Break Paycheck Cycle: 30-Day Plan (2026 Guide)

Discover the systematic 30-day plan that breaks the paycheck-to-paycheck cycle. Includes budget optimization, emergency fund strategies, and income acceleration tactics for 2026.

In This Article

Why 78% Of Americans Are Trapped In The Paycheck Cycle (2026 Reality Check)

The paycheck-to-paycheck crisis reached an unprecedented level in 2026. According to the Federal Reserve’s latest Economic Well-Being survey, 78% of American workers now live paycheck to paycheck, up from 64% just three years ago. This isn’t about income level anymore—even households earning $100,000+ report financial fragility.

The numbers tell a brutal story. January 2026 inflation data from the Bureau of Labor Statistics shows core expenses rising 3.4% year-over-year while wage growth stagnates at 2.1%. Your paycheck buys less, while rent, groceries, and healthcare costs accelerate beyond your income’s reach.

But here’s what separates people who break free from those who stay trapped: a systematic 30-day plan. Not generic budgeting advice. Not willpower. A surgical protocol that attacks the paycheck cycle from multiple angles simultaneously.

The psychological cost extends beyond bank accounts. The American Psychological Association reports money stress affects 72% of Americans’ mental health, disrupting sleep, relationships, and career performance. One unexpected car repair or medical bill becomes a crisis instead of an inconvenience.

This guide delivers what others won’t: specific dollar amounts, week-by-week action steps, and the exact tools to build your first $1,000 emergency fund while simultaneously optimizing your budget. No fluff. No theory. Just the championship playbook that ends the cycle in 30 days.

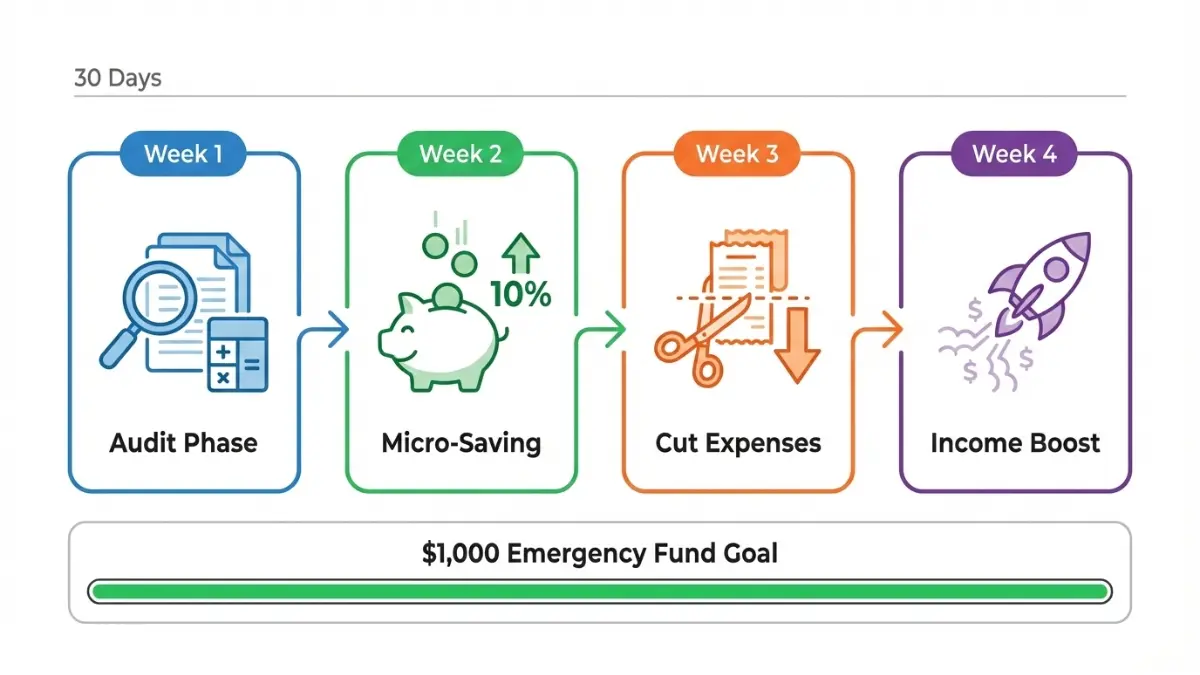

Your 30-day Plan To Break The Paycheck Cycle

Week 1: Financial Awareness Audit

Your first seven days focus on brutal honesty about money flow. Track every dollar using the 50/30/20 budget framework we’ve refined for 2026 inflation realities. Download your last 90 days of bank statements and categorize each transaction into needs, wants, and savings.

