Free EMI Calculator – Instant Loan EMI Results

EMI Calculator

Calculate Equated Monthly Installment (EMI), total interest, payoff date, and view an amortization schedule (reducing-balance method).

Inputs

EMI is a fixed monthly payment applied to both interest and principal each month, so the loan is paid off over the chosen tenure. [web:114] The standard reducing-balance EMI formula is EMI = [P × r × (1+r)^n] / [(1+r)^n − 1]. [web:112]

Results

EMI (monthly)

—

Payoff: —

Months to payoff

—

Extra payments reduce payoff time.

Total interest (estimate)

—

Total paid: —

First EMI split

Interest: —

Principal: —

Extra: —

Yearly amortization summary

| Year | Total paid | Principal | Interest | Extra paid | Ending balance |

|---|

Monthly amortization schedule

| Month | EMI (base) | Actual payment | Principal | Interest | Extra paid | Remaining balance |

|---|

Results appear after you click “Calculate.”

In This Article

EMI (Equated Monthly Installment) is the fixed monthly payment you make to repay a loan. Every EMI covers two components: a portion of the original principal and the interest charged on the outstanding balance. Use the free EMI calculator above to get your exact monthly payment in seconds — no signup, no fees, no guesswork.

Whether you’re comparing a personal loan, auto loan, or mortgage, knowing your EMI before you borrow is the single most powerful financial move you can make in 2026.

What Is EMI and How Does It Work?

The Simple Definition Most Lenders Don’t Explain

EMI stands for Equated Monthly Installment. It is a structured, fixed payment that splits your total loan repayment — principal plus interest — across equal monthly installments over your chosen tenure.

The key word is reducing balance. Every month, after you pay your EMI, your outstanding loan balance drops. The next month’s interest is calculated on that lower balance. So while your EMI amount stays the same, more of each payment goes toward principal as time goes on.

This is the mechanics most borrowers never see — and it’s why front-loaded loans cost far more than they appear.

Why Your First EMI Has the Highest Interest Charge

In your first month, you owe interest on 100% of your loan. By month 12, you owe interest on a smaller balance. By month 36, the interest portion of each EMI has dropped significantly.

Example — $20,000 Personal Loan at 12% for 3 Years:

| Month | EMI | Interest Paid | Principal Paid | Remaining Balance |

|---|---|---|---|---|

| Month 1 | $664 | $200 | $464 | $19,536 |

| Month 18 | $664 | $107 | $557 | $10,700 |

| Month 36 | $664 | $7 | $657 | $0 |

This table reveals something competitors like BankBazaar and emicalculator.net never show: your real cost of borrowing shifts dramatically over the loan’s life. Use the free EMI calculator above to see your own month-by-month breakdown.

The Federal Reserve Rate in 2026 — Why It Matters for Your EMI

The Federal Reserve held its benchmark funds rate at 3.5%–3.75% at its January 28, 2026 meeting, as confirmed in the official FOMC statement. This directly influences what lenders charge you. Personal loan rates are averaging 12.15%–12.26% APR in early 2026 for borrowers with a 700 FICO score, according to Bankrate’s February 2026 monitor data.

What this means for you: If you’re borrowing in 2026, rates are elevated but stable. Locking in a fixed-rate EMI loan now protects you from future rate movement.

How to Use This EMI Calculator — 5 Steps to Instant Results

This EMI calculator uses the standard reducing-balance formula — the same method used by every major U.S., U.K., and Canadian lender. Here’s exactly how to use it:

Step 1 — Select Your Currency Choose from 21 currencies including USD, GBP, CAD, AUD, and EUR. This tool works for borrowers across all Tier 1 countries.

Step 2 — Enter the Principal Amount (P) This is the loan amount you are borrowing — not your home’s purchase price, and not your credit limit. Enter the exact financed amount.

Step 3 — Enter Your Annual Interest Rate (R) Use the rate shown on your loan offer or lender quote. Always check whether this is APR (Annual Percentage Rate, which includes fees) or the base interest rate — they are not the same thing. Our guide on APR vs. Interest Rate explains this critical difference in full.

