Down Payment Calculator – Avoid PMI in 2026

Down Payment Calculator

Estimate down payment amount/% and loan amount (LTV), plus a detailed “cash to close” estimate and optional monthly payment view.

Inputs

If you roll some closing costs into the loan, cash-to-close decreases but loan amount increases.

Results

Down payment

—

Down payment %: —

Loan + LTV

—

LTV: —

Estimated cash to close

—

Purchase price: —

Monthly estimate (optional)

P&I: —

PMI: —

All-in (P&I+PMI+tax+ins+HOA): —

Cash-to-close building blocks

Closing costs (total): — • Financed: —

Prepaids/escrow: — • Credits: — • Earnest: —

Cash-to-close breakdown

| Item | Value |

|---|

Down payment scenarios (side-by-side)

| Down % | Down amount | Loan amount | LTV | P&I | PMI | All-in monthly | Cash to close |

|---|

Results appear after you click “Calculate.”

In This Article

What Is a Down Payment Calculator — And Why It Matters in 2026

A down payment calculator tells you exactly how much cash you need upfront to buy a home — including your down payment amount, loan size, LTV ratio, and estimated cash to close. It eliminates guesswork and helps you plan strategically before you ever talk to a lender.

Here’s the number most buyers don’t know: first-time buyers put down a median of just 10% in 2025, compared to 23% for repeat buyers — not the 20% most people assume. Yet crossing the 20% threshold is still the single most powerful move you can make to avoid PMI and save hundreds every month.

Use our Down Payment Calculator above to run your numbers instantly. Then use this guide to understand exactly what those numbers mean — and how to use them to buy smarter in 2026.

Before calculating your down payment, check how much home you can actually afford using our Home Affordability Calculator.

How to Use Our Down Payment Calculator (Step-by-Step)

Our calculator is built for real buyers making real decisions. Here’s how to get the most out of it.

Step 1 — Enter Your Purchase Price

Type the home price you’re targeting. Example: $350,000.

Step 2 — Choose Your Down Payment Mode

The calculator offers three input modes — a feature no competitor tool provides:

- “I know %” — Enter a percentage (e.g., 10%) and see the dollar amount instantly

- “I know amount” — Enter a dollar figure and calculate the percentage and loan amount

- “I know loan amount” — Enter your desired loan and back-calculate your required down payment

Step 3 — Enter Closing Costs

Closing costs typically run 2%–5% of the purchase price. Enter them as a percentage or a fixed dollar amount. For a $350,000 home, budget $7,000–$17,500.

Step 4 — Toggle PMI Estimate On

Check “Include PMI estimate” and enter a PMI rate (typically 0.30%–1.15% annually). This shows you exactly how much PMI adds to your monthly payment — and how much you save by avoiding it.

Step 5 — Run the Scenario Table

The built-in scenario table compares 3%, 5%, 10%, and 20% down side-by-side — showing down payment amount, loan size, LTV, monthly P&I, PMI cost, and cash to close for each. No other calculator on the internet offers this in one view.

Step 6 — Download Your CSV Report

Export your full breakdown as a CSV for your mortgage lender or financial planner.

For your full monthly payment picture after calculating your down payment, run the numbers through our Mortgage Calculator.

How Much Down Payment Do You Actually Need in 2026?

The 20% rule is a myth. The average down payment for first-time buyers is between 8% and 13%, and loan programs exist that allow as little as 0% down. What you actually need depends on your loan type, credit score, and financial goals.

