Credit Score: Complete Guide to 800+

Discover how to build and maintain an 800+ credit score in 2026. Our comprehensive guide covers FICO vs VantageScore, the 5 key factors, proven improvement strategies, and more.

In This Article

What Is a Credit Score? (Complete Foundation)

A credit score is a three-digit number ranging from 300 to 850 that predicts your likelihood of repaying borrowed money on time. According to the Consumer Financial Protection Bureau, lenders use this numerical snapshot to assess credit risk before approving loans, credit cards, mortgages, and other financial products.

In 2026, understanding your credit score is more critical than ever. With average interest rates at historic levels and inflation affecting consumer spending, a strong credit score directly impacts your financial opportunities and borrowing costs.

FICO vs VantageScore: The Two Main Models

You don’t have just one credit score—you have multiple scores calculated by different models. The two dominant scoring systems are FICO (used by 90% of top lenders) and VantageScore, both using the 300-850 range.

FICO Score has been the industry standard since 1989, with different versions including FICO Score 8, FICO Score 9, and the newer FICO Score 10T. Each version weighs credit factors slightly differently, but all prioritize payment history as the most crucial element.

VantageScore was created in 2006 by the three major credit bureaus—Equifax, Experian, and TransUnion—to provide a consistent scoring model across all agencies. VantageScore 4.0, the latest version, can generate scores with as little as one month of credit history compared to FICO’s six-month requirement.

Credit Report vs Credit Score: Key Distinction

Your credit report is a detailed record of your credit history, including account information, payment patterns, credit inquiries, and public records like bankruptcies. Your credit score is derived from this report using mathematical algorithms.

Think of it this way: your credit report is the full story, while your credit score is the executive summary. Lenders review both when making lending decisions, but the score provides the quickest risk assessment.

Credit Score Ranges & What They Mean

Understanding where your score falls on the spectrum helps you gauge your creditworthiness and predict lender responses. As of 2026, the national average FICO score stands at 715, maintaining stability from the previous year despite economic pressures.

Complete Score Breakdown

300-579 (Poor): Approximately 16% of Americans fall into this range. Lenders view these scores as high-risk, often resulting in loan denials or approval only with extremely high interest rates and strict terms. Securing traditional credit products becomes challenging.

580-669 (Fair): About 18% of consumers have fair credit scores. You may qualify for some loans and credit cards, but expect higher interest rates and lower credit limits. Many premium credit card products remain inaccessible at this tier.

670-739 (Good): This represents 21% of the population. A good credit score opens doors to competitive interest rates and better loan terms. Most mortgage lenders, auto financiers, and credit card companies will approve applications in this range.

740-799 (Very Good): Approximately 25% of Americans achieve very good credit. You’ll qualify for lower interest rates than the national average and gain access to premium credit cards with superior rewards programs.

800-850 (Exceptional): Only 23% of consumers reach this elite tier. According to recent data, exceptional scores guarantee the lowest available interest rates, highest credit limits, and easiest approval processes across all credit products.

2026 Credit Score Statistics

The average credit score varies significantly by demographic factors. Gen Z averages 681 (good range), Millennials reach 691, Gen X achieves 707, Baby Boomers score 746, and the Silent Generation tops the chart at 760.

Geographically, Minnesota leads the nation with an average score of 742, followed by Wisconsin at 738 and Vermont at 737. Conversely, Mississippi averages 680, Louisiana 690, and Alabama 692—reflecting regional economic differences and financial literacy levels.

The 5 Factors That Determine Your Credit Score

Both FICO and VantageScore analyze your credit report using five core categories, though they weigh these factors differently. Understanding this breakdown is essential for strategic credit improvement.

1. Payment History (35% FICO, 40% VantageScore)

Your track record of on-time payments is the single most influential factor in your credit score. Every late payment, missed payment, collection account, or bankruptcy significantly damages your score. The Consumer Financial Protection Bureau emphasizes that payment history demonstrates your reliability as a borrower.

Recent research shows that 100% of consumers with 800+ credit scores pay all bills on time, every time. A single payment that’s 30 days late can drop your score by 50-100 points, depending on your overall credit profile.

2. Credit Utilization (30% FICO, 20% VantageScore)

Credit utilization measures how much of your available revolving credit you’re currently using. Calculate it by dividing your total credit card balances by your total credit limits, then multiplying by 100.

Formula: (Total Balances ÷ Total Credit Limits) × 100 = Utilization %

For example, if you have two credit cards—one with a $5,000 balance and $10,000 limit, another with a $2,000 balance and $8,000 limit—your utilization is 38.9% ($7,000 ÷ $18,000). While experts recommend staying below 30%, consumers with 800+ scores average just 7% utilization or less.