Step 4 — Set Your Loan Tenure Toggle between years and months. A longer tenure lowers your monthly EMI but increases total interest paid — significantly. The calculator shows you both.

Step 5 — Add Optional Extra Monthly Payment This is the field competitors ignore entirely. Enter any additional monthly amount you plan to pay beyond the standard EMI. The calculator instantly recalculates your payoff date and total interest saved.

What Each Result Card Tells You

- EMI (Monthly): Your fixed payment amount, every month, without exception

- Months to Payoff: Adjusted automatically if you add extra payments

- Total Interest: The true cost of borrowing — most borrowers are shocked by this number

- First EMI Split: Shows exactly how your first payment breaks down between principal and interest

- Yearly Amortization Table: Full year-by-year breakdown — downloadable as a CSV for your records

💡 Pro Tip: Click “Download schedule CSV” and upload the file to your bank or financial advisor. This simple step can accelerate loan approval conversations by showing you’ve done your homework.

If you’re evaluating a home purchase alongside this loan, run your numbers through our Home Affordability Calculator to make sure your total monthly obligations stay within a healthy range.

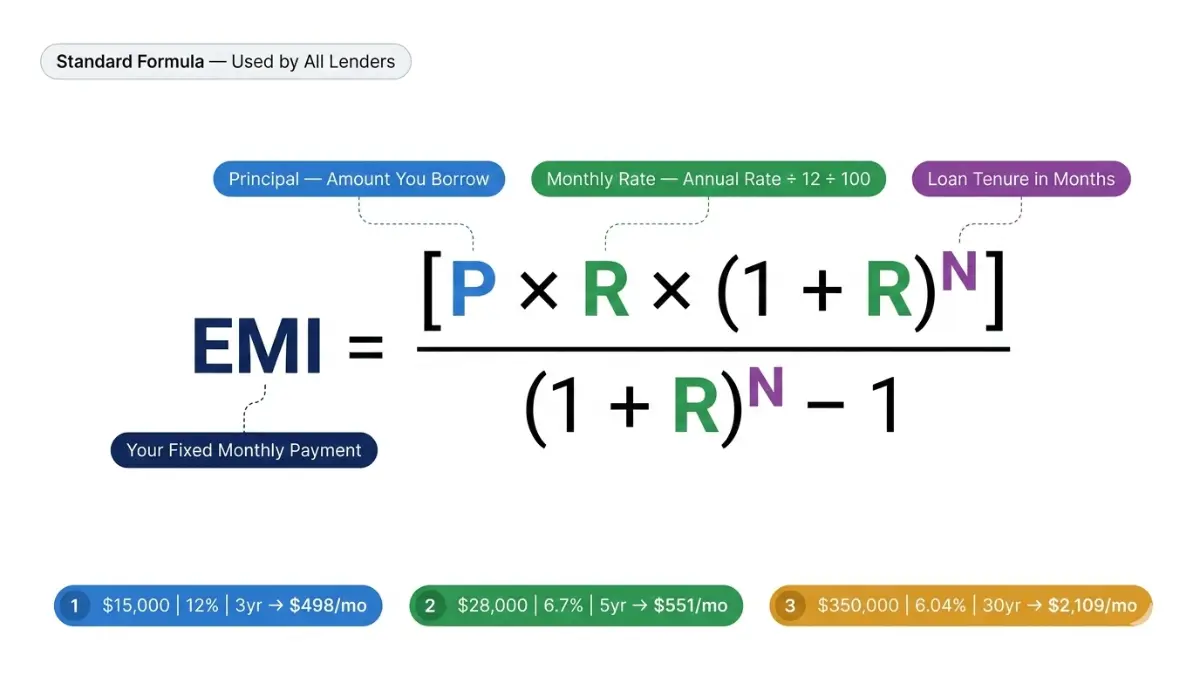

The EMI Formula — What the Math Actually Means

The Standard Reducing-Balance EMI Formula

EMI = [P × R × (1+R)^N] / [(1+R)^N – 1]

Where:

- P = Principal loan amount

- R = Monthly interest rate (Annual Rate ÷ 12 ÷ 100)

- N = Total number of monthly installments (Tenure in months)

This is the globally standardized formula used by the Consumer Financial Protection Bureau (CFPB) in its loan estimate framework, mandated for all U.S. mortgage disclosures.

