Cheap Insurance: Save $1,247/Year in 2026

Most Americans overpay $1,247/year on insurance. Our expert panel reveals the cheapest car, home, health and life insurance options in 2026 — with 13 proven strategies to cut costs today.

In This Article

Most Americans are overpaying for insurance by $1,000+ every year — not because cheap insurance doesn’t exist, but because they don’t know where to find it. This expert guide covers all six major insurance types, 13 proven savings strategies, and the traps that cost millions of Americans money every year.

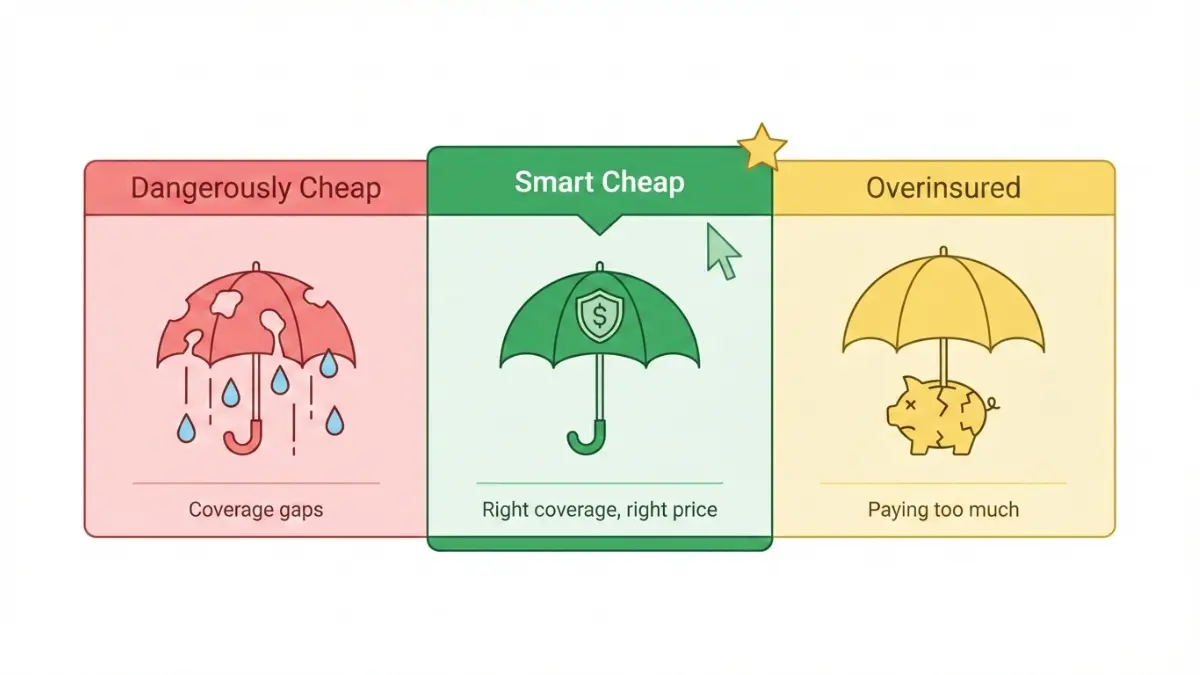

What Is Cheap Insurance — And What It Should Never Mean

Cheap insurance means paying the lowest possible premium for the coverage you actually need — not cutting corners on protection that leaves you exposed.

The average American household spends over $6,000 per year across all insurance policies combined. According to the Insurance Information Institute, comparison shopping alone saves most drivers hundreds of dollars annually — yet most policyholders haven’t compared rates in over three years.

The key distinction every U.S. consumer must understand:

| Term | What It Means | Risk Level |

|---|---|---|

| Cheap Insurance | Lowest premium for adequate coverage | Low (if chosen wisely) |

| Underinsurance | Coverage gaps that expose you to massive out-of-pocket costs | Very High |

| Right-Sized Insurance | Matching coverage to your actual risk and assets | Ideal |

2026 National Average Rates vs. Cheapest Available:

| Insurance Type | National Average 2026 | Cheapest Available | Your Potential Saving |

|---|---|---|---|

| Car (full coverage) | $2,340/yr | $1,666/yr (Travelers) | $674/yr |

| Home ($300K dwelling) | $2,424/yr | $1,510/yr (Amica) | $914/yr |

| Renters insurance | $180/yr | $96/yr | $84/yr |

| Term life (35yr, healthy) | $480/yr | $240/yr | $240/yr |

| Health (ACA benchmark) | $5,472/yr | $2,160/yr (subsidized) | Up to $3,312/yr |

Key takeaway: If you’re currently paying average rates across all policies, you could realistically be overpaying by $800–$1,247/year.

