Refinance Calculator: See Your Savings Instantly (2026)

Mortgage Refinance Calculator

Compare your current mortgage vs a refinance: new payment, monthly savings, break-even time, and amortization schedules.

Inputs

Enter your remaining balance + remaining term (not the original term).

Optionally roll closing costs into the new loan and/or add cash-out.

Tip: If you roll closing costs into the loan, break-even (upfront cost recovery) may show as 0 months, so focus on total interest + payment impact.

Results

Current payment (P&I)

—

Payoff: — • Months: —

Refinance payment (P&I)

—

Payoff: — • Months: —

Monthly savings (P&I)

—

Break-even months: —

Break-even date: —

New loan amount

—

Cash-out: —

Closing costs: — (—)

Interest comparison (P&I only)

Interest remaining (current): —

Interest (refinance): —

Current loan — yearly amortization summary

| Year | Paid (P&I) | Principal | Interest | Extra paid | Ending balance |

|---|

Refinance loan — yearly amortization summary

| Year | Paid (P&I) | Principal | Interest | Extra paid | Ending balance |

|---|

Current loan — monthly amortization schedule

| Month | Payment (P&I) | Principal | Interest | Extra paid | Remaining balance |

|---|

Refinance loan — monthly amortization schedule

| Month | Payment (P&I) | Principal | Interest | Extra paid | Remaining balance |

|---|

Results appear after you click “Calculate.”

In This Article

A refinance calculator tells you exactly how much money you can save by replacing your current mortgage with a new loan at a lower rate. Enter your current balance, current rate, new rate, and closing costs — and see your monthly savings, break-even point, and total interest difference in seconds.

Use the Mortgage Refinance Calculator above to run your numbers before reading this guide.

What Is a Refinance Calculator — and Why Does It Matter in 2026?

Mortgage refinancing is the process of replacing your existing home loan with a new one that carries different — ideally better — terms. A refinance calculator automates the math so you don’t have to guess whether the switch actually saves you money.

In 2026, this tool matters more than ever. According to Bankrate’s March 2026 lender survey, the 30-year fixed rate sits at approximately 6.15% — down from the 7%+ peak seen as recently as January 2025. That gap is the refinance window millions of homeowners have been waiting for.

Who Should Use a Refinance Calculator Right Now?

- Homeowners who locked in a rate above 6.75% between 2022–2024

- Borrowers whose credit score has improved 50+ points since origination

- Homeowners planning a cash-out refinance to fund renovations

- Anyone considering switching from an adjustable-rate mortgage (ARM) to a fixed rate

What This Calculator Instantly Shows You

| Output | What It Means |

|---|---|

| Monthly savings (P&I) | Your new payment vs. your current payment |

| Break-even point | How many months until savings cover closing costs |

| Total interest saved | Full-term cost comparison, current vs. new loan |

| Amortization schedule | Month-by-month payment breakdown for both loans |

| After-tax break-even | Break-even adjusted for your marginal tax rate |

| Horizon analysis | How costs compare at 12, 36, 60, and 120 months |

Key Takeaway: The calculator does not just tell you your new payment. It tells you whether refinancing is financially rational given your specific situation — something no competitor tool explains clearly.