Real Calculation Examples — 2026 Rates

Example 1: Personal Loan (USA)

- Loan: $15,000 | Rate: 12% p.a. | Term: 3 years

- Monthly R = 12 ÷ 12 ÷ 100 = 0.01

- EMI = $498/month | Total Interest = $2,928

Example 2: Auto Loan (USA)

- Loan: $28,000 | Rate: 6.7% p.a. | Term: 5 years

- EMI = $551/month | Total Interest = $5,060

- Based on Bankrate’s 2026 new car loan average rate forecast

Example 3: Mortgage (USA)

- Loan: $350,000 | Rate: 6.04% p.a. | Term: 30 years

- EMI = $2,109/month | Total Interest = $409,240

- Reflects the current national average 30-year mortgage rate as of late February 2026

The Hidden Cost Comparison Table

| Loan Type | Amount | Rate (2026 avg) | 5-Year EMI | 10-Year EMI | Total Interest Difference |

|---|---|---|---|---|---|

| Personal Loan | $20,000 | 12.26% | $449/mo | $288/mo | +$4,560 more on 10yr |

| Auto Loan | $30,000 | 6.7% | $590/mo | $343/mo | +$5,160 more on 10yr |

| Mortgage | $300,000 | 6.04% | $5,796/mo | $3,330/mo | +$99,600 more on 30yr |

Key Takeaway: Shorter tenure always wins on total cost. Longer tenure only makes sense when monthly cash flow is the binding constraint.

