Term Insurance: Real Costs Most People Never See

Most people overpay for term insurance — or skip it entirely. See the real 2026 premiums by age, hidden charges agents hide, and expert picks that actually protect your family.

In This Article

If you died tomorrow, would your family be financially protected — or financially destroyed?

Term insurance is the most affordable way to answer that question with confidence. A healthy 30-year-old can secure $500,000 in coverage for as little as $22 per month. Yet according to research cited by Guardian Life, 82% of Americans overestimate its cost — and 60% who skip it cite price as the reason.

That disconnect costs families everything.

This guide exposes what competitors and agents never fully explain: the real costs, the hidden charges, the claim traps, and exactly how to buy smarter in 2026.

What Is Term Insurance? (The 60-Second Answer)

Term insurance is a life insurance policy that pays a tax-free death benefit to your beneficiaries if you die within a set period — called the “term.” If you outlive the policy, no benefit is paid and coverage ends.

That’s it. No cash value. No investment component. Pure, affordable protection.

According to the National Association of Insurance Commissioners (NAIC), term insurance is designed specifically for people who need coverage for a defined period — such as while raising children, paying a mortgage, or replacing income during peak earning years.

Three things every buyer must know upfront:

- It’s temporary — policies run 10, 15, 20, 25, or 30 years

- It’s affordable — far cheaper than whole or permanent life insurance

- It’s pure protection — your premium buys coverage only, nothing else

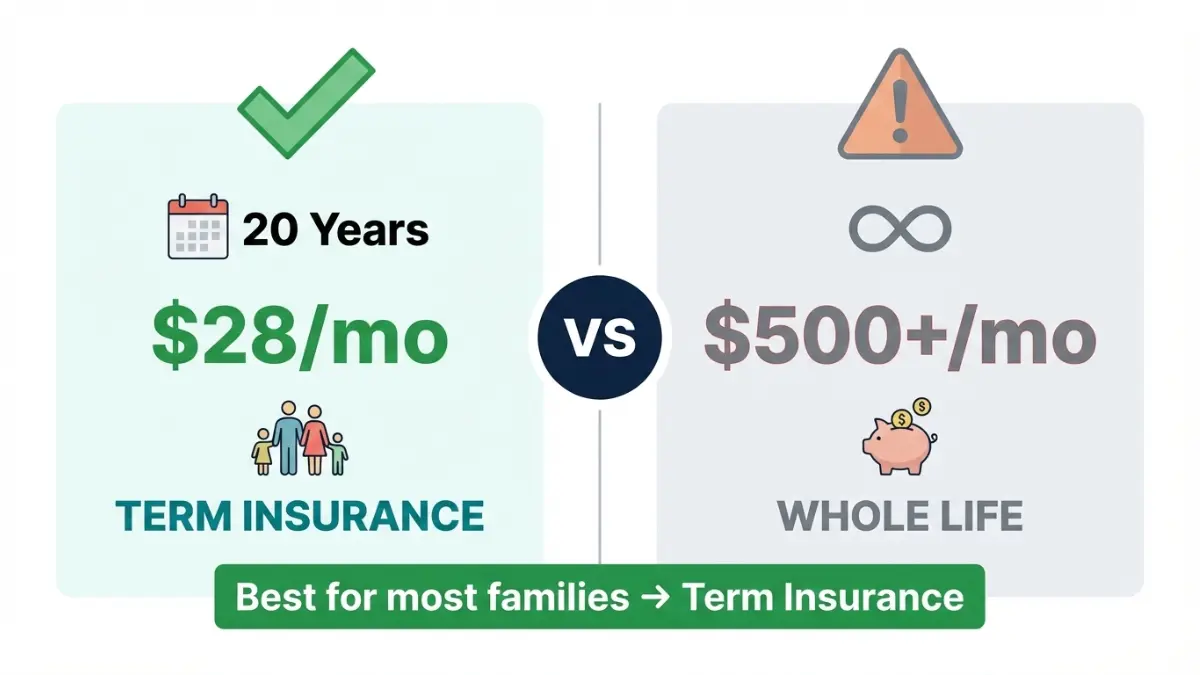

Term Insurance vs. Whole Life: Quick Comparison

| Feature | Term Insurance | Whole Life Insurance |

|---|---|---|

| Coverage period | 10–30 years | Lifetime |

| Monthly cost (age 30, $500K) | ~$22–$28 | ~$400–$600 |

| Cash value | ❌ None | ✅ Builds over time |

| Death benefit | ✅ Tax-free payout | ✅ Tax-free payout |

| Best for | Families, mortgage holders | Estate planning, high earners |

| Simplicity | ✅ Very simple | ⚠️ Complex |

| Verdict for most Americans | ✅ Recommended | ⚠️ Only for specific needs |

For a deeper look at permanent coverage alternatives, see our full guide on whole life insurance and how it compares.