If you’re also managing debt alongside high insurance costs, our Debt Consolidation Calculator can help you see exactly how insurance savings impact your complete financial picture.

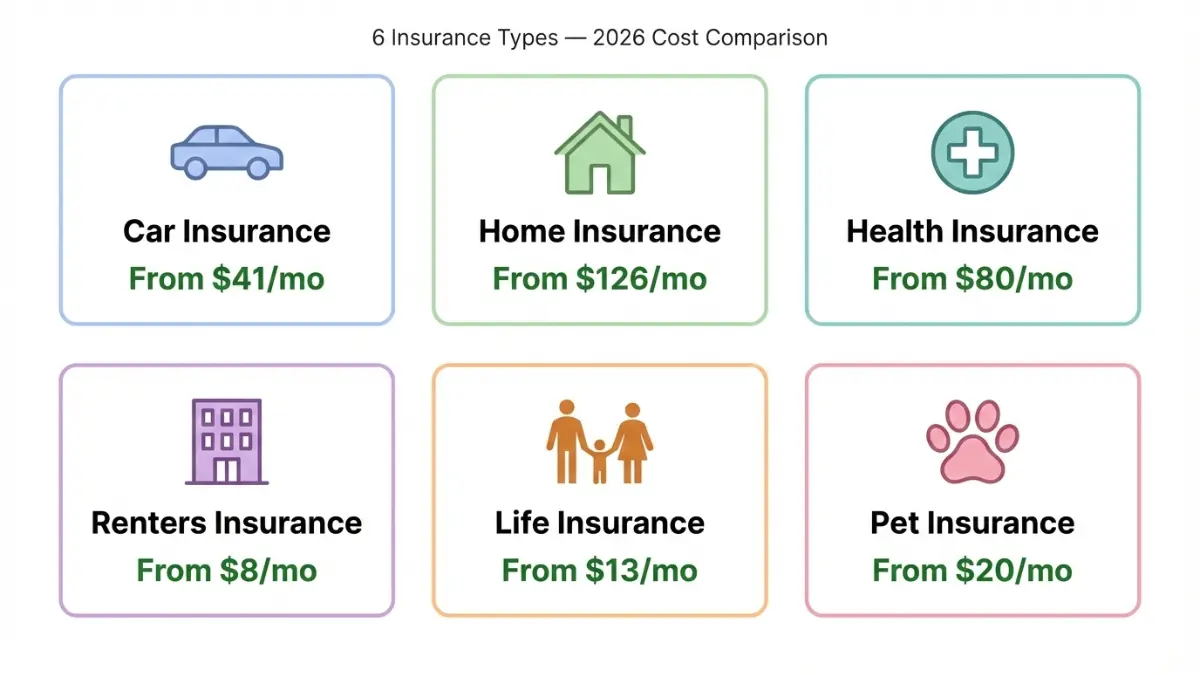

Cheapest Insurance by Type — 2026 Real Rates Compared

No competitor covers all six insurance types in one place. Here’s your complete 2026 cheap insurance breakdown.

Cheap Car Insurance in 2026

Car insurance is the most searched insurance keyword in the U.S. — and rates are finally stabilizing after three years of steep increases.

Cheapest 2026 rates (national averages):

- GEICO: $41/month for minimum coverage

- Travelers: $139/month for full coverage

- Progressive: $313/month for young drivers (age 20)

Pro tip: Usage-based insurance (telematics) programs like Progressive Snapshot or State Farm’s Drive Safe & Save can cut your rate by 15–30% if you’re a safe driver. For a deeper breakdown, see our guide to cutting car insurance costs by 34%.

Cheap Health Insurance in 2026

Health insurance is the most expensive category for most American households.