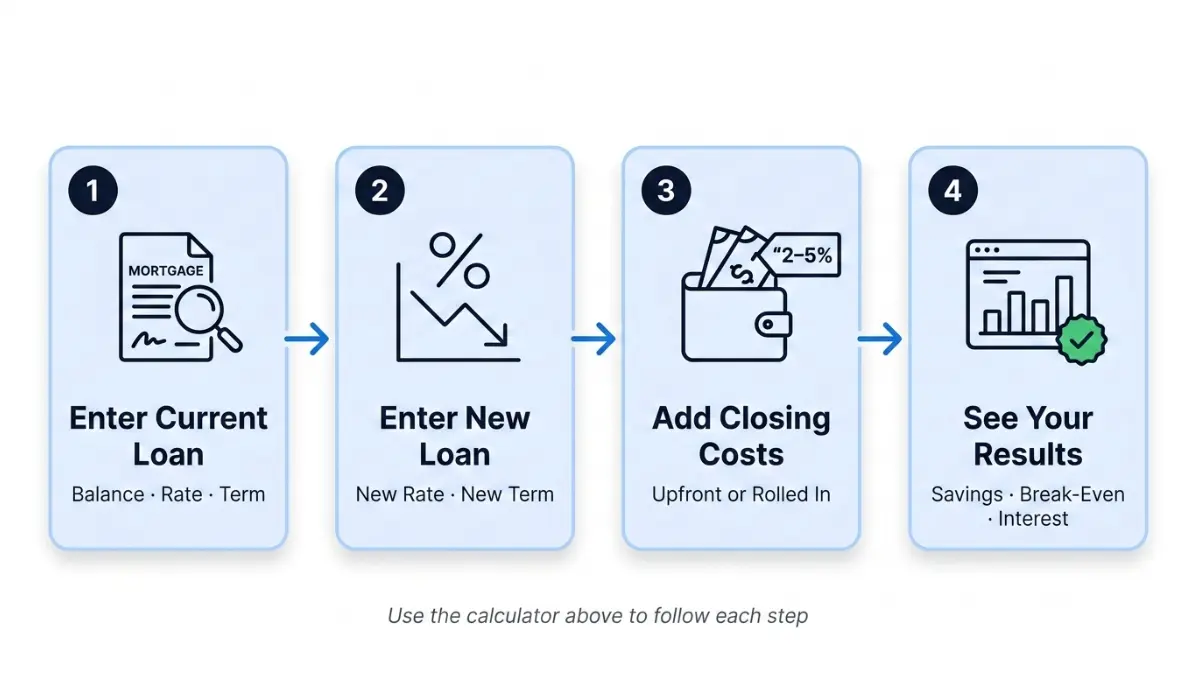

How to Use This Refinance Calculator — Step-by-Step

Most refinance calculators online are black boxes. You enter numbers, get a result, and have no idea what it means. This guide walks you through every input in our free refinance calculator so your results are accurate and actionable.

Step 1 — Enter Your Current Mortgage Details

Current Remaining Balance This is your payoff amount — not your original loan. Find it on your most recent mortgage statement or call your servicer. Example: $285,000.

Current Rate (APR %) Use your APR, not just the interest rate. These differ when fees are rolled in. APR gives a more accurate picture; you can check the full difference in our APR vs. Interest Rate guide.

Remaining Term How many years and months are left on your loan — not the original term. If you took a 30-year mortgage 5 years ago, your remaining term is 25 years.

Step 2 — Enter Your New Refinance Loan Details

New Rate (APR %) Shop at least three lenders before entering this number. According to the Consumer Financial Protection Bureau (CFPB), borrowers who compare multiple lenders save significantly more over the life of the loan.

New Term This is one of the most important decisions. A 15-year term saves more interest but raises your monthly payment. A 30-year term lowers your payment but extends debt. See our 15 vs. 30-Year Mortgage Comparison for a full breakdown.

Extra Payment (Optional) Adding even $100/month to principal can shave years off your loan. Enter it here to see the compounding impact over time. Our Amortization Calculator can model this separately.

Step 3 — Add Closing Costs

Closing costs on a refinance typically run 2%–5% of the loan amount, according to Fannie Mae’s consumer refinance guide. On a $300,000 loan, that’s $6,000–$15,000.

You have two choices in the calculator:

- Pay upfront — lower loan balance, break-even happens faster

- Roll into new loan — no cash out of pocket, but you pay interest on those costs for the life of the loan

Cash-Out / Cash-In Fields

- Cash-out: Borrow more than you owe and receive the difference in cash. Requires minimum 20% equity.

- Cash-in: Bring money to closing to reduce your principal. Useful if you’re near the 80% LTV threshold to eliminate PMI.

Step 4 — Read and Interpret Your Results

Once you click Calculate, here’s how to read the output:

| Result | Green Light | Yellow | Red Flag |

|---|---|---|---|

| Monthly savings | $200+/month | $100–199 | Under $100 |

| Break-even months | Under 24 months | 24–48 months | Over 48 months |

| Total interest saved | More than closing costs | Within 10% of costs | Less than closing costs |

Bold Takeaway: If your break-even is under 24 months and you plan to stay in your home, refinancing almost certainly makes financial sense.

Is Refinancing Worth It in 2026?

This is the most-searched question in this category right now — and the one no competitor answers with current data. Here is the honest, data-backed answer.