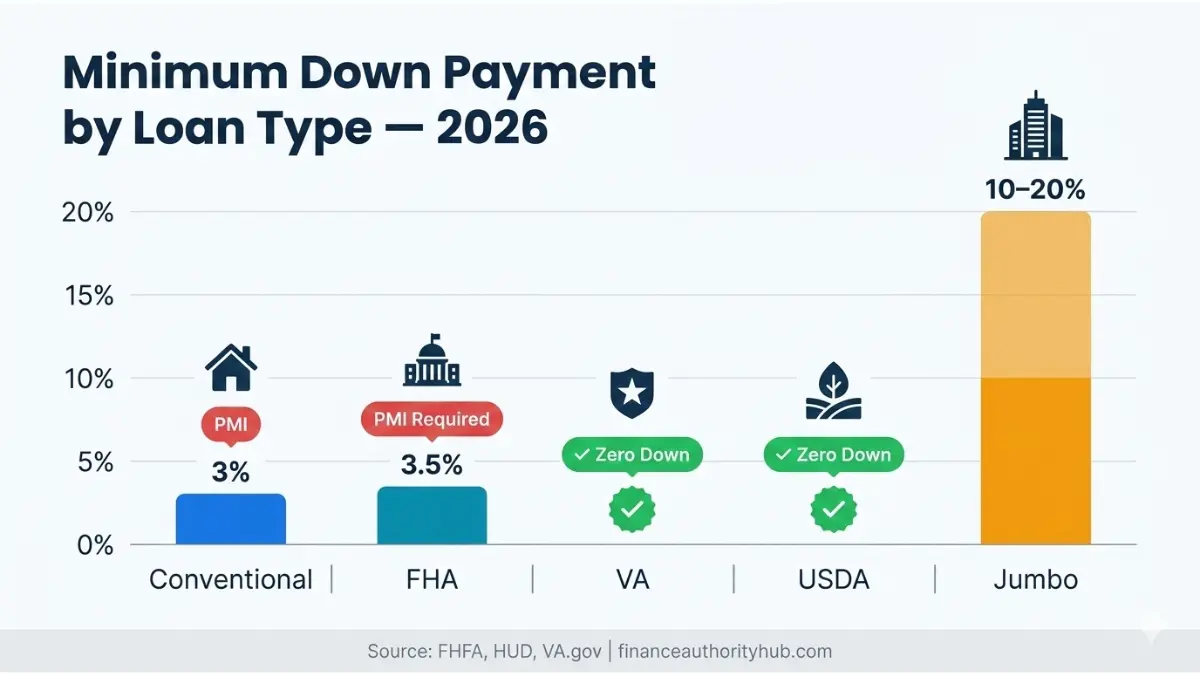

Down Payment by Loan Type — 2026 Comparison Table

| Loan Type | Min. Down Payment | PMI Required? | Best For |

|---|---|---|---|

| Conventional | 3% | Yes (if <20%) | Buyers with 620+ credit score |

| FHA | 3.5% | MIP required | Lower credit scores (580+) |

| VA | 0% | No | Veterans & active military |

| USDA | 0% | No | Rural area buyers |

| Jumbo | 10%–20% | Varies | Homes above $832,750 |

Note: The conforming loan limit for a single-family home in most U.S. counties in 2026 is $832,750, set by the FHFA. Loans above this threshold are jumbo loans with stricter down payment requirements.

Real Dollar Amounts by Scenario

| Down % | $300K Home | $400K Home | $500K Home |

|---|---|---|---|

| 3% | $9,000 | $12,000 | $15,000 |

| 5% | $15,000 | $20,000 | $25,000 |

| 10% | $30,000 | $40,000 | $50,000 |

| 20% | $60,000 | $80,000 | $100,000 |

Down Payment by Buyer Age — 2026 NAR Data

Homebuyers ages 22–30 put down 6%, buyers ages 31–40 put down 10%, and buyers ages 41–55 put down 13%. If you’re in your 20s or 30s, you’re already on track — you do not need 20% to get started.

The Consumer Financial Protection Bureau’s mortgage guide is the most reliable government resource for understanding your down payment options across all loan types.

Planning your first purchase? Read our complete Buy First Home 2026 Guide for the full roadmap.

