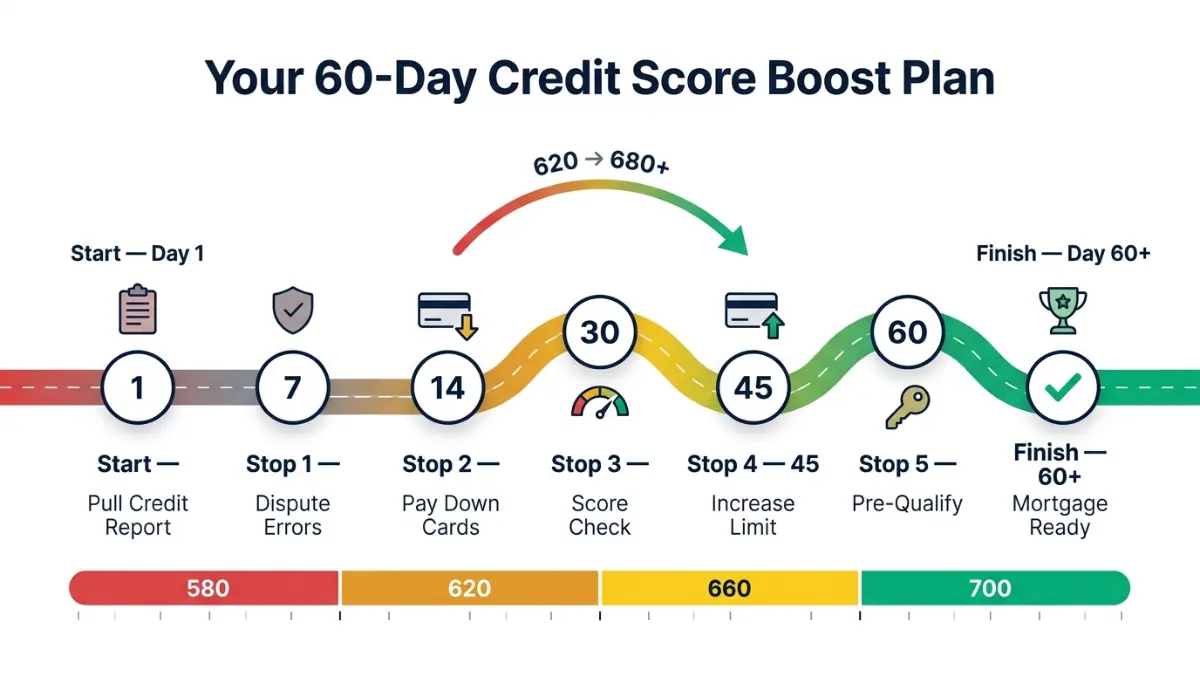

Your 60-Day Credit Score Action Plan Before Buying a House

Most buyers can improve their credit score for a mortgage by 20–80 points in 60–90 days with focused action. Here’s the exact playbook.

Month 1 Action Plan (Days 1–30)

Step 1: Pull Your Free Credit Report Get your free reports from all three bureaus at AnnualCreditReport.com — the only official federally authorized site. Check for errors, duplicate accounts, and anything unfamiliar.

Step 2: Dispute Errors Immediately Credit report errors affect about 1 in 5 Americans. A single corrected error can boost your score by 10–100 points. Dispute directly with the bureau reporting the error.

Step 3: Pay Down Revolving Balances Credit utilization is 30% of your FICO score. Pay down credit card balances to:

- Below 30% of each card’s limit (minimum target)

- Below 10% of each card’s limit (optimal for mortgage applications)

Step 4: Don’t Close Old Accounts Length of credit history matters. Closing old cards reduces your available credit and raises your utilization ratio — both hurt your score.

Step 5: Set Up Autopay Payment history is 35% of your FICO score — the single largest factor. Autopay eliminates the risk of accidental missed payments during the home search process.

Month 2 Action Plan (Days 31–60)

Step 6: Freeze New Credit Applications Every hard inquiry drops your score by 5–10 points. Avoid applying for any new credit cards, auto loans, or personal loans during this window. For mortgage shopping specifically, multiple lender inquiries within a 45-day window count as just one inquiry — per CFPB guidelines.

Step 7: Request Credit Limit Increases Calling your card issuers to request a higher limit (without spending more) reduces your utilization ratio instantly. Most issuers do a soft pull only.

Step 8: Add Alternative Credit Data If you have a thin credit file, tools like Experian Boost allow you to add utility, phone, and streaming payment history directly to your Experian credit report — often delivering an immediate score increase.