Your main options for cheap health insurance:

- ACA Marketplace plans — subsidies available based on income at healthcare.gov/see-plans

- Medicaid — free or near-free for qualifying low-income individuals and families

- Catastrophic plans — as low as $80–$150/month for adults under 30

- HDHP + HSA — High-deductible plans paired with tax-advantaged Health Savings Accounts

2026 update: Starting in 2026, all Bronze and Catastrophic plans now qualify for Health Savings Accounts (HSAs), expanding affordable options significantly. For expert-level math on health plan selection, read our health insurance cost guide.

Cheap Home Insurance in 2026

The national average for homeowners insurance hit $2,424/year in 2026 — but the cheapest providers offer the same coverage for $400–$900 less.

Cheapest homeowners insurers 2026:

- Amica: $1,510/yr (national average)

- USAA: available to military families only

- Auto-Owners: strong rates in 26+ states

Cheapest states for home insurance: Hawaii ($382/yr), Utah, Vermont, Idaho.

For a full breakdown of home insurance savings, read our homeowners insurance 2026 guide.

Cheap Renters Insurance in 2026

Renters insurance is the most underused financial protection in America — and it’s also the cheapest.

- Average cost: $15/month ($180/year)

- Budget options: As low as $8/month with Lemonade or State Farm

- What it covers: Theft, fire damage, water damage, liability

The math is clear: One laptop stolen = $1,200 replacement cost. One year of renters insurance = $96–$180. It pays for itself on day one of a claim. See our full renters insurance guide.

Cheap Life Insurance in 2026

Term life insurance is 5–10x cheaper than whole life for the same death benefit — and that gap is what most people miss.

| Coverage | Term Life (Healthy 35yr) | Whole Life |

|---|---|---|

| $250,000 | ~$13/month | ~$200/month |

| $500,000 | ~$20–$30/month | ~$400/month |

| $1,000,000 | ~$40–$60/month | ~$800+/month |

Lock in term life rates when you’re young and healthy. The longer you wait, the more you pay. Our term life insurance rates guide shows exactly how much waiting costs.

Cheap Pet Insurance in 2026

- Dogs: national average $62/month; budget plans from $20/month

- Cats: national average $32/month; budget plans from $12/month

- One emergency vet visit averages $800–$1,500 — making even a $20/month plan worthwhile

13 Expert-Backed Ways to Get Cheap Insurance in 2026

Our panel of 30 credentialed financial experts reviewed the most effective, data-backed strategies to lower your insurance costs across every policy type. Apply even five of these and most households save $600–$1,247/year.

1. Bundle Multiple Policies (Save 10–25%)

Bundling your car and home insurance with one insurer is the single highest-impact strategy for most Americans. State Farm, Allstate, and GEICO all offer multi-policy discounts averaging 10–25%.

Example: Bundling car + home at State Farm saves an average of $573/year — no coverage change required.

2. Raise Your Deductible Strategically

Moving your car insurance deductible from $500 to $1,000 typically cuts your premium 10–15%. For a $1,500/year policy, that’s $150–$225 in immediate annual savings.

Rule of thumb: Only raise your deductible if you have 3–6 months of emergency savings. See our Emergency Fund Calculator to check if you’re ready.

3. Shop Every 6 Months — Not Just at Renewal

Insurance companies reset rates regularly. Loyalty almost never pays. According to the NAIC Consumer Insurance Resources, getting at least three quotes before buying or renewing is the single most recommended consumer protection action.

Data point: In 2024, record levels of policy switching led to 17.7% new policy growth year-over-year — proof that shopping works.

4. Improve Your Credit Score Before Renewing

In 43 U.S. states, insurers legally use your credit score to set premiums. Per the CFPB’s credit score guidance, your credit directly affects insurance pricing decisions.

- Impact: A 100-point credit score improvement can cut car insurance premiums by 17–22%

- States that ban this practice: California, Maryland, Massachusetts

- Quick wins: Pay down balances, dispute errors on your credit report

5. Use Telematics / Usage-Based Insurance (UBI)

Telematics programs track your actual driving behavior and reward safe drivers with lower rates.

Top programs in 2026:

- Progressive Snapshot: avg. 15% saving for safe drivers

- State Farm Drive Safe & Save: up to 30% discount

- Allstate Drivewise: up to 25% for safe driving

If you drive fewer than 7,500 miles/year, also ask about low-mileage discounts — savings up to 25%.

