Business Insurance Costs Revealed: What No One Tells You

Business insurance costs $65–$141/month in 2026 — but most owners are dangerously underinsured. See real costs by industry and avoid 6 claim denial traps.

In This Article

Business insurance costs $65–$141 per month on average in 2026 — but that number alone will not protect you. According to the U.S. Small Business Administration, accidents, natural disasters, and lawsuits can run a business into the ground overnight. What NerdWallet, Bankrate, and Investopedia won’t tell you: roughly 3 in 4 small businesses are dangerously underinsured — and most only discover it when a claim is denied.

This guide reveals exactly what business insurance costs by industry in 2026, which types you actually need, and the 6 claim-denial traps that quietly destroy small businesses every year.

What you’ll learn:

- Real 2026 cost data broken down by policy type and industry

- The 7 types of business insurance — and which one fits your business

- Why claims get denied (and how to prevent it)

- A step-by-step buying guide to avoid overpaying

- 11 expert-answered FAQs covering every major question

What Is Business Insurance — And Why Most Owners Are Underprotected

Business insurance is a group of commercial policies that protect your business from financial losses caused by lawsuits, property damage, employee injuries, cyber attacks, and forced closures. It is not a single product — it is a customized portfolio of coverage types.

Many business owners assume an LLC structure fully protects them. It does not. According to the SBA, an LLC protects your personal assets from certain lawsuits, but it cannot cover property destruction, employee injuries, professional errors, or cyber breaches. Business insurance fills those gaps.

The Underinsurance Crisis Nobody Talks About

The U.S. SBA reports that approximately 3 in 4 small businesses are underinsured. Between March 2021 and March 2022 alone, over 917,000 U.S. businesses closed — with small businesses accounting for more than 833,000 of those closures.

Many of those closures were preventable with the right commercial insurance coverage in place.

Which Businesses Are Legally Required to Have Insurance?

| Insurance Type | Who Legally Needs It |

|---|---|

| Workers’ Compensation | Most businesses with employees (state laws vary) |

| Commercial Auto | Any business using vehicles for operations |

| Disability Insurance | Required in some states (California, New York, New Jersey, Hawaii, Rhode Island) |

| Unemployment Insurance | Federal requirement for all businesses with employees |

Key takeaway: Even if you are not legally required to hold a specific policy, the financial risk of going uninsured in most categories far outweighs the premium cost. Use our Debt Consolidation Calculator to see how insurance costs fit into your overall financial obligations.

Business Insurance Costs Revealed — 2026 Real Data by Industry

This is the section competitors fail to deliver. Here is the real 2026 cost data you need before purchasing any commercial insurance policy.

Average Business Insurance Cost by Policy Type (2026)

| Policy Type | Avg Monthly Cost | Avg Annual Cost | Best For |

|---|---|---|---|

| General Liability | $42–$100 | $500–$1,200 | All businesses — the baseline |

| Business Owner’s Policy (BOP) | $67–$115 | $800–$1,380 | Small businesses with a physical location |

| Professional Liability (E&O) | $61–$72 | $732–$864 | Consultants, freelancers, service providers |

| Workers’ Compensation | $45–$69 | $540–$828 | Any business with employees |

| Commercial Auto | $137–$147 | $1,644–$1,764 | Vehicle-dependent operations |

| Cyber Liability | $145–$200 | $1,740–$2,400 | Any business storing customer data |

| Business Interruption | Bundled in BOP | $0–$500 add-on | Any business with physical operations |

Source: MoneyGeek study of 79 industries and 5 major coverage types, 2026

Business Insurance Cost by Industry — What Competitors Hide

This is the breakdown NerdWallet and Bankrate bury or skip entirely:

| Industry | Avg Monthly Premium | Risk Classification |

|---|---|---|

| Freelancer / Consultant | $40–$65 | Low |

| Home-Based Business | $35–$75 | Low |

| Tech Startup | $85–$150 | Low–Medium |

| Retail Store | $100–$175 | Medium |

| Restaurant / Food Service | $125–$225 | High |

| Contractor / Construction | $175–$350 | Very High |

| Healthcare / Medical Services | $200–$500+ | Highest |

What Drives Your Premium Up — or Down

Your small business insurance quote is shaped by these 8 factors:

- Industry risk classification — Construction pays far more than accounting

- Number of employees — Each additional employee adds 5–10% to your premium

- Annual business revenue — Revenue over $1M increases premiums by 15–25%

- Location — High-crime or disaster-prone areas cost more

- Claims history — Prior claims signal higher future risk to insurers

- Coverage limits — Doubling your limit raises premiums by 25–50%

- Deductible level — Raising your deductible from $500 to $2,500 can cut premiums by 10–20%

- Risk management practices — Safety protocols and employee training can reduce rates

Commercial insurance rates rose approximately 3% overall in the first half of 2025 — but specific categories like commercial property and cyber liability saw increases of 10–20% (SmartFinancial / MarketScout, 2025).

