Homeowners Insurance 2026: Stop Overpaying Today

Homeowners insurance costs average $2,543/yr in 2026 — but millions overpay. Compare best companies, real rates by state, hidden gaps & 11 expert ways to slash your premium today.

In This Article

Homeowners insurance is a financial protection policy that covers your home, belongings, and personal liability against damage, theft, and accidents. In 2026, the national average cost is $2,543 per year — but millions of Americans are overpaying by hundreds of dollars. This guide gives you everything: what’s covered, what’s not, real 2026 rates, the best companies, and 11 expert-verified ways to cut your premium starting today.

🔑 Key Stat: Home insurance rates rose 10.4% in 2024, and analysts forecast another 3–8% increase in 2026. If you haven’t reviewed your policy in the last 12 months, you are almost certainly overpaying.

What Is Homeowners Insurance — and Why It’s Non-Negotiable in 2026

Homeowners insurance protects what is likely your single largest financial asset: your home. A standard policy bundles together property protection, liability coverage, and living expense support into one annual premium.

Mortgage lenders require it. But even if you own your home outright, going without coverage is a catastrophic financial risk. According to the Insurance Information Institute, approximately 12% of US homeowners currently carry no home insurance — a number that leaves millions of families exposed to six-figure losses.

Here’s what’s changed in 2026:

- 47% of homeowners experienced a lender-initiated premium increase in the past year — the highest rate in over a decade

- Rates are rising not just in disaster-prone states but nationally, driven by inflation, supply chain costs, and extreme weather

- The average claim processing time has reached 44 days — the longest since J.D. Power began tracking in 2008

If you’re buying your first home, our Home Affordability Calculator can help you factor insurance costs into your total ownership budget before you commit. And if you’re already a homeowner, keep reading — the savings tactics in Section 5 could cut hundreds off your next renewal.

What Does Homeowners Insurance Cover in 2026?

The 6 Core Coverage Types

A standard homeowners insurance policy (most commonly an HO-3) includes six protection categories. Here’s the complete breakdown:

| Coverage Type | What It Protects | Typical Limit |

|---|---|---|

| Dwelling Coverage | Home structure: walls, roof, floors, attached garage | Full replacement cost |

| Other Structures | Detached garage, fence, shed | 10% of dwelling limit |

| Personal Property | Furniture, electronics, clothing, appliances | 50–70% of dwelling limit |

| Liability Protection | Legal fees + settlements if someone is injured on your property | $100K–$500K |

| Loss of Use (ALE) | Hotel, meals, rent while home is being repaired | 20–30% of dwelling limit |

| Medical Payments | Medical bills for guests injured on your property | $1K–$5K |

What This Means For You: Dwelling coverage should always equal your home’s replacement cost — not its market value or tax assessment. These are very different numbers, and getting this wrong is the single most expensive mistake homeowners make.

What Your Homeowners Insurance Policy Will NOT Cover

This is the section that no competitor covers deeply enough — and where most claim disputes happen.

Standard exclusions in virtually every policy:

- 🚫 Flood damage — requires a completely separate policy through the National Flood Insurance Program (NFIP)

- 🚫 Earthquake damage — requires a separate endorsement or standalone policy; critical in California, the Pacific Northwest, and the New Madrid Seismic Zone

- 🚫 Pest and mold damage — considered maintenance negligence; not covered

- 🚫 Normal wear and tear — aging roof, deteriorating plumbing; homeowner’s responsibility

- 🚫 High-value jewelry, art, collectibles — standard policies sub-limit these at $1,000–$2,500; a scheduled rider is required for full protection

- 🚫 Home-based business liability — if a client is injured during a business meeting at your home, a personal homeowners policy will not cover it

- 🚫 Power outages causing food spoilage — often excluded unless caused by a covered peril directly

⚠️ Important: Nearly one-third of NFIP flood claims come from outside designated high-risk flood areas. Don’t assume you’re safe because you’re not in a flood zone. Almost every US county has experienced flooding since 1996.

HO-3 vs. HO-5: Which Policy Type Do You Have?

Most homeowners carry an HO-3, but understanding the difference matters significantly.

| Policy | Home Structure Coverage | Personal Property Coverage | Best For |

|---|---|---|---|

| HO-2 (Broad Form) | Named perils only | Named perils only | Budget-constrained buyers |

| HO-3 (Special Form) | Open perils (all risks except exclusions) | Named perils only | Most homeowners |

| HO-5 (Comprehensive) | Open perils | Open perils | High-value homes + maximum protection |

The HO-3 coverage gap most homeowners miss: Your belongings are only covered for named perils (fire, theft, wind). If something unlisted damages your laptop — say, accidental dropping — you’re not covered under HO-3 personal property. Upgrading to HO-5 closes that gap.

