Dental Insurance 2026: Stop Overpaying Today

Dental insurance costs $20–$50/month — but millions overpay or go without. Get 2026 plan comparisons, real cost math, and expert picks to stop wasting money today.

In This Article

What Is Dental Insurance — And Are You Paying Too Much?

Dental insurance is a health benefit plan that helps cover the cost of routine and major dental care — from cleanings to crowns — in exchange for a monthly premium. Yet according to the CDC’s 2024 Oral Health Surveillance Report, nearly 1 in 5 adults aged 20–64 has at least one untreated cavity, and financial barriers remain the #1 reason Americans skip the dentist.

The average individual dental insurance plan costs just $20–$50 per month. But millions of Americans are either paying too much for coverage they don’t use — or going completely uninsured and facing $1,000+ bills when problems hit.

This guide cuts through the noise. You’ll get 2026 cost data, a real math breakdown, and a plain-English decision framework to choose — or ditch — the right plan.

| Key Metric | 2026 Figure |

|---|---|

| Average monthly premium (individual) | $20–$50/month |

| Average family plan cost | $50–$150/month |

| Typical annual deductible | $25–$100 |

| Average annual benefit maximum | $1,000–$2,000 |

| Routine cleaning without insurance | ~$200 per visit |

| Root canal without insurance | $900–$1,100+ |

What This Means For You: If you haven’t compared dental coverage recently, you’re likely either overpaying or under-protected. Read the cost math in Section 2 before making any decision.

Dental Insurance Costs in 2026 — What You Actually Pay

Monthly Premiums by Plan Type (2026)

Understanding dental insurance cost starts with knowing that the premium is just one piece of the puzzle. Here’s what the four major plan types cost per month on average:

| Plan Type | Avg. Monthly Premium | Network | Best For |

|---|---|---|---|

| Dental PPO (DPPO) | ~$41/month | Large, flexible | Those who want choice |

| Dental HMO (DHMO) | ~$15/month | Restricted | Budget-conscious buyers |

| Indemnity Plan | $80+/month | Any dentist | Maximum freedom |

| Dental Discount Plan | $7–$17/month | Participating only | No-insurance alternative |

Source: MoneyGeek, Aflac, Cigna Healthcare — 2026 national averages

The Hidden Costs Nobody Warns You About

The monthly premium is only your starting point. Affordable dental insurance can become expensive fast if you ignore these:

- Deductible: $25–$100/year before coverage starts

- Coinsurance: You pay a percentage even after the deductible

- Annual maximum: Most plans cap insurer payouts at $1,000–$2,000/year — a limit that hasn’t changed since the 1970s

- Waiting periods: 6–18 months before major procedures are covered on many PPO plans

- Exclusions: Cosmetic work, most whitening, and some implants are commonly excluded

The 100-80-50 Rule: Real Cost Math

Most dental plans follow the 100-80-50 coverage structure. Here’s what that means in dollars:

Scenario A — Healthy teeth, 2 cleanings only:

- Annual premiums: $420 (PPO at $35/month)

- 2 cleanings at $0 copay (100% covered)

- Out-of-pocket dental costs: $50 deductible

- Total cost with insurance: $470

- 2 cleanings without insurance: ~$400

- Net verdict: You lose $70. A discount plan may serve you better.

Scenario B — One crown + 2 cleanings needed:

- Annual premiums: $420

- Crown ($1,200) covered at 50% → Insurance pays $600

- 2 cleanings: $0 copay

- You pay: $420 premiums + $50 deductible + $600 crown share = $1,070

- Without insurance: $1,200 crown + $400 cleanings = $1,600

- Net verdict: You save $530. Insurance wins clearly.

Key Takeaway: Dental insurance is a financial tool, not a guarantee. It pays off when you need at least one major procedure per year. For those with healthy teeth, a dental discount plan or paying cash is often smarter. If dental bills are adding to your financial stress, use our Debt Consolidation Calculator to see how large healthcare debts affect your overall budget.