4 Proven Ways to Lower Your Business Insurance Premium

- Bundle policies into a BOP — saves 10–15% vs. buying separately

- Pay annually instead of monthly — saves an additional ~5%

- Raise your deductible — can reduce premiums by up to 20%

- Implement workplace safety protocols — lowers workers’ comp and liability rates

If you are managing multiple financial obligations alongside your insurance costs, our Debt Consolidation Calculator can help you prioritize payments effectively.

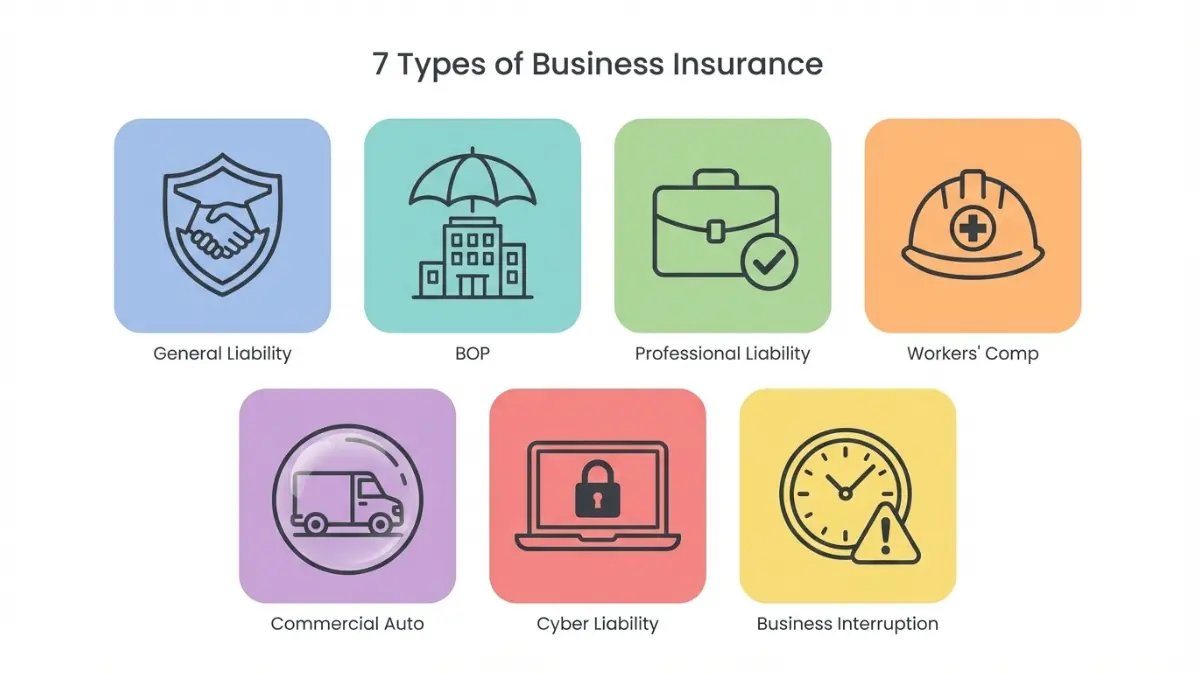

7 Types of Business Insurance — Which One Do YOU Actually Need?

Most competitors list these types without telling you who needs each one. This section fixes that.

1. General Liability Insurance

What it covers: Third-party bodily injury, property damage, and advertising injury lawsuits. Who needs it: Every business, without exception. This is the baseline of commercial insurance. Average cost: $42–$100/month

2. Business Owner’s Policy (BOP)

What it covers: Bundles general liability + commercial property + business interruption into one policy. Who needs it: Small businesses with a physical location — restaurants, retailers, contractors, clinics. Average cost: $67–$115/month — always cheaper than buying policies individually.