For a deeper look at how insurance costs intersect with your overall property investment, explore our guide on property value factors that set your real price in 2026.

Homeowners Insurance Cost in 2026 — Are You Overpaying?

National Average + State-by-State Snapshot

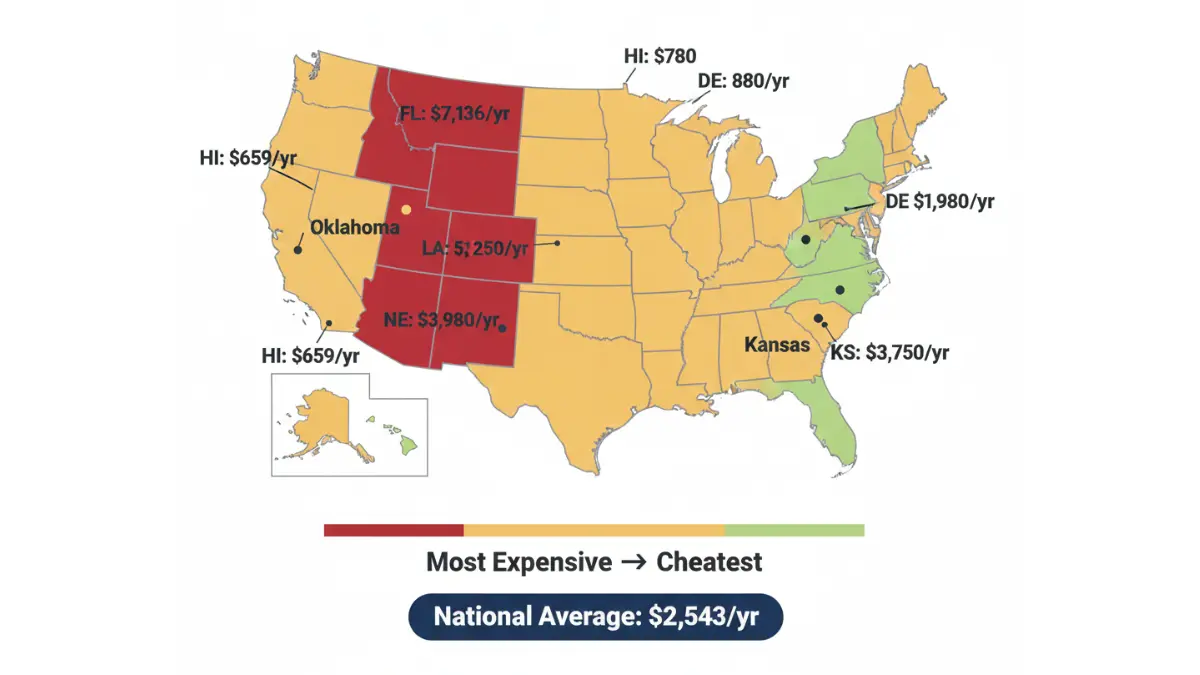

The national average homeowners insurance cost is $2,543/year for a policy with $300,000 in dwelling coverage, a $300,000 liability limit, and a $1,000 deductible. But state-level variation is extreme.

Top 5 Most Expensive States (2026):

| State | Average Annual Premium | Why So High |

|---|---|---|

| 🔴 Florida | $7,136 | Hurricanes, litigation, insurer exits |

| 🔴 Louisiana | ~$5,800 | Hurricane + flooding risk |

| 🔴 Oklahoma | ~$4,900 | Tornadoes, hail |

| 🔴 Nebraska | ~$4,600 | Hail + 20%+ rate hike in 2024 |

| 🔴 Kansas | ~$4,300 | Tornado corridor |

Top 5 Cheapest States (2026):

| State | Average Annual Premium |

|---|---|

| 🟢 Hawaii | $659 |

| 🟢 Vermont | ~$900 |

| 🟢 Delaware | ~$950 |

| 🟢 Alaska | ~$1,000 |

| 🟢 New Hampshire | ~$1,050 |

Florida Reality Check: Florida homeowners pay 181% above the national average. Multiple major insurers have exited the state entirely. If you’re in Florida, shopping your policy every single year is not optional — it’s essential.