Calculate your actual paycheck utilization rate. Most people discover 15-23% of spending goes to forgotten subscriptions, impulse purchases, and “lifestyle creep” expenses they can’t remember authorizing. Use our Budget Calculator to identify your baseline spending across eight core categories.

The goal isn’t judgment—it’s data. By day seven, you’ll know your exact financial starting point, including hidden money leaks draining $200-$400 monthly from your paycheck before you even notice.

Week 2: Micro-Saving Implementation

Week two activates your first emergency fund deposits. The Consumer Financial Protection Bureau recommends starting with just $500 for psychological momentum. Open a high-yield savings account offering 4.5-5.0% APY—our comparison of banks with zero fees shows current rates from FDIC-insured institutions.

Implement the “paycheck splitting strategy”: route 10% of each paycheck directly to savings before it touches your checking account. This isn’t willpower—it’s automation that removes temptation entirely. For a $3,000 monthly paycheck, that’s $300 monthly or $150 per bi-weekly deposit.

Enable round-up savings through your banking app. Every purchase rounds to the nearest dollar, transferring the difference to savings. This micro-saving approach accumulates $40-$80 monthly without lifestyle disruption, leveraging the psychological power of invisible savings.

Week 3: Expense Elimination Sprint

The third week targets your highest-impact expense cuts. Review week one’s audit and identify three categories for aggressive reduction. Most households find $300-$600 in monthly savings through strategic cuts, not deprivation.

Cancel unused subscriptions immediately—the average American pays for 4.7 services they don’t use regularly. Renegotiate your car insurance (comparison shopping saves $400-$800 annually). Switch to a cheaper phone plan (MVNOs offer identical coverage for 40-60% less than major carriers).

Apply the “72-hour rule” to all non-essential purchases over $50. This cooling-off period eliminates 68% of impulse spending according to behavioral economics research. Your paycheck cycle breaks when you stop treating checking account balances as “available to spend” money.

Week 4: Income Acceleration Protocol

Week four launches your side income strategy. The Bureau of Labor Statistics reports 41% of workers now supplement income through gig work or side businesses. Your goal: add $200-$500 monthly within 30 days of starting.

Identify your monetizable skills using our income assessment framework. Freelance writing, virtual assistance, tutoring, or delivery services offer immediate cash flow. Platforms like Upwork, Fiverr, and TaskRabbit provide built-in customer bases requiring zero marketing investment.

Simultaneously, prepare your salary negotiation case if employed full-time. Research market rates for your position, document your achievements, and schedule the conversation. A 5% raise on $50,000 salary equals $2,500 annually—$208 monthly added to your paycheck without extra hours worked.