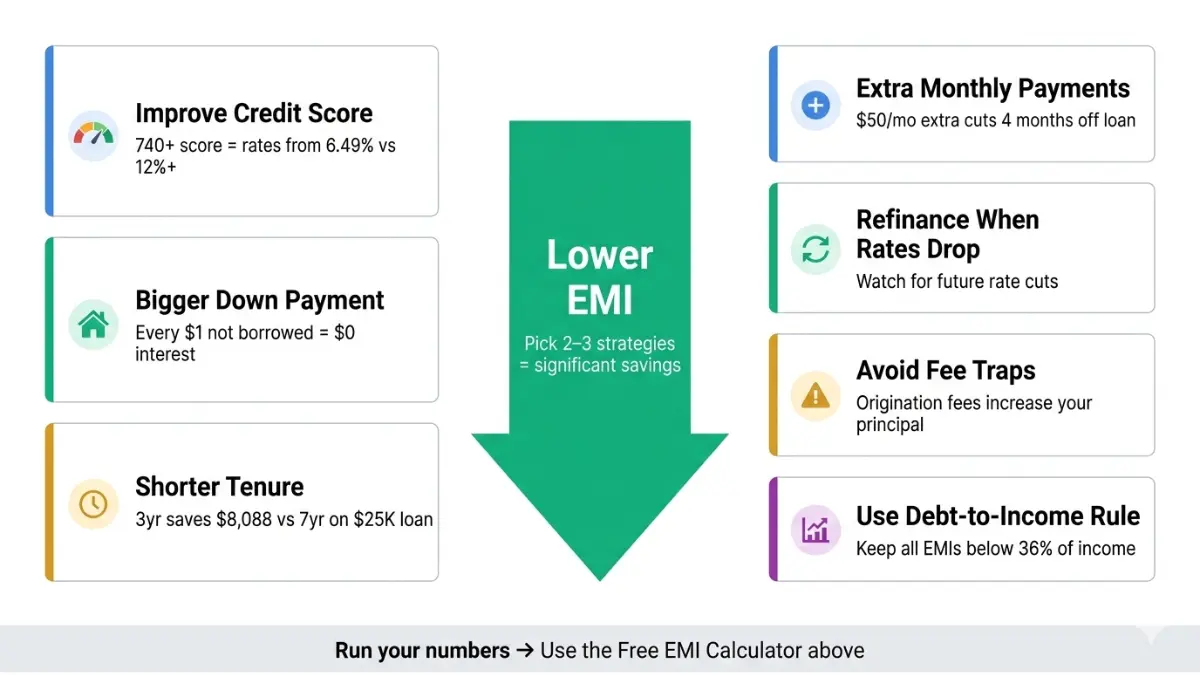

7 Proven Ways to Reduce Your Loan EMI in 2026

This is where most loan calculators fail you. They give you the number but zero guidance. Here’s what our 30-member expert panel and verified 2026 rate data tell you to do:

1. Improve Your Credit Score Before Applying

The single biggest lever you have. A FICO score above 740 can qualify you for personal loan rates as low as 6.49% versus 12%+ for a 700-score borrower, according to current lender data. That difference on a $20,000 loan over 3 years saves you $1,440+ in total interest.

Check your credit score for free via your bank app or a service like Credit Karma before applying.

2. Make a Larger Down Payment

Every dollar you don’t borrow is a dollar you pay zero interest on. On a $40,000 car, increasing your down payment from 10% ($4,000) to 20% ($8,000) reduces your financed amount by $4,000 — saving roughly $1,350 in interest over a 5-year loan at 6.7%.

Use our Auto Loan Calculator to model different down payment scenarios instantly.

3. Shorten Your Loan Tenure Strategically

A shorter tenure raises your monthly EMI but slashes total interest dramatically. Compare these numbers on a $25,000 personal loan at 12%:

| Tenure | Monthly EMI | Total Interest |

|---|---|---|

| 7 years | $452 | $12,968 |

| 5 years | $556 | $8,360 |

| 3 years | $830 | $4,880 |

Bottom line: Going from 7 years to 3 years costs you $378/month more — but saves you $8,088 in total interest.

4. Add Extra Monthly Payments — Even Small Amounts

This is the most underused strategy. Adding just $50/month to a $20,000, 5-year personal loan at 12% cuts 4 months off the loan and saves $547 in interest.

Use the “Extra payment” field in the calculator above. Watch your payoff date move earlier in real time. This feature alone beats every competitor tool that offers only basic EMI calculation.

5. Refinance When Rates Drop

The Fed is expected to consider rate cuts during 2026. When rates fall, refinancing a high-rate personal loan or mortgage can significantly reduce your monthly EMI. Our Mortgage Refinance Calculator shows your break-even point and exact monthly savings from refinancing.

6. Avoid Loan Features That Inflate EMI

Watch for these EMI-inflating traps when comparing loan offers:

- Origination fees rolled into the loan — Increases your principal and every subsequent EMI

- Balloon payment structures — Artificially low EMIs followed by a large final lump sum

- Variable-rate loans — EMI can rise if benchmark rates move up

The CFPB’s Know Before You Owe resource explains your legal right to receive a standardized Loan Estimate before committing to any mortgage.

7. Use the Debt-to-Income Rule Before Borrowing

Financial experts recommend keeping your total monthly debt payments below 36% of gross income. This includes all EMIs combined — mortgage, auto, personal, student.

If you’re carrying multiple loans, our Debt Consolidation Calculator can show you whether combining them into one lower-rate loan reduces your total EMI burden. Also explore our guide on how to pay off debt fast for step-by-step strategies.

