Credit Card Payoff Calculator – See Your Debt-Free Date

Credit Card Payoff Calculator

Estimate payoff time, payoff date, total interest, and a full amortization schedule. Includes “Pay off in N months” mode and optional comparison vs minimum payments.

Inputs

Results

Payoff

—

Months to payoff: —

Costs

Total interest: —

Total paid: —

Final payment: —

Payment setup

Balance: —

APR: —

Rate detail: —

First month split

Interest: —

Principal: —

Payment used: — + Extra: —

Comparison vs minimum payments

Minimum-payment payoff time

— months

Minimum total interest: —

Minimum total paid: —

Estimated savings (your plan)

—

Time saved: —

Yearly summary

| Year | Paid | Principal | Interest | Extra paid | Ending balance |

|---|

Monthly payoff schedule

| Month | Payment | Principal | Interest | Extra paid | Remaining balance |

|---|

Educational estimate. Many issuers compute interest using a daily periodic rate (APR ÷ 365 or 360) and billing-cycle day counts can vary. [web:31][web:33]

In This Article

Use our free credit card payoff calculator above to instantly see your exact debt-free date, total interest cost, and a full monthly payment schedule — in under 30 seconds.

Americans now owe $1.277 trillion in credit card debt, and the average APR hit 25.2% in 2024 — the highest since 2015, according to the CFPB’s 2025 Consumer Credit Card Market Report. If you’re carrying a balance, knowing your exact payoff date isn’t optional — it’s urgent.

How to Use the Credit Card Payoff Calculator (Results in 30 Seconds)

Our credit card payoff calculator is built to give you real answers — not guesses.

4 Steps to Your Debt-Free Date:

- Enter your current balance — the exact amount you owe today

- Enter your APR — find it on your card statement or app

- Choose your payment mode — fixed monthly payment, payoff in N months, or minimum payments

- Hit Calculate — your payoff date, total interest, and full amortization schedule appear instantly

| Feature | What It Shows You |

|---|---|

| Debt-Free Date | The exact month and year you’ll be out of debt |

| Total Interest Cost | Real dollar amount lost to interest over time |

| Monthly Schedule | Every payment broken down — downloadable as CSV |

| Minimum Payment Comparison | Side-by-side: your plan vs. paying minimums only |

| Daily vs. Monthly Interest Method | Matches how your actual bank calculates charges |

What makes this calculator different from every competitor: It lets you choose between the monthly approximation method (APR ÷ 12) and the daily periodic rate method (APR ÷ 365 × billing days) — the exact same method most U.S. issuers use. No other free calculator in the top 10 offers this level of precision.

If you’re also managing other debts, explore our Debt Consolidation Calculator to compare consolidation vs. individual card payoff strategies.

The Minimum Payment Trap — Why Most Americans Never Escape Credit Card Debt

This is the most expensive mistake in personal finance — and almost nobody talks about it.

The share of cardholders making only the minimum payment is at its highest level since at least 2015. In 2024, consumers were assessed $160 billion in interest charges, up from $105 billion in 2022.

What Minimum Payments Actually Cost You (2026 Real Numbers)