Step 9: Get Pre-Qualified (Soft Pull) Pre-qualification uses a soft inquiry that doesn’t hurt your score. It also tells you exactly where you stand before applying formally.

Credit Score Boost Reference Table

| Action | Potential Score Boost | Timeframe |

|---|---|---|

| Pay down credit card to under 10% utilization | +20 to +50 points | 30–45 days |

| Dispute and fix credit errors | +10 to +100 points | 30–60 days |

| Add rent/utility history (Experian Boost) | +10 to +20 points | Immediate |

| Avoid all hard inquiries | Preserve 5–10 points | Ongoing |

| Maintain on-time payments | +5 to +15 points | 30+ days |

| Request credit limit increase | +10 to +30 points | 7–14 days |

What This Means For You: Going from a 619 to a 621 isn’t just 2 points — it’s the difference between needing 10% down on an FHA loan vs. only 3.5% down. On a $350,000 home, that’s a $22,750 difference in cash you need upfront.

If high-interest debt is holding your score down, use our debt consolidation calculator to see if consolidating could lower your utilization and monthly obligations simultaneously.

For buyers who are close to qualifying for a better rate tier, our mortgage refinance calculator shows exactly how much you’d save by locking in a lower rate once your score improves.

Also, before you buy, check our comprehensive credit score complete guide to understand every factor affecting your score in depth.

Frequently Asked Questions About Credit Score for Buying a House

1. What is the minimum credit score to buy a house in 2026?

The absolute minimum is 500 with an FHA loan and a 10% down payment. For FHA with 3.5% down, you need 580. Conventional loans typically require 620. VA and USDA loans don’t set official minimums, though most lenders want 580–640.

2. Can I buy a house with a 580 credit score?

Yes. A 580 credit score qualifies you for an FHA loan with just 3.5% down. VA loans may also be available at 580 depending on your lender. You’ll pay higher mortgage insurance, but homeownership is achievable right now.

3. Can I buy a house with a 500 credit score?

Yes, but only with an FHA loan and a 10% down payment. Many lenders also require strong compensating factors — stable income, low debt-to-income ratio, and reserves. Very few conventional lenders will approve a 500 score.

4. What credit score do I need for a conventional loan in 2026?

Most conventional lenders require a minimum of 620. However, to access the best interest rates and avoid costly PMI tiers, you’ll want a 740 or higher score. Fannie Mae’s automated underwriting now considers your full financial profile alongside your score.

5. Does the VA loan have a minimum credit score?

The U.S. Department of Veterans Affairs does not set an official minimum credit score. However, individual lenders typically require 580–620. Some lenders will approve VA loans with scores as low as 500 if you have a clean 12-month payment history.

6. What credit score do I need for an FHA loan?

FHA requires 580 for 3.5% down and 500 for 10% down. These are the FHA’s official minimums — individual lenders may set higher “overlay” requirements of 620 or 640.

7. How much does a low credit score cost on a mortgage?

A lot. On a $400,000 loan, a borrower with a 620 score may pay approximately $269 more per month and nearly $97,000 more in total interest compared to a borrower with a 760+ score over 30 years.

8. Does VantageScore 4.0 replace FICO for mortgages in 2026?

No — it joins FICO, not replaces it. As of July 2025, lenders can now choose to use either Classic FICO or VantageScore 4.0 for loans sold to Fannie Mae and Freddie Mac. This lender-choice model is new and represents a historic shift in mortgage credit scoring.

9. How fast can I raise my credit score to buy a house?

Most buyers can realistically improve their score by 20–50 points in 30–60 days by paying down revolving balances and disputing errors. More significant improvements of 50–100 points typically require 3–6 months of consistent effort.

10. What else do lenders look at besides credit score?

Lenders evaluate your debt-to-income ratio (DTI), employment history, income stability, cash reserves, down payment amount, and the property itself. A strong DTI can compensate for a weaker credit score in some loan programs. Use our debt-to-income ratio calculator to know exactly where you stand.

11. Is a 700 credit score good enough to buy a house in 2026?

Yes — a 700 score qualifies you for conventional, FHA, VA, and USDA loans. You’ll receive better rates than the 620–660 range, though you’ll unlock the very best interest rates at 740+. A 700 score is a solid foundation to buy now while continuing to build credit.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial, mortgage, or legal advice. Credit score requirements vary by lender, loan type, and individual financial profile. Please consult a licensed mortgage professional or HUD-approved housing counselor before making any financial decisions. Published March 2026.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.