Term Insurance Real Costs in 2026 — What You’re Quoted vs. What You Actually Pay

Here’s where most guides fail you. They show the sticker price. We show the full price — including the charges nobody warns you about.

2026 Premium Benchmark Table

20-Year Term Policy | Non-Smoker | Preferred Health Class

| Age | Gender | $250,000 Coverage | $500,000 Coverage | $1,000,000 Coverage |

|---|---|---|---|---|

| 25 | Male | ~$13/mo | ~$22/mo | ~$38/mo |

| 25 | Female | ~$11/mo | ~$18/mo | ~$32/mo |

| 30 | Male | ~$15/mo | ~$28/mo | ~$48/mo |

| 30 | Female | ~$13/mo | ~$23/mo | ~$42/mo |

| 35 | Male | ~$20/mo | ~$35/mo | ~$62/mo |

| 35 | Female | ~$17/mo | ~$29/mo | ~$52/mo |

| 40 | Male | ~$32/mo | ~$55/mo | ~$98/mo |

| 40 | Female | ~$26/mo | ~$45/mo | ~$84/mo |

| 45 | Male | ~$52/mo | ~$88/mo | ~$162/mo |

| 45 | Female | ~$42/mo | ~$72/mo | ~$138/mo |

| 50 | Male | ~$85/mo | ~$145/mo | ~$265/mo |

| 50 | Female | ~$68/mo | ~$115/mo | ~$215/mo |

Sources: Industry average data from major U.S. carriers, 2026. Actual rates vary by state, health classification, and carrier underwriting.

Key insight: Waiting just 10 years — from age 30 to 40 — nearly doubles your monthly premium for the same coverage. Every year you delay costs money.

⚠️ The Hidden Costs Most People Never See

This is what NerdWallet, Bankrate, and Investopedia skip. These charges can quietly inflate your total insurance cost by 15–30%:

1. Monthly vs. Annual Billing Surcharge Paying monthly instead of annually adds 5–8% to your total cost. On a $500K policy at age 35, that’s $25–$45 extra per year — every year for 20 years.

2. Smoker Reclassification Trap If you vape, use nicotine gum, or smoked within the last 12 months, insurers classify you as a “smoker” — doubling or tripling your premium. This applies even to occasional cigar use at social events.

3. Rider Add-On Inflation Agents often bundle in optional riders — waiver of premium, accidental death benefit, child riders — adding $10–$50/month. Ask specifically which riders are included and which are optional before signing.

4. Substandard Rate Reclassification If your medical exam reveals elevated blood pressure, BMI outside normal range, or a family history of heart disease, your health class drops from “Preferred” to “Standard” or “Substandard.” This can raise premiums by 25–75% from your initial quote.

5. Policy Lapse Penalty (The Silent Killer) Miss two consecutive payments and your policy lapses. Reinstating it requires a new medical exam — at your current age and health. A 40-year-old reinstating a lapsed policy they got at 30 faces dramatically higher premiums.

The Insurance Information Institute (III) confirms that in most term policies, if you haven’t had a claim by expiry, no premium refund is issued — unless you specifically purchased a Return of Premium (ROP) rider, which itself costs significantly more.

How Term Insurance Works — The 5-Phase Lifecycle

Understanding the full lifecycle of a term policy protects you from surprises at every stage.

Phase 1: Application & Underwriting

You apply and provide health history, lifestyle details, and financial information. Most policies require a brief medical exam — blood draw, urine test, and blood pressure check. The insurer’s underwriters assess your mortality risk and assign a health classification that determines your premium.

Health classification tiers (best to worst):

- Preferred Plus / Super Preferred

- Preferred

- Standard Plus

- Standard

- Substandard (rated)

Phase 2: Premium Lock-In

Once approved, your premium is locked in for the full term. A 35-year-old who locks in a 20-year policy at $35/month keeps that rate until age 55 — regardless of health changes, job changes, or market conditions.

This is why buying early saves money. Locking in at 30 vs. 40 could save $5,000–$15,000 in total premiums over a 20-year policy.

Phase 3: Active Coverage Period

Your policy is in force. If you die during this period, your named beneficiaries file a claim and typically receive the full death benefit within 30–60 days, tax-free. The NAIC’s Life Insurance guidance confirms insurers cannot cancel a policy due to health changes once it’s issued.