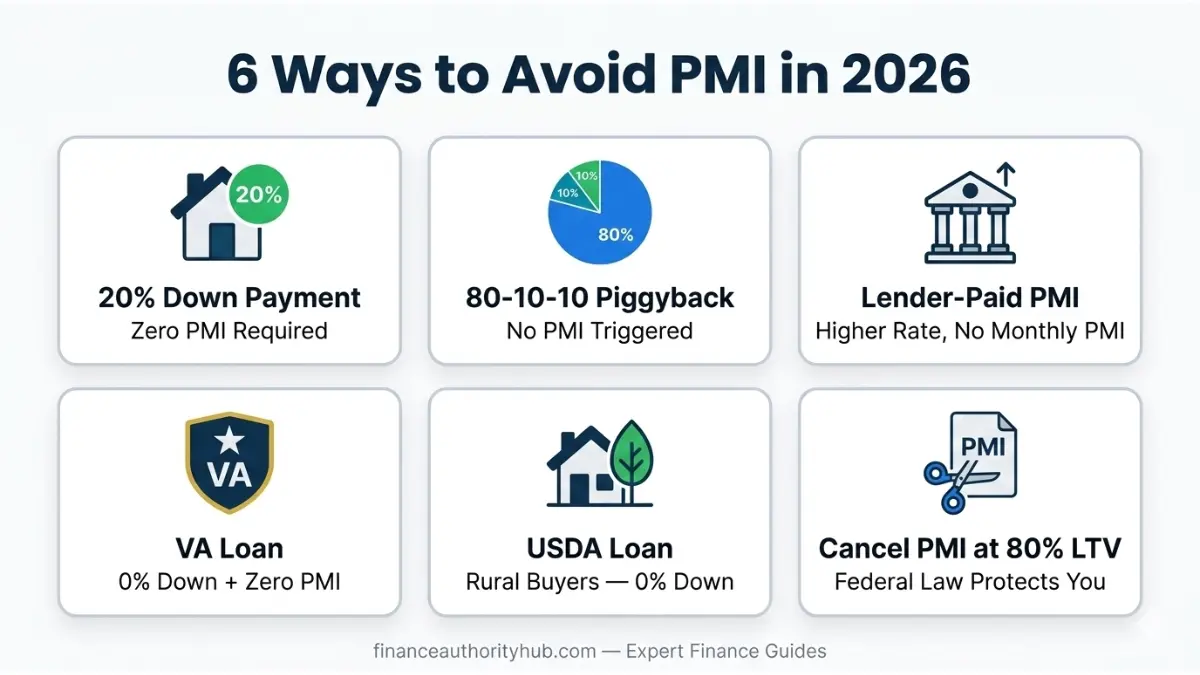

How to Avoid PMI in 2026: 6 Proven Strategies

This is the section no competitor has built properly. PMI is not inevitable — and eliminating it can save you $105–$245 every single month.

What Does PMI Actually Cost?

PMI generally ranges between 0.3% and 2% of the original loan amount per year. On a $350,000 loan, that equals $1,050–$7,000 per year — or $87–$583 per month added to your mortgage payment. That money protects your lender, not you.

🆕 2026 Tax Update: Congress reinstated the PMI deduction in 2025 and made it permanent — starting with the 2026 tax year, eligible borrowers can claim it when they file in spring 2027. This changes the math on whether PMI is worth carrying short-term.

Strategy 1 — Put 20% Down (The Clean Break)

The simplest route. If you buy a home for $400,000 with a conventional loan, you need a down payment of at least $80,000 to avoid paying PMI. Use our scenario table above to calculate your exact 20% target.

Strategy 2 — Piggyback Loan (80-10-10)

Take two loans simultaneously — an 80% primary mortgage and a 10% second loan — and put 10% down yourself. Your primary loan stays at 80% LTV, so no PMI is triggered. The second loan typically carries a higher rate, so run the math carefully.

Strategy 3 — Lender-Paid PMI (LPMI)

Your lender pays the PMI upfront in exchange for a slightly higher interest rate on your mortgage. You avoid the monthly PMI line item, but the higher rate is permanent until you refinance. Best for buyers who plan to sell or refinance within 5–7 years.

Strategy 4 — VA Loan (Zero Down, Zero PMI)

VA loans require no down payment and no PMI for eligible veterans and active service members. There is a one-time funding fee (typically 2.15%–3.3%), which can be rolled into the loan. This is the most powerful first-time buyer tool available in the U.S. for those who qualify.

Strategy 5 — USDA Loan (Rural Buyers)

USDA loans offer zero down payment for buyers in eligible rural areas. There is an upfront guarantee fee (1% of the loan) and an annual fee (0.35%), both significantly cheaper than PMI on a conventional loan.

Strategy 6 — Request PMI Cancellation at 80% LTV

Already have a loan with PMI? You don’t have to wait. Under the Homeowners Protection Act, federal law requires lenders to automatically cancel PMI when the mortgage balance drops to 78% of the home’s purchase price. You can request cancellation earlier, as soon as your balance hits 80%.

What This Means For You: If your home has appreciated in value, a new appraisal may push your LTV below 80% even without making extra payments — triggering PMI removal years ahead of schedule. Explore whether refinancing makes sense using our Mortgage Refinance Calculator.