Types of Dental Insurance Plans Decoded

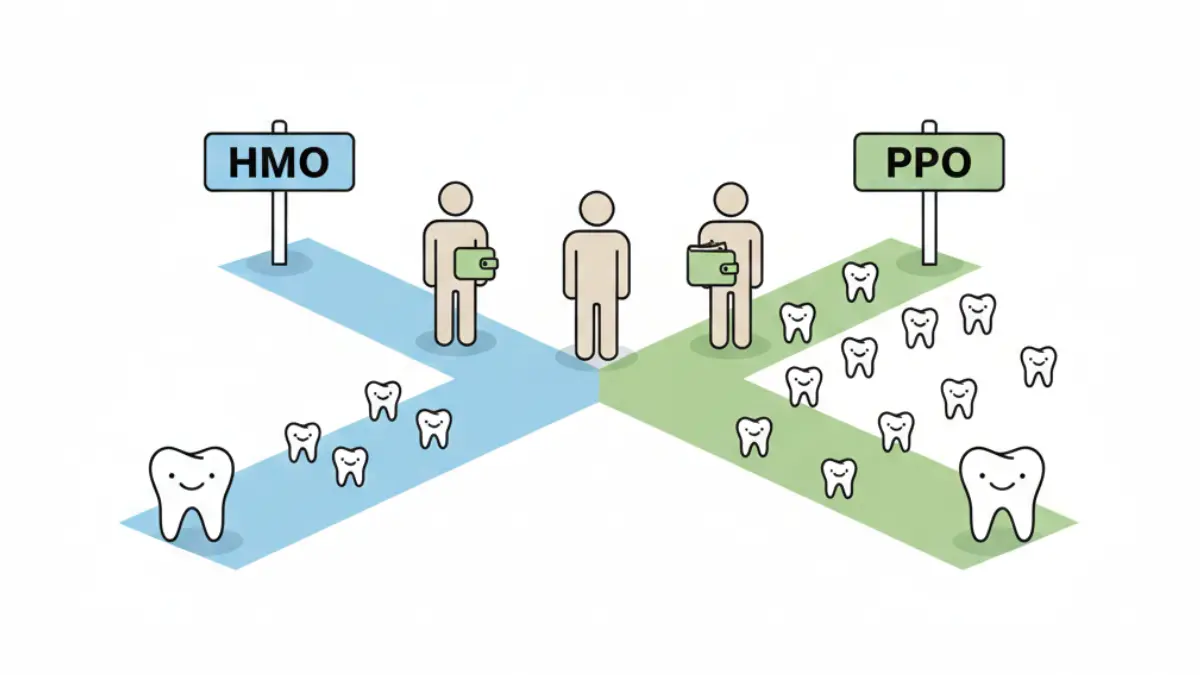

Dental PPO (DPPO) — Best for Flexibility

A PPO dental insurance plan is the most popular choice in the U.S., accounting for roughly 8 in 10 private dental plans.

- Higher monthly premiums (~$41/month average)

- Large network — see most dentists without a referral

- Partial reimbursement for out-of-network dentists

- Annual maximum applies ($1,000–$2,000)

- Deductible required before major coverage starts

Best for: Families, anyone with a preferred dentist, and people who anticipate needing specialist care.

Dental HMO (DHMO) — Best for Low Cost

A dental HMO trades flexibility for affordability. Plans average just $15/month.

- Lower premiums and fixed copays (no surprise bills)

- Must choose a primary care dentist from the network

- Referral required to see a specialist

- No annual maximum on covered services

- No deductible in most cases

Best for: Budget-conscious individuals who are comfortable using in-network providers and don’t need specialist access.

Indemnity Plans — Best for Total Freedom

- See any licensed dentist, anywhere

- Insurer reimburses 50–80% of “reasonable and customary” fees

- Highest premiums ($80+/month)

- More paperwork — you pay upfront, then file for reimbursement

Best for: People in rural areas with limited network access, or those with a long-term preferred dentist outside standard networks.

Dental Discount Plans — Not Insurance, But Useful

Often confused with dental insurance plans, discount plans are membership programs — not insurance. You pay an annual fee ($70–$200/year) and receive discounted rates at participating dentists.

- No waiting periods

- No annual maximum

- No claims process

- Savings of 10–60% on procedures

- No coverage guarantee — just a negotiated rate

Best for: Self-employed individuals between jobs, those with pre-existing dental conditions, or anyone who just needs cleanings covered immediately.

Side-by-Side Plan Comparison

| Feature | PPO | HMO | Indemnity | Discount Plan |

|---|---|---|---|---|

| Avg. Monthly Cost | ~$41 | ~$15 | $80+ | $7–$17/yr |

| Waiting Period | Often yes | Often no | Varies | None |

| Out-of-Network | Partial | No | Yes | No |

| Annual Max | $1–2K | None | Varies | None |

| Referral Needed | No | Yes | No | No |

| Deductible | Yes | Rarely | Varies | No |

For a broader look at how dental insurance fits within your total protection strategy, see our comprehensive insurance guide and our deep-dive on health insurance costs — both updated for 2026.

What Does Dental Insurance Actually Cover?