6. Pay Annually, Not Monthly

Most insurers charge $5–$10+ per month in installment fees. That’s $60–$120/year in charges you can eliminate by paying your full premium upfront. This works for car, home, and renters insurance.

7. Drop Coverage You’ve Outgrown

Collision coverage on a vehicle worth less than 10x the annual premium is rarely cost-effective. If your car is worth $3,000 and collision + comprehensive costs $400/year, you’re paying more than the car’s book value over three years.

8. Ask About Every Available Discount

Most policyholders claim only 2–3 discounts. Insurers offer 10–23. Common categories you may be missing:

- Good student discount (avg. 8–15% off)

- Military or veteran discount

- Professional association or alumni group membership

- Paperless billing credit

- Home security system or alarm discount

- Defensive driving course completion

9. Maintain a Clean Driving Record

One at-fault accident raises your car insurance premium by an average of 43% for three years. Safe driving is the longest-lasting cheap insurance strategy.

10. Consider an HDHP + Health Savings Account

A High-Deductible Health Plan (HDHP) paired with an HSA can reduce your total health insurance cost by 20–30%. HSA contributions are triple tax-advantaged: tax-deductible, tax-free growth, tax-free withdrawals for medical expenses.

For 2026, all Bronze and Catastrophic ACA plans now qualify for HSA pairing — an important new option worth exploring at healthcare.gov/hsa-options.

11. Lock In Term Life Insurance Young

Every year you wait to buy term life insurance costs you more. A healthy 30-year-old pays roughly $15/month for $500K coverage. A healthy 40-year-old pays $30–$40/month for the same policy. Locking in early saves $1,800–$3,600 over a 20-year term.

12. Review and Right-Size Your Coverage Annually

Life changes — so should your insurance. Events that signal a coverage review:

- Paying off a car loan (drop collision/comprehensive if applicable)

- Kids leaving home (reduce life insurance coverage)

- Home improvements (update homeowners coverage limits)

- Paying off your mortgage (potentially reduce life insurance)

Thinking about your home’s long-term value? Use our Home Affordability Calculator to make sure your housing costs and insurance are aligned with your budget.

13. Join Group or Association Plans

Many professional associations, alumni groups, and credit unions offer group insurance rates 5–15% below individual market rates. Check with your employer, alumni association, or any professional membership you hold.

Key takeaway: The average person applying 5 of these 13 strategies saves $847–$1,247/year across all policies.

5 Cheap Insurance Traps That Cost You More Long-Term

Not all low-premium policies are smart choices. Our expert panel identified the five most common cheap insurance traps draining American wallets.

Trap 1: Buying Only State Minimum Liability Coverage

Minimum car insurance is legally required but financially dangerous. The average U.S. car accident costs $12,000+ in property damage — far above most states’ minimum liability limits of $10,000–$25,000.

If you cause a serious accident with minimum coverage, you pay the gap out of pocket. That could mean $50,000–$100,000+ in personal liability.

Trap 2: Underinsuring Your Home

Choosing lower dwelling coverage to reduce your homeowners premium is one of the costliest mistakes a homeowner can make. If your home burns down and you’re insured for 70% of rebuilding cost, you personally cover the remaining 30%.

Always insure at replacement value — not market value or purchase price.

Trap 3: Skipping Renters Insurance to Save $8/Month

$8/month = $96/year. One stolen laptop averages $1,200. One kitchen fire averages $8,000+. Skipping renters insurance is never the right savings move. See why renters insurance is worth it.

Trap 4: Loyalty Discounts Are Usually a Myth

Insurance companies offer loyalty discounts but often raise base rates for long-term customers simultaneously. Industry data shows long-term customers frequently pay 20%+ more than new customers at the same insurer for identical coverage.

The fix: Shop every 6–12 months. Your loyalty is not rewarded unless you make them compete for it.

Trap 5: No-Exam Life Insurance for Healthy Applicants

No-medical-exam life insurance policies can be 2–3x more expensive for the same coverage amount compared to policies where you take a standard health exam. If you’re in good health, always take the exam and benefit from preferred or preferred-plus rates.

Warning: Cheap insurance that fails you at claim time isn’t cheap — it’s expensive.