Phase 4: Policy Expiry Options

When your term ends, you have three choices:

- Let it lapse — coverage ends, no refund (unless ROP rider applies)

- Renew annually — allowed by most policies, but premiums jump sharply (often 3–5x) based on your age at renewal

- Convert to permanent — if your policy has a conversion option, you can switch to whole life without a new medical exam

Phase 5: The Claim Process

Beneficiaries contact the insurer, submit a death certificate, and complete a claim form. Most straightforward claims are paid within 2–4 weeks.

Real case example: A 32-year-old father in Ohio locked in a 20-year, $500,000 term policy for $24/month in 2006. He died of a sudden cardiac event at 48. His wife and two children received the full $500,000 — tax-free — within 30 days. His total premium outlay over 16 years: ~$4,600. The family’s return: $500,000.

That is the power of term insurance done right.

If you’re also weighing how your coverage fits alongside mortgage obligations, our Mortgage Calculator can help you calculate how much debt your family would need covered.

Term vs. Whole Life — The Honest Expert Verdict (What Agents Won’t Tell You)

Most agents earn 70–100% of the first-year premium as commission on whole life policies — compared to 40–60% on term. That financial incentive shapes which product they recommend. Knowing this changes how you listen to advice.

Deep Comparison: Term Insurance vs. Whole Life Insurance

| Factor | Term Insurance | Whole Life Insurance |

|---|---|---|

| Monthly cost (age 35, $500K) | ~$35/mo | ~$500+/mo |

| Coverage duration | Fixed term (10–30 yrs) | Lifetime |

| Cash value | None | Yes (slow growth) |

| Tax benefits | Death benefit tax-free | Cash value tax-deferred growth |

| Flexibility | Choose any term length | Less flexible |

| Best use case | Income replacement, mortgage, kids | Estate planning, ultra-high earners |

| Agent commission incentive | Lower | Higher |

| Expert consensus verdict | ✅ Best for 80% of Americans | ⚠️ For specific financial plans only |

What This Means For You

If you are under 50, have dependents, carry a mortgage, or are in your peak earning years — term insurance almost always wins. The cost difference is dramatic. The money saved on premiums (compared to whole life) can be invested in your 401(k), Roth IRA, or index funds for far greater long-term returns.

Our Life Insurance guide covers all policy types in detail if you want to explore every option before deciding.

The NAIC confirms that term life insurance is intended to provide lower-cost coverage for a specific period and is particularly appropriate when coverage is needed for a limited time or to cover a specific financial obligation such as a mortgage.

How to Buy Term Insurance in 2026 — 6 Steps That Save You Money

Follow this exact sequence. Skip any step and you risk overpaying or being underinsured.

Step 1: Calculate Your Coverage Need

Use this formula as your starting point:

Coverage = (Annual income × 10) + Outstanding mortgage + Children’s future education costs − Existing savings/assets

Example: $80,000 income × 10 = $800,000 + $250,000 mortgage = $1,050,000 − $50,000 savings = $1,000,000 target coverage

If you carry significant debt, our Debt Consolidation Calculator can help you factor existing liabilities into your total coverage need.

Step 2: Choose the Right Term Length

Match your term to your longest financial obligation:

| Life Stage | Recommended Term |

|---|---|

| Young family with newborns | 25–30 years |

| Parent with school-age kids | 20 years |

| Mortgage with 15 years left | 15–20 years |

| Business owner, key person | 10–20 years |

| Pre-retirement income gap | 10 years |

Step 3: Shop at Least 3–5 Carriers

Premiums for identical coverage can vary 30–40% between carriers for the same age and health class. Never accept a single quote. Use an independent broker who has access to multiple insurers — not a captive agent who sells only one company’s products.

The III recommends that you compare similar policies from different companies after deciding on the type that best fits your needs.

Step 4: Understand Your Health Classification Before Applying

Your health class determines your real premium — not the advertised rate. Before applying formally:

- Get your blood pressure checked

- Know your BMI

- Review any prescription history (insurers access prescription drug databases)

- Disclose all health conditions accurately — omissions can void claims

Step 5: Avoid These 3 Rider Traps

- Accidental Death Benefit Rider: Pays double if death is accidental — but most deaths aren’t accidents. Rarely worth the added premium.

- Return of Premium (ROP) Rider: Refunds premiums if you outlive the term — but the policy costs 2–3x more. Investing the premium difference usually outperforms this.

- Waiver of Premium Rider: Waives premiums if you become disabled. Useful, but scrutinize the disability definition — many policies use strict “own occupation” or “any occupation” triggers.