3. Professional Liability Insurance (Errors & Omissions)

What it covers: Financial losses caused by your professional advice, services, or errors. Who needs it: Consultants, financial advisors, accountants, lawyers, designers, IT professionals. Average cost: $61–$72/month

4. Workers’ Compensation Insurance

What it covers: Medical bills, lost wages, and rehabilitation costs for employees injured on the job. Who needs it: Any business with employees — legally required in most U.S. states. Average cost: $45–$69/month (varies sharply by industry risk)

5. Commercial Auto Insurance

What it covers: Accidents, vehicle damage, and liability when employees drive for business purposes. Who needs it: Any business using vehicles for operations — delivery, contracting, field services. Critical warning: Personal auto policies deny claims for business use. This gap silently destroys thousands of businesses each year.

6. Cyber Liability Insurance ⚡ (Most Underrated in 2026)

What it covers: Costs of a data breach, ransomware attack, notification expenses, and cyber recovery. Who needs it: Any business that stores customer data, processes payments, or operates online. 2026 data point: The average cyber claim for a small business costs $79,000. According to Fitch Ratings, nearly 1 in 4 cyber insurance claims were denied in 2024 for failing to meet policy requirements. Standard general liability policies do not cover cyber incidents.

7. Business Interruption Insurance

What it covers: Lost income and operating expenses during a forced closure from a covered disaster. Who needs it: Any business dependent on a physical location — yet 68% of small business owners lack this coverage.

For a complete view of your insurance needs across home and business, also read our guides on home insurance costs and how to stop overpaying on insurance.

Quick Decision Table: Which Policies Do You Need?

| Business Type | Gen. Liability | BOP | Prof. Liability | Workers’ Comp | Cyber | Commercial Auto |

|---|---|---|---|---|---|---|

| Freelancer/Consultant | ✅ | — | ✅ | — | ✅ | — |

| Retail Store | ✅ | ✅ | — | ✅ | ✅ | — |

| Restaurant | ✅ | ✅ | — | ✅ | — | ⚠️ |

| Contractor | ✅ | ✅ | — | ✅ | — | ✅ |

| Tech/SaaS Company | ✅ | — | ✅ | ✅ | ✅ | — |

The Hidden Truth — 6 Reasons Your Business Insurance Claim Gets Denied

This is the section NerdWallet, Bankrate, and Investopedia all skip. These are the real reasons claims fail — with real financial consequences.

1. You Used a Personal Auto Policy for Business Use

A restaurant owner’s employee causes an accident during a delivery. The personal auto insurer denies the claim — business use is excluded. The business owner absorbs $47,000 out-of-pocket in damages and legal fees.

Fix: Obtain commercial auto insurance for any vehicle used for business operations.

2. You Didn’t Update Your Policy After Your Business Grew

You hired three new employees. You bought new equipment. You expanded to a second location. None of it is in your policy. Your insurer covers only what you declared at signing.

Failing to update your policy can also be treated as misrepresentation, which gives insurers grounds to deny unrelated claims as well.

3. Your Claim Was Filed Too Late

Most business insurance policies require you to report an incident within 24–72 hours. Waiting to “assess damage first” is the most common reason cyber and property claims are voided. Late filing = automatic denial in most policies.

4. The Incident Falls Under a Policy Exclusion

Standard general liability policies typically exclude: floods, earthquakes, cyber attacks, pandemic-related closures, and employee discrimination claims. If it’s in the exclusion list — your insurer owes you nothing.

The IRS confirms that many business insurance premiums are tax-deductible, which makes proper coverage even more financially rational. Make sure you are buying the right coverage in the first place.

5. Errors in Your Claims Paperwork

A typo in a policy number. An incorrect date. A missing document. These are all grounds for denial. Insurers use rigorous fraud detection systems — any inconsistency triggers scrutiny.

6. Your Coverage Limit Was Too Low

Your general liability policy covers up to $1 million. The lawsuit demands $2.3 million. Your insurer pays $1 million. You absorb the remaining $1.3 million personally.

Bold takeaway: Underinsurance is not just a problem — it is a silent financial crisis. Nearly 1 in 4 cyber claims were denied in 2024 alone. Review your policy exclusions and coverage limits annually.

How to Buy Business Insurance in 2026 Without Getting Ripped Off

This 5-step framework is what our 30 expert panel recommends for every business owner purchasing or renewing commercial coverage.

Step 1 — Conduct a Real Risk Assessment First

Before requesting a single quote, answer these questions:

- Who could realistically sue my business?