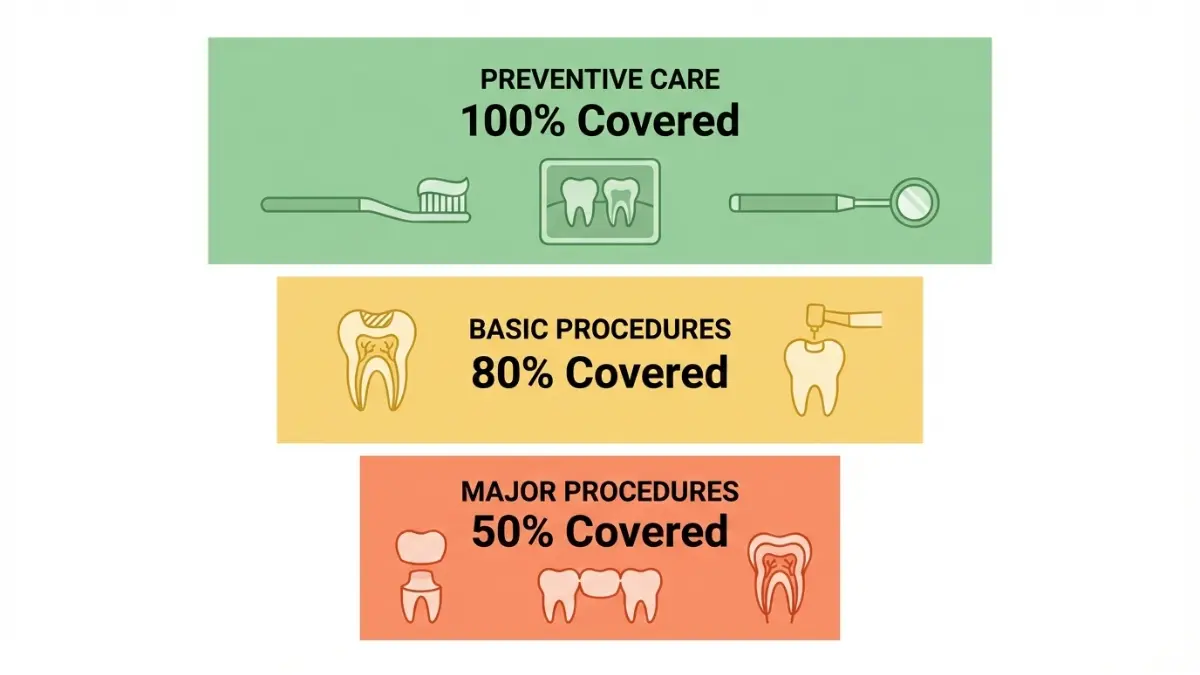

The Three Coverage Tiers Explained

Every standard dental coverage plan is built around three service tiers. Knowing these tiers prevents bill shock.

Tier 1 — Preventive Care (Covered 100%)

- Routine exams and cleanings (typically 2x/year)

- Dental X-rays

- Fluoride treatments (often for children)

- Sealants

Tier 2 — Basic Procedures (Covered ~80%)

- Cavity fillings (composite and amalgam)

- Simple extractions

- Basic periodontal treatment

- Emergency dental exams

Tier 3 — Major Procedures (Covered ~50%)

- Crowns and bridges

- Root canals

- Dentures

- Oral surgery

- Dental implants (plan-dependent — confirm before purchasing)

What Most Dental Plans Do NOT Cover

This is the gap most competitors don’t explain clearly:

- Cosmetic veneers — virtually never covered

- Teeth whitening — excluded by most plans (a small number of PPOs now include it)

- Adult orthodontics (braces/Invisalign) — rarely covered without a specific rider

- Implants — coverage varies widely; some PPOs cover 50% after waiting periods, many HMOs exclude them entirely

- Pre-existing conditions — some plans have exclusions or extended waiting periods for conditions that existed before enrollment

Real Cost Savings Table

| Procedure | Without Insurance | With Insurance (50%) | Potential Savings |

|---|---|---|---|

| Routine Cleaning | ~$200 | $0 (100% covered) | $200 |

| Composite Filling | ~$200 | ~$40 (80% covered) | $160 |

| Root Canal (molar) | ~$1,100 | ~$550 | $550 |

| Crown (porcelain) | ~$1,500 | ~$750 | $750 |

| Dental Implant | ~$4,000 | ~$2,000 | $2,000 |

Sources: ADA Health Policy Institute fee data; MoneyGeek 2026 cost analysis

Key Takeaway: One crown per year makes a standard PPO plan pay for itself — twice over. The real question isn’t whether insurance saves money, it’s how much dental work you realistically need.