3. Length of Credit History (15% FICO, 21% VantageScore)

Lenders want to see an established track record. This factor considers the age of your oldest account, your newest account, and the average age across all accounts. The longer you’ve responsibly managed credit, the higher your score climbs.

Data shows consumers with exceptional credit have an average oldest account age of 23.3 years. Opening new accounts reduces your average account age, temporarily lowering your score—though the long-term benefits of additional available credit can outweigh this initial dip.

4. Credit Mix (10% Both Models)

Having different types of credit—installment loans (mortgages, auto loans, student loans) and revolving credit (credit cards, lines of credit)—demonstrates your ability to manage various payment structures. A diverse credit mix slightly improves your score.

However, don’t open unnecessary accounts just to diversify. Only pursue new credit when it serves a legitimate financial purpose.

5. New Credit and Inquiries (10% FICO, 5% VantageScore)

Applying for multiple credit accounts in a short timeframe signals financial distress to lenders. Each hard inquiry (when a lender checks your credit for a lending decision) can reduce your score by 5-10 points.

Important exception: When rate-shopping for mortgages, auto loans, or student loans, multiple inquiries within a 14-45 day window typically count as a single inquiry. This allows you to compare offers without penalty.

What Doesn’t Affect Your Credit Score

Contrary to popular belief, your income, savings account balances, employment status, checking account activity, and marital status play no role in credit score calculations. These factors may influence a lender’s approval decision, but they don’t impact the score itself.

How to Achieve an 800+ Credit Score (The Ultimate Guide)

Reaching the 800+ threshold places you among America’s financial elite. While only 23% of consumers achieve this milestone, it’s entirely attainable with disciplined credit management over time.

Why 800+ Matters: Tangible Benefits

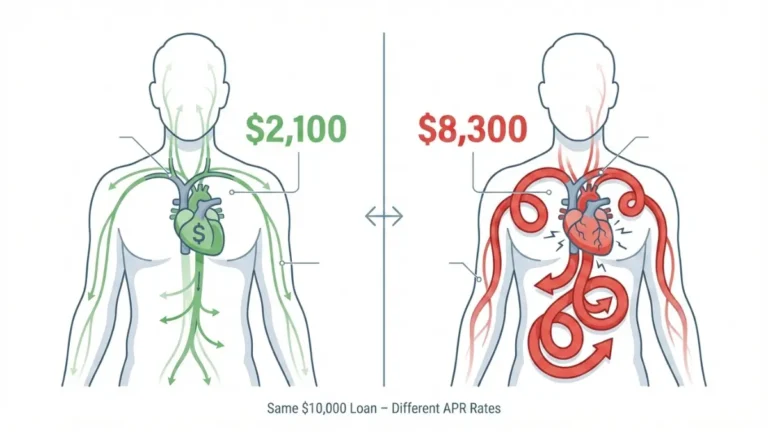

Lower Interest Rates: The difference between a 740 score and an 800+ score can save you tens of thousands of dollars. On a $350,000 30-year mortgage, borrowers with 800+ scores may secure rates 0.23% lower than those in the 700-750 range—translating to approximately $19,000 in savings over the loan’s lifetime.

Higher Credit Limits: Credit card issuers reward exceptional scores with substantially higher limits, sometimes exceeding $50,000 on premium cards. This expanded credit availability makes maintaining low utilization ratios easier.

Superior Insurance Rates: Most states allow insurers to use credit-based insurance scores when calculating premiums. Exceptional credit can reduce your auto and homeowners insurance costs by 10-30% compared to consumers with average credit.

Better Approval Odds: While 800+ doesn’t guarantee approval—lenders also consider income, employment, and debt-to-income ratios—it maximizes your chances across all credit products.

The 100% Payment Rule

LendingTree’s analysis of 100,000 credit reports revealed that 100% of consumers with 800+ scores paid every bill on time, every time. There are no exceptions to this rule. Even one 30-day late payment in the past seven years can prevent you from reaching 800+.

Action Steps:

- Set up automatic payments for all recurring bills

- Create calendar reminders for due dates

- Pay bills when you receive them, not on the due date

- Contact creditors immediately if you anticipate difficulty making a payment

Master Credit Utilization

Consumers with 800+ scores maintain average utilization rates of 7% or less—far below the commonly cited 30% threshold. This requires strategic balance management.

Optimization Strategies:

- Pay credit card balances before the statement closing date to report lower balances

- Make multiple payments throughout the month instead of one large payment

- Request credit limit increases on existing cards (without opening new accounts)

- Use our Credit Score Calculator to model how utilization changes affect your score

If you’re carrying balances, deploy either the debt avalanche method (paying highest-interest debts first) or the debt snowball method (paying smallest balances first for psychological wins). Our comprehensive guide on how to pay off debt fast provides detailed implementation strategies.