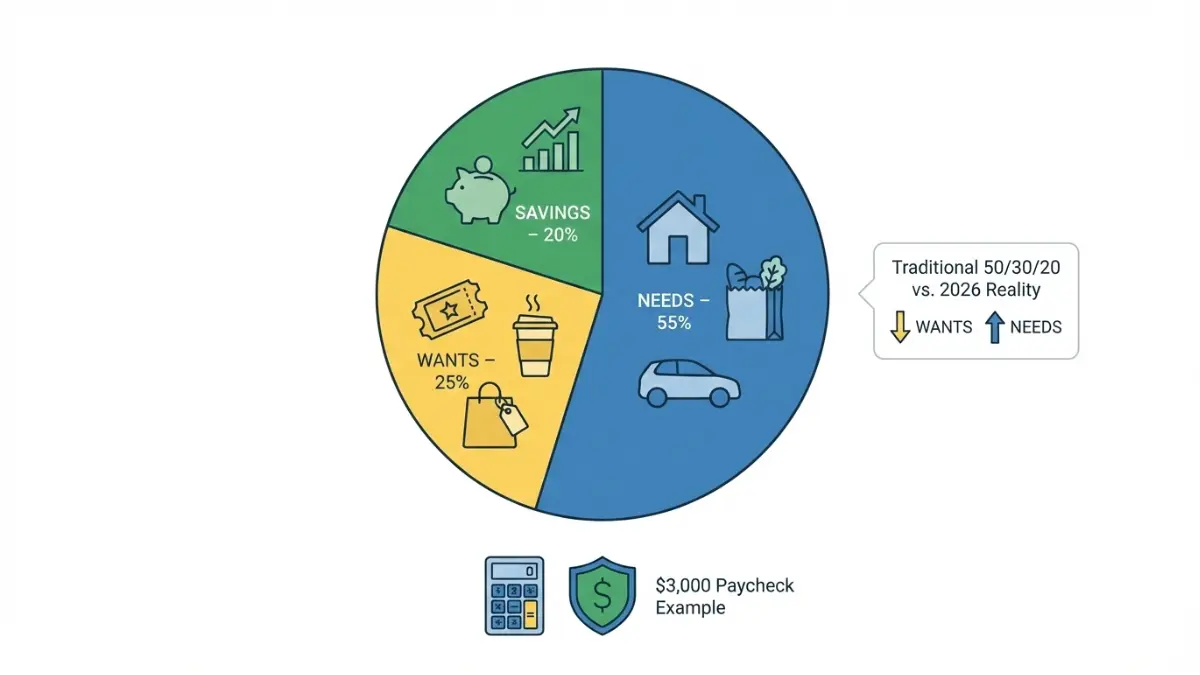

The 2026 Budget System That Ends The Cycle

50/30/20 Rule (2026 Inflation-Adjusted)

The traditional 50/30/20 budget framework requires modification for 2026’s economic reality. With housing costs consuming 35-40% of median incomes in most metro areas, strict adherence becomes impossible. Our refined approach adjusts to 55/25/20 for high-cost-of-living areas.

Allocate 55% to true needs: housing, utilities, groceries, transportation, insurance, and minimum debt payments. Limit wants to 25%—dining out, entertainment, hobbies, and non-essential shopping. Protect the 20% savings allocation aggressively, treating it as a non-negotiable bill your paycheck must cover first.

Track your ratios monthly using our Budget Calculator. When needs exceed 60%, you’re in the danger zone where one emergency creates immediate paycheck cycle stress. The solution isn’t shame—it’s strategic income increase or housing cost reduction.

Zero-Based Budgeting for Irregular Income

Freelancers, commission-based workers, and gig economy participants need different frameworks. Zero-based budgeting assigns every dollar a specific job before spending occurs, crucial when your paycheck varies $500-$2,000 monthly.

Start with your lowest-earning month from the past year as your baseline budget. Cover essential expenses from this floor, then allocate surplus income from better months to savings, debt acceleration, and discretionary spending—in that priority order.

Build a “income smoothing account” that captures extra earnings during peak months, then supplements lean periods. This self-created paycheck consistency breaks the feast-or-famine cycle destroying irregular income earners’ financial stability.

Paycheck Splitting Strategy

The moment your paycheck deposits, execute this protocol: 20% to savings (split between emergency fund and long-term goals), 30% to fixed monthly bills, 50% to variable expenses and discretionary spending. Use separate checking accounts if needed—physical separation prevents accidental overspending from your rent money.

Automate everything possible. According to research from the National Endowment for Financial Education, automated savings systems increase follow-through rates by 73% compared to manual transfers. Your paycheck cycle ends when the system runs itself without requiring daily willpower or decision-making.