The 2026 Rate Environment You Need to Know

- 30-year fixed refinance rate: ~6.15% (Bankrate, March 2026)

- 15-year fixed refinance rate: ~5.38% (NerdWallet/Zillow, March 2026)

- Refinance Index: Up 109% year-over-year (Mortgage Bankers Association, 2026)

The refinance window is open — but it’s not open for everyone. The math only works if your current rate is meaningfully higher than today’s available rates.

Does the “1% Rule” Still Apply?

The old rule says refinance only if you can drop your rate by at least 1%. This rule is outdated. What actually matters is your break-even period relative to how long you plan to stay.

According to the Federal Reserve’s consumer mortgage refinancing guide, the break-even calculation — closing costs divided by monthly savings — is the correct primary test. A 0.75% rate drop on a $400,000 loan can be more valuable than a 1.5% drop on a $100,000 loan.

Expert insight from Laura M. Bennett, CFP: “In 2026, I’m advising clients to focus less on the rate gap and more on their 5-year plan. If they’re staying in the home, even a $150/month savings pays back $6,000 in closing costs in under 3.5 years — that’s a strong return.”

5 Signs You Should Refinance Now

- ✅ Your current rate is above 6.75%

- ✅ Your credit score has improved 50+ points since origination

- ✅ You plan to stay in the home more than 3 years (past break-even)

- ✅ You have an ARM and want rate stability

- ✅ You want to consolidate high-interest debt using home equity — see our Debt Consolidation Calculator

3 Signs You Should Wait

- ❌ Your planned break-even exceeds your expected time in the home

- ❌ You have fewer than 5 years left on your current loan

- ❌ Closing costs exceed 18 months of projected savings

Quick Decision Table

| Scenario | Verdict |

|---|---|

| Rate was 7.5%, now 6.1% | ✅ Strong case to refinance |

| Rate was 6.2%, now 5.9% | ⚠️ Run the calculator first |

| 5 years left on loan | ❌ Likely not worth it |

| ARM → Fixed rate | ✅ Strongly consider it |

| Improving credit score | ✅ Shop aggressively |

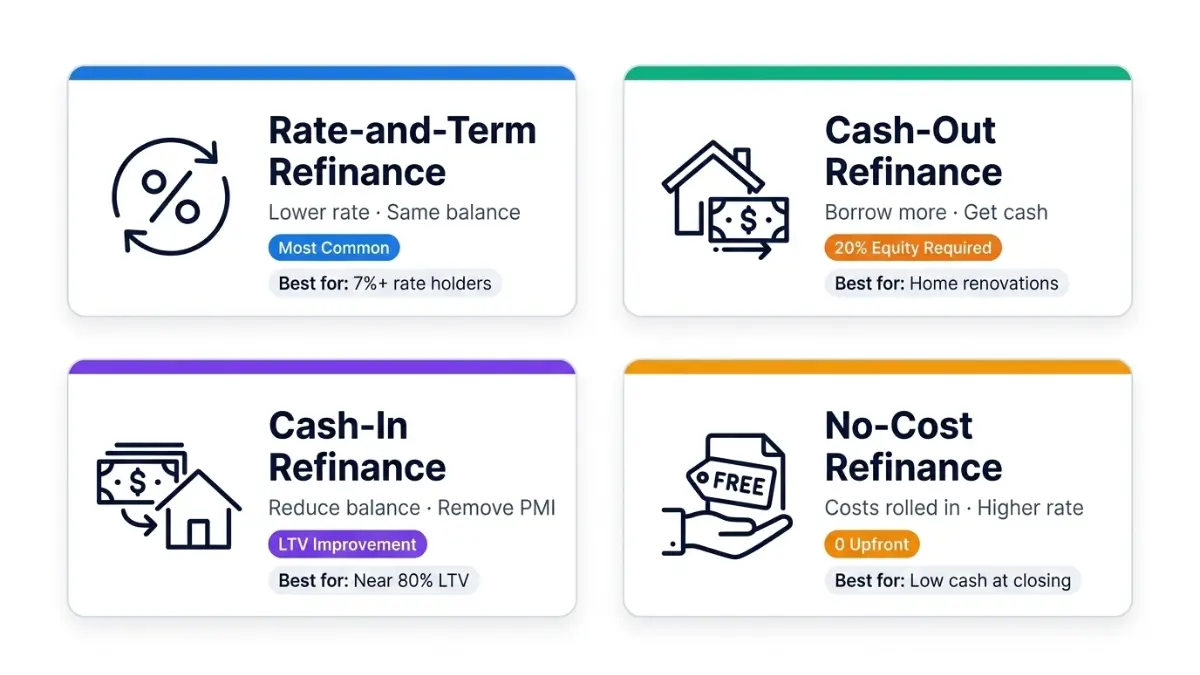

Types of Refinancing — Match the Right Type to Your Goal

Competitors list refinancing types generically. We go further: for each type, we show you exactly how to model it inside this calculator.