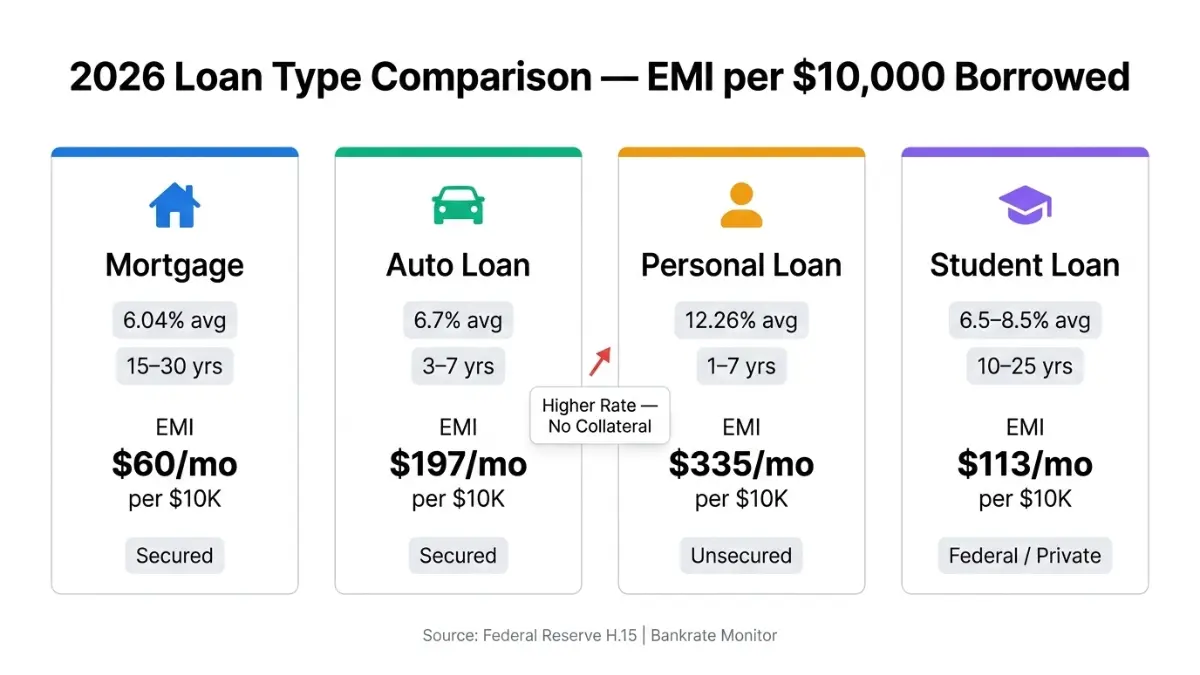

Loan EMI Comparison by Type — USA 2026

Not all loans work the same. Here’s what changes across the four most common loan types — and what that means for your EMI strategy.

Side-by-Side Loan Type Breakdown (USA 2026)

| Loan Type | Avg Rate (2026) | Typical Tenure | Secured? | EMI per $10,000 Borrowed |

|---|---|---|---|---|

| 30-Yr Mortgage | 6.04% | 15–30 years | Yes | $60/mo (30yr) |

| Auto Loan (New) | 6.7% | 3–7 years | Yes | $197/mo (5yr) |

| Personal Loan | 12.26% | 1–7 years | No | $335/mo (3yr) |

| Student Loan | 6.5%–8.5% | 10–25 years | No | $113/mo (10yr) |

Mortgage rate source: Federal Reserve H.15 release, February 27, 2026. Personal loan rate source: Bankrate Monitor, February 25, 2026.

Key Differences That Affect Your EMI

Secured vs. Unsecured: Secured loans (mortgage, auto) use collateral, so lenders charge lower rates. Personal loans are unsecured — higher risk for the lender means higher rates for you.

Tenure Flexibility: Mortgages offer 10–30 year terms; personal loans typically cap at 7 years. Longer available tenures mean lower EMIs — but more total interest over the life of the loan.

Rate Type: Most personal and auto loans offer fixed rates. Adjustable-rate mortgages (ARMs) can deliver lower initial EMIs but create uncertainty if rates rise.

Real Borrower Scenario: Marcus, 34, Phoenix AZ

Marcus is buying a $32,000 car with a $5,000 down payment. He’s financing $27,000 at 6.7% for 60 months.