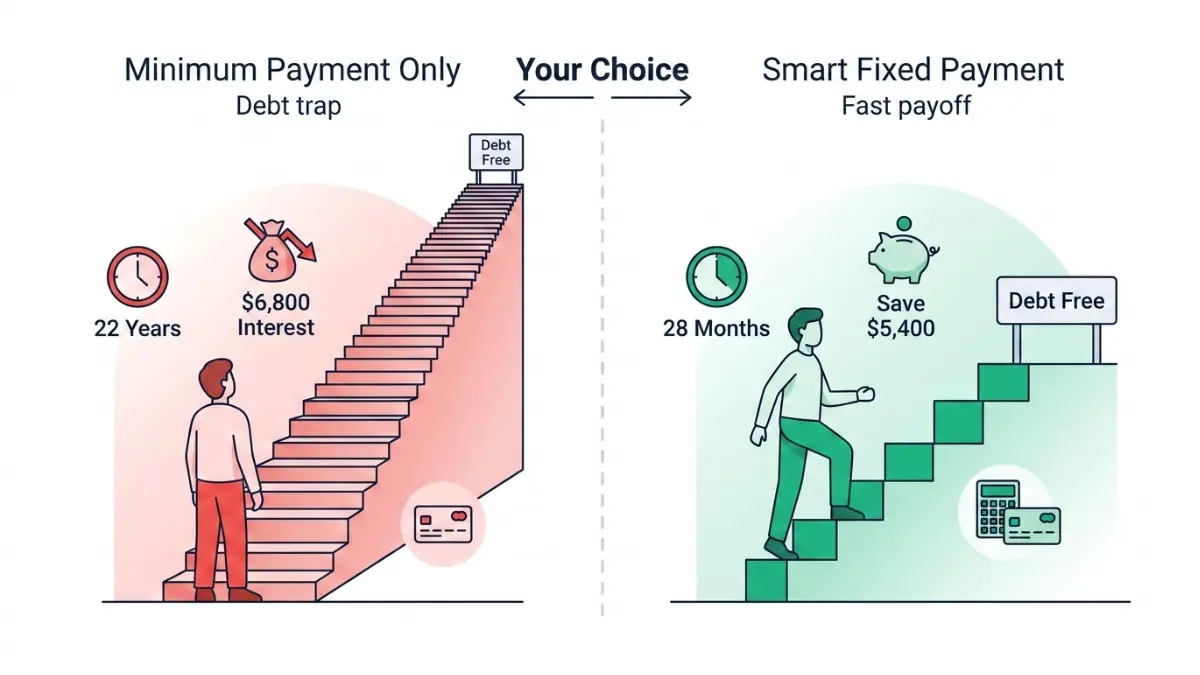

Here’s what happens on a $5,000 balance at 24.99% APR:

| Payment Strategy | Monthly Payment | Payoff Time | Total Interest Paid |

|---|---|---|---|

| Minimum only (~2%) | ~$100 (decreasing) | 22+ years | $6,800+ |

| Fixed $150/month | $150 | 4.5 years | $2,900 |

| Fixed $250/month | $250 | 2.1 years | $1,400 |

| Pay off in 12 months | ~$470 | 12 months | ~$640 |

Key Takeaway: That $5,000 vacation charged in 2024 could cost you over $11,800 by the time it’s fully paid off on minimum payments alone.

How the Minimum Payment Trap Works

Credit card issuers calculate your minimum as a small percentage of your balance — typically 1–2%, with a floor of around $25. As your balance decreases, so does your minimum payment. This creates a slow-motion debt spiral that can last two decades.

The CFPB’s credit card debt guidance confirms that even small increases above the minimum payment can dramatically cut your payoff timeline.

How Our Calculator Exposes the Trap

Toggle the “Compare vs minimum payments” checkbox in the calculator. It runs a parallel simulation and shows you exactly:

- How many extra months (often years) you’d stay in debt on minimums

- The exact dollar difference in total interest between the two plans

- Your interest savings by paying even $50–$100 more per month

No competitor calculator — not Bankrate, not Experian, not Calculator.net — shows this side-by-side comparison. You get it here, free.

Debt Avalanche vs. Debt Snowball — Which Credit Card Payoff Strategy Wins in 2026?

Choosing the wrong credit card debt payoff strategy can cost you thousands. Here’s the data-backed comparison every financial expert knows — but most websites explain poorly.

Debt Avalanche Method — Maximum Interest Savings

How it works: Pay minimums on all cards. Throw all extra money at the highest-APR card first.

- Best for: People motivated by saving the most money

- Result: Lowest total interest paid across all cards

- Challenge: Progress feels slow if the highest-APR card has a large balance

Debt Snowball Method — Maximum Psychological Momentum

How it works: Pay minimums on all cards. Attack the smallest balance first, regardless of APR.

- Best for: People who need early wins to stay motivated

- Result: Fastest emotional progress, slightly higher total interest

- Challenge: May cost more in interest if small-balance cards have low APRs

Fixed Extra Payment Accelerator — The Hybrid Winner

How it works: Add a fixed extra amount ($50, $100, $200) to your normal payment every month, consistently.

- Best for: Most Americans with 1–2 cards

- Result: Predictable payoff date, significant interest savings

- Use our calculator: Set “Extra payment (monthly)” to model your exact savings

Side-by-Side Strategy Comparison

| Strategy | Total Interest (on $7,886 avg. balance at 22.3% APR) | Payoff Speed | Difficulty |

|---|---|---|---|

| Avalanche | Lowest | Fast | Medium |

| Snowball | Medium | Medium | Easy |

| Fixed Extra (+$100/mo) | Medium-Low | Fast | Easy |

| Minimum Only | Highest | Slowest (10–20 yrs) | Deceptively Easy |

What This Means For You:

- 1 card? → Use Fixed Payment mode in our calculator. Model 3 different payment amounts.

- Multiple cards? → Start with the highest APR first (Avalanche). Track progress card by card.

- Need motivation? → Target the smallest balance first (Snowball), then switch to Avalanche.

For a deeper look at both strategies with real examples, see our dedicated guide on Debt Snowball vs. Debt Avalanche.

The CFPB’s debt consolidation guidance also recommends contacting individual creditors to negotiate lower rates before choosing any payoff strategy — a step most people skip.