Rate-and-Term Refinance

The most common type. You replace your mortgage with a new one at a lower rate, shorter term, or both — without changing the loan amount.

How to model it: Enter your current balance as-is. Enter the new lower rate. Adjust the term to match your goal (shorter term = more interest savings, higher monthly payment).

Best for: Borrowers who locked in rates above 7% in 2022–2023 and want pure payment relief.

Cash-Out Refinance

You borrow more than you owe and receive the difference as cash. Minimum 20% equity required by most conventional lenders.

How to model it: Enter your desired cash amount in the cash-out field. The calculator automatically increases your new loan principal and shows the updated payment and break-even.

2026 context: Popular for home renovations as HELOC rates remain elevated. According to HUD’s FHA streamline refinance guidelines, government-backed borrowers may also qualify for specialized cash-out programs with simplified documentation.

Cash-In Refinance

You bring money to closing to reduce your loan balance. This improves your LTV ratio and can eliminate PMI.

How to model it: Enter the amount in the cash-in field. Watch your new loan principal drop, your LTV improve, and — if you cross the 80% LTV threshold — your effective monthly savings increase further by eliminating mortgage insurance.

Best for: Homeowners near the 80% LTV line who want the best possible rate.

No-Cost Refinance

Closing costs are rolled into the loan or absorbed by accepting a slightly higher rate.

How to model it: Set closing costs to $0 and manually increase your new rate by ~0.25%–0.375% to simulate the lender covering costs. This shows you the real long-term trade-off.

Expert note from Daniel Moreau, CPA/CFP: “No-cost refinancing removes the cash barrier at closing, but you’re paying for it over 30 years. Run both scenarios in the calculator. The after-tax break-even difference often surprises people.”

Real 2026 Refinance Example — Full Calculator Walkthrough

Here’s a complete real-world scenario using current March 2026 rate data. This is what your calculator output would look like.