Step 6: Review Annually at Trigger Events

Your coverage need changes. Review and potentially increase your term insurance coverage at:

- Marriage or divorce

- Birth of a child

- New mortgage or major debt

- Significant income increase

- Business partnership formation

Buying your first home is one of the strongest triggers for term insurance. Our Home Affordability Calculator can help you see exactly how much mortgage coverage your family would need.

For a complete deep-dive on term rates and policy selection, our Term Life Insurance Rates & Calculator guide covers 2026-specific carrier comparisons.

Term Insurance FAQs — 11 Expert Answers

1. What is term insurance in simple words?

Term insurance is a life insurance policy that pays a set amount of money to your family if you die within a chosen period — typically 10 to 30 years. If you outlive the policy, no money is paid. It’s the most affordable type of life insurance available.

2. How much does term insurance cost per month in 2026?

A healthy 30-year-old non-smoker pays approximately $22–$28/month for $500,000 in 20-year term coverage. A 40-year-old pays roughly $45–$55/month for the same policy. Smokers pay 2–3x more. Rates vary by carrier, health class, and state.

3. What is the best age to buy term insurance?

The best age is as early as possible — ideally between 25 and 35. Premiums increase 8–12% per year with age. A 10-year delay from age 30 to 40 can nearly double your monthly premium for identical coverage.

4. Can I get term insurance without a medical exam?

Yes. “No-exam” or “simplified issue” term policies are available and can be approved within 24–48 hours. However, they cost 15–30% more than fully underwritten policies. They’re best for people who need fast coverage or have minor health issues. See our life insurance types guide for no-exam options.

5. What happens if I outlive my term insurance policy?

Coverage simply ends. No payout is made and premiums are not refunded — unless you purchased a Return of Premium (ROP) rider upfront. You can choose to renew (at significantly higher rates), convert to permanent insurance, or apply for a new policy.

6. Is the term insurance payout tax-free?

Yes. In the United States, term insurance death benefits paid to beneficiaries are generally income tax-free under IRS rules. The full benefit goes directly to your beneficiaries without federal income tax deduction. Some estate tax considerations may apply for very large policies — consult a tax advisor.

7. How much term insurance coverage do I actually need?

A common starting formula: multiply your annual income by 10–12, then add your outstanding mortgage balance and future education costs for children. Subtract any existing savings or employer life insurance. For most working families, $500,000 to $1 million is an appropriate target.

8. Can I convert my term policy to permanent insurance?

Many term policies include a conversion option that allows you to switch to whole life or universal life insurance without a new medical exam — even if your health has declined. This must typically be exercised before the policy’s conversion deadline. Check your policy documents for conversion eligibility terms.

9. What voids a term insurance claim?

Common claim denial reasons include: material misrepresentation on the application (undisclosed health conditions or lifestyle risks), death by suicide within the policy’s contestability period (typically the first 2 years), or death from an excluded activity specified in the policy. Always disclose all health information accurately when applying. The NAIC confirms accuracy at application is the foundation of a valid claim.

10. Is term insurance worth it in 2026?

For the vast majority of Americans with dependents, a mortgage, or income others rely on — yes, term insurance is worth it. At $22–$55/month, the protection-to-cost ratio is unmatched by any other financial product. The question isn’t whether you can afford term insurance. It’s whether your family can afford for you not to have it. For broader protection strategies, explore our insurance hub.

11. How is term insurance different from life insurance?

“Life insurance” is the broad category — it includes term, whole life, universal life, and variable life policies. “Term insurance” is one specific type within that category. The key distinction: term covers you for a set period at a fixed, affordable rate. Other life insurance types offer lifetime coverage but cost significantly more. Read our complete life insurance guide for the full breakdown.

Expert Summary

Our credentialed financial expert panel at FinanceAuthorityHub.com — with verified practitioners across the USA, UK, and Canada — reached a clear consensus:

“For Americans aged 25–55 with dependents, a mortgage, or financial obligations others rely on, term insurance is the most effective and cost-efficient risk management tool available in 2026. The barrier is never affordability — it’s awareness. Most people are paying more for streaming services than it would cost to protect their family’s financial future.”

⚠️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, legal, or insurance advice. All premium figures cited are industry averages based on 2026 data and are intended as general estimates only. Individual premiums vary based on age, health, state of residence, carrier underwriting, and policy structure. Always consult a licensed financial advisor or insurance professional before purchasing any insurance policy. FinanceAuthorityHub.com is not a licensed insurance producer.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.