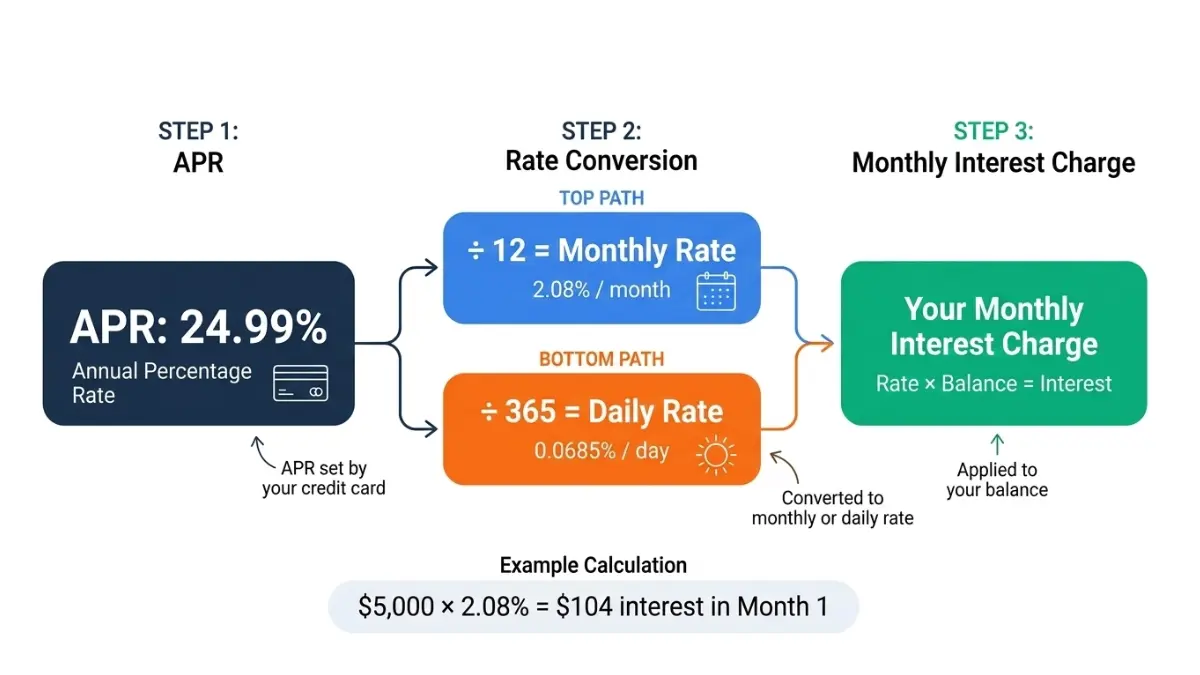

How Credit Card Interest Is Actually Calculated (What Your Bank Doesn’t Tell You)

Understanding this one concept will change how you use our credit card interest calculator — and could save you hundreds.

Monthly vs. Daily Periodic Rate — The Hidden Difference

Most Americans assume interest is calculated once a month. The reality: most major U.S. card issuers use a daily periodic rate, meaning interest compounds every single day.

| Method | Formula | Example at 24.99% APR |

|---|---|---|

| Monthly Rate | APR ÷ 12 | 2.0825% per month |

| Daily Periodic Rate | APR ÷ 365 | 0.06847% per day |

Why it matters: Over 30 billing days, the daily method produces slightly different interest than APR/12. On a $5,000 balance, this can mean $10–$30 difference per year. Multiply that across years of debt, and the gap grows.

Our calculator is the only free tool that lets you switch between both methods to match your exact card issuer’s calculation.

How to Use the APR Setting in Our Calculator

- Check your credit card statement or issuer’s website for your exact APR

- Select “Daily periodic rate” if your issuer is a major U.S. bank (Chase, Citi, Bank of America, Capital One)

- Enter your billing cycle days (usually 28–31)

- Select day-count base: 365 for most U.S. cards, 360 for some older accounts

What Is a Good APR for a Credit Card in 2026?

The average APR for credit cards accruing interest in Q4 2025 was 22.30%, while new credit card offers average 23.77% today.

| Credit Profile | Typical APR Range (2026) |

|---|---|

| Excellent (750+) | 18% – 21% |

| Good (700–749) | 21% – 24% |

| Fair (650–699) | 24% – 27% |

| Poor (below 650) | 27% – 31%+ |

To understand exactly how APR differs from your interest rate and what it really costs you, read our in-depth guide on APR vs. Interest Rate.

The Federal Reserve’s G.19 Consumer Credit Report tracks average APRs monthly and is the most authoritative source for benchmark rate data in the U.S.

7 Expert-Backed Ways to Pay Off Credit Card Debt Faster in 2026

Use these strategies alongside the credit card payoff calculator above. Each one is modeled with real numbers — not theory.

1. Use a Balance Transfer Card (0% APR Window)

What it does: Moves your high-APR balance to a new card with 0% intro APR — typically 12 to 21 months. Interest stops. Every dollar you pay reduces principal.