According to HealthCare.gov, dental coverage is not an essential health benefit for adults under the ACA, meaning most Marketplace health plans don’t automatically include it. You’ll need to shop for it separately.

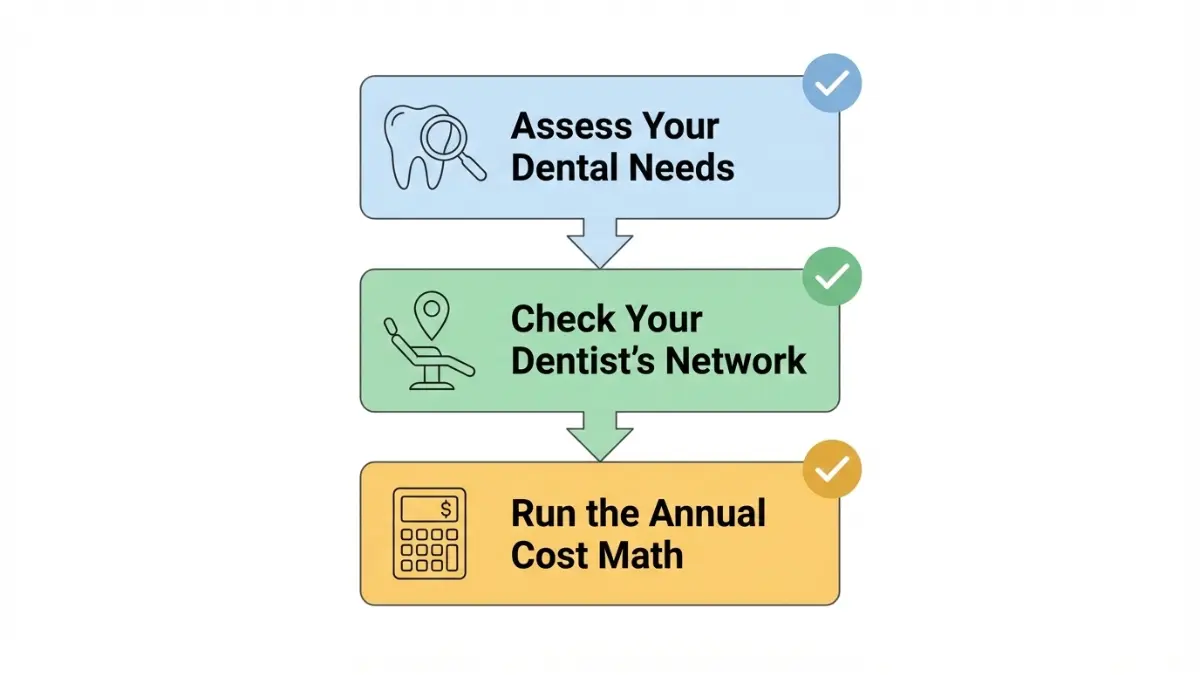

How to Choose the Best Dental Insurance Plan in 2026

Step 1 — Assess Your Dental Health Profile

Match your situation to the right plan tier before spending a dollar on premiums:

| Your Situation | Recommended Approach |

|---|---|

| Healthy teeth, 2 cleanings/year | Discount plan or low-cost HMO |

| Occasional fillings needed | Entry-level PPO or HMO |

| Crown, bridge, or root canal likely | Mid-tier PPO with low annual max deductible |

| Multiple major procedures | High-tier PPO or indemnity plan |

| Braces needed for child | PPO with orthodontic rider |

Step 2 — Verify Your Dentist’s Network Status

Before buying any plan, call your dentist’s office and confirm which dental insurance plans they accept. Switching dentists to stay in-network is one of the most common and avoidable mistakes.

- Use each insurer’s online dentist directory to check network size in your ZIP code

- A larger network = more flexibility and lower risk of disruption

- PPOs offer out-of-network partial coverage; HMOs offer zero

Step 3 — Do the Annual Math

Run this simple formula before committing:

(Monthly Premium × 12) + Deductible + Expected Copays vs. Expected Out-of-Pocket Without Insurance

If the second number is higher, dental insurance is worth it. If they’re equal or the first is higher, consider a discount plan.