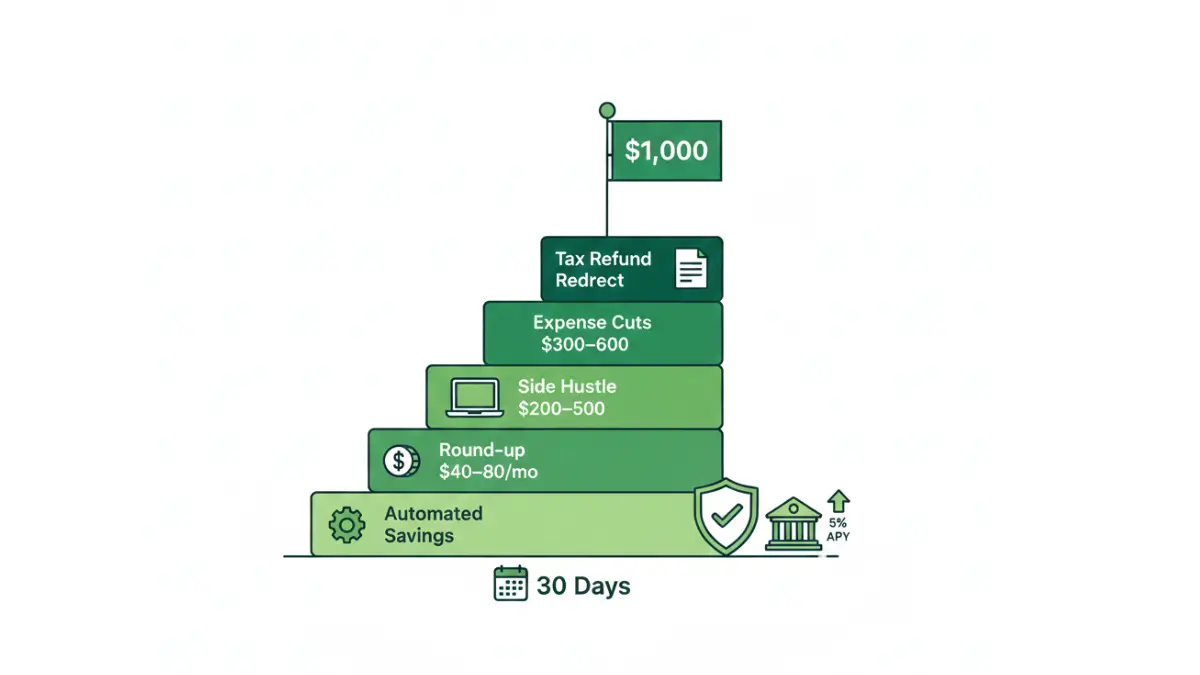

Build Your $1,000 Safety Net In 30 Days

The Emergency Fund Priority Matrix

Breaking the paycheck cycle requires buffer money that absorbs life’s inevitable shocks. The FDIC recommends starting with $500-$1,000 before tackling debt aggressively—this prevents backsliding when emergencies force new credit card charges.

Your 30-day emergency fund sprint uses the 52-week savings plan compressed format. Instead of year-long accumulation, contribute $33 daily ($231 weekly) to reach $1,000 in exactly 30 days. For most households, this requires combining expense cuts from week three with income boosts from week four.

Calculate your personalized emergency fund target using our Emergency Fund Calculator. While $1,000 starts the buffer, your complete goal depends on income stability, household size, and risk factors like health conditions or job security concerns.

Micro-Saving Tactics That Actually Work

Leverage every financial tool for passive accumulation. Enable round-up savings that turns $3.47 purchases into $4.00 charges, banking the $0.53 difference automatically. Monthly accumulation: $40-$80 without behavior change.

Redirect windfalls immediately—tax refunds, bonuses, gift money, freelance payments. The average tax refund reached $3,011 in 2024 according to IRS data. Banking this single deposit covers your entire starter emergency fund plus three months of additional savings.

Implement the “savings challenge” psychology: match every $20 restaurant meal with a $20 savings deposit. This 1:1 ratio maintains lifestyle enjoyment while forcing parallel wealth building, training your brain to associate spending with saving automatically.

High-Yield Savings Accounts (2026 Rates)

Your emergency fund must earn competitive interest while remaining instantly accessible. As of January 2026, top-tier high-yield savings accounts offer 4.50-5.00% APY compared to traditional banks’ 0.01-0.10% rates—a 50x return difference.

Our analysis of zero-fee banks identifies FDIC-insured institutions offering maximum rates without minimum balance requirements or monthly fees. On a $1,000 emergency fund, 5.00% APY generates $50 annually versus $1 at traditional banks—real money defending against inflation’s erosion of your paycheck’s purchasing power.