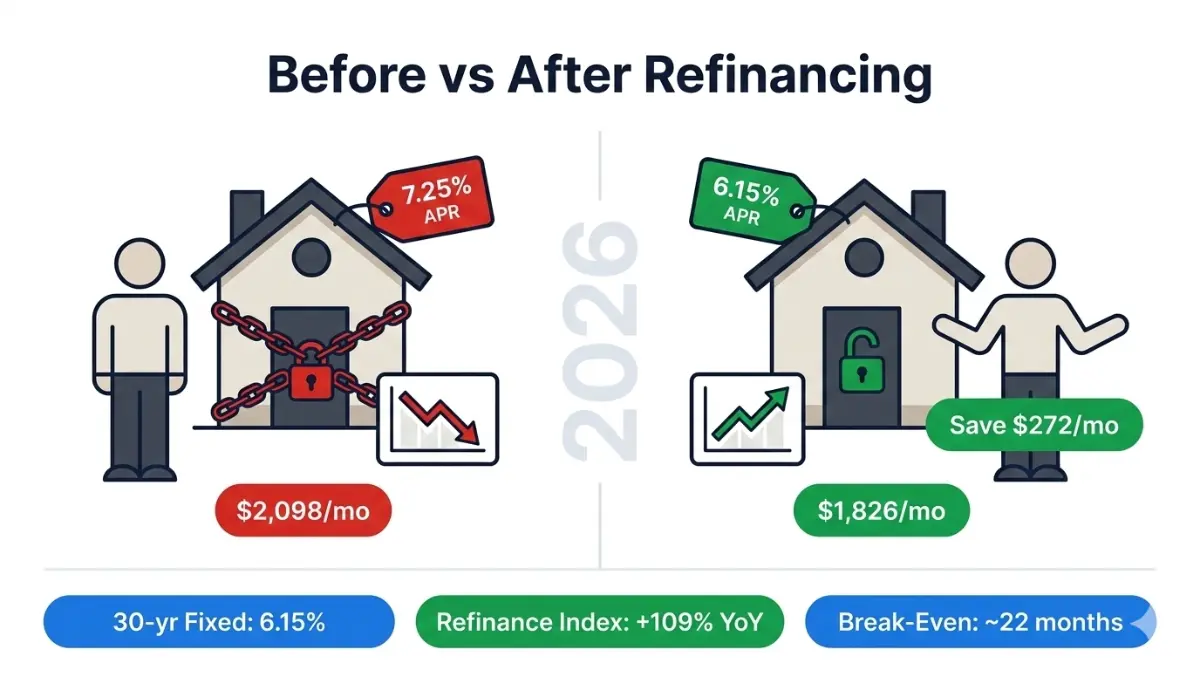

Scenario: Sarah, Dallas TX — $300,000 Mortgage, Rate 7.25%

Sarah bought her home in mid-2023 at the market peak. Her rate is 7.25% on a 30-year fixed loan. She now has 27 years remaining. Current 30-year refinance rates are at 6.15%.

| Input | Current Loan | New Refinance Loan |

|---|---|---|

| Balance | $300,000 | $300,000 |

| Rate | 7.25% | 6.15% |

| Term | 27 years remaining | 30 years |

| Closing Costs | — | $6,000 (upfront) |

Calculator Output

| Result | Value |

|---|---|

| Current monthly payment (P&I) | $2,098 |

| New monthly payment (P&I) | $1,826 |

| Monthly savings | $272/month |

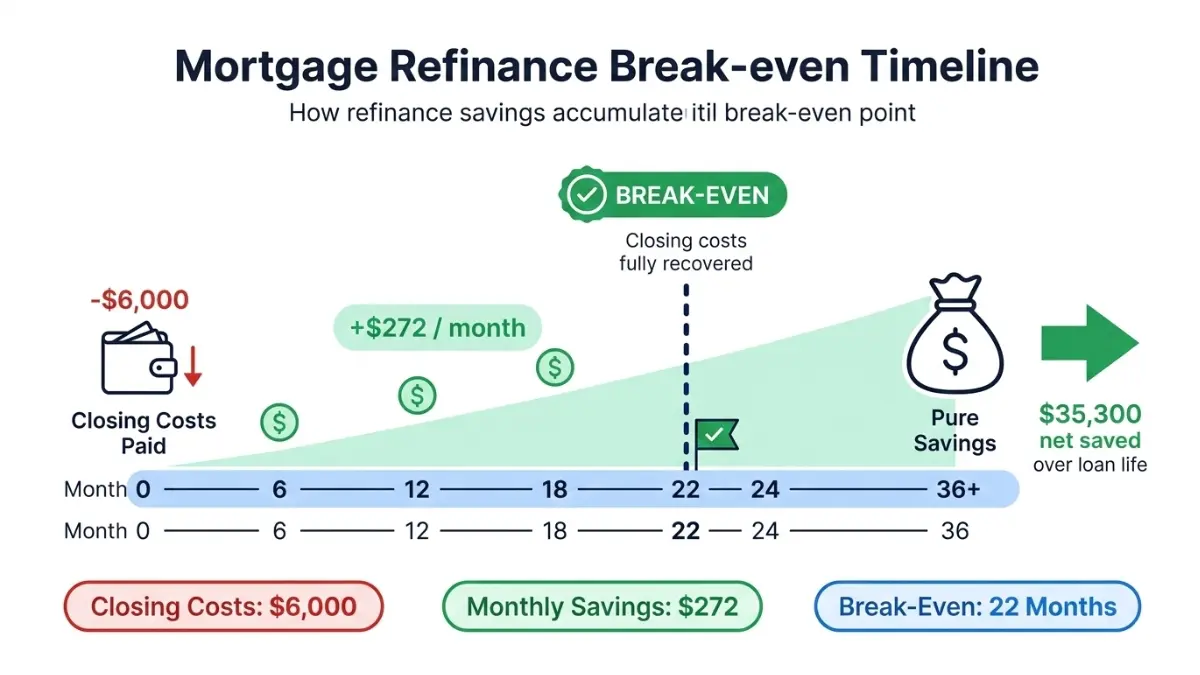

| Break-even point | 22 months |

| Break-even date | ~January 2028 |

| Total interest saved (full term) | $41,300 |

| Net savings after closing costs | $35,300 |

What This Means For You: Sarah saves $272 every month. After 22 months, she has fully recouped her $6,000 in closing costs. Over the life of the new loan, she saves $35,300 net — more than 10% of her original loan amount.