The 2026 Rate Crisis: What’s Coming

Two major forecasts paint different pictures for 2026:

- Cotality (real estate analytics): Projects home insurance rates will increase 8% in 2026 and another 8% in 2027, driven by extreme weather, tariffs, and rising construction material costs

- Swiss Re (global reinsurer): Projects a more moderate 3% increase for 2026, citing some market stabilization

The truth likely sits between both forecasts — and varies dramatically by state.

The Colorado Case Study (Competitor Blind Spot): Home insurance rates in Colorado increased by 91% between 2020 and 2025, according to ValuePenguin data. This is not a Florida or Louisiana story. This is happening in mainstream states across the country.

5 Factors That Drive YOUR Personal Premium

- Credit score — Homeowners with poor credit pay 137% more on average than those with excellent credit

- Home age and construction — Older homes with outdated electrical or plumbing face higher rates

- Roof type and age — Hip roofs (4 sloping sides) cost less to insure than gable roofs; impact-resistant roofing earns discounts

- Claims history — Filing even one claim can raise premiums for 3–5 years

- Distance from fire station — Homes within 5 miles of a fire station qualify for better fire protection class ratings

Understanding your premium drivers is the first step to reducing them. If your insurance costs are straining your monthly budget alongside debt payments, our Debt Consolidation Calculator can help you find real financial breathing room.

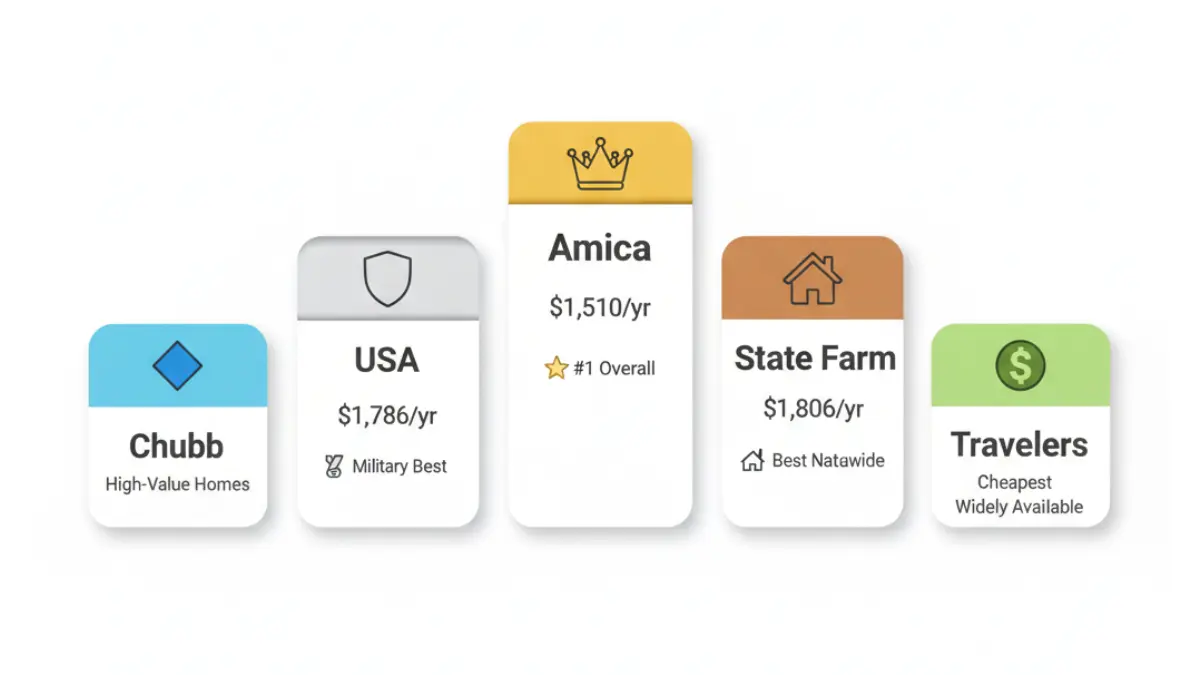

Best Homeowners Insurance Companies 2026 — Expert-Ranked

Top 5 Companies at a Glance

Our expert panel evaluated companies across J.D. Power satisfaction scores, NAIC complaint ratios, AM Best financial strength ratings, average premiums, and claims processing performance.