Boost Your Paycheck: 2026 Income Acceleration Guide

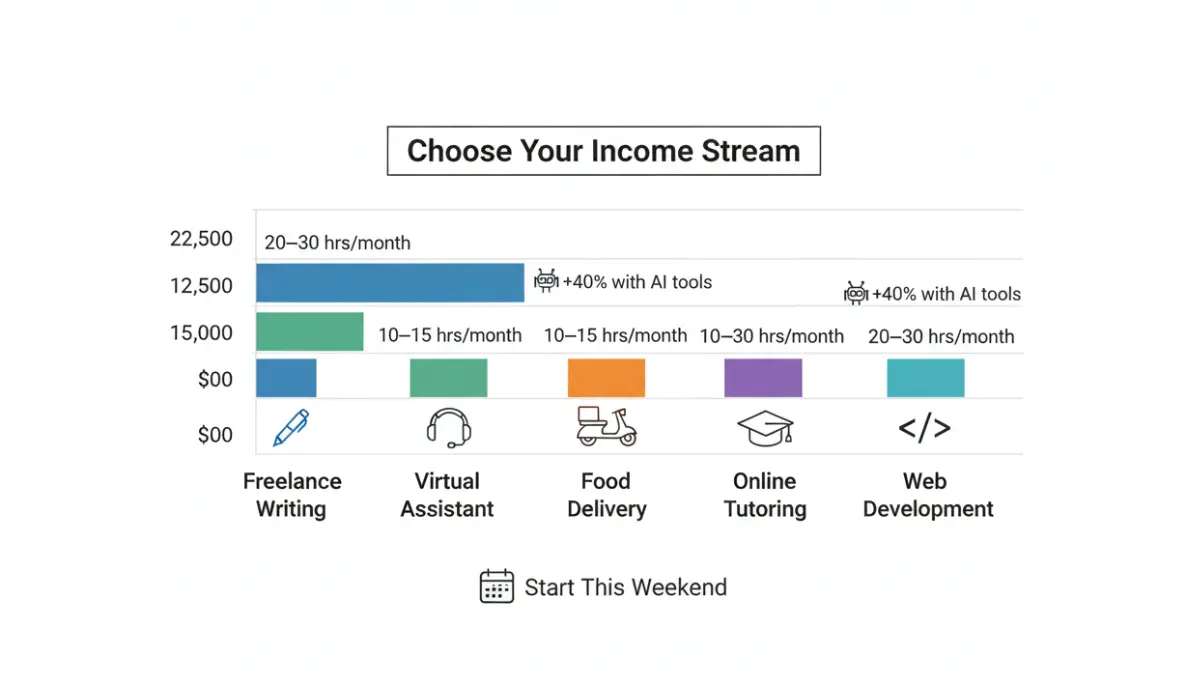

Side Hustle Matrix (Skill-to-Income Mapping)

The fastest paycheck cycle escape combines expense optimization with income expansion. Current labor market data shows side income averaging $810 monthly for active participants, though ranges vary dramatically by time investment and skill level.

High-income skills (20-30 hours monthly):

- Freelance writing: $500-$2,000/month

- Virtual assistance: $400-$1,200/month

- Online tutoring: $600-$1,800/month

- Graphic design: $800-$2,500/month

- Web development: $1,500-$5,000/month

Low-barrier opportunities (10-15 hours monthly):

- Food delivery: $300-$700/month

- Rideshare driving: $400-$900/month

- Pet sitting: $200-$600/month

- House cleaning: $300-$800/month

Start with one income stream requiring minimal startup investment. Your paycheck needs immediate supplementation, not business plans or extensive training. Focus on “this weekend” opportunities that generate first dollars within 7-14 days of starting.

Salary Negotiation Framework

Your existing paycheck likely underpays your market value by 5-15%. Bureau of Labor Statistics wage data provides occupation-specific salary ranges by geographic area—research your exact role and location before negotiations begin.

Document three concrete achievements from the past 12 months with quantifiable business impact. Frame your request around market data, not personal financial need. Timing matters: approach conversations during budget planning cycles or after major project completions, never during company financial stress periods.

A 5% raise on median household income ($74,580 in 2023) adds $3,729 annually or $310 monthly to your paycheck—permanent income increase requiring zero additional hours worked compared to side hustles.

AI-Powered Income Opportunities

The 2026 economy rewards AI-augmented skills. Freelancers using ChatGPT for content creation, Midjourney for design work, or Claude for research tasks complete projects 40-60% faster, increasing effective hourly rates without raising client prices.

Learn one AI tool deeply this month. Content creators using AI assistants report income increases of $300-$800 monthly from expanded client capacity. Your paycheck cycle breaks faster when technology multiplies your productive output without requiring proportional time investment.

Strategic Debt Payoff While Building Your Safety Net

The paycheck cycle often includes debt payments consuming 15-30% of monthly income. Strategic payoff accelerates freedom without sacrificing emergency fund building—the key is simultaneous execution, not sequential.

The Modified Avalanche Method prioritizes high-interest debt (credit cards at 18-29% APR) while maintaining minimum payments on everything else. Calculate your optimal strategy using our Debt Payoff Calculator—most households save $1,200-$3,400 in interest by attacking highest-rate balances first.

For credit card debt specifically, explore 0% APR balance transfer cards offering 15-21 month interest-free periods. This strategy saved users an average of $2,847 in interest charges according to our case analysis, converting every payment to pure principal reduction.