Timeline Expectations: Reality Check

Building credit from scratch to 800+ typically requires 7-10 years of perfect credit management. If you’re starting with good credit (670-739), expect 3-5 years to reach exceptional status with consistent effort.

Realistic Milestones:

- 0-6 months: Establish first credit account, reach 580-620

- 6-12 months: Build to 640-680 with on-time payments

- 1-3 years: Achieve 700-750 with diversified credit mix

- 3-5 years: Reach 760-790 with aged accounts and perfect history

- 5-7+ years: Break 800 with sustained excellent behavior

Advanced Strategies for 800+

Become an Authorized User: If you have a family member with excellent credit and a long-established account, ask to be added as an authorized user. You’ll inherit the account’s positive history, instantly boosting your average account age and utilization ratio.

Strategic Credit Limit Increases: Every 6-12 months, request credit limit increases on your existing cards. This lowers your overall utilization without opening new accounts. Most issuers perform soft inquiries for these requests, preserving your score.

Preserve Your Oldest Account: Never close your oldest credit card, even if you no longer use it actively. Make one small purchase every 3-6 months to keep it active. This account anchors your credit history length.

Optimize Your Credit Mix: If you only have credit cards, consider a credit builder loan or a small personal loan that you immediately pay off. This adds installment loan history to your profile. Our Loan Calculator helps you model payment scenarios.

Navigating 2026 Economic Challenges

With inflation moderating but interest rates remaining elevated, many consumers face pressure on their credit scores. Federal student loan payments resumed in 2024, affecting millions of borrowers’ payment histories. Focus on maintaining perfect payment records even if it means making minimum payments during tight months.

Common Credit Score Mistakes & How to Avoid Them

Even financially savvy consumers make errors that damage their credit scores. Awareness of these pitfalls helps you navigate credit management successfully.

Closing Old Credit Card Accounts

Many people close unused cards to simplify their finances, not realizing this hurts their credit in two ways. First, it reduces your total available credit, instantly increasing your utilization ratio. Second, closed accounts eventually fall off your credit report, reducing your average account age.

Better Approach: Keep old cards open with small recurring charges (like a streaming subscription) set to autopay. This maintains your credit history and available credit without requiring active management.

Making Only Minimum Payments

While minimum payments prevent late payment marks, they signal financial stress to credit scoring algorithms. VantageScore 4.0 specifically examines payment trends, penalizing consumers who consistently make only minimum payments.

Additionally, minimum payments on high-interest debt create a cycle where interest charges prevent meaningful balance reduction. Use our Credit Card Payoff Calculator to see how extra payments accelerate debt elimination.

Ignoring Credit Report Errors

The Federal Trade Commission estimates that 20% of credit reports contain errors that could negatively impact scores. Common mistakes include accounts that aren’t yours, incorrect payment statuses, duplicate accounts, and outdated negative information.

Applying for Too Much Credit Simultaneously

Each hard inquiry reduces your score by 5-10 points and remains on your report for two years. Applying for multiple credit cards, loans, or financing offers within a short period compounds this damage and signals desperation to lenders.

Maxing Out Credit Cards

Even if you pay your balance in full each month, high statement balances hurt your score. Credit card issuers typically report your balance to the bureaus on your statement closing date, not when you make your payment.

Co-Signing Loans Without Understanding Risk

When you co-sign a loan, it appears on your credit report as if it’s your own debt. If the primary borrower misses payments or defaults, your credit suffers equally. Additionally, the debt counts toward your debt-to-income ratio when you apply for your own credit.

Believing Credit Score Myths

Myth: Carrying a small balance improves your score. Reality: Credit scoring models don’t reward carrying balances. Paying in full is always optimal.

Myth: Checking your own credit hurts your score. Reality: Soft inquiries (when you check your own credit) have zero impact on your score.

Myth: Closing accounts removes negative history. Reality: Negative items remain on your report for 7-10 years regardless of account status.

Checking & Monitoring Your Credit Score

Regular credit monitoring helps you track progress, detect fraud, and identify errors before they cause significant damage. The federal government guarantees your right to access your credit information.

Free Credit Reports

Under federal law, you’re entitled to one free credit report every 12 months from each of the three major bureaus—Equifax, Experian, and TransUnion. Access these reports exclusively through AnnualCreditReport.com, the only official source authorized by the federal government.

Pro Strategy: Instead of requesting all three reports simultaneously, stagger them every four months. This provides year-round credit monitoring at no cost.

Additionally, Equifax currently offers six free credit reports per year through December 2026 as part of a settlement agreement. This enhanced access allows more frequent monitoring of one bureau’s data.