| Company | Best For | Avg Annual Cost | J.D. Power Score | AM Best |

|---|---|---|---|---|

| Amica | Overall + Customer Satisfaction | $1,510 | 705/1,000 ✅ #1 | A+ |

| USAA | Military Families | $1,786 | 746 (unranked) | A++ |

| State Farm | Nationwide Availability + Budget | $1,806 | Top 5 | A++ |

| Chubb | High-Value Homes | $3,048+ | #1 Claims (2025) | A++ |

| Travelers | Cheapest Widely Available | $2,055 | Competitive | A++ |

Expert Panel Note — FinanceAuthorityHub: “Amica’s combination of low complaint ratio, strong claims handling, and below-average premiums makes it the standout choice for most US homeowners in 2026. USAA remains the gold standard for military families, but eligibility restrictions apply.” — FinanceAuthorityHub Financial Expert Panel

The Metric That Competitors Don’t Mention: Claims Processing Time

Every competitor article focuses on premium and satisfaction scores. None of them highlight what happens after you file a claim.

According to J.D. Power’s 2025 US Home Insurance Study, the average claim cycle is now 44 days from first notice of loss to final payment — the longest recorded since the study began in 2008. When evaluating insurers, ask:

- What is their average claim resolution time in your state?

- Do they have a dedicated claims app with real-time tracking?

- What is their NAIC complaint index for claims handling specifically?

A lower premium is worthless if you’re waiting 60 days for your home to be repaired after a storm.

3 Key Metrics to Evaluate Any Homeowners Insurance Company

- NAIC Complaint Index: Below 1.0 is good; below 0.5 is excellent. Find verified scores at the NAIC Consumer Information Source

- AM Best Financial Strength Rating: Only consider companies rated A (Excellent) or above

- J.D. Power Satisfaction Score: Segment average is 642/1,000 for 2025; aim for companies scoring above this threshold

If you’re also considering life insurance alongside your homeowners coverage, compare costs in our life insurance rates and types guide to see the full picture of your household protection costs.

11 Proven Ways to Stop Overpaying on Homeowners Insurance in 2026

This is the section your current insurer hopes you never read.

1. Shop and Compare Quotes — Save an Average of $482/Year

The single most effective strategy. Rates for identical coverage vary by thousands of dollars between carriers. The Texas Department of Insurance recommends getting at least 3 quotes at every renewal. Most homeowners never do this.

Action step: Get quotes from at least 3 carriers — one national brand, one regional carrier, and one independent agent quote. Regional carriers frequently offer better rates and fewer complaints.

2. Bundle Home and Auto Insurance — Save 5–15%

Bundling your homeowners and auto policies with the same insurer typically earns a 5–15% discount. But — and this is critical — always compare bundled vs. separate rates. The bundle discount doesn’t always produce the cheapest combined total.

To understand how your auto insurance compares, see our car insurance cost-cutting guide for 2026.

3. Raise Your Deductible Strategically — Save 12–20%

Moving your deductible from $1,000 to $2,500 cuts your premium by 12–20% on average. Park the annual savings difference in a high-yield savings account earning 4–5% APY. Within 3 years, you’ve built your higher deductible covered even if a claim occurs.

4. Improve Your Credit Score

In most states, your credit score directly impacts your homeowners insurance premium. Homeowners with poor credit pay 137% more than those with excellent credit. Even moving from “fair” to “good” credit can trigger meaningful premium reductions at renewal.

Note: California, Maryland, Massachusetts, and Hawaii prohibit insurers from using credit in rate setting.

5. Install Security and Safety Systems — Save Up to 20%

- Monitored burglar alarm: up to 20% discount depending on insurer

- Smoke detectors and dead-bolt locks: at least 5% discount

- Smart water leak detection sensors: increasingly recognized by major insurers for additional discounts

Ask your insurer directly which devices qualify and what verification is required.

6. Upgrade to an Impact-Resistant Roof

In high-risk states, switching to impact-resistant roofing can cut 5–10% off premiums. In Florida, a positive wind mitigation inspection report can reduce your premium significantly. Check whether your state has a FORTIFIED™ Home designation program (run by the Insurance Institute for Business & Home Safety) — qualifying homes earn large discounts in participating states.

7. Review Your Replacement Cost — Not Your Market Value

Many homeowners are insuring their home for its purchase price rather than its rebuilding cost. These are very different numbers. The land under your home has no replacement cost — only the structure does.

Have a licensed insurance professional review your replacement cost estimate every 5–7 years. Overinsuring on dwelling coverage is money wasted every single year.