If Sarah plans to stay in the home 5+ years (and she does), this refinance is a clear financial win. You can model your own version of this scenario using our free loan calculator alongside the refinance calculator for a complete picture.

Note on investment opportunity cost, from Michael R. Thompson, CFA: “Before committing your closing cost cash to a refinance, verify the break-even aligns with your timeline. In a high-rate savings environment, $6,000 in a high-yield account also earns returns. The break-even analysis in this calculator already accounts for this trade-off when you model upfront costs vs. rolled-in costs.”

To see how your refinance savings can compound over time, run those monthly savings through our Compound Interest Calculator — the long-term wealth effect is often more powerful than the rate savings alone. And if you’re nearing retirement, consider how lower monthly payments affect your retirement runway using our Retirement Calculator.

Refinance Calculator — FAQs

1. What does a refinance calculator tell you?

It shows your new monthly payment, monthly savings, break-even period (how long until savings cover closing costs), total interest saved over the loan’s life, and an amortization schedule for both loans. Our tool also shows after-tax break-even and horizon analysis at 12, 36, 60, and 120 months.

2. How accurate is a refinance calculator?

Results are estimates based on your inputs. They assume a fixed rate and consistent payments throughout the term. Actual lender offers may vary based on your credit score, debt-to-income ratio, and property appraisal. Use results as a directional guide, then get official Loan Estimates from at least three lenders.

3. What is a good break-even period for refinancing?

Under 24 months is generally excellent. 24–36 months is solid if you plan to stay long-term. Over 48 months is risky — if you sell or refinance again before that point, you lose money on the transaction.

4. Does refinancing hurt your credit score?

Yes, slightly and temporarily. Each mortgage application generates a hard credit inquiry, which can lower your score by 5–10 points. However, multiple mortgage inquiries within a 45-day window are typically treated as one inquiry by FICO. The long-term impact of lower debt payments usually improves your score over 6–12 months.

5. What is the minimum equity needed to refinance?

For a conventional rate-and-term refinance, most lenders require at least 3%–5% equity (95–97% LTV). For a cash-out refinance, you need at least 20% equity (80% LTV maximum). FHA streamline refinances may require less — per HUD’s streamline refinance program, no appraisal is required for eligible borrowers.

6. Can I refinance if I rolled closing costs into my loan?

Yes. Your new starting balance simply reflects the higher amount. The calculator models this using the “roll into new loan” option under closing costs. Be aware that you pay interest on those rolled-in costs for the full term — visible in the total interest comparison output.

7. What is a cash-out refinance vs. a rate-and-term refinance?

A rate-and-term refinance changes only your rate and/or term — your loan balance stays the same. A cash-out refinance increases your loan balance by the amount you withdraw as cash. Rate-and-term is for saving money; cash-out is for accessing equity. Both are fully modelable in this calculator.

8. How do I calculate my refinance break-even point?

Divide your total closing costs by your monthly savings. Example: $6,000 in closing costs ÷ $272/month in savings = 22 months to break even. The calculator does this automatically — including an after-tax version if you enter your marginal tax rate.

9. Is refinancing worth it for just a 0.5% rate reduction?

It depends entirely on your loan size and break-even period. On a $400,000 loan, 0.5% saves roughly $130/month. With $5,000 in closing costs, break-even is about 38 months. If you plan to stay 5+ years, yes — it’s worth it. On a $100,000 loan, the math rarely works for only 0.5%.

10. How long does refinancing take in 2026?

According to the CFPB’s mortgage resource center, refinancing typically takes 30–45 days from application to closing. FHA and VA streamline refinances can close faster — sometimes in 2–3 weeks — due to reduced documentation requirements.

11. What refinance rate should I be targeting in 2026?

With the 30-year fixed sitting at ~6.15% in March 2026, a meaningful target for borrowers with good credit (720+) is 5.75%–6.25% depending on loan size, LTV, and term. Shop at least 3 lenders to find the best offer. Use our APR Calculator to compare real total costs across lender offers — not just the headline rate. For a deeper look at how today’s rates vary by state, see our Lowest Mortgage Rates by State guide.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.