- What would a fire, flood, or theft cost me in lost assets?

- Do I have employees? Do any drive vehicles for work?

- Do I store customer data or process payments online?

- What would happen if I had to close for 30–60 days?

Your answers determine which policies are essential vs. optional.

Step 2 — Get Quotes From at Least 3 Providers

Insurance rates for identical coverage can vary by up to 50% across providers. Use an independent broker (not a captive agent tied to one insurer) to access multiple quotes simultaneously.

The SBA advises business owners to compare rates, terms, and benefits from several agents before committing.

Step 3 — Check These 5 Critical Policy Details

Before signing any business insurance policy:

- Read the exclusions page — this is where claims get denied

- Verify coverage limits match your worst-case scenarios

- Confirm cyber liability is included or explicitly added

- Check your state’s legal requirements — workers’ comp rules vary significantly

- Understand the claims filing window — typically 24–72 hours after an incident

Step 4 — Bundle Policies to Maximize Savings

A Business Owner’s Policy (BOP) bundles general liability + property + business interruption into one package at 10–15% less than buying separately. Paying your annual premium upfront instead of monthly saves an additional ~5%.

Step 5 — Review Your Coverage Every 12 Months

Your business is not static. New employees, new equipment, new locations, and new revenue streams all change your risk profile. The SBA recommends reassessing your business insurance coverage every year — especially after any major operational change.

Planning to expand your business with a property purchase or refinance? Our Mortgage Calculator, Mortgage Refinance Calculator, and Home Affordability Calculator help you factor all costs into your financial plan. Also, learn how debt types and risks in 2026 could affect your business’s financial health.

Frequently Asked Questions about Business Insurance

Q1: What is the average cost of business insurance in 2026?

Business insurance averages $65–$141 per month ($780–$1,687/year) depending on coverage type and industry. General liability alone averages $42–$100/month for most small businesses.

Q2: Is business insurance tax deductible?

Yes. According to the IRS, you can generally deduct the ordinary and necessary cost of insurance as a business expense if it is for your trade, business, or profession. This includes general liability, commercial auto, workers’ compensation, and business interruption premiums.

Q3: What business insurance is legally required?

The federal government requires workers’ compensation, unemployment insurance, and disability insurance for all businesses with employees. Some states require additional coverage. Check your state’s specific requirements via the SBA.

Q4: What is a Business Owner’s Policy (BOP)?

A BOP bundles general liability + commercial property + business interruption insurance into one discounted policy. It is the most cost-effective option for small businesses with a physical presence, averaging $67–$115/month.

Q5: Does general liability insurance cover cyber attacks?

No. Standard general liability policies explicitly exclude cyber incidents. You need a separate cyber liability insurance policy. The average small business cyber claim costs $79,000 — and 1 in 4 cyber claims were denied in 2024 for not meeting requirements.

Q6: Can I use personal insurance for my business?

No. Personal auto and homeowners policies exclude commercial activity. Using personal policies for business purposes and then filing a claim will result in denial. This is one of the most expensive mistakes small business owners make.

Q7: How much does business insurance cost for a sole proprietor?

A sole proprietor can typically obtain general liability coverage for $400–$600/year. Adding professional liability brings the total to $800–$1,200/year. Home-based business endorsements are available from $150–$300/year.

Q8: What does business interruption insurance cover?

It covers lost net income and operating expenses (rent, utilities, payroll) during a forced closure caused by a covered disaster such as fire, storm damage, or equipment failure. The standard restoration period is 30 days, extendable to 360 days.

Q9: When can a business insurance claim be denied?

Claims are most commonly denied for: late filing beyond the policy window, excluded perils, coverage limits exceeded, using personal policies for business, errors in paperwork, and failure to update the policy after business changes.

Q10: How can I lower my business insurance premium?

Bundle policies into a BOP, pay annually instead of monthly, raise your deductible, implement documented safety protocols, compare quotes from at least 3 providers, and review coverage every 12 months to remove outdated items.

Q11: Do I need business insurance if I work from home?

Yes. Standard homeowners insurance policies do not cover business equipment, client injuries, or professional liability for home-based operations. You need either a home-based business endorsement or a separate Business Owner’s Policy.

For more ways to protect your financial health in 2026, explore our complete guide on life insurance costs and types, and see how your income tax brackets for 2026 affect your deduction strategy.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.