8. Ask About Hidden Discounts

Most insurers offer discounts that are never proactively mentioned:

- Retiree discount — retirees statistically maintain homes better and spot hazards earlier

- New homebuyer discount — available in the first year with many carriers

- Claims-free discount — typically unlocks after 3 consecutive years with no claims

- Auto-pay and paperless billing discount — small but free savings

- Paid-in-full discount — paying annually instead of monthly saves 5–8% with many carriers

9. Be Strategic About Filing Small Claims

Filing a claim for minor damage often costs more long-term than paying out of pocket. A single claim can raise your renewal premium for 3–5 years and eliminate your claims-free discount. If the repair cost is within $500–$1,000 of your deductible, strongly consider self-insuring that loss.

10. Request a Fire Protection Class Re-Inspection

Every home is assigned a fire protection class rating based on proximity to fire stations and fire hydrants. If your rating hasn’t been updated recently and a new station has opened nearby, you may qualify for a lower rate. Contact your county or local fire department to initiate a re-inspection.

11. Reduce “Other Structures” Coverage If Appropriate

Other structures coverage defaults to 10% of your dwelling limit. If you live on a small lot with minimal detached structures, you may be paying for coverage you don’t need. Ask your agent if this limit can be reduced — but only do this if it genuinely reflects your property.

💡 What This Means For You: Implementing just 3–4 of these strategies — shopping quotes, raising your deductible, bundling, and improving credit — can realistically save $600–$1,200 per year on your homeowners insurance premium. That’s a mortgage payment.

FAQs About Homeowners Insurance (2026)

Q1: What is homeowners insurance?

Homeowners insurance is a financial protection policy covering your home’s structure, personal belongings, and personal liability. Most mortgage lenders require it as a condition of your loan.

Q2: How much does homeowners insurance cost in 2026?

The national average is $2,543/year for $300,000 in dwelling coverage. Florida averages $7,136/year — the highest in the US. Hawaii averages just $659/year — the lowest. Your personal rate depends on location, home age, credit score, and coverage level.

Q3: What does homeowners insurance cover?

Standard policies cover dwelling damage, personal property, other structures, personal liability, loss of use, and medical payments for guests. Flood and earthquake damage require separate policies.

Q4: Is homeowners insurance legally required?

No state law requires it. However, virtually every mortgage lender mandates coverage. Approximately 12% of US homeowners currently have no coverage — leaving them fully exposed to catastrophic financial loss.

Q5: What is the most common type of home insurance policy?

The HO-3 (Special Form) is the standard for single-family homes. It covers your home’s structure on an open-perils basis but covers personal belongings only for named perils. The HO-5 provides broader open-perils coverage for both.

Q6: Does homeowners insurance cover floods?

No. Flood damage is explicitly excluded from standard homeowners policies. You need a separate flood insurance policy, available through the National Flood Insurance Program (NFIP) or a private flood insurer. Critically, nearly one-third of all NFIP flood claims come from properties outside designated high-risk flood zones.

Q7: How can I lower my homeowners insurance premium?

The five most impactful strategies are: (1) compare quotes annually, (2) bundle home and auto, (3) raise your deductible, (4) improve your credit score, and (5) install security systems. Shopping around alone saves an average of $482/year. See our full guide on cutting insurance costs in 2026 for the complete playbook.

Q8: Will my homeowners insurance premium go up in 2026?

Most likely, yes. Analysts project 3–8% increases nationally in 2026, driven by extreme weather events, tariffs on construction materials, and inflation in labor costs. Some states — particularly Florida, Louisiana, and Colorado — face far steeper increases.

Q9: What is dwelling coverage?

Dwelling coverage pays to repair or rebuild your home’s physical structure after a covered event. Your coverage limit should equal your home’s full replacement cost — not its market value or tax assessment. These numbers can differ by tens of thousands of dollars.

Q10: What is a homeowners insurance deductible?

Your deductible is the amount you pay out of pocket before your insurer covers a claim. The most common deductible is $1,000. Raising it to $2,500 typically saves 12–20% on annual premiums — a smart trade-off if you have emergency savings to cover the difference.

Q11: Which homeowners insurance company is best in 2026?

Amica ranks #1 for overall customer satisfaction and has one of the lowest NAIC complaint ratios in the industry, with an average annual premium of $1,510. USAA is the top choice for military families at $1,786/year. Chubb is the leading option for high-value homes. Always compare quotes before committing — rates vary significantly even for the same coverage level.

Related Guides: If you’re in the process of buying a home, our first-time home buyer guide for 2026 walks through every cost to budget for — including insurance. Already a homeowner exploring your equity? See 4 ways to use your home equity in 2026. If you’re also reviewing renters insurance for a family member or investment property, our renters insurance guide for 2026 covers everything.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.