Key Takeaway: On a $5,000 balance, eliminating 18 months of 24.99% interest saves approximately $1,875. Use our APR Complete Guide to calculate your exact savings before applying.

2. Add Even $50 Extra Per Month — Calculator Proof

On a $5,000 balance at 24.99% APR with a $150 fixed payment:

- Without extra: Payoff in 54 months, $2,900 interest

- With $50 extra ($200 total): Payoff in 38 months, $1,950 interest

- Savings: $950 and 16 months — from just $50 more per month

Enter these numbers in our calculator right now. The result will surprise you.

3. Debt Consolidation Loan Strategy

A personal loan at 10–14% APR used to pay off cards at 24.99% cuts your interest rate nearly in half. Use our Debt Consolidation Calculator to model your exact monthly savings and total interest reduction before contacting any lender.

4. Biweekly Payment Hack

Instead of one monthly payment, make half-payments every two weeks. Result: 26 half-payments per year = 13 full payments instead of 12. That’s one free extra payment annually — costing you nothing extra in monthly cash flow.

5. Negotiate Your APR Directly

Call your card issuer. Ask for a rate reduction. This works more often than people realize, especially if you have a good payment history. Many credit card companies are willing to offer lower minimum monthly payments, waive certain fees, or reduce your interest rate for cardholders facing financial difficulty.

6. Automate Your Payments

Set your payment to auto-debit 3–5 days before the due date. This eliminates late fees (average $32 per incident) and protects your credit score — which directly affects future APR offers.

7. Use a Payoff Schedule — Download CSV from Our Calculator

Once you calculate your payoff plan, download the monthly CSV schedule from our tool. Print it. Track it. Cross off each month as you pay. Research consistently shows visible progress is one of the strongest behavioral drivers of debt payoff success.

If you’re struggling with multiple debts beyond credit cards, our guide on How to Pay Off Debt Fast covers a systematic multi-debt elimination framework used by certified financial planners.

Expert Insight: “Most clients who commit to just $100 extra per month on their credit card are completely debt-free 3 to 4 years sooner than they expected — and often save over $2,000 in interest.” — Laura M. Bennett, CFP®, Senior Financial Advisor, financeauthorityhub.com

Frequently Asked Questions — Credit Card Payoff Calculator

1. How do I use the credit card payoff calculator?

Enter your current balance, APR, and monthly payment amount, then click Calculate. The tool instantly shows your debt-free date, total interest, and a complete month-by-month payoff schedule.

2. What happens if I only make minimum payments?

Your balance barely moves. On a $5,000 balance at 24.99% APR, paying only the minimum could take over 20 years and cost more than $6,800 in interest alone — more than the original debt.

3. How much interest will I pay on my credit card?

Use our calculator for your exact figure. As a reference: in 2024, U.S. consumers paid $160 billion in credit card interest charges — an average of over $1,000 per indebted household annually.

4. What is a good monthly payment to pay off credit card debt fast?

Target a payment that covers at least 2–3x your minimum payment. For most balances, paying 5–10% of your balance monthly will get you debt-free within 12–24 months.

5. Does paying more than the minimum really help?

Dramatically. Even $50 extra monthly on a $5,000 balance can cut your payoff time by over a year and save hundreds in interest. Use the extra payment field in our calculator to model your exact scenario.

6. What is the fastest way to pay off credit card debt?

The fastest method is a combination of a balance transfer to a 0% APR card + maximum extra payments during the promotional window. Our 0% APR Credit Cards guide covers the best options for 2026.

7. What is the difference between APR and interest rate on a credit card?

For credit cards, APR and interest rate are effectively the same — unlike mortgages, where APR includes fees. Your monthly interest charge = (APR ÷ 12) × balance. Our APR vs. Interest Rate guide explains this in full detail.

8. Can I pay off my credit card early without penalty?

Yes, always. Federal law prohibits prepayment penalties on credit cards. Paying early or paying more than the minimum is always in your favor — there are zero penalties.

9. How does a balance transfer affect my payoff timeline?

It can dramatically accelerate it. Transferring a $5,000 balance from 24.99% to a 0% card for 18 months means all of your payment goes to principal — not interest. Model the exact impact using our Debt Consolidation Calculator.

10. Is this credit card payoff calculator free to use?

Yes — 100% free, with no login, no sign-up, and no limits. Use it as many times as you need with different scenarios.

⚠️ Disclaimer: This Credit Card Payoff Calculator and all content on this page are provided for educational and informational purposes only. Results are mathematical estimates based on the inputs provided and do not account for changes in interest rates, fees, or credit card terms. This is not financial, legal, or tax advice. Individual results will vary based on your specific card issuer’s billing methods. Consult a Certified Financial Planner (CFP®) or licensed financial advisor for personalized debt management guidance. Visit financeauthorityhub.com for full terms and conditions.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.