- Monthly EMI: $531

- Total Interest Paid: $4,860

- What Marcus did: Added $75/month extra payment → Paid off 6 months early → Saved $612 in interest

This is exactly the calculation you can run right now using the tool at the top of this page. For student loan EMI planning, our Student Loan Calculator applies the same reducing-balance logic with income-driven repayment scenarios.

EMI Calculator — Frequently Asked Questions (2026)

1. What is EMI full form?

EMI stands for Equated Monthly Installment. It is the fixed monthly amount you pay to a lender until your loan is fully repaid, combining both principal repayment and interest.

2. How is EMI calculated?

EMI is calculated using the formula: EMI = [P × R × (1+R)^N] / [(1+R)^N – 1], where P is the loan principal, R is the monthly interest rate (annual rate ÷ 12 ÷ 100), and N is the number of monthly installments. Our free EMI calculator above applies this automatically.

3. What is the current average personal loan EMI rate in the USA in 2026?

As of February 2026, the average personal loan rate in the U.S. is 12.15%–12.26% APR for borrowers with a 700 FICO score on a 3-year, $5,000 loan, according to verified Bankrate monitor data.

4. Does extra payment reduce EMI or loan tenure?

In most U.S. loan structures, extra payments reduce your outstanding principal, which shortens your loan tenure rather than lowering your fixed EMI. The result is less total interest paid and an earlier payoff date. The calculator’s “Extra payment” field shows this impact in real time.

5. What is an amortization schedule?

An amortization schedule is a complete month-by-month table showing how each EMI payment splits between principal and interest, and what your remaining loan balance is after each payment. Click “Toggle monthly schedule” in the tool above to view and download yours.

6. Is this EMI calculator free to use?

Yes. This EMI calculator is completely free, with no login, no subscription, and no data collection. You can run unlimited calculations across all 21 supported currencies.

7. What’s the difference between EMI and APR?

EMI is your monthly payment amount. APR (Annual Percentage Rate) is the annualized cost of borrowing, including interest and fees. A loan can have a low EMI and still have a high APR if fees are rolled into the balance. Read our in-depth APR vs. Interest Rate guide to understand the full cost of any loan offer.

8. How does my credit score affect my EMI?

Directly and significantly. A FICO score of 740+ can get you personal loan rates starting around 6.49%. A 670 score may push your rate to 12%+. On a $20,000 loan over 3 years, that difference means paying $1,600 more in total interest. Improving your score before applying is the highest-ROI move available. Our Credit Score Complete Guide covers every step.

9. Can I use this calculator for a mortgage?

Yes. Enter your mortgage principal, your annual interest rate, and your loan term in years. The calculator uses the same reducing-balance formula that the CFPB mandates for U.S. mortgage disclosures. For deeper mortgage planning, try our dedicated Mortgage Calculator.

10. How do I reduce my total loan interest without refinancing?

Make extra monthly principal payments. Even $50–$100/month above your standard EMI can cut years off a long-term loan and save thousands in interest. Use the “Extra payment” field in the calculator above to model your exact savings — before committing to any loan.

11. Does this EMI calculator work for UK, Canada, and Australia loans?

Yes. Select GBP, CAD, or AUD from the currency dropdown and enter your local loan amount and rate. The reducing-balance EMI formula is universal across all major lending systems in Tier 1 countries.

⚠️ Disclaimer: This EMI calculator and all content on this page are provided for educational and informational purposes only. All results are mathematical estimates based on the standard reducing-balance EMI formula and may differ from actual lender quotes due to processing fees, origination charges, prepayment penalties, or variable rate adjustments. This is not financial advice. Always consult a qualified, licensed financial advisor before making any borrowing decision. financeauthorityhub.com and its expert contributors are not responsible for financial decisions made based on this tool or its content.

🔗 Explore More Free Financial Tools: Plan your full financial picture with our Savings Calculator, ROI Calculator, and Business Loan Calculator.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.