PMI Cancellation Timeline — $350,000 Home at 6.5% Rate

| Down Payment | LTV at Closing | Est. Months to Reach 80% LTV | Monthly PMI Cost |

|---|---|---|---|

| 3% ($10,500) | 97% | ~120 months | ~$168/mo |

| 5% ($17,500) | 95% | ~96 months | ~$150/mo |

| 10% ($35,000) | 90% | ~60 months | ~$115/mo |

| 20% ($70,000) | 80% | PMI not required | $0 |

Fannie Mae’s official PMI guide explains exactly when and how PMI is calculated on conventional loans backed by government-sponsored enterprises.

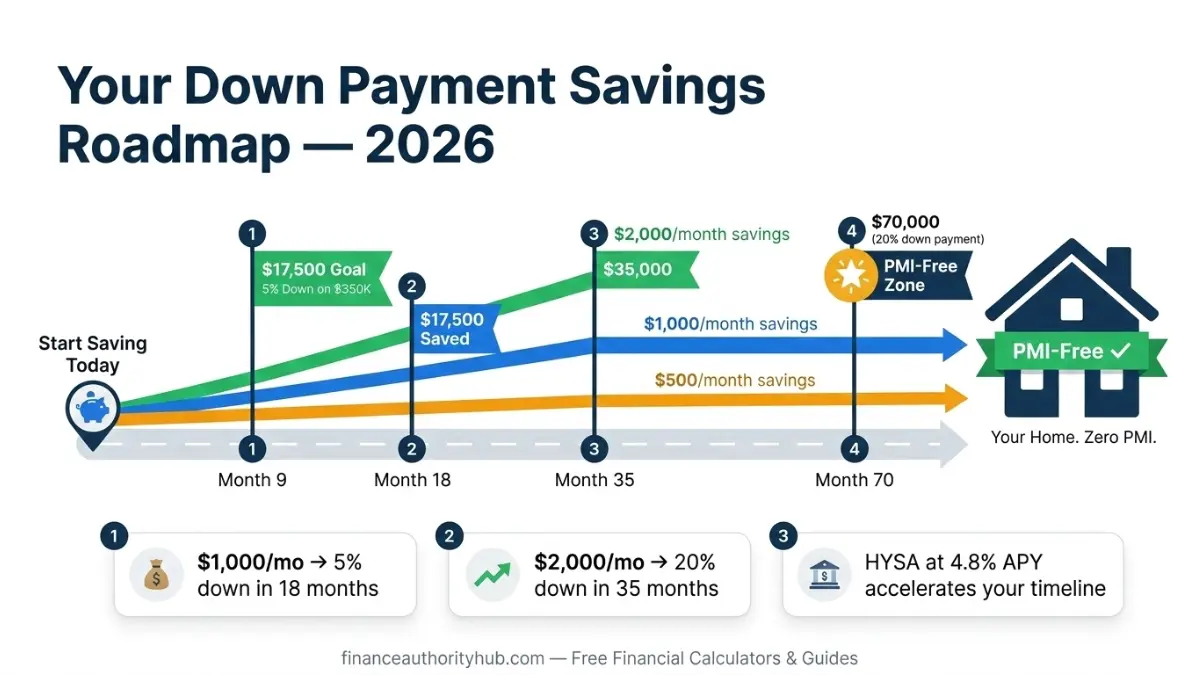

How to Save for a Down Payment Fast in 2026

Knowing your target number is step one. Getting there is step two. Here’s how buyers are doing it in 2026.

Real Savings Timeline

| Monthly Savings | $17,500 (5% on $350K) | $35,000 (10% on $350K) | $70,000 (20% on $350K) |

|---|---|---|---|

| $500/mo | 35 months | 70 months | 140 months |

| $1,000/mo | 18 months | 35 months | 70 months |

| $2,000/mo | 9 months | 18 months | 35 months |

Case Example — First-Time Buyer, Chicago, 2026: Jasmine, 29, targets a $340,000 condo. Her goal: 5% down = $17,000. She opens a high-yield savings account earning 4.8% APY, saves $1,500/month, and hits her target in 11 months. She uses our down payment calculator to confirm her cash-to-close total ($17,000 down + $8,500 closing costs = $25,500 needed), then applies for a conventional loan with PMI — with a plan to cancel it at month 48. See our High-APY Banks guide for where to park your savings right now.

Down Payment Assistance Programs — 2026

Many buyers don’t realize they qualify for free money. Down payment assistance programs are typically geared toward first-time and low-to-moderate income buyers, and some come as grants or forgivable loans — meaning you never repay them.