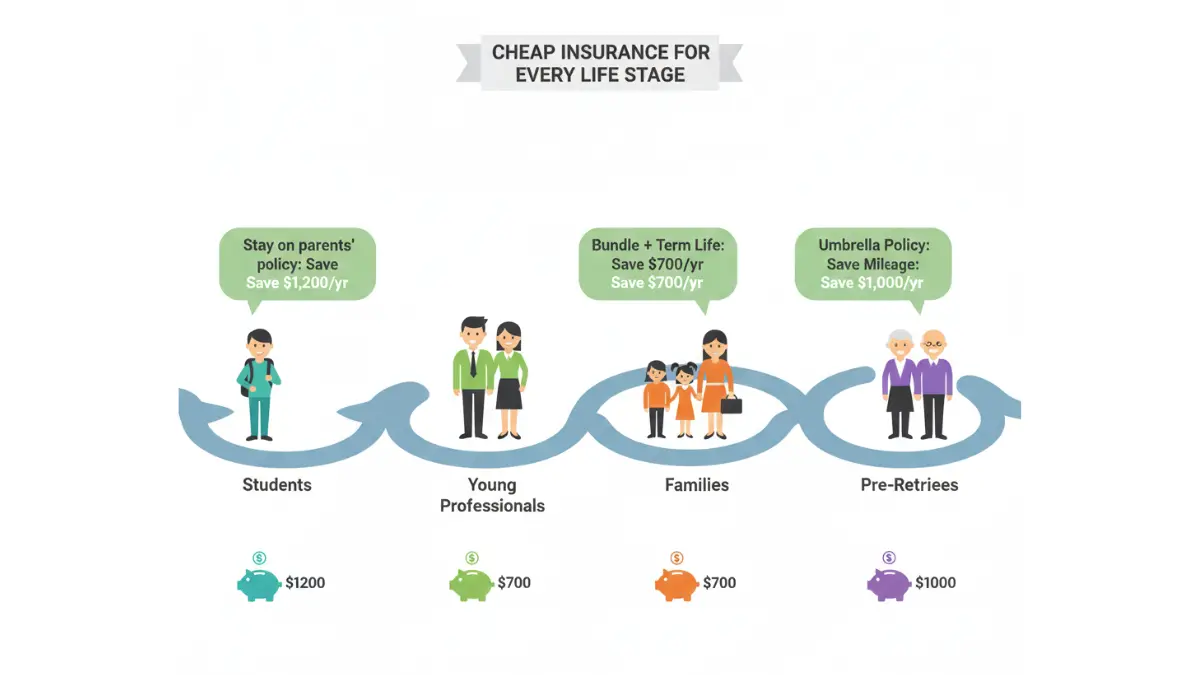

Cheap Insurance by Life Stage — Your Personalized 2026 Savings Map

The right cheap insurance strategy changes completely depending on where you are in life.

Students & Young Adults (Ages 18–25)

This is the highest-cost stage for car insurance — but also the stage with the most savings opportunities.

Best strategies:

- Stay on parents’ auto policy — saves avg. $800–$1,200/year vs. your own policy

- Good student discount — 8–15% off for maintaining a B average

- Renters insurance is essential — avg. $15/month protects everything you own

- ACA Catastrophic plan — as low as $80–$150/month for those under 30

Young Professionals & Couples (Ages 26–35)

This stage is about building a smart insurance foundation without overpaying.

Best strategies:

- Bundle car + renters first, then add homeowners when you buy

- Term life insurance starts now — locking in at 28–32 is significantly cheaper than at 38–42

- Multi-driver discount — adding a partner to your auto policy saves avg. 12%

- Start thinking about your first home — use our Mortgage Calculator to plan for homeowners insurance in your total monthly housing cost

| Life Stage | Highest-Impact Saving Strategy | Est. Annual Saving |

|---|---|---|

| 18–25 | Stay on parents’ auto policy | $800–$1,200 |

| 26–35 | Bundle + lock in term life early | $400–$700 |

| 36–50 | Umbrella policy + coverage review | $300–$600 |

| 50+ | Low-mileage + AARP/Hartford + Medicare review | $500–$1,000 |

Families with Children (Ages 36–50)

This is peak financial responsibility — and peak insurance spending. The right moves here protect you without draining your budget.