Free Credit Score Access

While credit reports are guaranteed free, credit scores typically cost money—unless you access them through these legitimate free sources:

- Many credit card issuers (Capital One, Discover, Chase, American Express)

- Bank account benefits (Bank of America, Wells Fargo, Citi)

- Nonprofit credit counseling services

- Credit monitoring websites (with free tiers)

Be cautious of “free credit score” advertisements that require credit card information. Many of these offers automatically enroll you in paid monitoring services unless you cancel during a trial period.

How Often to Check

Monitor your credit at least quarterly, but monthly is ideal for proactive management. Your score updates whenever new information is reported to the bureaus, typically once per month when lenders submit updates.

Checking more frequently than weekly provides little additional value, as most changes occur on monthly reporting cycles.

Disputing Credit Report Errors

If you discover inaccuracies, you have the legal right to dispute them with both the credit reporting company and the company that furnished the incorrect information. The credit bureau must investigate within 30 days and correct verified errors.

Dispute Process:

- Clearly identify each error in writing

- Explain why you believe it’s incorrect

- Include copies (not originals) of supporting documents

- Send via certified mail with return receipt requested

- Submit disputes to all three bureaus separately

The Consumer Financial Protection Bureau provides detailed guidance and sample dispute letters on their website.

Frequently Asked Questions about Credit Score

Q1: What is a good credit score?

A good credit score ranges from 670-739 on the FICO scale and 661-780 for VantageScore. Scores in this range qualify you for most credit products with competitive terms.

Q2: How long does it take to build credit from zero?

Expect 6-12 months to establish a scorable credit file and reach the fair range (580-669), then 2-3 additional years of responsible management to achieve good credit (670+).

Q3: Can I get an 850 credit score?

Yes, but it’s extremely rare—only 1.7% of Americans achieve a perfect 850. More importantly, scores above 760 typically receive identical treatment from lenders, making perfection unnecessary.

Q4: Do hard inquiries hurt my score?

Yes, each hard inquiry can reduce your score by 5-10 points. However, the impact is temporary, and multiple inquiries for the same loan type within 14-45 days count as one inquiry.

Q5: How much can one late payment hurt?

A single 30-day late payment can drop your score by 50-100 points, depending on your overall credit profile. The damage persists for seven years but diminishes over time.

Q6: Does checking my score lower it?

No. Checking your own credit score or report is a soft inquiry that has zero impact on your credit score.

Q7: What’s the fastest way to improve my score?

Pay down high-balance credit cards to reduce utilization below 30% (ideally below 10%). This can produce score improvements within 30-60 days.

Q8: Can I remove accurate negative items?

No. Only inaccurate or unverifiable information can be removed through disputes. Accurate negative items remain for 7 years (most items) or 10 years (bankruptcies).

Q9: Do credit repair companies work?

Most credit repair companies can’t do anything you can’t do yourself for free. Many charge hundreds or thousands of dollars for services that are legally available to all consumers at no cost.

Q10: How often does my score update?

Your score updates whenever new information is reported to the credit bureaus, typically monthly. Different lenders report on different schedules, so update frequency varies.

Q11: What credit score do I need for a mortgage?

Conventional mortgages typically require a minimum 620 FICO score, though 740+ unlocks the best rates. FHA loans may accept scores as low as 580 (with 3.5% down) or 500 (with 10% down). Use our Mortgage Calculator to explore payment scenarios at different score tiers.

Disclaimer

This article provides educational information only and does not constitute financial, legal, or professional advice. The content is accurate to the best of our knowledge as of January 2026, but credit scoring models, lending practices, and regulations change frequently.

We are not licensed financial advisors, credit counselors, or legal professionals. Credit score improvement strategies involve inherent risks and individual results vary significantly based on personal credit history, financial circumstances, and economic conditions.

Important Warnings:

- Past credit score improvements do not guarantee future results

- Credit scoring models may change without notice, affecting score calculations

- Lender decisions involve factors beyond credit scores alone

- Economic conditions and lending market changes can impact credit availability regardless of score

All data presented comes from publicly available sources including government agencies, credit bureaus, and peer-reviewed financial research. While we strive for accuracy, we cannot guarantee that all information is current, complete, or error-free.

Before making financial decisions, consult qualified professionals including licensed financial advisors, certified credit counselors, or legal counsel who can provide personalized guidance based on your specific situation.

The strategies discussed may not be suitable for all individuals. Credit management approaches should align with your overall financial goals, risk tolerance, and personal circumstances. No guaranteed credit score increases or loan approval outcomes are promised or implied.

Sources: Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), Fair Isaac Corporation (FICO), VantageScore Solutions, Experian, Equifax, TransUnion, and various federal government publications.

For official credit score information and consumer rights, visit www.consumerfinance.gov or call (855) 411-CFPB.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.