Types of assistance available:

- Grants — Free money, no repayment required

- Forgivable loans — Written off after 3–5 years in the home

- Deferred payment loans — Repaid only when you sell or refinance

- Matched savings programs — Employer or government matches your savings

Find every program available in your state through the HUD homebuying resource center — the most comprehensive government database of down payment assistance by location.

Additional ways to build your down payment faster:

- Use gift funds from a family member (document properly — lender will require a gift letter)

- Roll in your tax refund — the average 2026 refund is over $3,000 (see our Tax Refund 2026 Guide)

- Apply an inheritance or bonus directly to your savings account

- Explore your Savings Calculator to model exactly how long your savings plan takes

If you’re carrying high-interest debt alongside your savings goal, use our Debt-to-Income Ratio Calculator — most lenders require a DTI below 43% for mortgage approval.

For a complete down payment assistance guide with state-specific programs, read our dedicated Down Payment Help Guide 2026.

Down Payment Calculator FAQs

1. What is a good down payment on a house in 2026?

A good down payment is 20% to eliminate PMI — but 5%–10% is realistic and sufficient for most buyers. First-time buyers put down a median of just 9%–10%, and programs exist that allow as little as 3% for conventional loans and 3.5% for FHA loans.

2. What is the minimum down payment for a $300,000 house?

The minimum is $9,000 (3%) on a conventional loan or $10,500 (3.5%) on an FHA loan. VA and USDA loans allow $0 down for eligible buyers. PMI will apply unless you reach 20% ($60,000)

3. How does down payment affect my monthly mortgage payment?

A larger down payment means a smaller loan, lower monthly payments, and no PMI. On a $300,000 home at 4%, putting 20% down instead of 10% saves approximately $300 per month. Use our Amortization Calculator to see the full impact over 30 years.

4. What is PMI and how much does it cost per month?

PMI (Private Mortgage Insurance) protects your lender if you default — it does not protect you. The average annual PMI cost is $30–$70 per $100,000 borrowed, according to Freddie Mac — meaning a $350,000 loan costs $105–$245/month in PMI alone.

5. Can I avoid PMI without a 20% down payment?

Yes — through piggyback loans, VA loans, USDA loans, or lender-paid PMI. You can also request PMI removal at 80% loan-to-value or wait for automatic cancellation at 78%. See our full 6-strategy guide above.

6. What is the difference between down payment and closing costs?

Down payment is the upfront equity portion of the home price. Closing costs are separate fees — typically 2%–5% of the purchase price — covering appraisal, title insurance, lender fees, and prepaid taxes. Both are required at closing. Our calculator shows both in its cash-to-close breakdown.

7. How does LTV ratio affect my mortgage rate?

Lower LTV = lower risk for lenders = better interest rate for you. A buyer with 20% down (80% LTV) typically qualifies for a lower rate than one with 5% down (95% LTV). Even a 0.25% rate reduction on a $350,000 loan saves over $17,000 in interest over 30 years.

8. Can I use gift money for a down payment?

Yes, most loan programs allow gift funds from family members. Your lender will require a signed gift letter confirming the money is not a loan. FHA, VA, USDA, and conventional loans all permit gift funds with proper documentation.

9. What credit score do I need to put 3% down?

You need a minimum 620 credit score for a 3% conventional loan, or 580 for a 3.5% FHA loan. Higher scores unlock better rates and lower PMI costs. Check your score with our Credit Score Calculator before applying.

10. Is a 10% down payment enough in 2026?

Yes — 10% down is a solid, realistic target for most first-time buyers. First-time buyers put down only 13% on average, and putting 10% down leaves cash reserves intact for repairs, moving costs, and emergencies. You’ll pay PMI until reaching 20% equity, but it can be canceled.

11. How does this down payment calculator work?

Enter your purchase price, choose your input mode (%, amount, or loan amount), add closing costs, and click Calculate. The tool instantly outputs your down payment amount, LTV ratio, estimated PMI, and full cash-to-close estimate. Toggle the scenario table to compare 3%, 5%, 10%, and 20% down side-by-side. Download your results as a CSV for your records.

⚠️ Disclaimer: This article and calculator are provided for educational and informational purposes only. They do not constitute financial, mortgage, legal, or tax advice. Down payment requirements, PMI rates, loan limits, and assistance programs vary by lender, state, and individual financial situation. All calculations are estimates only. Always consult a licensed mortgage professional, HUD-approved housing counselor, or CFPB-certified financial advisor before making any home-buying decisions. PMI tax deduction eligibility depends on your individual tax situation — consult a qualified tax professional.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.