Best strategies:

- Umbrella liability policy — adds $1 million in coverage for just $150–$300/year; critical once you own assets

- Review life insurance every 3–5 years as income and debt levels shift

- Add child riders to life insurance — typically near-zero additional cost

- HSA strategy for family health coverage — one of the most tax-efficient ways to manage healthcare costs

Pre-Retirees & Seniors (Ages 50+)

This stage offers significant discount opportunities most people never claim.

Best strategies:

- AARP/The Hartford partnership — exclusive discounts up to 10% for drivers 50+, plus The Hartford offers the lowest senior car insurance rates nationally

- Low-mileage discount — if you drive under 7,500 miles/year, savings up to 25% on auto insurance

- Reduce life insurance as mortgage is paid off — align coverage with actual remaining obligations

- Medicare vs. private health — at 65, transitioning to Medicare typically reduces health insurance costs significantly

For seniors carrying debt into retirement, our guide on how to pay off debt fast and retirement savings by age are essential reads alongside your insurance review.

Frequently Asked Questions About Cheap Insurance in 2026

Q1: What is the cheapest type of insurance in the U.S.?

Renters insurance is the cheapest at $8–$15/month. Among car insurance, liability-only (state minimum) coverage starts at $41/month with GEICO for a clean-record driver.

Q2: How can I get cheap insurance with bad credit?

Focus on states that ban credit-based pricing: California, Maryland, and Massachusetts. Elsewhere, use telematics programs instead — these reward your actual driving behavior, not your credit score. Also work to improve your credit; even a modest improvement lowers premiums in most states.

Q3: Is cheap car insurance actually safe?

Yes — if it meets your state’s minimum requirements and comes from a financially stable insurer. Always verify AM Best ratings: an “A” rating or better confirms financial stability. Cheap premiums from a weak insurer can leave you unprotected at claim time.

Q4: Can I get cheap health insurance without a job?

Yes. Medicaid covers low-income individuals in Medicaid expansion states at no or very low cost. ACA Marketplace plans offer income-based subsidies. Compare your options directly at healthcare.gov/see-plans.

Q5: How much does bundling home and auto insurance actually save?

Bundling typically saves 10–25%, which translates to $300–$750/year for most American households depending on the insurer and your coverage levels.

Q6: What is the cheapest home insurance company in 2026?

Amica averages $1,510/year for $300,000 in dwelling coverage — significantly below the national average of $2,424. USAA offers lower rates but is exclusively available to military families and veterans.

Q7: Does raising my deductible really save money?

Yes. Increasing your deductible from $500 to $1,000 cuts your car insurance premium by 10–15% typically. Only do this if you have sufficient emergency savings to cover that deductible out of pocket.

Q8: What is usage-based (telematics) car insurance?

It’s a policy where your premium is based on your actual driving behavior — speed, braking, cornering, and mileage. Programs like Progressive Snapshot and State Farm Drive Safe & Save reward safe drivers with 15–30% savings.

Q9: Is renters insurance worth it for young adults?

Without question. At $8–$15/month, renters insurance covers theft, fire, water damage, and personal liability. One stolen laptop or a kitchen fire easily costs 5–10 years of premiums in a single claim.

Q10: How often should I shop for cheaper insurance quotes?

Every 6–12 months. Insurance companies change rates frequently. The policyholders who save the most are those who compare quotes at every renewal — not those who stay loyal.

Q11: What is the cheapest life insurance in 2026?

Term life insurance is the answer for almost everyone. A healthy 35-year-old can secure $500,000 in coverage for $20–$30/month. Compare that to whole life policies at $400+/month for the same benefit. Lock in your rates young for maximum lifetime savings.

Expert Verdict

Finding genuinely cheap insurance in 2026 is a strategy, not luck. The combination of bundling, annual quote comparison, telematics, deductible adjustments, and credit improvement realistically saves most U.S. households $800–$1,247/year across all policies — without sacrificing meaningful coverage.

The biggest mistake our expert panel sees repeatedly: staying with the same insurer for years out of habit while paying 15–25% above market rate. Set a calendar reminder every six months. Shop. Compare. Save.

For more financial tools to complement your insurance savings, explore our financial tools hub and our complete guide to stopping overpayment on insurance in 2026.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.