Debt consolidation makes sense when multiple high-interest debts create payment confusion and stress. Our comprehensive guide shows when consolidation saves money versus when it extends repayment unnecessarily. The decision depends on your credit score, total debt load, and current interest rates.

Student loan and medical debt require specialized approaches. Federal student loans offer income-driven repayment plans that adjust payments to your paycheck’s reality. Medical debt often negotiates to 40-60% of billed amounts when you request itemized billing and payment plans directly from providers.

Build your $1,000 emergency fund first, then split extra money 50/50 between emergency fund expansion and debt acceleration until you reach 3-6 months of expenses saved.

Frequently Asked Questions

1. How long does it take to break the paycheck cycle?

Most people achieve meaningful progress in 30-90 days using our systematic approach. Building a complete 3-6 month emergency fund typically requires 6-18 months depending on income and expense levels.

2. What is the fastest way to save $1,000 for emergencies?

Combine expense elimination ($300-$600 monthly) with income boost ($200-$500 monthly) for 30-45 day achievement. Redirect your next tax refund or bonus for instant funding.

3. Can I save money while paying off debt?

Yes—build your starter $1,000 emergency fund first, then split extra money 50/50 between savings growth and debt acceleration until you reach 3-6 months of expenses saved.

4. What budget method works best for irregular income?

Zero-based budgeting using your lowest-earning month as the baseline, with surplus income allocated to savings, debt, and discretionary spending in that priority order.

5. How much should I save from each paycheck?

Target 20% of gross income for combined emergency fund and retirement savings. Start with 10% if 20% feels impossible, increasing by 2% every three months as income grows or expenses decrease.

6. What are the best side hustles in 2026?

AI-augmented freelancing (writing, design, virtual assistance) offers highest income-to-time ratios at $25-$75 hourly. Delivery services provide fastest cash flow for immediate paycheck supplementation.

7. Should I focus on saving or paying off debt first?

Save $1,000 for emergencies first to prevent new debt during unexpected expenses, then tackle high-interest debt (18%+ APR) aggressively while building savings to 3-6 months of expenses.

8. How do I stop overspending between paychecks?

Automate your budget with paycheck splitting—route savings and bills immediately upon deposit, leaving only discretionary spending money in your main checking account.

9. What percentage of Americans live paycheck to paycheck?

78% as of 2026 according to Federal Reserve data, up from 64% three years prior—affecting even high-income households earning $100,000+ annually.

10. Can you build an emergency fund in 30 days?

Yes—a starter $1,000 fund requires $33 daily savings, achievable through combined expense cuts and income boosts implemented simultaneously during your first month.

11. What is a realistic emergency fund goal for beginners?

Start with $500-$1,000 for immediate crisis buffer, then build toward 3-6 months of essential expenses ($10,000-$25,000 for most households) over 12-24 months.

Financial Disclaimer

This guide provides educational information about personal finance strategies and budgeting techniques. We are not certified financial advisors, and this content does not constitute professional financial, legal, or tax advice. Individual financial situations vary significantly based on income, expenses, debt levels, credit scores, and personal circumstances.

All statistics, interest rates, and savings account yields mentioned are accurate as of January 2026 but may change. Past budgeting results and debt payoff timelines do not guarantee future financial outcomes. Investment strategies, debt consolidation, and balance transfer approaches carry risks including potential fees, credit score impacts, and extended repayment periods.

The tools and calculators referenced provide estimates based on your inputs but cannot account for all personal variables affecting your financial decisions. External links to government sources (.gov), educational institutions (.edu), and financial organizations (.org, .com) are provided for informational purposes—we do not control their content or guarantee their ongoing accuracy.

Before making major financial decisions including debt consolidation, balance transfers, investment changes, or employment transitions, consult with a certified financial planner (CFP), credit counselor, or tax professional who can evaluate your complete financial picture. The strategies presented work best when customized to your specific income level, expense structure, risk tolerance, and long-term financial goals.

This content is designed for educational purposes and general guidance. Your financial success depends on consistent execution, realistic goal-setting, and adaptation of these strategies to your unique circumstances. No guaranteed returns, specific timeline promises, or universal outcomes are implied.

Informational disclaimer

The content on Finance Authority Hub is provided for general informational and educational purposes only and should not be considered personalized financial, investment, tax, legal, or professional advice. Financial decisions depend on your individual goals, income, risk tolerance, location, and regulatory situation. Before acting on any information, strategy, estimate, or calculator result, consult a qualified licensed professional who can evaluate your specific circumstances.