Special Situations — Critical Guidance

Self-Employed and Freelancers

Nearly 27% of uninsured American adults are self-employed or lack employer-sponsored dental benefits. Your options in 2026:

- Purchase an individual PPO or HMO through a dental insurer directly

- Explore stand-alone dental plans on the ACA Marketplace (available at healthcare.gov/coverage/dental-coverage)

- Use a dental discount plan as a lower-cost bridge while building emergency savings — see our Emergency Fund Guide to prepare for unexpected dental bills

- HSA contributions (up to $4,300/year for individuals in 2026) can cover dental costs tax-free if paired with a qualifying high-deductible health plan

Seniors

Original Medicare does not cover routine dental care — cleanings, fillings, extractions, or dentures. Your options:

- Medicare Advantage plans — most include some dental coverage; compare at medicare.gov

- Stand-alone individual dental insurance — Spirit Dental, Humana, and Aetna offer senior-specific plans with no age limits

- No waiting period plans are available; check Spirit Dental’s PPO options

Families

- Family dental plans average $50–$150/month

- Children’s dental coverage is an essential health benefit under the ACA — it must be available through Marketplace plans

- Add an orthodontic rider if braces are on the horizon ($1,500–$3,000 lifetime benefit typical)

- Children can stay on a parent’s plan in some cases; verify by plan

Planning homeownership alongside healthcare costs? Our Home Affordability Calculator helps you factor insurance into your total monthly budget picture.

Is Dental Insurance Worth It? The 2026 Verdict

Yes — if you expect at least one major procedure (filling, crown, root canal) per year. A single crown saves $500–$750 net after premiums.

No — if your teeth are consistently healthy and you only need 2 cleanings/year. A discount plan ($8–$17/month) often covers the same ground at a fraction of the cost.

For self-employed individuals: An HSA + dental discount plan combination often beats a standalone PPO on total annual cost.

Dental Insurance FAQs — 11 Expert Answers

1. What is the average cost of dental insurance per month?

Individual dental insurance costs $20–$50/month on average in 2026. Family plans typically run $50–$150/month. HMO plans start as low as $15/month; indemnity plans can exceed $80/month.

2. Is dental insurance worth it in 2026?

Yes, if you need one or more major procedures annually. For those only getting 2 cleanings/year, a dental discount plan is usually more cost-effective than a full dental insurance plan.

3. What does dental insurance NOT cover?

Most dental coverage plans exclude: cosmetic veneers, most teeth whitening, elective orthodontics for adults (without a rider), and purely aesthetic procedures. Always read the exclusions section before buying.

4. Can I get dental insurance if I’m self-employed?

Yes. You can buy individual dental insurance directly from insurers or explore stand-alone dental plans through the ACA Marketplace. Dental discount plans are also widely available with no enrollment period.

5. What is a dental waiting period?

A waiting period is a delay — typically 6–18 months — before your dental insurance will pay for basic or major procedures. Some plans waive this if you had prior dental coverage within the last 60–90 days. HMO and discount plans often have no waiting periods.

6. Does dental insurance cover implants?

It depends on the plan. Some PPO dental insurance plans cover 50% of implant costs after a waiting period. Many HMOs and budget PPOs exclude implants entirely. Always confirm implant coverage in writing before selecting a plan.

7. What is the 100-80-50 rule?

The 100-80-50 rule describes how most dental plans share costs: preventive care (cleanings, X-rays) at 100%, basic procedures (fillings, extractions) at 80%, and major procedures (crowns, root canals, dentures) at 50%.

8. What’s the difference between a dental PPO and HMO?

A dental PPO offers more provider flexibility and covers out-of-network visits at a higher premium (~$41/month). A dental HMO restricts you to a network but costs as little as $15/month with no deductible.

9. Does Medicare cover dental care?

Original Medicare (Parts A & B) does not cover routine dental care. Most Medicare Advantage plans include some basic dental benefits. For comprehensive coverage, seniors need a stand-alone dental plan or a Medicare Advantage plan with strong dental riders.

10. What is an annual maximum in dental insurance?

The annual maximum is the total dollar amount your dental insurance plan pays per year — typically $1,000–$2,000. Once reached, you pay 100% out-of-pocket. This cap has barely changed since the 1970s, which is why many Americans exhaust coverage after just one major procedure.

11. Can I get dental insurance with no waiting period?

Yes. Most dental HMO plans have no waiting periods for covered services. Dental discount plans have no waiting periods by design. Some PPO insurers also offer no-waiting-period plans if you can prove 12+ months of prior dental coverage.

⚠️ Disclaimer: This article is for educational and informational purposes only and does not constitute financial, insurance, or professional advice. Dental insurance costs, coverage terms, and plan availability vary by state, insurer, and individual circumstances. Always consult a licensed insurance professional before purchasing any dental insurance plan. All data is sourced from verified industry publications and updated as of February 2026.

Explore more ways to protect your finances: our expert guides on life insurance rates, car insurance savings, and cheap insurance strategies are all updated for 2026.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.